Global Flexible Packaging Market Research Report 2026-2031

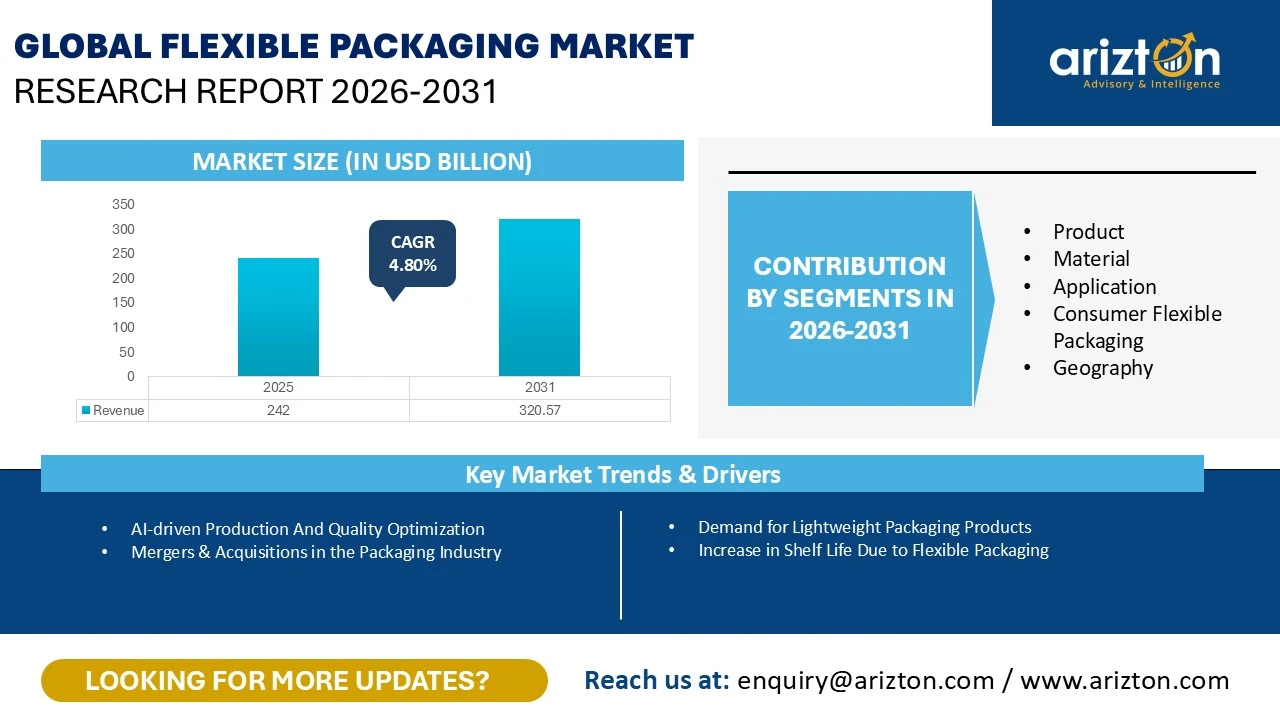

THE GLOBAL FLEXIBLE PACKAGING MARKET WAS VALUED AT USD 242 BILLION IN 2025 AND IS EXPECTED TO REACH USD 320.57 BILLION BY 2031, GROWING AT A CAGR OF 4.80%.

Flexible Packaging Market Growth Insights – Driven by Rising Demand for Convenient, Lightweight, and Sustainable Packaging Solutions Across Food, Beverage, Healthcare, Personal Care, and Consumer Goods Industries (2026–2031)

Published Date : June 2026

Last Updated : July 2026

format: PDF

edition : Sixth Edition

320 pages

5 region

30 countries

80 company

5 segments

Purchase Options

Global Flexible Packaging Market Research Report 2026-2031

THE GLOBAL FLEXIBLE PACKAGING MARKET WAS VALUED AT USD 242 BILLION IN 2025 AND IS EXPECTED TO REACH USD 320.57 BILLION BY 2031, GROWING AT A CAGR OF 4.80%.

