Europe Doors & Windows Market Research Report 2026–2031

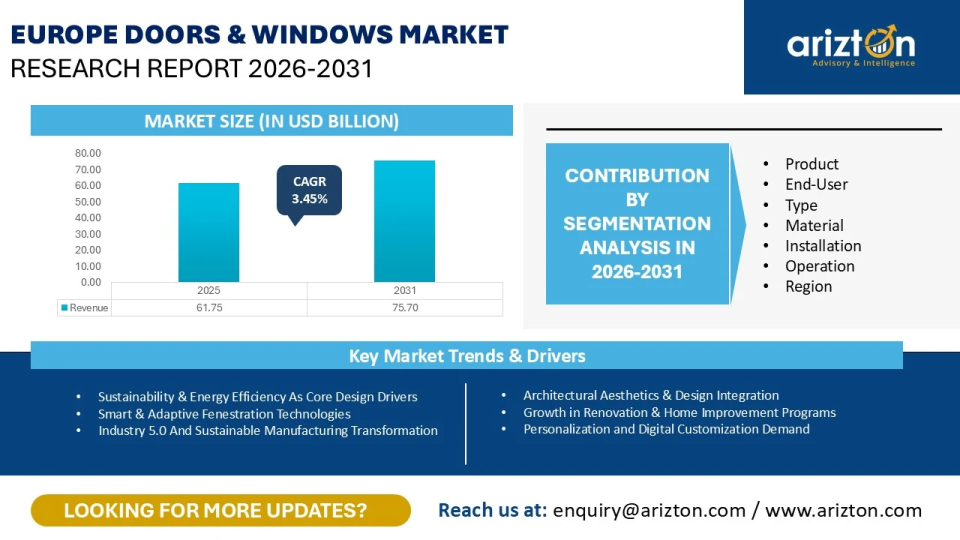

EUROPE DOORS AND WINDOWS MARKET WAS VALUED AT USD 61.75 BILLION IN 2025 AND IS PROJECTED TO REACH USD 75.70 BILLION BY 2031, GROWING AT A CAGR OF 3.45% FROM 2025 TO 2031.

The Europe Doors & Windows Market Size, Share, & Trends By Product, By End-User, By Type, By Material, By Installation, By Operation, & By Region. This Industry Analysis Covers The Market Size (in USD Billion) For The Above Segments.

Published Date : February 2026

Last Updated : May 2026

format: PDF

edition : Third Edition

530 pages

50 company

07 segments

1 region

13 countries

Purchase Options

Europe Doors & Windows Market Research Report 2026–2031

EUROPE DOORS AND WINDOWS MARKET WAS VALUED AT USD 61.75 BILLION IN 2025 AND IS PROJECTED TO REACH USD 75.70 BILLION BY 2031, GROWING AT A CAGR OF 3.45% FROM 2025 TO 2031.

The Europe Doors & Windows Market Size, Share, & Trends Analysis Report By

- Product: Doors and Windows

- End-User: Residential and Non-Residential

- Type: Interior and Exterior

- Material: Plastic & Glass, Wood, Metal, Composite, and Others

- Installation: Replacement and New Construction

- Operation: Manual and Automatic

- Region: Germany, UK, Italy, France, Spain, Netherlands, Poland, Sweden, Belgium, Norway, Switzerland, Denmark, and Finland

Industry Analysis Report, Regional Outlook, Growth Potential, Price Trends, Competitive Market Share & Forecast 2026–2031.

This report includes market data points, ranging from trend

analyses to market estimates & forecasts that you can customize

EUROPE DOORS AND WINDOWS MARKET REPORT SCOPE

| REPORT ATTRIBUTE | DETAILS |

|---|---|

| MARKET SIZE (2031) | USD 75.70 Billion |

| MARKET SIZE (2025) | USD 61.75 Billion |

| CAGR (2025-2031) | 3.45% |

| MARKET SIZE (UNIT SHIPMENT) | 156.41 Million Units (2031) |

| HISTORIC YEAR | 2022-2024 |

| BASE YEAR | 2025 |

| FORECAST YEAR | 2026-2031 |

| SEGMENTS BY | Product, End User, Type, Material, Installation, Operation, and Region |

| REGIONAL ANALYSIS | Germany, UK, Italy, France, Spain, Netherlands, Poland, Sweden, Belgium, Norway, Switzerland, Denmark, and Finland |

| KEY PLAYERS | VKR Holding, JELD-WEN, Schüco International, Internorm, Inwido, and VEKA |

EUROPE DOORS & WINDOWS MARKET SIZE ANALYSIS

Europe doors and windows market size was valued at USD 61.75 billion in 2025 and is projected to reach USD 75.70 billion by 2031, growing at a CAGR of 3.45% during the forecast period. The market demand is supported by steady new construction activity and a structurally large replacement base across residential and non-residential buildings. Ageing housing stock, rising energy costs, and higher efficiency expectations continue to sustain replacement cycles across both mature and emerging European markets.

