Latin America Data Center Market Landscape 2026-2031

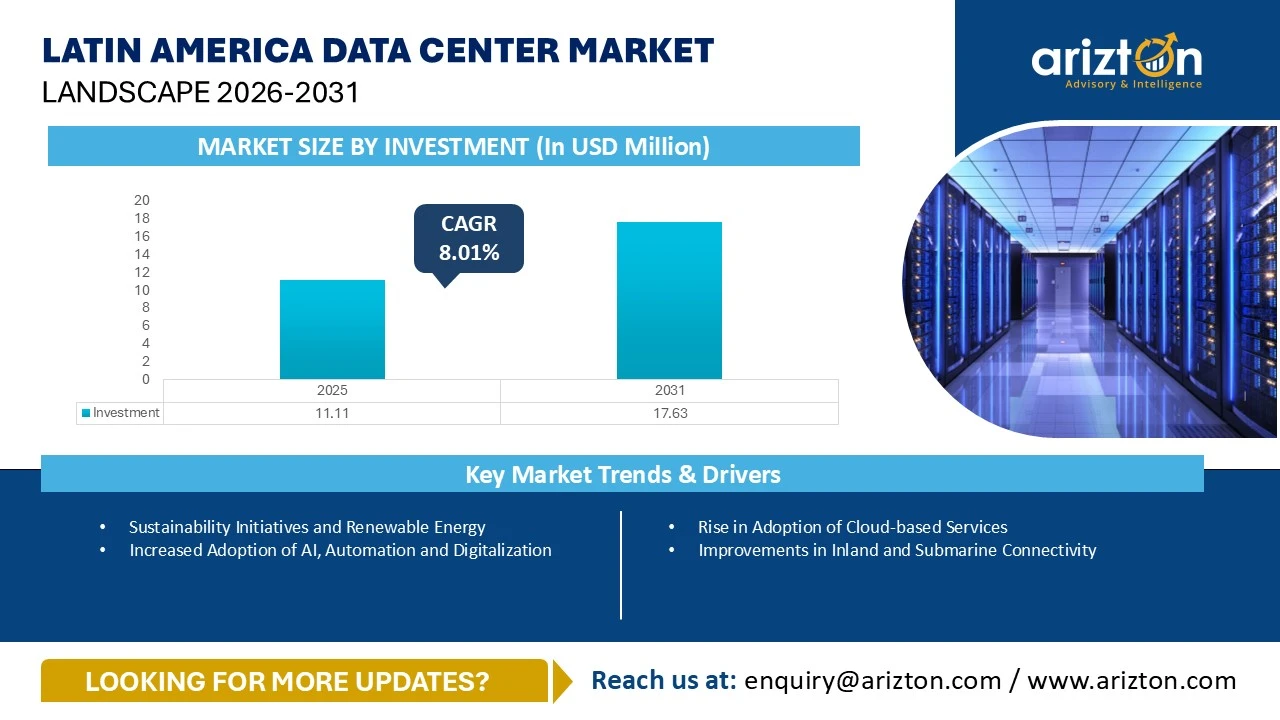

THE LATIN AMERICA DATA CENTER MARKET SIZE WITNESSED INVESTMENTS OF USD 11.11 BILLION IN 2025 AND WILL WITNESS INVESTMENTS OF USD 17.63 BILLION BY 2031, GROWING AT A CAGR OF 8.01% DURING THE FORECAST PERIOD.

Latin America Data Center Market Growth Insights – Market Area to Reach 2.13 Million Sq. Ft. and Power Capacity to Exceed 536 MW by 2031, Driven by Cloud Adoption, Edge Computing Expansion, and Rising AI, Big Data & IoT Deployments Across the Region (2026–2031)

Published Date : June 2026

Last Updated : July 2026

format: PDF

edition : Fourth Edition

219 pages

114 company

9 segments

1 region

6 countries

Purchase Options

Latin America Data Center Market Landscape 2026-2031

THE LATIN AMERICA DATA CENTER MARKET SIZE WITNESSED INVESTMENTS OF USD 11.11 BILLION IN 2025 AND WILL WITNESS INVESTMENTS OF USD 17.63 BILLION BY 2031, GROWING AT A CAGR OF 8.01% DURING THE FORECAST PERIOD.