The Flexible Packaging Market Size, Share & Trends Analysis Report By

- Product: Bags & Sacks, Pouches, and Others

- Material: Flexible Plastic, Flexible Paper, and Foil

- Application: Consumer Packaging and Industrial Packaging

- Consumer Flexible Packaging: Bakery & Confectionery, Meat, Poultry & Seafood, Dairy, RTE, Frozen Food, Healthcare, Personal Care, Tea & Coffee, Pet Food, and Others

- Geography: North America, Europe, APAC, Latin America, and Middle East & Africa

Industry Analysis Report, Regional Outlook, Growth Potential, Price Trends, Competitive Market Share & Forecast 2026–2031.

This report includes market data points, ranging from trend

analyses to market estimates & forecasts that you can customize

FLEXIBLE PACKAGING MARKET REPORT SCOPE

| REPORT ATTRIBUTE | DETAILS |

|---|---|

| MARKET SIZE (2031) | USD 320.57 Billion |

| MARKET SIZE (2025) | USD 242 Billion |

| CAGR (2025-2031) | 4.80% |

| HISTORIC YEAR | 2022-2024 |

| BASE YEAR | 2025 |

| FORECAST YEAR | 2026-2031 |

| SEGMENTS BY | Product, Material, Application, Consumer Flexible Packaging, and Geography |

| GEOGRAPHIC ANALYSIS | North America, Europe, APAC, Latin America, & Middle East & Africa |

| KEY PLAYERS | Amcor, Berry Global Inc., Mondi Group, Sealed Air, Transcontinental Inc., Sonoco Products Company, Huhtamaki, Ahlstrom, Smurfit Westrock, and AptarGroup, Inc. |

FLEXIBLE PACKAGING MARKET SIZE & SHARE

The flexible packaging market size was valued at USD 242 billion in 2025 and is expected to reach USD 320.57 billion by 2031, growing at a CAGR of 4.80% during the forecast period. Demand is strengthening across categories where packaging must protect the product while improving usability and supply-chain movement. Flexible formats such as pouches, wraps, sachets, lidding films, refill packs, and spouted packs support freshness, portion control, dispensing, portability, shelf visibility, and efficient distribution. This makes the flexible plastic packaging market relevant across daily-consumption categories and higher-value products requiring stable quality and convenient consumer handling.

Shelf-life protection remains a key value proposition for the flexible packaging market, especially where moisture and oxygen exposure can reduce product freshness, safety, and commercial value. High-barrier flexible materials support food, beverages, nutraceuticals, pharmaceuticals, pet food, and other sensitive products — particularly within the medical flexible packaging market — by helping maintain product stability during storage, distribution, and retail display, while also supporting convenient pack formats and lower product wastage across supply chains.

E-commerce and delivery-led retail are increasing the need for lighter, right-sized, and lower-waste packaging systems. Amazon, a global e-commerce and logistics company, reported that it avoided 4.2 million metric tons of packaging materials since 2015 and reduced single-use plastic delivery packaging globally by 16.4% in 2024, reinforcing demand for packaging that reduces parcel weight, shipment inefficiency, and waste for retailers.

Key Takeaways

- Product: The bags & sacks accounted for the largest market share of around 43%.

- Material: The flexible paper is expected to grow at a CAGR of 4.73% during 2025–2031.

- Application: The industrial packaging segment accounted for the second-largest global flexible packaging market share in 2025.

- Consumer Flexible Packaging: The bakery & confectionery dominates and holds the largest market share.

- Geography: The APAC flexible packaging market accounted for the largest market share of around 38%.

Mergers & Acquisitions in the Flexible Packaging Market

- In April 2025, Amcor completed its merger with Berry Global, expanding its global scale across consumer and healthcare packaging and strengthening its flexible packaging footprint.

- In April 2025, TOPPAN completed the acquisition of Sonoco's Thermoformed & Flexibles Packaging business for approximately $1.8 billion, accelerating its global expansion in sustainable packaging.

- In March 2026, Amcor partnered with DCM to introduce recycle-ready mono-PE fertilizer packaging in Europe with 35% post-consumer recycled content. The new flexible packaging replaces a previous multi-material structure, supports existing recycling streams, reduces the carbon footprint by 17%, and strengthens Amcor's position in sustainable industrial and specialty flexible packaging.

Recent Product Developments in the Flexible Packaging Market

- In February 2025, Berry Global unveiled its next-generation Bontite Sustane Stretch Film with 30% certified post-consumer recycled content. The film supports palletized goods across logistics, food & beverage, retail, manufacturing, pharmaceuticals, and e-commerce, while improving load stability, reducing reliance on virgin plastic, and supporting recyclable PE film applications where collection systems exist.