Europe doors and windows market unit shipments are expected to reach around 156.41 million units by 2031. Doors and windows represent a critical performance layer within the building envelope, as they have a direct impact on heat retention, air leakage, and indoor comfort. The market is moving away from standard products toward high-performance glazing, insulated frames, and improved sealing systems. Specification decisions increasingly prioritize thermal performance, durability, and long-term energy savings rather than initial product cost.

Renovation-driven demand is being reinforced by EU-level policy. The EU Renovation Wave targets the renovation of around 35 million buildings by 2030 and aims to double annual energy renovation rates. Doors and windows are among the most frequently specified upgrade components in renovation programs due to their high impact on energy performance and relatively short installation timelines.

Product innovation and construction practices are reshaping competitive dynamics. Manufacturers are expanding the use of recycled aluminium, certified timber, advanced PVC profiles, warm-edge spacers, and low-emissivity coatings to meet stricter sustainability and performance requirements. In parallel, the rise of prefabricated and modular construction in Northern and Western Europe, including around 45% of new housing in Sweden delivered through off-site manufacturing, is increasing demand for factory-fitted, airtight window and door systems with consistent quality and compliance.

IMPACT OF US & CHINA TRADE WAR

Trade policy shifts in 2025 have increased cost volatility across the Europe doors and windows value chain, particularly for systems with high metal content and cross-border exposure. US Section 232 tariffs on steel and aluminum, including derivative products, raised landed costs for aluminum frames, facade systems, hardware, and fittings commonly used in commercial and premium residential applications. This tightened pricing headroom for export-oriented European manufacturers and increased margin pressure on projects with US exposure.

At the same time, broader tariff uncertainty affecting China- and India-linked inputs has complicated sourcing for hardware, fasteners, motors, sensors, and control components increasingly embedded in automated and smart doors and windows. Temporary easing under the US–China tariff treaty improved short-term procurement visibility, while the US–India tariff escalation forced mid-cycle cost resets and supplier reassessment. For European players, these shifts are reinforcing regional sourcing, material substitution, and tighter supplier qualification to protect compliance, lead times, and project delivery reliability.

Also, read: Global Windows Market. Analysis, 2031

EUROPE DOORS & WINDOWS MARKET TRENDS & DRIVERS

- Sustainability is reshaping product design in Europe’s doors and windows industry. Suppliers are increasing the use of recycled or responsibly sourced inputs such as wood, aluminum, and composites to reduce embodied impact and improve circularity. The EU’s Ecodesign for Sustainable Products Regulation strengthens this direction by pushing higher expectations on durability, recyclability, and overall product sustainability placed on the EU market.

- Energy performance is accelerating the adoption of advanced glazing and insulated system designs. Triple glazing and vacuum-insulated glazing are increasingly used to improve thermal insulation and indoor comfort, while also supporting quieter interiors. This innovation tailwind aligns with the recast Energy Performance of Buildings Directive, which tightens requirements for new buildings to move toward zero-emission standards with clear implementation timelines.

- Home improvement and retrofit activity is expanding faster than many new-build segments, making replacement demand a structural growth engine. The European Commission’s Renovation Wave targets a major step-up in renovation volumes and aims to at least double the annual rate of energy renovations by 2030. This directly supports demand for higher-efficiency windows and doors in ageing housing stock.

- Regulation is also raising the limit on construction product compliance and market transparency. The revised Construction Products Regulation (EU) 2024/3110 sets updated rules for products placed on the EU market, with applicability beginning in January 2026. In parallel, EU-backed one-stop shop renovation models and regional pilots, including activity in Valencia, are improving guidance and financing access for upgrades.