The Latin America Data Center Market Size, Share, & Trends Analysis By

- Infrastructure: IT Infrastructure, Electrical Infrastructure, Mechanical Infrastructure, and General Construction

- IT Infrastructure: Server Infrastructure, Storage Infrastructure, and Network Infrastructure

- Electrical Infrastructure: UPS Systems, Generators, Transfer Switches & Switchgear, PDUs, and Other Electrical Infrastructure

- Mechanical Infrastructure: Cooling Systems, Racks, and Other Mechanical Infrastructure

- Cooling Systems: CRAC & CRAH Units, Chiller Units, Cooling Towers, Condensers, Dry Coolers, and Other Cooling Units

- Cooling Techniques: Air-based and Liquid-based

- General Construction: Core & Shell Development, Installation & Commissioning Services, Engineering & Building Design, Physical Security, Fire Detection & Suppression, and DCIM

- Tier Standard: Tier I & II, Tier III, and Tier IV

- Geography: Brazil, Chile, Mexico, Colombia, Argentina, and the Rest of Latin America

Industry Analysis Report, Regional Outlook, Growth Potential, Price Trends, Competitive Market Share & Forecast 2026–2031.

This report includes market data points, ranging from trend

analyses to market estimates & forecasts that you can customize

LATIN AMERICA DATA CENTER MARKET REPORT SCOPE

| REPORT ATTRIBUTE | DETAILS |

|---|---|

| MARKET SIZE – INVESTMENT (2031) | USD 17.63 Billion |

| MARKET SIZE – INVESTMENT (2025) | USD 11.11 Billion |

| CAGR - INVESTMENT (2025-2031) | 8.01% |

| MARKET SIZE - AREA (2031) | 2.13 Million Square feet |

| POWER CAPACITY (2031) | 536 MW |

| HISTORIC YEAR | 2022-2024 |

| BASE YEAR | 2025 |

| SEGMENTS BY | Infrastructure, IT Infrastructure, Electrical Infrastructure, Mechanical Infrastructure, Cooling Systems, Cooling Techniques, General Construction, Tier Standard, Geography |

| GEOGRAPHIC ANALYSIS | Brazil, Mexico, Chile, Colombia, Argentina, and Rest of Latin America |

LATIN AMERICA DATA CENTER MARKET SIZE & INSIGHTS

The Latin America data center market size witnessed investments of USD 11.11 billion in 2025 and will witness investments of USD 17.63 billion by 2031, growing at a CAGR of 8.01% during the forecast period. The Latin American data center market continues to experience rapid global growth, driven by increasing cloud adoption, the expansion of edge computing, and the growing deployment of technologies such as AI, big data, and the IoT.

Brazil holds a significant share of the market in the data center growth of Latin America. The digital transformation policies of the country, coupled with the widespread adoption of IoT and Big Data, support major investments in data center infrastructure. In September 2025, Alibaba Cloud announced plans to launch its first data center in Brazil as part of a broader global expansion across eight locations. The investment supports rising demand for AI-driven cloud services and strengthens the role of Brazil in the international cloud infrastructure network of Alibaba.

The average cost of constructing a data center in Latin America typically ranges from $7 million to $10 million per megawatt (MW), depending on the location. These high costs are influenced by various factors, including limited land availability, elevated labor rates, inflation, and access to power. As a result, operators are exploring markets that offer lower construction costs, abundant power and land, and favorable regulatory environments, making these locations more appealing for cost-efficient development.

Chile is increasingly establishing itself as a leading destination for data center investments in South America, supported by its strategic geographical position, strong digital infrastructure, and supportive government policies. In January 2024, AWS secured approval for a $205 million data center project in Santiago, the first cloud campus of the company in the country, with construction of the first building scheduled for completion in April 2025 and the second by 2028.

Colombia is the fourth-largest economy in Latin America, playing an important role in the expansion of data centers across the region. In August 2025, Colombia launched ACOLDC, the Colombian Association of Data Centers and Data Technology, a non-profit organization that brings together key companies in the data center industry of Colombia.

LATIN AMERICA DATA CENTER MARKET KEY TRENDS

Sustainability Initiatives and Renewable Energy

- The Latin American data center market is witnessing a growing emphasis on sustainable infrastructure and clean energy adoption, driven by supportive government initiatives and corporate decarbonization goals. Several countries in the region are promoting renewable energy integration, carbon reduction strategies, and energy-efficient digital ecosystems, creating favorable conditions for the expansion of green hyperscale and colocation data centers.

- In October 2025, Amazon Brazil partnered with Petrobras to explore the use of certified low-carbon fuels in its logistics operations, supporting the goal of achieving net-zero carbon emissions by 2040. The collaboration aims to decarbonize transportation in Brazil while strengthening the leadership of the country in biofuels, waste-based energy, and sustainable logistics solutions.

