China Data Center Market - Investment Analysis & Growth Opportunities 2026-2031

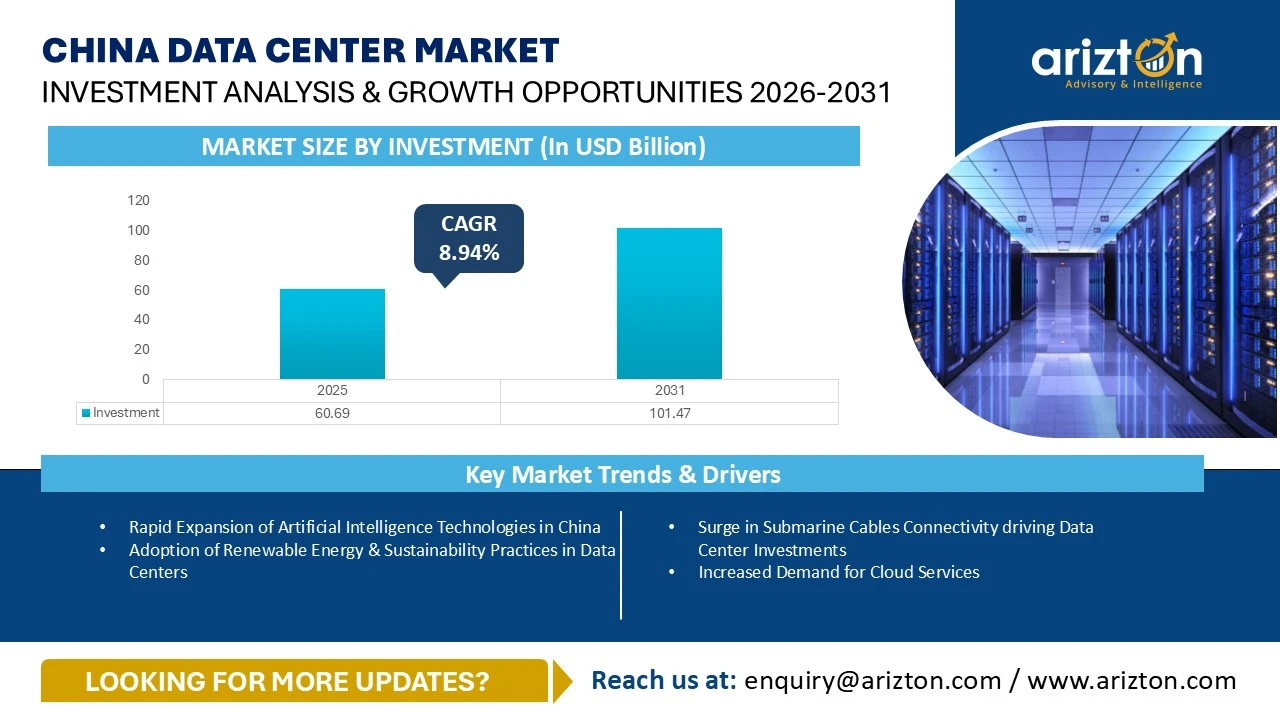

THE CHINA DATA CENTER MARKET SIZE WAS VALUED AT USD 60.69 BILLION IN 2025 AND IS EXPECTED TO REACH USD 101.47 BILLION BY 2031, GROWING AT A CAGR OF 8.94% DURING THE FORECAST PERIOD.

158 pages

84 company

8 segments

1 region

1 countries

Purchase Options

China Data Center Market - Investment Analysis & Growth Opportunities 2026-2031

THE CHINA DATA CENTER MARKET SIZE WAS VALUED AT USD 60.69 BILLION IN 2025 AND IS EXPECTED TO REACH USD 101.47 BILLION BY 2031, GROWING AT A CAGR OF 8.94% DURING THE FORECAST PERIOD.

