Portugal Data Center Market – Investment Analysis & Growth Opportunities 2026-2031

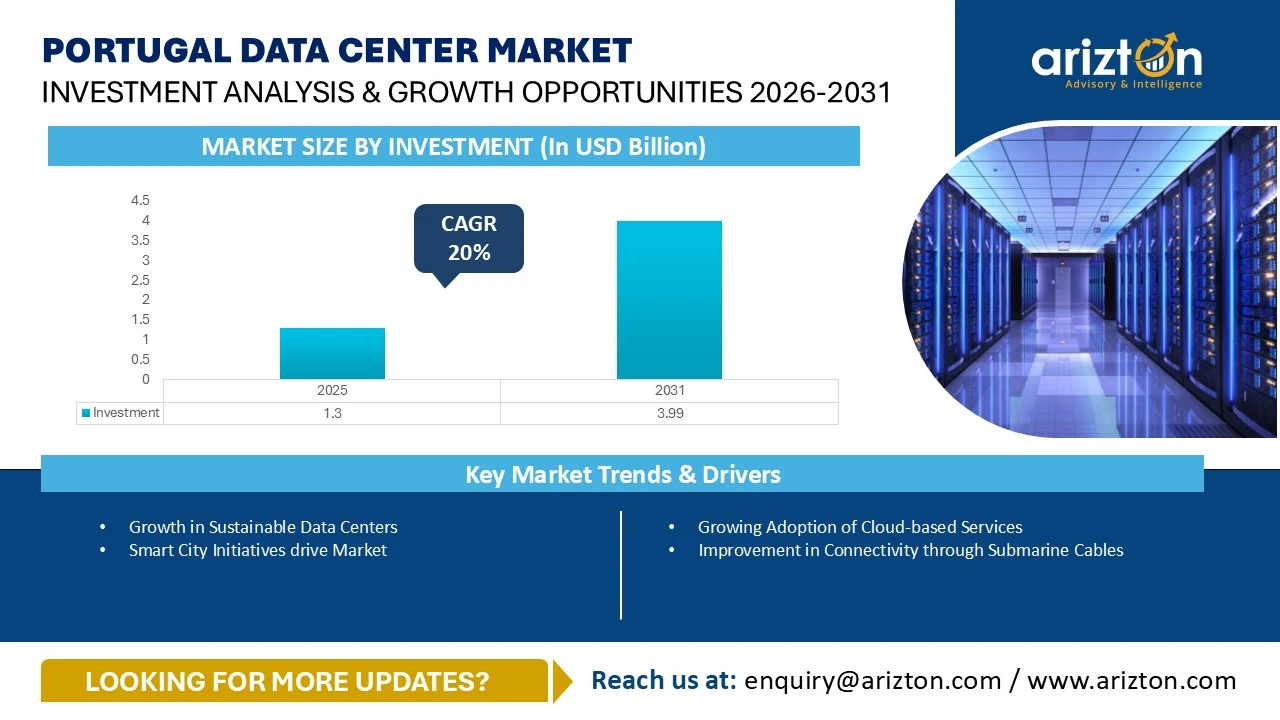

THE PORTUGAL DATA CENTER MARKET SIZE WAS VALUED AT USD 1.30 BILLION IN 2025 AND IS EXPECTED TO REACH USD 3.99 BILLION BY 2031, GROWING AT A CAGR OF 20% DURING THE FORECAST PERIOD.

104 pages

46 company

6 segments

1 region

1 countries

Purchase Options

Portugal Data Center Market – Investment Analysis & Growth Opportunities 2026-2031

THE PORTUGAL DATA CENTER MARKET SIZE WAS VALUED AT USD 1.30 BILLION IN 2025 AND IS EXPECTED TO REACH USD 3.99 BILLION BY 2031, GROWING AT A CAGR OF 20% DURING THE FORECAST PERIOD.