- The combination of renewable energy expansion, supportive government policies, and sustainability-focused investments strengthens the position of Latin America as an attractive destination for green data center development. These initiatives are expected to accelerate the adoption of low-carbon power, energy-efficient technologies, and environmentally responsible digital infrastructure across the region.

Increased Adoption of AI, Automation and Digitalization

- Brazil has placed strong emphasis on AI as a driver of future growth. The AI Strategy of the country seeks to stimulate investment in R&D, foster a robust AI ecosystem, encourage the international positioning of Brazilian AI solutions, and reduce barriers to innovation, while also promoting the responsible use of AI through workforce education. Building on this vision, Brazil introduced its National AI Plan in 2024, committing around $4 billion to support business innovation projects and expand AI-related infrastructure and capabilities. By 2025, internet penetration in Brazil had surpassed 86.5%, translating to more than 184 million users nationwide.

- Colombia continues to enter a new phase of digital maturity, and AI is at the forefront of this transformation. The Colombian government is actively pushing the adoption of AI across several sectors by establishing AI research centers, funding AI startups, and implementing AI-driven solutions in public services. Its National Public Policy on AI, approved through CONPES, aims to position AI as a catalyst for sustainable development and economic transformation by 2030. Supported by a budget of $116 million, the policy focuses on strengthening governance, digital talent, technological infrastructure, and ethical AI adoption.

- Chile is increasingly positioning itself as a regional center for digital innovation and emerging technologies, driven by a strong tech ecosystem and forward-thinking government policies. Government initiatives such as the Digital Transformation Strategy 2035 emphasise improving digital skills, strengthening cybersecurity frameworks, and enhancing technology-enabled public services. Active measures to attract global tech partnerships are further elevating the position of Chile as a regional innovation powerhouse.

LATIN AMERICA DATA CENTER MARKET SEGMENTATION INSIGHTS

- Server infrastructure in Latin America data center market is a rapidly evolving segment, driven by digital transformation, increasing internet penetration, and the need for cloud services in the region. Petrobras has deployed its first AI–focused supercomputer in Brazil, known as Tatu, which is built on 224 NVIDIA GPUs with 80 GB of memory each, distributed across 11 racks within a 7.4-meter equipment row. The region’s data storage infrastructure is transitioning from traditional storage systems to modern Software-Defined Storage (SDS) and HCI, offering better scalability and flexibility

- The electrical infrastructure is witnessing several innovations in the UPS systems, generators, transfer switches & switchgears and other electrical equipment. Some of these innovations include HVO fuel for generator sets, which reduces emissions as a measure to curb emissions.

- Additionally, several innovative UPS batteries, such as Nickel-Zinc (NiZn) and Sodium-Ion batteries, are gaining traction in the market due to their high-power density, safety, sustainability, and other factors.

- Liquid cooling is becoming a significant trend that major colocation operators are implementing in their data center facilities. It is emerging as a key differentiator for colocation providers as AI and compute-intensive workloads continue to grow. Companies like ODATA (Aligned Data Centers), Scala Data Centers, Ascenty and several others are leading the way by offering scalable and energy-efficient solutions that can support the increasing demands of high-performance computing.

LATIN AMERICA DATA CENTER MARKET GEOGRAPHICAL ANALYSIS:

- In the Latin America data center market, Brazil is expected to be the largest market in 2031 in terms of power capacity, with a share of around 36% in 2031. In September 2025, DataSpots secured key network access approvals from Brazil’s national grid operator for three planned data center projects across São Paulo, Rio de Janeiro, and Paraná, unlocking a combined investment of roughly about $2.7 billion (R$15 billion) and advancing development of major digital infrastructure in those states.

- The long-term energy strategy of Chile includes achieving carbon neutrality by 2050 and converting a significant portion of coal-fired units by the end of 2025 under the Ministry of Energy’s Decarbonization Plan. In January 2025, ODATA signed a 100% renewable PPA with Atlas Renewable Energy to supply the full energy requirements of its 28MW ST01 data center in Chile, using power from Atlas’s 1.5GW solar and storage portfolio. This agreement supports the aim of ODATA to run all Chilean operations on renewable energy and strengthen its sustainability commitments.

- Mexico holds a significant share of the Latin American data center market growth. In February 2026, Terranova, the hyperscale data center platform backed by the Actis infrastructure fund, launched its first facility in Mexico, officially beginning operations in the country as part of a broader $1.5 billion investment plan to develop large-scale campuses across Brazil, Mexico, and Chile over the next three years, with additional markets also under evaluation for future expansion.