INDUSTRY RESTRAINTS

- In recent years, elevated interest rates and high building costs have reduced the urge for new residential and commercial projects across Europe, weakening new-build demand for doors and windows. Industry bodies also point to a contraction in EU construction investment in 2024 and continued flexibility into 2025. Even where renovation programs support demand, manufacturers face volume risk in new construction pipelines.

- Cost volatility remains a structural restraint because doors and windows depend heavily on energy-intensive inputs and processes. Aluminum, glass production, and PVC extrusion are sensitive to power and gas price swings, which compress margins when contracts are fixed and procurement delays. This is amplified for smaller fabricators with limited ability to manage input-price risk, forcing frequent price resets and delaying purchase decisions.

EUROPE DOORS & WINDOWS MARKET SEGMENTATION INSIGHTS

INSIGHT BY PRODUCT

The Europe doors and windows market by product is segmented into doors and windows. The window segment accounted for the largest market share of over 55% in 2025. The window segment plays a central role in Europe’s transition toward low-emission and energy-efficient buildings, as it directly influences daylight penetration, heat retention, and ventilation efficiency. As a result, window replacement has emerged as one of the most effective interventions under Europe’s broader renovation and decarbonisation strategies.

Renovation activity across Western and Northern Europe continues to dominate demand, supported by governments strengthening building-envelope requirements under the recast Energy Performance of Buildings Directive. These regions account for the largest share of the installed window stock, driven by high renovation intensity and widespread access to public incentive programs.

Within this environment, product differentiation is increasingly shaped by proprietary system design and performance-led engineering rather than aesthetic variation alone. For example, Schüco differentiates its aluminum window portfolio through the AWS 75.SI+ system, which combines high thermal insulation with precision profile engineering to meet stringent European energy standards. Similarly, Reynaers Aluminum reinforces its competitive positioning through the MasterLine 8 platform, engineered for high airtightness, durability, and architectural flexibility across residential and mixed-use applications.

INSIGHT BY END-USER

Based on the end-user, the residential segment holds the largest Europe doors and windows market share. Residential demand is driven by a combination of new housing supply and sustained refurbishment activity, with the segment projected to grow at a CAGR of 2.98% in volume. While new construction contributes to incremental demand, the residential market is structurally supported by upgrades aimed at improving building performance and comfort, which continue to drive replacement volumes across Europe. This is reflected in large-scale residential refurbishment initiatives such as Germany’s WBS 70 prefabricated housing renovation programmes, the UK’s Social Housing Decarbonization Fund–backed retrofit projects, and France’s MaPrimeRenovv residential renovation scheme, all of which typically include window and door replacement as part of envelope upgrades.

Renovation-led demand is particularly pronounced in Spain, Italy, Portugal, and Greece, where refurbishment accounts for most installations. In parallel, government-supported housing programs in countries such as Germany and France, partly linked to demographic pressures, are supporting demand for cost-efficient door and window solutions. These programs increasingly favour plastic systems due to their balance of affordability, durability, and thermal performance compared with wood and metal alternatives.

INSIGHT BY TYPE

Based on the type, the exterior segment accounted for the largest Europe doors and windows market share. Exterior doors and windows form the backbone of Europe’s architectural envelope and play a decisive role in building energy performance, accounting for a significant share of façade-related efficiency gains in both new construction and renovation projects. Market strength in this segment is driven by advancements in high-performance glazing systems, insulated frame profiles, and automation technologies that balance visual transparency with effective thermal control.

Within this landscape, exterior doors are increasingly evolving toward enhanced functionality and climate resilience. Materials such as fibreglass, steel, and composite cores are steadily replacing traditional solid wood, as they offer superior insulation, reduced susceptibility to warping, and improved compliance with the EPBD 2024 durability and performance requirements. In commercial buildings, the adoption of revolving and automatic entrance systems is accelerating, as these solutions minimise air infiltration losses while meeting accessibility and safety standards established by the European Committee for Standardization (CEN/TC 33).

INSIGHT BY MATERIAL

By material, the plastic and glass segment dominates the doors and windows market in Europe. Plastic doors and windows are expected to continue gaining share as they replace wood and metal alternatives in cost-sensitive and renovation-driven applications. Lower installation costs and consistent performance have supported the widespread adoption of uPVC across residential markets in multiple European countries.

Glass doors show strong penetration in non-residential buildings, particularly in retail and corporate office environments. Frameless glass door systems are increasingly preferred over traditional framed designs, reflecting architectural trends toward transparency, openness, and modern aesthetics.