FLEXIBLE PACKAGING MARKET TRENDS & ENABLERS

- Sustainability-led redesign is strengthening flexible packaging market adoption as brands shift toward recyclable, downgauged, compostable, and mono-material formats to meet customer expectations and regulatory requirements. This supports packaging converters — companies that transform films, paper, foil, and laminates into finished flexible packaging — by improving material efficiency while helping brand owners align with circularity goals. Collaboration among material suppliers, converters, and equipment makers is making recyclable laminate development more scalable across food, personal care, and household applications, particularly as the flexible plastic packaging market transitions toward lower-impact material systems.

- Lightweight flexible packaging is gaining traction as brands focus on material efficiency, lower transport intensity, and more sustainable pack design. Flexible Packaging Europe, an industry association representing the European flexible packaging sector, states that flexible packaging can deliver a packaging-to-product ratio 5 to 10 times lower than alternative formats. This strengthens its value proposition for cost-sensitive and high-volume product categories where packaging weight, freight efficiency, and material use directly influence margins.

- Shelf-life extension remains a strong demand enabler for the flexible packaging market because brand owners and retailers need formats that protect products from oxygen, moisture, and contamination during storage and distribution. This is especially important in food and fresh produce, where spoilage affects margins and sustainability performance. United Nations Environment Programme (UNEP), the United Nations' environmental authority, states that food loss and waste account for 8%–10% of global greenhouse gas emissions, reinforcing the commercial value of protective packaging.

INDUSTRY RESTRAINTS

- Raw material volatility restrains the flexible packaging market size by raising costs for packaging converters across resins, films, adhesives, paper, and board. Flexible Packaging Europe, an industry association representing the European flexible packaging sector, reported that high-density polyethylene (HDPE) and low-density polyethylene (LDPE) prices increased by 3% and 4%, respectively, in Q1 2025 versus Q4 2024, making sourcing discipline, pricing pass-through, and inventory planning important for companies and converters globally. This cost pressure is particularly pronounced in the north america flexible packaging market, where converters serve high-volume, margin-sensitive categories across food, household, and industrial segments.

FLEXIBLE PACKAGING MARKET SEGMENTAL INSIGHTS

INSIGHT BY PRODUCT

The flexible packaging market by product is segmented into bags & sacks, pouches, and others. The bags & sacks accounted for the largest market share of around 43%. Flexible bags and sacks formats are widely used across sectors, including agriculture, food, pet care, home care, and retail applications. Their lightweight, handling efficiency, and product protection continue to support adoption across high-volume categories where cost-effective transport, storage, and shelf presentation remain important.

The personal care sector also heavily utilises flexible bags, particularly in the form of refill pouches for shampoos, lotions, and cleaning agents, as brand owners continue to expand refill-led packaging models to reduce pack weight and improve material efficiency.

Food and Agriculture Organization (FAO), a United Nations food agency, forecast world cereal utilization at 2,946 million tonnes in 2025/26, reinforcing long-term demand for high-volume grain, food, and bulk commodity packaging formats.

INSIGHT BY MATERIAL

Based on the material, the flexible packaging market size for flexible paper is expected to grow at a CAGR of 4.73% during 2025–2031 as brands shift toward lower-plastic and recyclable packaging formats in food, bakery, confectionery, personal care, and dry goods applications. These solutions use paper as the primary material while retaining key flexible packaging features such as lightweight structure, printability, easy handling, and adaptability across pouches, sachets, flow packs, wraps, and other flexible formats.

Demand is being supported by e-commerce, snacks, coffee, pet food, personal care, and selected dry food applications where lightweight and space-efficient formats matter. Paper-based pouches and mailer-style structures can lie flat, reduce storage space, and support transport efficiency, while offering brands — including those across the flexible plastic packaging market — a more visible sustainability cue than many conventional plastic-based formats.

INSIGHT BY APPLICATION

Based on the application, the industrial packaging segment accounted for the second-largest global flexible packaging market share in 2025. Industrial packaging is used in chemicals, construction materials, agricultural inputs, processed goods, and export shipments. Form-fill-seal bags, liners, heavy-duty sacks, and protective films help companies reduce packaging weight while maintaining product containment, handling efficiency, and shipment safety. This strengthens adoption across industrial supply chains where bulk movement, logistics reliability, and cost control remain key customer requirements.