- The cost of developing a data center facility in Colombia ranges between $7 and $8 million per MW. However, these figures are expected to increase annually due to various factors, including supply chain disruptions, inflation, and rising interest rates.

- Beyond Argentina, Chile, Brazil, Mexico, and Colombia, investments are also expanding into other Latin American markets. In February 2026, Google announced a $500 million investment to develop a new international digital exchange hub (“Digital Port”) in the Dominican Republic, marking its first such facility in Latin America outside the US. The project also includes new submarine cable connections to the US, significantly enhancing regional connectivity and positioning the country as a strategic digital gateway across the Americas.

LATIN AMERICA DATA CENTER MARKET VENDOR LANDSCAPE

- The Latin America data center market has the presence of key investors such as Actis, Ascenty, AWS, Cirion Technologies, Claro, EdgeConneX, Elea Data Centers, EMPATEL SAPEM, Equinix, Etix Everywhere, G2K, Google, GTD, HostDime, Iplan, IPXON Networks, KIO Data Centers, Microsoft, ODATA (Aligned Data Centers), OneX Data Center, Quantico Data Center, Scala Data Centers, Takoda Data Centers, Tecto Data Centers, Telecentro Empresas and others.

- Mergers & Acquisitions is growing in the LATAM data center industry because it is the fastest and most effective way to acquire capacity, secure power, and scale globally in response to the explosive demand for AI and cloud infrastructure. For instance, in April 2025, Alianza Investimentos Imobiliários, the Brazilian investment company, formed a data center joint venture with GIC, the Singaporean wealth fund, to jointly invest approximately $338 million to develop multiple data centers in Brazil.

- New Entrants include 247 Data Centers, Ada Infrastructure, Atlantic Data Centers, Ava Telecom, CloudHQ, Fermaca Networks, Layer 9 Data Centers, MDC Data Centers, OpenAI & Sur Energy, Surfix Data Center, Terranova, TECfusions and several others.

- Various well-known companies like Google, Microsoft, AWS, Meta, and Apple are investing in this region. For instance, in February 2026, Google announced a $500 million investment to develop a new international digital exchange hub (“Digital Port”) in the Dominican Republic, marking its first such facility in Latin America outside the US. The project also includes new submarine cable connections to the US, significantly enhancing regional connectivity and positioning the country as a strategic digital gateway across the Americas.

SNAPSHOT

The Latin America data center construction market size by investment will reach USD 11.39 billion by 2031, growing at a CAGR of 25.79% from 2025 to 2031.

The following factors are likely to contribute to the growth of the Latin America data center construction market during the forecast period:

- Rise in Adoption of Cloud-based Services

- Improvements in Inland and Submarine Connectivity

- Big Data and IoT Investments Driving the Data Center Market

Base Year: 2025

Forecast Year: 2026-2031

The study considers the present scenario of the Latin America data center construction market and its market dynamics for 2026−2031. It covers a detailed overview of several market growth enablers, restraints, and trends. The report offers both the demand and supply aspects of the market. It profiles and examines leading companies and other prominent ones operating in the market.