INSIGHT BY INSTALLATION

Replacement installations dominate Europe’s doors and windows market as building renovation activity accelerates under increasingly stringent energy-efficiency mandates. With more than 85% of Europe’s building stock constructed before 2000, upgrading thermal performance has become a critical pillar of the region’s climate and decarbonisation objectives. In this context, initiatives such as the EU Renovation Wave, Germany’s BEG 2.0, and France’s MaPrimeRénov’ 2025 are driving large-scale adoption of high-efficiency fenestration products across both residential and public-sector buildings.

Correspondingly, the focus of replacement projects has shifted away from aesthetic upgrades toward measurable performance improvements. Homeowners and building managers are increasingly opting for prefabricated or prehung door and window systems, which are delivered with integrated frames, seals, and insulation. These systems shorten installation timelines, improve on-site quality control, and significantly reduce air leakage, reinforcing their appeal in energy-focused renovation programs.

INSIGHT BY OPERATION

The Europe doors and windows market by operation is segmented into manual and automatic. Manual doors and windows accounted for over 80% of total revenue in 2025, reflecting their widespread use across residential buildings, commercial spaces, and high-traffic environments. Hinged and sliding formats remain the most common configurations. In developed European markets, manual revolving doors have gained adoption in selected applications where controlled air flow and short-duration high footfall are required, such as cinemas and educational institutions.

Manual systems continue to be preferred in residential and small commercial settings due to lower upfront costs, ease of airflow regulation, and cost-effective maintenance. Automatic door and window systems remain largely concentrated in premium commercial and institutional buildings, where accessibility, convenience, and controlled access are higher priorities.

EUROPE DOORS AND WINDOWS MARKET REGIONAL ANALYSIS

Germany region shows significant growth, with the fastest-growing CAGR of 5.59%, supported by sustained investment in non-residential construction and large-scale renovation of ageing commercial and institutional buildings. This is reflected in serial refurbishment initiatives such as Energiesprong Deutschland, including a series of renovations of a WBS 70 prefabricated building in Ludwigsfelde (Brandenburg), which directly elevates demand for high-performance facade elements, windows, and doors. Product uptrading is also visible in facade renewal projects such as the Lenderoth Renovation Project in Bremen, which included replacement glazing and recycled aluminium facade profiles, reinforcing the premiumisation trend in specifications.

In the UK, the doors and windows market growth is driven by replacement demand across commercial buildings and public infrastructure. A clear instance is the Salisbury Square Development in the City of London, where delivery plans include a new City of London Law Courts and associated civic buildings that specify fire-rated doors and high-security glazing window solutions. This type of public-sector and civic redevelopment supports higher-value demand where safety performance and compliance are procurement priorities.

EUROPE DOORS & WINDOWS MARKET VENDOR LANDSCAPE

- The Europe doors and windows market remains highly fragmented, with over 5,000 manufacturers operating across major countries. Numerous regional fabricators, extrusion firms, and integrated system houses coexist, creating intense price and design competition across materials and segments.

- Vendors are expanding through localized partnerships, installer networks, and service alliances to strengthen brand presence and ensure compliance with evolving national and EU building energy standards.

- Leading manufacturers such as Schuco, VEKA, Deceuninck, Reynaers, Hydro Building Systems, Velux, Inwido, and Internorm are focusing on sustainability, smart-home integration, and circular materials to differentiate their portfolios and align with the EU Green Deal 2030 targets.

- Regional demand is driven by renovation programs, energy performance directives, and building modernization initiatives such as the EU Renovation Wave and EPBD recast 2024. Western and Northern Europe lead in high-efficiency retrofits, while Central and Southern Europe are expanding replacement activity under subsidy-linked schemes.

- Fabricators and profile extruders form the backbone of the supply chain. uPVC and aluminum profiles are assembled locally into complete units with glazing, insulation, and smart fittings, allowing flexibility but sustaining market fragmentation. For instance, Germany’s top 300 firms account for nearly 60% of sales, while thousands of micro-fabricators share the rest.

- Access to capital, testing, and certification capabilities remains a barrier to entry, consolidating the market around established brands that can meet CE and sustainability documentation requirements.

- Rapid advances in automation, robotics, and prefabrication are reshaping production economics, challenging traditional workshops and accelerating efficiency-driven consolidation.