The China Data Center Market Report Includes Size in Terms of

- Facility Type: Colocation Data Centers, Hyperscale Data Centers, and Enterprise Data Centers

- IT Infrastructure: Servers, Storage Systems, and Network Infrastructure

- Electrical Infrastructure: UPS Systems, Generators, Transfer Switches & Switchgears, PDUs, and Other Electrical Infrastructure

- Mechanical Infrastructure: Cooling Systems, Rack Cabinets, and Other Mechanical Infrastructure

- Cooling Systems: CRAC & CRAH Units, Chiller Units, Cooling Towers, Condensers & Dry Coolers, and Other Cooling Units

- General Construction: Core & Shell Development, Installation & Commissioning Services, Engineering & Building Design, Fire Detection & Suppression Systems, Physical Security, and Data Center Infrastructure Management (DCIM)

- Tier Standard: Tier I & Tier II, Tier III, and Tier IV

- Geography: East China, West China, North China, and South China

Get Insights over 350 Upcoming Facilities across China

This report includes market data points, ranging from trend

analyses to market estimates & forecasts that you can customize

CHINA DATA CENTER MARKET REPORT SCOPE

| REPORT ATTRIBUTE | DETAILS |

|---|---|

| MARKET SIZE (INVESTMENT) | USD 101.47 Billion (2031) |

| MARKET SIZE (AREA) | 16.35 Million Sq. feet (2031) |

| MARKET SIZE (POWER CAPACITY) | 4,420 MW (2031) |

| CAGR - INVESTMENT (2025-2031) | 8.94% |

| HISTORIC YEAR | 2022-2024 |

| BASE YEAR | 2025 |

| FORECAST YEAR | 2026-2031 |

CHINA DATA CENTER MARKET SIZE & OUTLOOK

The China data center market size was valued at USD 60.69 billion in 2025 and is expected to reach USD 101.47 billion by 2031, growing at a CAGR of 8.94% during the forecast period. China is one of the well-established data center markets in the APAC region that is witnessing rapid data center growth year-on-year, fuelled by multiple growth factors, such as, continuous advancements in Artificial Intelligence and Machine Learning, surge in cloud computing adoption, expansion of sub-marine and inland cables, rising demand for digitalization, government support for data centers, strict data regulation laws, adoption of sustainability measures among data center operators and cloud companies, and other growth factors.

Owing to the rapid surge in demand for processing Artificial Intelligence workloads, data center companies are increasing rack power densities and investing to install advanced liquid cooling techniques and the clusters of Graphic Processing Units in their data centers to support Artificial Intelligence workloads efficiently. For instance, in September 2025, Alibaba Group supplied more than 23 thousand domestically manufactured Graphic Processing Units to China Unicom to install in its Xining data center facility in Qinghai province of China. The demand for advanced graphics processing units is slated to increase significantly in the China data center market during the forecast period.

The Cumulative power capacity of China data center market from 2026 to 2031 is anticipated to reach to around 21,600 MW, growing with an absolute growth rate of around 81.15% from 2025 to 2031.

The major cloud service providers like Alibaba Group, Huawei, and others are continuously investing in China to expand their cloud and Artificial intelligence service offerings across the country. For example, in September 2025, Alibaba Group secured a fund of around $3.2 billion to expand the company’s data center, cloud computing and other digital capabilities. The demand for cloud computing services is increasing rapidly across China as the businesses across wide range of industries are shifting their workloads to cloud platforms for better efficiency. For example, in August 2025, the World Aquatics Organization that specializing in organizing water sports competitions, collaborated with Alibaba Group to migrate its core systems to the Alibaba Group’s cloud platform to enhance operational efficiency and boost productivity.

China hosts around 22 Free Trade Zones across multiple provinces, including, Fujian, Guangdong, Henan, Sichuan, Shaanxi, Tianjin, Zhejiang, and other provinces to support enterprises across multiple sectors by offering wide range of advantages for establishing and operating their businesses efficiently across the country. The Free Trade Zones in China offer enterprises, including data center operators with simplified customs and business-registration procedures, financial liberation measures like free-trade accounts and cross-border RMB flexibility, tax incentives for high-tech industries, and other benefits.

China controls personal and sensitive data through several laws, including the Personal Information Protection Law, Data Security Law, and Cybersecurity Law, which sets clear rules on how data should be collected, stored, used, and shared; these laws also give people rights over their personal data and require companies to follow strong security practices, regularly check risks, obtain government approval before sending data outside the country, and report any major data security issues on time.