The Portugal Data Center Market Report Includes Size in Terms of

- IT Infrastructure: Servers, Storage Systems, and Network Infrastructure

- Electrical Infrastructure: UPS Systems, Generators, Transfer Switches & Switchgears, PDUs, and Other Electrical Infrastructure

- Mechanical Infrastructure: Cooling Systems, Rack Cabinets, and Other Mechanical Infrastructure

- Cooling Systems: CRAC & CRAH Units, Chiller Units, Cooling Towers, Condensers & Dry Coolers, and Other Cooling Units

- General Construction: Core & Shell Development, Installation & Commissioning Services, Engineering & Building Design, Fire Detection & Suppression Systems, Physical Security, and Data Center Infrastructure Management (DCIM)

- Tier Standard: Tier I & Tier II, Tier III, and Tier IV

Get Insights on 14 Existing Data Centers and 11 Upcoming Facilities across Portugal

This report includes market data points, ranging from trend

analyses to market estimates & forecasts that you can customize

PORTUGAL DATA CENTER MARKET REPORT SCOPE

| REPORT ATTRIBUTE | DETAILS |

|---|---|

| MARKET SIZE (INVESTMENT) | USD 3.99 Billion (2031) |

| MARKET SIZE (AREA) | 230 Thousand Sq. feet (2031) |

| MARKET SIZE (POWER CAPACITY) | 14 MW (2031) |

| CAGR - INVESTMENT (2025-2031) | 20% |

| COLOCATION MARKET SIZE (REVENUE) | USD 350 Million (2031) |

| HISTORIC YEAR | 2022-2024 |

| BASE YEAR | 2025 |

| FORECAST YEAR | 2026-2031 |

PORTUGAL DATA CENTER MARKET SIZE & OUTLOOK

The Portugal data center market size was valued at USD 1.30 billion in 2025 and is projected to experience explosive growth, reaching USD 3.99 billion by 2031. This path represents a staggering Compound Annual Growth Rate (CAGR) of 20% over the forecast period.

Portugal is rapidly solidifying its standing as a fast-growing, highly strategic digital infrastructure hub in Southern Europe. This accelerating Portugal data center growth is fueled by widespread corporate digital transformation, surging cloud adoption across industrial sectors, and an unprecedented demand for artificial intelligence (AI) high-density compute clusters.

Several macroeconomic and structural advantages make the country a premier destination for Portugal data center investment:

- Regulatory & Political Stability: A strong data privacy framework aligned with EU regulations, paired with long-term political stability, minimizes risk for multinational enterprise operators.

- Unmatched Subsea Connectivity: The Iberian Peninsula serves as a critical bridge. Portugal acts as the direct landing point for 16 major submarine cable systems, meaning roughly 25% of the world's subsea data traffic passes through the nation.

- Dense Terrestrial Networks: Complementing international subsea cables, Portugal boasts a remarkable 92% fiber-optic network coverage, ranking third across the entire European Union.

- Abundant Renewable Energy: Massive domestic wind, solar, and hydro generation capacity allows operators to build large-scale, sustainable digital infrastructure with a minimal carbon footprint.

To support this expanding landscape, the Associação Portuguesa de Centros de Dados (Portugal DC) was founded in 2023. As an independent, non-profit industry body, Portugal DC unifies developers, engineers, and operators to standardize guidelines and sustainably scale the Portugal data center ecosystem.

KEY MARKET HIGHLIGHTS

The Shift to Sustainable, Coastal Ecosystems

The European landscape is experiencing a clear structural shift away from traditional, power-constrained FLAP (Frankfurt, London, Amsterdam, Paris) markets. Capital is migrating toward strategic coastal locations that offer direct Atlantic cable access and abundant green energy grids.

As of December 2025, the Portugal colocation market maintained 67.1 MW of operational core and shell IT load capacity. However, the upcoming pipeline reveals a massive scale-up, with over 1,930 MW (1.93 GW) of capacity currently in various development phases.

Geographic Distribution: Growth Beyond Lisbon

While Lisbon remains the primary and most preferred zone for colocation deployments, severe space constraints are distributing infrastructure outward:

- Sines: Evolving into a premier European hyperscale destination due to its direct proximity to ocean cable landings and deep-water port infrastructure.

- Pego & Abrantes: Emerging as vital secondary infrastructure hubs, capturing investments from operators converting legacy industrial grid access points into high-density digital server campuses.

Development Costs and Architecture Trends

Building a facility in Portugal remains highly economical compared to core European markets like the UK, Germany, France, or Switzerland.

Development Cost Benchmark: Data center construction in Portugal averages between $9 million and $10 million per Megawatt (MW). While raw material inflation, supply chain bottlenecks, and interest rates are pushing this baseline up annually, it remains a highly cost-effective alternative.