The importance of industrial packaging is evident in its contribution to health and safety. It helps businesses comply with laws and regulations that mandate stringent health and safety standards. In addition, industrial packaging is essential for protecting products from damage or contamination. Cardboard boxes can safeguard goods during transit from warehouses to stores.

INSIGHT BY CONSUMER FLEXIBLE PACKAGING

The flexible packaging market by consumer application is led by bakery & confectionery, which dominates and holds the largest global market share. Bakery and confectionery applications continue to support demand because these products require freshness retention, contamination protection, texture preservation, and strong shelf appeal. Cookies, brownies, pastries, chocolates, and other bakery and confectionery products need packaging that protects flavour, controls moisture exposure, and presents products attractively across retail and premium channels.

The medical flexible packaging market is expected to experience significant growth during 2025–2031 as medicines, diagnostics, hygiene products, and medical consumables require sterility, tamper evidence, dosage protection, and clear labelling. World Health Organization (WHO), the global public health agency, states that one in six people worldwide will be aged 60 years or over by 2030, supporting long-term demand for reliable healthcare packaging formats as ageing populations increase the need for medicines, medical consumables, and patient-safe packaging.

FLEXIBLE PACKAGING MARKET GEOGRAPHICAL ANALYSIS

The flexible packaging market size across North America is expected to maintain its position during the forecast period, with the united states flexible packaging market contributing the highest revenue share due to its large end-use base across food and beverage, pharmaceuticals, personal care, e-commerce, and household products.

The north america flexible packaging market remains one of the most mature packaging markets globally, supported by its large food, healthcare, personal care, retail, and e-commerce base. Flexible packaging continues to hold a strong position in the country's packaging mix, while film and flex packaging circularity is increasingly influencing material selection, package design, and recovery pathways.

The APAC flexible packaging market accounted for the largest share of around 38%, supported by packaged food demand, urban consumption, e-commerce growth, recyclable packaging policies, and rising converting capacity across major manufacturing hubs. This positions APAC as a scale-led growth market for converters, resin suppliers, film producers, and brand owners expanding flexible packaging capacity.

China and India remain central to APAC's flexible packaging growth because both markets combine large consumer bases, expanding packaged food demand, quick-commerce growth, and increasing domestic converting capacity.

Europe remains the second-largest flexible packaging market, with growth increasingly shaped by recyclability, waste reduction, circular material use, and brand commitments to lower-plastic packaging. Eurostat, the European Union's statistical office, reported that the European Union generated 35.3 kilograms of plastic packaging waste per person in 2023, with 14.8 kilograms recycled, reinforcing demand for recyclable flexible packaging formats that can support compliance and circularity targets.

Germany remains a key European flexible packaging market because of its strong food processing base, pharmaceutical demand, recycling infrastructure, and mature packaging conversion ecosystem. The italy flexible packaging market is also gaining relevance, supported by its established food processing sector, premium consumer goods output, and increasing pressure on brand owners to align with EU recyclability mandates. German Environment Agency (UBA), Germany's federal environmental authority, and Central Agency Packaging Register (ZSVR), Germany's packaging compliance authority, reported that the proportion of plastic packaging recycled rose from 42.1% in 2018 to 68.9% in 2023. This supports demand for mono-material structures, recyclable laminates, and recovery-ready packaging designs that align with Germany's advanced recycling and compliance environment.

FLEXIBLE PACKAGING MARKET VENDOR LANDSCAPE

The flexible packaging market remains highly fragmented, comprising a mix of large multinational corporations and numerous regional or niche players across the world. While global players continue to lead through advanced technologies, economies of scale, and extensive distribution networks, local manufacturers still compete by offering customization, cost advantages, and faster turnaround times.

Competition is fueled by rapid innovation in materials, barrier technologies, and sustainability-driven R&D. Players continue to invest in developing recyclable, mono-material, and other advanced flexible packaging solutions to meet regulatory and consumer demands. This is particularly evident in the medical flexible packaging market, where sterility requirements and compliance standards are raising the bar for material performance and traceability.

Flexible packaging companies are competing by offering high customization, short-run capabilities, and digital printing solutions. This remains particularly important in industries such as snacks, pet food, and cosmetics, where brand differentiation and faster product launches are key.