CHINA DATA CENTER MARKET - KEY HIGHLIGHTS

- The government of China is actively supporting the data center industry by funding domestic technology firms to strengthen local GPU manufacturing and to address the export restrictions imposed by international governments that limit the supply of advanced semiconductors to Chinese companies. In September 2025, Alibaba Group announced the development of a new AI inferencing chip, which will be more flexible compared to its earlier semiconductors.

- China’s AI Plus initiative focuses on accelerating the adoption of artificial intelligence across key sectors such as research, public, finance, and others to boost productivity and drive innovation across the nation. The initiative also aims to strengthen the country’s AI infrastructure and position China as one of the leading global hubs for advanced artificial intelligence development.

- The trend of forming joint ventures and signing Memoranda of Understanding has been increasing in the China data center market to enhance digital capabilities and data center infrastructure across the country. The technology companies and data center operators are collaborating with companies across diverse sectors to develop data centers across multiple locations in China. In July 2025, Nyocor, along with several other companies, announced plans to develop multiple data center facilities in the desert regions of Xinjiang, which will be capable of hosting over 100,000 AI chips. As of December 2024, local authorities in Xinjiang and Qinghai had already approved proposals from various firms to establish around 39 data centers across China

- The Green Data Center Government Procurement Demand Standard requires data center operators in China to maintain high energy efficiency, meaning any data center built after June 2023 should have a Power Usage Effectiveness (PUE) of not more than 1.4, and it also require companies to gradually use more renewable energy, with at least 30% renewable power usage, increasing to 50% by 2027, around 75% by 2030, and eventually reaching close to 100% by 2032.

- As the demand for data center infrastructure is rising significantly, the data center companies are sourcing funds and finances from multiple organizations, financial institutions, and banks to expand data center service offerings. For example, in December 2024, Chindata Group secured a fund of over $490 million from multiple financial institutions to expand digital infrastructure capabilities across China and other nations.

- In China, companies that offer internet-related data center services—such as renting servers, storage, racks, providing bandwidth, or managing IT systems must obtain an Internet Data Center License, as these services involve handling internet access and customer data.

WHY SHOULD YOU BUY THIS RESEARCH?

- Market size available in the investment area, and power capacity

- An assessment of the data center investment in China by colocation, hyperscale, and enterprise operators.

- Data center investments in the area (square feet) and power capacity (MW) across regions in the country.

- A detailed study of the existing China data center market landscape, an in-depth industry analysis, and insightful predictions about the China data center market size during the forecast period.

- Snapshot of upcoming third-party data center facilities in China

- Facilities Identified (Upcoming): 700+

- Coverage: 73+ Provinces

- Upcoming Data Center Location

- Upcoming Data Center Status

- Investment opportunities by facility type (value, area, and power capacity): Colocation data centers, Hyperscale data centers, and Enterprise data centers

- China data center landscape market investments are classified into IT, power, cooling, and general construction services with sizing and forecast.

- A comprehensive analysis of the latest trends, growth rate, potential opportunities, growth restraints, and prospects for the industry.

- Business overview and product offerings of prominent IT infrastructure providers, construction contractors, support infrastructure providers, and investors operating in the industry.

- A transparent research methodology and the analysis of the demand and supply aspects of the market.

CHINA DATA CENTER MARKET VENDOR LANDSCAPE

- The colocation data center companies contribute to generating the majority of the data center investments in China. Some of the prominent colocation companies operating in China include, aofei data international company, @hub, BDx Data Centers, CASIT Information Technology, China Communications Construction Company, Shijiazhuang Changshan Beiming Technology, Chayora, China Datang Corporation, China International Capital Corporation, China Mobile International, China Telecom Corporation, China Unicom, Chindata Group, Deheng Data, Digital Guangxi Group, Dr. Peng Telecom & Media Group, Fujian Douxun Technology, GDS Holdings, Heying Data, Hotwon Network Group, Kehua Tech, Keppel Data Centres, HAILANYUN Technology, Beijing Sinnet Technology, China Three Gorges Corp., Tianjin Jiangtian Data Technology, VNET Group, Zhejiang Hanggang Digital Technology, ZDATA Group, Hefei City Cloud Data Center, Henan Digital Zhongyuan Data, Volcano Cloud (Datong) Technology, and others.