- Competitive advantage increasingly depends on low-carbon materials, smart functionality, and verified energy performance rather than cost alone. Vendors investing in digital-ready, circular, and high-performance systems are expected to gain long-term share through 2030.

Recent Developments in the Europe Doors and Windows Market

- In October 2025, Inwido expanded its UK footprint by acquiring Fast Frame Ltd., a PVC window and door manufacturer serving commercial clients. The acquisition strengthens Inwido’s market presence and local supply capacity under its Dekko platform.

- In July 2025, Schuco International announced that over 75 % of aluminum profiles used in 2024 came from low-carbon sources, cutting its operational CO₂ intensity by 17%. This achievement accelerates Schüco’s goal of a fully circular supply chain for facades, doors, and window systems.

- In March 2025, the VELUX Group reported a 60% reduction in Scope 1 and 2 emissions compared with 2020 and launched new circularity pilots extending window lifespans through refurbishment and reuse. This milestone reinforces VELUX’s leadership in carbon-neutral manufacturing and circular roof-window systems under the EU Green Deal framework.

- In December 2024, VELUX partnered with Thylander to build over 500 low-carbon rental homes under its Living Places concept in Denmark. The project showcases scalable daylight, ventilation, and low-CO₂ window integration, underscoring VELUX’s role in sustainable housing innovation.

- In September 2024, Inwido’s Pihla Group acquired Arctic-Kaihdin Oy, a Finnish producer of blinds and sun-protection systems. The deal broadens Inwido’s portfolio for retrofit and energy-management solutions in Northern Europe.

- In April 2024, VEKA UK increased its recycling capacity to over 20,000 tonnes per year through expanded processing lines and closed-loop collection programs. This initiative advances VEKA’s sustainability roadmap and supports Europe’s shift toward circular PVC-U profile manufacturing.

SNAPSHOT

The Europe doors and windows market size is expected to grow at a CAGR of approximately 3.45% from 2025 to 2031.

The following factors are likely to contribute to the growth of the Europe doors and windows market during the forecast period:

- Architectural Aesthetics & Design Integration

- Growth in Renovation & Home Improvement Programs

- Personalization and Digital Customization Demand

- Material Innovation & Smart Manufacturing Ecosystem

Base Year: 2025

Forecast Year: 2026-2031

The report considers the present scenario of the Europe doors and windows market and its market dynamics for 2026−2031. It covers a detailed overview of several market growth enablers, restraints, and trends. The study covers both the demand and supply sides of the market. It also profiles and analyses leading companies and several other prominent companies operating in the market.

Key Company Profiles

- VKR Holding

- Business Overview

- Product Offerings

- Key Developments

- Key Strategies

- Key Strengths

- Key Opportunities

- JELD-WEN

- Schüco International

- Internorm

- Inwido

- VEKA

Other Prominent Company Profiles

- Aluplast

- Business Overview

- Product Offerings

- Anglian Home Improvement

- Arbonia

- ASSA ABLOY

- Astraseal

- Bertrand

- Crystal Windows

- Deceuninck

- Dormakaba

- Drutex

- Eko-Okna

- Finstral

- Gartfen

- GEZE

- Gealan

- Slowinscy

- Svenska Fonster

- Weru

- Reynaers Aluminum

- REHAU Group

- Rawington

- Profine Group

- Profel Group

- Piva Group

- Oknoplast

- Nusco

- NorDan

- Neuffer Windows + Doors

- Masonite

- MALERBA

- Korzekwa

- Josko

- Gretsch-Unitas

- Goran

- Gilje

- Karo

- Ford Windows

- Hörmann

- DAKO

- Wicona

- Groupe Liebot

- Epwin Group

- Technal

- CMAI

Segmentation by Product

- Doors

- Windows

Segmentation by End-User

- Residential

- Non-Residential

Segmentation by Type

- Interior

- Exterior

Segmentation by Material

- Plastic & Glass

- Wood

- Metal

- Composite

- Others

Segmentation by Installation

- Replacement

- New Construction

Segmentation by Operation

- Manual

- Automatic

Segmentation by Geography

- Europe

- Germany

- UK

- Italy

- France

- Spain

- Netherlands

- Poland

- Sweden

- Belgium

- Norway

- Switzerland

- Denmark

- Finland

EUROPE DOORS AND WINDOWS MARKET FAQs

How big is the Europe doors and windows market?