Segmentation by Infrastructure

- IT Infrastructure

- Electrical Infrastructure

- Mechanical Infrastructure

- General Construction

Segmentation by IT Infrastructure

- Server Infrastructure

- Storage Infrastructure

- Network Infrastructure

Segmentation by Electrical Infrastructure

- UPS Systems

- Generators

- Transfer Switches & Switchgear

- PDUs

- Other Electrical Infrastructure

Segmentation by Mechanical Infrastructure

- Cooling Systems

- Racks

- Other Mechanical Infrastructure

Segmentation by Cooling Systems

- CRAC & CRAH Units

- Chiller Units

- Cooling Towers, Condensers, and Dry Coolers

- Other Cooling Units

Segmentation by Cooling Techniques

- Air-based

- Liquid-based

Segmentation by General Construction

- Core & Shell Development

- Installation & Commissioning Services

- Engineering & Building Design

- Physical Security

- Fire Detection & Suppression

- DCIM

Segmentation by Tier Standard

- Tier I & II

- Tier III

- Tier IV

Segmentation by Geography

- Latin America

- Brazil

- Mexico

- Chile

- Colombia

- Argentina

- Rest of Latin America

VENDOR LANDSCAPE

Key Data Center IT Infrastructure Providers

- Arista Networks

- Business Overview

- Service Offerings

- Broadcom

- Cisco Systems

- Dell Technologies

- Hewlett Packkard Enterprice

- Huawei Technologies

- IBM

- Lenovo

- NetApp

- NVIDIA

- Oracle

- Pure Storage

- Super Micro Computer

Key Data Center Support Infrastructure Providers

- ABB

- Business Overview

- Service Offerings

- Alfa Laval

- ASSA ABLOY

- Axis Communications

- Bosch

- Bruno Generators

- Caterpillar

- Cummins

- Daikin Applied

- Delta Electronics

- Detroit Diesel

- Eaton

- Generac Power Systems

- Honeywell

- Johnson Controls

- KOHLER

- Legrand

- Mitsubishi Electric

- Munters

- Narada

- Panduit

- Piller Power Systems

- Rittal

- Rolls-Royce

- Schneider Electric

- Siemens

- STULZ

- Vertiv

Key Data Center Contractors & Subcontractors

- AECOM

- Business Overview

- Service Offerings

- Aceco TI

- Afonso França Engenharia

- Constructora Sudamericana

- Datawaves

- DLR Group

- Fluor Corporation

- Gensler

- Grupo PML

- Hyphen

- Jacobs Engineering

- KMD Architects

- Mendes Holler Engineering

- Micrico

- Modular Data Centers

- PQC

- Quark

- Racional Engenharia

- Soben

- Syska Henessey Group

- The Weitz Company

- Turner & Townsend

- Turner Construction

- Zeittec

- ZFB Group

Key Data Center Investors

- Actis (NextStream)

- Business Overview

- Service Offerings

- Angola Cables

- Ascenty

- Amazon Web Services

- Cirion Technologies

- Claro

- DHAmericas

- Edge Uno

- EdgeConneX

- Elea Data Centers

- EMPATEL SAPEM

- Equinix

- Etix Everywhere

- EVEO

- G2K

- GlobeNet International Corp

- GTD

- HostDime

- Iplan

- IPXON Networks

- Internexa

- KIO Data Centers

- Mexico Telecom Partners

- Microsoft

- NetGlobalis

- ODATA (Aligned Data Centers)

- OneX Data Center

- PowerHost

- Quantico Data Center

- Scala Data Centers

- SONDA

- Takoda Data Centers

- Tecto Data Centers

- Telecentro Empresas

- Telecom Argentina

New Entrants

- 247 Data Centers

- Business Overview

- Service Offerings

- Ada Infrastructure

- Atlantic Data Centers

- Ava Telecom

- CloudHQ

- Fermaca Networks

- Layer 9 Data Centers

- MDC Data Centers

- OpenAI & Sur Energy

- Surfix Data Center

- Terranova

- TECfusions

LATIN AMERICA DATA CENTER MARKET FAQ's

What is the growth rate of the Latin America data center market?

How big is the Latin America data center market?

What is the estimated market size in terms of area in the Latin America data center market by 2030?

What are the key trends in the Latin America data center market?

How much MW of power capacity is expected to reach the Latin America data center market by 2030?

For more details, please reach us at [email protected]

For more details, please reach us at [email protected]

Select a license type that suits your business needs

Single User Licence

- Report accessible by one user only

- Free 10% or 3 days of customization

- Free post-sale service assistance

- Continuous support through email

5 User Licence

- Report accessible by 5 users within the organization

- Free 15% or 4.5 days of customization

- Continuous support through email and telephone

- Free analyst hour

- Free Upgrade: If an updated report published within 180 days of purchase, you will get the revised report free of charge

Corporate Licence

- Free Datasheet worth $1500

- Report accessible by the entire organization

- Free 20% or 6 days of customization

- Free post-sale service assistance

- Continuous support through email and telephone

- Direct access to lead analysts

- Free analyst hour

- Free Upgrade: If an updated report published within 180 days of purchase, you will get the revised report free of charge

Datasheet Licence

- Report accessible by 1 user only

- Free 15% or 32 hours of customization

- Free post-sale service assistance

- Direct access to lead analysts

Frequently Asked Questions

What is the growth rate of the Latin America data center market?

How big is the Latin America data center market?

What is the estimated market size in terms of area in the Latin America data center market by 2030?

What are the key trends in the Latin America data center market?

How much MW of power capacity is expected to reach the Latin America data center market by 2030?

Other RELATED Reports

Latin America Data Center Colocation Market - Industry Outlook and Forecast 2024-2029

Published : November 2024