Major firms are actively using mergers and acquisitions to enter new regions, broaden product portfolios, and strengthen production capabilities. Consolidation is becoming an important route to build scale, improve material innovation, and serve multinational customers that require consistent quality, compliance, and supply reliability across multiple packaging markets.

Sustainability has become a core competitive battleground. Firms that offer lightweight, recyclable, and mono-material packaging continue to gain advantage, especially in Europe and North America, where regulatory pressure and customer expectations remain strong.

SNAPSHOT

The global flexible packaging market size is expected to grow at a CAGR of approximately 4.80% from 2025 to 2031.

The following factors are likely to contribute to the growth of the global flexible packaging market during the forecast period:

- Increasing Workplace Safety Regulations

- Rising Healthcare Demand

- Rising Industrialization and Infrastructure Booms

Base Year: 2025

Forecast Year: 2026-2031

The report examines the current state of the global flexible packaging market and its market dynamics through 2026−2031. It covers a detailed overview of several market growth enablers, restraints, and trends. The study covers both the demand and supply sides of the market. It also profiles and analyses leading companies and several other prominent companies operating in the market.

Key Vendors

- Amcor

- Berry Global Inc.

- Mondi Group

- Sealed Air

- Transcontinental Inc.

- Sonoco Products Company

- Huhtamaki

- Ahlstrom

- Smurfit Westrock

- AptarGroup, Inc.

Other Prominent Vendors

- All4Labels

- Aluberg S.p.A.

- American Packaging Corporation

- Aran Group

- Bioplast

- Bischof+Klein SE & Co. KG

- Bühler

- Carcano Antonio S.p.A.

- CCL Industries Inc.

- Cellografica Gerosa S.p.A.

- Cosmo Films

- Coveris

- Danaflex

- DazPak

- Di Mauro Officine Grafiche S.p.A.

- Eco Flexibles

- ePac Holdings, LLC

- Etapak

- Eurofoil Luxembourg S.A.

- FlexPack

- Gascogne Flexible

- Glenroy, Inc.

- Global-Pak, Inc.

- Goglio S.p.A.

- Grupo Lantero

- Guala Pack

- Innovia Films

- International Paper

- Industria Termoplastica Pavese (ITP)

- O. Kleiner AG

- Korozo Group

- Krajcár Packaging Ltd.

- LEEB GmbH & Co. KG

- Notpla Limited

- Novolex

- Perlen Packaging

- Plastic Suppliers Inc.

- Plastixx FFS Technologies

- Polypak Packaging

- Printpack

- ProAmpac

- Pro-Pac Packaging Limited

- Reynolds Group Ltd.

- Ringmetall

- RKW Group

- Rockwell Solutions

- Saica

- SCHMID FOLIEN GmbH & Co. KG

- Schur

- SIG

- Sigma Plastics Group

- Stora Enso

- Südpack

- Symetal

- Reflex Group

- UFlex Limited

- Walki Group Oy

- Winpak Ltd.

- Wipf AG

- Constantia Flexibles

- TOPPAN Holdings

- SCG Packaging (SCGP)

- Jindal Films

- Oben Group

- Elif

- PPC Flex

- C-P Flexible Packaging

- Accredo Packaging

- KM Packaging

- Liquibox

Segmentation by Product

- Bags & Sacks

- Pouches

- Others

Segmentation by Material

- Flexible Plastic

- Flexible Paper

- Foil

Segmentation by Application

- Consumer Packaging

- Industrial Packaging

Segmentation by Consumer Flexible Packaging

- Bakery & Confectionery

- Meat, Poultry & Seafood

- Dairy

- RTE

- Frozen Food

- Healthcare

- Personal Care

- Tea & Coffee

- Pet Food

- Others

Segmentation by Geography

- North America

- US

- Canada

- APAC

- China

- India

- Japan

- Australia

- South Korea

- Indonesia

- Vietnam

- Thailand

- New Zealand

- Europe

- Germany

- UK

- France

- Italy

- Benelux

- Scandinavia

- Spain

- Poland

- Switzerland

- Austria

- Latin America

- Brazil

- Mexico

- Argentina

- Chile

- Middle East & Africa

- Turkey

- Egypt

- Saudi Arabia

- UAE

- South Africa

FLEXIBLE PACKAGING MARKET FAQs

How big is the global flexible packaging market?