Furthermore, developers are increasingly constructing Open Compute Project (OCP) ready facilities. These layouts strictly adhere to unified OCP guidelines originally spearheaded by tech giants like Meta to completely optimize rack spaces, maximize power delivery efficiency, and scale hardware infrastructure seamlessly.

Market Segmentation: Revenue & Engineering Domains

The total addressable investment within the country is heavily categorized by delivery framework and hardware provisioning.

Colocation Revenue Distribution

The Portugal colocation market is divided cleanly into wholesale allocations (hyperscalers and cloud providers) and retail spaces (regional enterprise architectures and edge processing node networks).

Infrastructure Procurement Segments

The ongoing buildouts require specialized vendors across multiple highly detailed asset classes:

- IT Infrastructure: Procurement of enterprise rack servers, flash storage arrays, and AI-optimized hardware (GPUs).

- Electrical Infrastructure: Advanced Uninterruptible Power Supply (UPS) configurations, industrial backup generators, automatic transfer switches, switchgears, and smart Power Distribution Units (PDUs).

- Mechanical & Cooling Systems: Next-generation Computer Room Air Conditioning/Handler (CRAC/CRAH) setups, industrial chiller units, open-loop cooling towers, condensers, dry coolers, and liquid immersion equipment.

- General Construction: Comprehensive core & shell development, building engineering design, active fire suppression, biometric physical security, and integrated Data Center Infrastructure Management (DCIM) software.

- Tier Standard Classifications: The market is dominated by Tier III and Tier IV certified builds, reflecting a strict requirement for concurrent maintainability and fault tolerance.

Competitive & Vendor Landscape

The competitive landscape of the Portugal data center market is witnessing an aggressive influx of capital, driven by domestic incumbents, prominent new entrants, and global hyperscalers eager to secure Southern European capacity.

1. The Core Ecosystem: Established Operators

Portugal’s colocation foundation continues to be anchored by heavily capitalized institutional players and telecom operators, with key market anchors including Altice Portugal, AR Telecom, Equinix, NOS Sistemas, REN, and Start Campus. A prime catalyst of this segment is Start Campus and its ambitious project in Sines. In April 2025, the developer inaugurated its first facility building, SIN01. Immediately following this milestone, construction began on the second facility, SIN02, in June 2025. The SIN02–SIN06 builds represent the second multi-year phase of the infrastructure project, which is scheduled to roll out progressively over the next five years. Upon final completion of all phases, total capital investment into the Start Campus Sines megaproject will exceed $10 billion.

2. Emerging Market Challengers: Highly Capitalized Entrants

Driven by the shifting geography of European data infrastructure, a dynamic wave of new players is establishing operations in Portugal to capture unmet demand for high-density colocation. The most notable new entrants include AtlasEdge, Digital Realty, EDC One, Edged, FF Ventures, Quetta Data Centers, and Templus.

A major highlight in this sector occurred in September 2025, when EDC One unveiled a massive $8.2 billion development plan for a data center campus in Abrantes, Portugal. Built on industrial land in the Pego industrial zone, the project is structured across three distinct phases and is scheduled to become fully operational in the second quarter of 2028. To accelerate construction and attract foreign investment, the Abrantes City Council approved a critical municipal support package providing $19.1 million in tax exemptions.

3. Hyperscale Acceleration: Cultivating Europe’s AI Factories

Global cloud and technology giants are aggressively positioning Portugal as their principal Southern European hub for artificial intelligence computing. In November 2025, Microsoft announced a landmark $10 billion investment strategy focused entirely on building advanced, AI-optimized supercomputing data centers in Sines. This deployment aims to integrate thousands of next-generation AI processors, transforming the coastal region into a primary regional processing hub for complex enterprise cloud and large-scale language model workloads.

4. Mergers & Acquisitions: Fast-Tracking Market Entry

Strategic corporate acquisitions have become the preferred mechanism for international real estate investment trusts (REITs) looking to establish immediate market presence or expand their current market share in the region. As a clear reflection of this trend, Digital Realty announced its entry into the market in March 2026 through the acquisition of an under-development facility in Lisbon. Backed by an initial deal valuation of around $8.3 million, this facility features an initial power capacity of 2.4 MW and is projected to reach its operational target by early 2027.

Here is a rewritten, professional version of the "Why Should You Buy This Research?" section, optimized for flow, clarity, and scannability while retaining all core deliverables.

Why Buy This Research?