- The country also hosts major cloud service providers such as, Alibaba Group, Baidu, Huawei, and others that operate multiple hyperscale data centers and cloud regions across Beijing, Chengdu, Chongqing, Guangzhou, Guiyang, Nanjing, Shanghai, Ulanqab, Wuhu, Wuhan, and others. The cloud market in China is anticipated to continue witnessing substantial growth during the forecast period. For instance, in September 2025, Alibaba Group planned to obtain a fund of around $3.2 billion to expand its cloud computing and data center service offerings across China.

- China has the presence of global as well as local support infrastructure providers, which supply, support infrastructure for resilient data center operations. Some of the prominent support infrastructure providers in China include, ABB, AIRSYS, Baudouin, Carrier, Caterpillar, Cummins, Delta Electronics, EAST GROUP, Eaton, EVADA (Xiamen) Technology, Fuji Electric, Shenling, HITEC Power Protection, Hongbao Power Supply, INVT Power, Legrand, Mitsubishi Electric, Nanjing Jialitu Data Center Environment Technology, Piller Power Systems, Rittal, Rolls Royce, Schneider Electric, KSTAR, STULZ, Trane, Vertiv, and others.

- The prominent IT infrastructure companies like Cisco, Dell Technologies, Hewlett Packard Enterprise, Huawei Technologies, IBM, Inspur Group, Lenovo, Everpure, Quanta Cloud Technology, Wiwynn, and others supply IT infrastructure, including servers, storage systems, and networking equipment for data centers in China.

- The companies like AECOM, ATS Global, Aurecon, China Electronics Engineering Design Institute, China Railway Construction, China State Construction Engineering Corporation, DSCO Group, MCC Group, Zhejiang Cloud Valley, and others offer wide range of construction, installation, commissioning, and engineering services for the construction of data centers in China.

REPORT COVERAGE:

This report analyses the China data center market share. It elaboratively analyses the existing and upcoming facilities and investments in facility type, IT, electrical, mechanical infrastructure, cooling systems, general construction, and Tier standards. It discusses market sizing and investment estimation for different segments. The segmentation includes:

- Facility Type

- Colocation Data Centers

- Hyperscale Data Centers

- Enterprise Data Centers

- IT Infrastructure

- Server Infrastructure

- Storage Infrastructure

- Network Infrastructure

- Electrical Infrastructure

- UPS Systems

- Generators

- Switches & Switchgears

- PDUs

- Other Electrical Infrastructure

- Mechanical Infrastructure

- Cooling Systems

- Rack Cabinets

- Other Mechanical Infrastructure

- Cooling Systems

- CRAC and CRAH

- Chillers

- Cooling Towers, Condensers and Dry Coolers

- Other Cooling Units

- General Construction

- Core & Shell Development

- Installation & commissioning Services

- Building & Engineering Design

- Fire Detection & Suppression Systems

- Physical Security

- Data Center Infrastructure Management (DCIM)

- Tier Standard

- Tier I & Tier II

- Tier III

- Tier IV

- Geography

- East China

- West China

- North China

- South China

VENDOR LANDSCAPE

- IT INFRASTRUCTURE PROVIDERS: Cisco, Dell Technologies, Hewlett-Packard Enterprise, Huawei Technologies, IBM, Inspur Group, Lenovo, Everpure (Pure Storage), Quanta Cloud Technology (QCT), NVIDIA, and Wiwynn.

- DATA CENTER CONSTRUCTION CONTRACTORS & SUB-CONTRACTORS: AECOM, ATS Global, Aurecon, China Electronics Engineering Design Institute (CEEDI), China Railway Construction, China State Construction Engineering Corporation, DSCO Group, MCC Group, and Zhejiang Cloud Valley.

- SUPPORT INFRASTRUCTURE PROVIDERS: ABB, AIRSYS, Baudouin, Carrier, Caterpillar, Cummins, Delta Electronics, EAST GROUP, Eaton, EVADA (Xiamen) Technology, Fuji Electric, Shenling, HITEC Power Protection, Hongbao Power Supply, INVT Power, Legrand, Mitsubishi Electric, Nanjing Jialitu Data Center Environment Technology, Piller Power Systems, Rittal, Rolls Royce, Schneider Electric, KSTAR, STULZ, Trane, and Vertiv.