What is the growth rate of the global flexible packaging market?

What are the key trends in the global flexible packaging market?

Which region dominates the global flexible packaging market?

Who are the major players in the global flexible packaging market?

For more details, please reach us at [email protected]

- Chapter 1- Scope & Coverage

- Market Definition

- Inclusion

- Exclusions

- Market Estimation Caveats

- Market Derivation

- Market Segmentation by Product

- Market Segmentation by Material

- Market Segmentation by Application

- Market Segmentation by Consumer Flexible Packaging

- Chapter 2- Premium Insights

- Chapter 3- Market Dynamics

- Introduction

- Product Architecture and Design Intelligence

- End-Use Market Trends and Demand Linkages

- Value Chain and Industry Ecosystem Analysis

- Technology and Material Innovation Outlook

- AI and Digital Enablement in Flexible Packaging

- Market Opportunities & Trends

- Increased Focus on Sustainable Flexible Packaging

- AI-driven Production and Quality Optimization

- Rising Demand for E-commerce-optimized Flexible Packaging

- Mergers & Acquisitions in the Packaging Industry

- Market Growth Enablers

- Demand for Lightweight Packaging Products

- Increase in Shelf Life due to Flexible Packaging

- Increasing Demand from Healthcare & Pharmaceutical Sectors

- Market Restraints

- Rise in Cost of Raw Materials

- Perishability of Packaging Materials

- Recycling Challenges with Flexible Packaging Products

- Market Landscape

- Five Forces Analysis

- Chapter 4- Market Segmentation

- Product (Market Size & Forecast: 2022-2031)

- Bags & Sacks

- Pouches

- Others

- Material (Market Size & Forecast: 2022-2031)

- Flexible Plastic

- Flexible Paper

- Foil

- Application (Market Size & Forecast: 2022-2031)

- Consumer Packaging

- Industrial Packaging

- Consumer Flexible Packaging (Market Size & Forecast: 2022-2031)

- Bakery & Confectionery

- Meat, Poultry & Seafood

- Dairy

- RTE

- Frozen Food

- Healthcare

- Personal Care

- Tea & Coffee

- Pet Food

- Others

- Chapter 5- Geography Segmentation

- Geography Segmentation (Market Size & Forecast: 2022-2031)

- Geographic Overview – Market Maturity Index

- APAC

- China

- India

- Japan

- Australia

- South Korea

- Indonesia

- Vietnam

- Thailand

- New Zealand

- North America

- US

- Canada

- Europe

- Germany

- UK

- France

- Italy

- Benelux

- Scandinavia

- Spain

- Poland

- Switzerland

- Austria

- Latin America

- Brazil

- Mexico

- Argentina

- Chile

- MEA

- Turkey

- Egypt

- Saudi Arabia

- UAE

- South Africa

- Chapter 6- Competitive Landscape

- Competitive Landscape

- Competition Overview

- Key Developments

- Market Share Analysis

- Key Company Profiles

- Other Prominent Company Profiles

- Report Summary

- Key Takeaways

- Strategic Recommendations

Select a license type that suits your business needs

Single User Licence

- Report accessible by one user only

- Free 10% or 3 days of customization

- Free post-sale service assistance

- Continuous support through email

5 User Licence

- Report accessible by 5 users within the organization

- Free 15% or 4.5 days of customization

- Continuous support through email and telephone

- Free analyst hour

- Free Upgrade: If an updated report published within 180 days of purchase, you will get the revised report free of charge

Corporate Licence

- Free Datasheet worth $1500

- Report accessible by the entire organization

- Free 20% or 6 days of customization

- Free post-sale service assistance

- Continuous support through email and telephone

- Direct access to lead analysts

- Free analyst hour

- Free Upgrade: If an updated report published within 180 days of purchase, you will get the revised report free of charge

Datasheet Licence

- Report accessible by 1 user only

- Free 15% or 32 hours of customization

- Free post-sale service assistance

- Direct access to lead analysts

Frequently Asked Questions

How big is the global flexible packaging market?

What is the growth rate of the global flexible packaging market?

What are the key trends in the global flexible packaging market?

Which region dominates the global flexible packaging market?

Who are the major players in the global flexible packaging market?