What is the growth rate of the Europe doors and windows market?

What are the key trends in the Europe doors and windows market?

Who are the major players in the Europe doors and windows market?

Which region shows fastest growth in the Europe doors and windows market?

For more details, please reach us at [email protected]

- Chapter 1- Scope & Coverage

- Market Definition

- Inclusion

- Exclusions

- Market Estimation Caveats

- Market Derivation

- Market Segmentation by Product

- Market Segmentation by End-User

- Market Segmentation by Type

- Market Segmentation by Material

- Market Segmentation by Installation

- Market Segmentation by Operation

- Chapter 2- Premium Insights

- Chapter 3- Market Dynamics

- Introduction

- Biophilic Design

- Value Chain Analysis

- Consumer Preference

- Emerging Touchless Access Control Technologies

- Future Outlook of the Europe Doors & Windows Market

- Government Regulations Promoting Energy-Efficient Doors & Windows

- Impact of The Ongoing Tariff War

- Market Opportunities & Trends

- Smart & Adaptive Fenestration Technologies

- Sustainability & Energy Efficiency as Core Design Drivers

- Industry 5.0 and Sustainable Manufacturing Transformation

- Energy-Active and Solar-Integrated Building Exteriors

- Circular Materials, Lifecycle Value & Digital Ecosystem Integration

- Market Growth Enablers

- Architectural Aesthetics & Design Integration

- Growth in Renovation & Home Improvement Programs

- Personalization and Digital Customization Demand

- Material Innovation & Smart Manufacturing Ecosystem

- Market Restraints

- Volatility in Raw Material Prices and Energy Costs

- Market Fragmentation and Pricing Pressure

- Subdued Construction Outlook and Investment Constraints

- Market Landscape

- Five Forces Analysis

- Chapter 4- Market Segmentation

- Product (Market Size & Forecast: 2022-2031)

- Doors

- Windows

- End-User (Market Size & Forecast: 2022-2031)

- Residential

- Non-Residential

- Type (Market Size & Forecast: 2022-2031)

- Interior

- Exterior

- Material (Market Size & Forecast: 2022-2031)

- Plastic & Glass

- Wood

- Metal

- Composite

- Others

- Installation (Market Size & Forecast: 2022-2031)

- Replacement

- New Construction

- Operation (Market Size & Forecast: 2022-2031)

- Manual

- Automatic

- Chapter 5- Geography Segmentation

- Geography Segmentation (Market Size & Forecast: 2021-2030)

- Geographic Overview – Market Maturity Index

- Europe

- Germany

- UK

- Italy

- France

- Spain

- Netherlands

- Poland

- Sweden

- Belgium

- Norway

- Switzerland

- Denmark

- Finland

- Chapter 6- Competitive Landscape

- Competitive Landscape

- Competition Overview

- Consumer Satisfaction Benchmarking

- Country-wise Market Share Analysis of the Doors Market

- Country-wise Market Share Analysis of the Windows Market

- Recent Developments

- Key Company Profiles

- Other Prominent Company Profiles

- Report Summary

- Key Takeaways

- Strategic Recommendations

Select a license type that suits your business needs

Single User Licence

- Report accessible by one user only

- Free 10% or 3 days of customization

- Free post-sale service assistance

- Continuous support through email

5 User Licence

- Report accessible by 5 users within the organization

- Free 15% or 4.5 days of customization

- Continuous support through email and telephone

- Free analyst hour

- Free Upgrade: If an updated report published within 180 days of purchase, you will get the revised report free of charge

Corporate Licence

- Free Datasheet worth $1500

- Report accessible by the entire organization

- Free 20% or 6 days of customization

- Free post-sale service assistance

- Continuous support through email and telephone

- Direct access to lead analysts

- Free analyst hour

- Free Upgrade: If an updated report published within 180 days of purchase, you will get the revised report free of charge

Datasheet Licence

- Report accessible by 1 user only

- Free 15% or 32 hours of customization

- Free post-sale service assistance

- Direct access to lead analysts

Frequently Asked Questions

How big is the Europe doors and windows market?

What is the growth rate of the Europe doors and windows market?

What are the key trends in the Europe doors and windows market?

Who are the major players in the Europe doors and windows market?

Which region shows fastest growth in the Europe doors and windows market?

Other RELATED Reports

Europe Garage Doors Installation And Maintenance Market Research Report 2025-2030

Published : October 2025