- DATA CENTER INVESTORS: Alibaba Group, aofei data international company, @hub, Baidu, BDx Data Centers, Capitalonline Data Service, CASIT Information Technology, China Communications Construction Company Shijiazhuang Changshan Beiming Technology, Chayora, China Datang Corporation, China International Capital Corporation, China Mobile International, China Telecom Corporation, China Unicom, Chindata Group, Deheng Data, Digital Guangxi Group, Dr. Peng Telecom & Media Group, Fujian Douxun Technology, GDS Holdings, Heying Data, Hotwon Network Group, Huawei, Kehua Tech, Keppel Data Centres, HAILANYUN Technology, Beijing Sinnet Technology, Tencent, China Three Gorges Corp., Tianjin Jiangtian Data Technology, VNET Group, Zhejiang Hanggang Digital Technology, ZDATA Group, Hefei City Cloud Data Center, Henan Digital Zhongyuan Data, and Volcano Cloud (Datong) Technology.

SNAPSHOT

The China data center market size is projected to reach USD 101.47 billion by 2031, growing at a CAGR of 8.94% from 2025 to 2031.

The following factors are likely to contribute to the growth of the China data center market

- Surge in Submarine Cables Connectivity driving Data Center Investments

- Increased Demand for Cloud Services

Base Year: 2025

Forecast Year: 2026-2031

The report considers the present scenario of the China data center market and its market dynamics for 2026-2031. It covers a detailed overview of several market growth enablers, restraints, and trends. The study includes the demand and supply aspects of the market.

This report also analyses the China data center market share. It elaborately analyses the existing and upcoming facilities and investments in IT, electrical, mechanical infrastructure, general construction, and tier standards. It discusses market sizing and investment estimation for different segments.

The segmentation includes:

- IT Infrastructure

- Servers

- Storage Systems

- Network Infrastructure

- Electrical Infrastructure

- UPS Systems

- Generators

- Transfer Switches & Switchgears

- PDUs

- Other Electrical Infrastructure

- Mechanical Infrastructure

- Cooling Systems

- Rack Cabinets

- Other Mechanical Infrastructure

- Cooling Systems

- CRAC & CRAH Units

- Chiller Units

- Cooling Towers, Condensers & Dry Coolers

- Other Cooling Units

- General Construction

- Core & Shell Development

- Installation & Commissioning Services

- Engineering & Building Design

- Fire Detection & Suppression Systems

- Physical Security

- Data Center Infrastructure Management (DCIM)

- Tier Standard

- Tier I & Tier II

- Tier III

- Tier IV

- Geography

- East China

- West China

- North China

- South China

VENDOR LANDSCAPE

IT Infrastructure Providers

- Cisco

- Dell Technologies

- Hewlett Packard Enterprise

- Huawei Technologies

- IBM

- Inspur Group

- Lenovo

- Pure Storage (Everpure)

- Quanta Cloud Technology (QCT)

- NVIDIA

- Wiwynn

Data Center Construction Contractors & Sub-Contractors

- AECOM

- ATS Global

- Aurecon

- China Electronics Engineering Design Institute (CEEDI)

- China Railway Construction Corporation

- China State Construction Engineering Corporation

- DSCO Group

- MCC Group

- Zhejiang Cloud Valley

Support Infrastructure Providers

- ABB

- AIRSYS

- Baudouin

- Carrier

- Caterpillar

- Cummins

- Delta Electronics

- EAST Group

- Eaton

- EVADA (Xiamen) Technology

- Fuji Electric

- Shenling

- HITEC Power Protection

- Hongbao Power Supply

- INVT Power

- Legrand

- Mitsubishi Electric

- Nanjing Jialitu Data Center Environment Technology

- Piller Power Systems

- Rittal

- Rolls-Royce

- Schneider Electric

- KSTAR

- STULZ

- Trane

- Vertiv

Data Center Investors

- Alibaba Group

- Aofei Data International Company

- @hub

- Baidu

- BDx Data Centers

- Capitalonline Data Service

- CASIT Information Technology

- China Communications Construction Company

- Shijiazhuang Changshan Beiming Technology

- Chayora

- China Datang Corporation

- China International Capital Corporation

- China Mobile International

- China Telecom Corporation

- China Unicom

- Chindata Group

- Deheng Data

- Digital Guangxi Group

- Dr. Peng Telecom & Media Group

- Fujian Douxun Technology

- GDS Holdings

- Heying Data

- Hotwon Network Group

- Huawei

- Kehua Tech

- Keppel Data Centres

- Hailanyun Technology

- Beijing Sinnet Technology

- Tencent

- China Three Gorges Corporation

- Tianjin Jiangtian Data Technology

- VNET Group

- Zhejiang Hanggang Digital Technology

- ZDATA Group

- Hefei City Cloud Data Center

- Henan Digital Zhongyuan Data

- Volcano Cloud (Datong) Technology

CHINA DATA CENTER MARKET FAQs

How much MW of power capacity will be added across China during 2026-2031?

How big is the China data center market?

What factors are driving China data center market?

Which all geographies are included in China center market report?

For more details, please reach us at [email protected]

1. CHAPTER 1: INVESTMENT OPPORTUNITIES IN CHINA

• Microeconomic & Macroeconomic Factors for China Market

• Impact of AI on Data Center Industry in China

• Investment Opportunities in China

• Government Rules & Regulations for Data Centers

• Market Investment by Area

• Market Investment by Power Capacity

2. CHAPTER 2: INVESTMENT BY FACILITY TYPE

• Facility Type by Investment

• Facility Type by Area

• Facility Type by Power Capacity

3. CHAPTER 3: MARKET DYNAMICS

• Market Enablers

• Market Trends

• Market Restraints

4. CHAPTER 4: MARKET SEGMENTATION

• IT Infrastructure: Market Size & Forecast

• Electrical Infrastructure: Market Size & Forecast

• Mechanical Infrastructure: Market Size & Forecast

• General Construction: Market Size & Forecast

• Construction Cost Break-up

5. CHAPTER 5: TIER STANDARDS INVESTMENT

• Tier I & II

• Tier III

• Tier IV

6. CHAPTER 6: GEOGRAPHY EGMENTATION

• East China

• West China

• North China

• South China

7. CHAPTER 7: KEY MARKET PARTICIPANTS

• IT Infrastructure Providers

• Construction Contractors & Sub-Contractors

• Support Infrastructure Providers

• Data Center Investors

8. CHAPTER 8: APPENDIX

• Market Derivation

• Site Selection Criteria

• Quantitative Summary

• Abbreviations

Select a license type that suits your business needs

Single User Licence

- Report accessible by one user only

- Free 10% or 3 days of customization

- Free post-sale service assistance

- Continuous support through email

5 User Licence

- Report accessible by 5 users within the organization

- Free 15% or 4.5 days of customization

- Continuous support through email and telephone

- Free analyst hour

- Free Upgrade: If an updated report published within 180 days of purchase, you will get the revised report free of charge

Corporate Licence

- Free Datasheet worth $1500

- Report accessible by the entire organization

- Free 20% or 6 days of customization

- Free post-sale service assistance

- Continuous support through email and telephone

- Direct access to lead analysts

- Free analyst hour

- Free Upgrade: If an updated report published within 180 days of purchase, you will get the revised report free of charge

Datasheet Licence

- Report accessible by 1 user only

- Free 15% or 32 hours of customization

- Free post-sale service assistance

- Direct access to lead analysts

Frequently Asked Questions

How much MW of power capacity will be added across China during 2026-2031?

How big is the China data center market?

What factors are driving China data center market?

Which all geographies are included in China center market report?

Other RELATED Reports

India Data Center Market - Investment Analysis & Growth Opportunities 2026-2031

Published : January 2026

Japan Data Center Market - Investment Analysis & Growth Opportunities 2026-2031

Published : January 2026

Thailand Data Center Market – Investment Analysis & Growth Opportunities 2026-2031

Published : January 2026

Indonesia Data Center Market – Investment Analysis & Growth Opportunities 2026-2031

Published : January 2026