This report provides an in-depth, data-driven assessment of the Portugal data center market size and its evolving digital landscape. It delivers actionable insights, historical data, and granular forecasts to help investors, operators, and infrastructure providers identify high-growth opportunities and navigate the Portugal data center industry with confidence.

1. Granular Market Sizing & Forecasts (2022–2031)

- Comprehensive Metric Tracking: Access precise historical data and future projections for total capital investment, facility square footage, and total IT power capacity (MW).

- Colocation Market Segmentation: Review detailed revenue streams and growth forecasts, distinguishing the retail and wholesale sectors of the Portugal colocation market.

- Pricing Intelligence: Evaluate shifting pricing models and rack-space cost structures for both retail cages and wholesale hyperscale leases across key regions.

2. In-Depth Operational & Infrastructure Analysis

- Strategic Asset Breakdown: Analyze how capital is being distributed across critical technological segments, including IT hardware (servers, storage, networking), electrical infrastructure, mechanical cooling, and general civil construction services.

- Tier Standard Assessment: Understand the market share and pipeline velocity of Tier I through Tier IV facilities, mapping out where the highest redundancies are being deployed.

- Ecosystem Tracking: Gain a 360-degree view of market dynamics, assessing competitive macro trends, emerging opportunities, localized growth restraints, and regulatory shifts shaping Portugal data center investment.

3. Third-Party Facility Snapshot

The research tracks a robust regional portfolio across 7+ critical cities, detailing the physical scale and IT loads of active vs. pipeline facilities:

- Existing Infrastructure Covered: Labeled operational analysis of 14 active data centers.

- Upcoming Pipeline Identified: In-depth blueprints and delivery targets for 11 planned facilities.

- Spatial Comparison: Direct visual data mapping comparing existing white-floor space against future capacity additions to identify localized supply gaps.

4. Competitive Intelligence & Vendor Profiles

- Operator Mapping: Identify market share shifts among colocation providers, enterprise operators, and global giants expanding Portugal cloud data centers.

- Supply Chain Assessment: Evaluate the product offerings, technical capabilities, and localized presence of key market participants, categorized into four vital pillars:

- IT Infrastructure Providers (Compute, storage, and specialized AI hardware)

- Data Center Construction Contractors (General EPC, design, and commissioning firms)

- Support Infrastructure Providers (Power delivery, MEP engineering, and industrial cooling vendors)

- Institutional Investors & New Entrants (Capital platforms driving the rollout of Portugal hyperscale data centers)

Methodology Note: Built on a transparent, verified supply-and-demand research methodology, this report bridges the gap between macroeconomic trends and actual infrastructure deployments, making it an essential playbook for navigating the Portugal data center ecosystem.

VENDOR LANDSCAPE

- IT INFRASTRUCTURE PROVIDERS: Cisco, Dell Technologies, Everpure, Fujitsu, Hewlett Packard Enterprise, IBM, Inspur, Lenovo, NEC Corporation, NVIDIA, NetApp and Oracle.

- DATA CENTER CONSTRUCTION CONTRACTORS & SUB-CONTRACTORS: ARSMAGNA, Arcadis, ARX Portugal Arquitectos, ACA, Afaconsult, CAP DC, Conduril, DST Group, Gleeds, J.AGOSTINHO SILVA ENGENHARIA, O/M, Proef, Quark and SOMA PARALELA.

- SUPPORT INFRASTRUCTURE PROVIDERS: ABB, Caterpillar, Daikin Applied, Ebm-Papst, Johnson Controls, Legrand, Schneider Electric, and Siemens.

- DATA CENTER INVESTORS: Altice Portugal, AR Telecom, Equinix, NOS Sistemas, REN and Start Campus.

- NEW ENTRANTS: AtlasEdge, Digital Realty, EDC One, Edged, FF Ventures, Quetta Data Centers and Templus.

SNAPSHOT

The Portugal data center market size is projected to reach USD 3.99 billion by 2031, growing at a CAGR of 20% from 2025 to 2031.

The following factors are likely to contribute to the growth of the Portugal data center market

- Growing Adoption of Cloud-based Services

- Improvement in Connectivity through Submarine Cables

- Rise in Automation and Digitalization Trends

Base Year: 2025

Forecast Year: 2026-2031

The report considers the present scenario of the Portugal data center market and its market dynamics for 2026-2031. It covers a detailed overview of several market growth enablers, restraints, and trends. The study includes the demand and supply aspects of the market.

This report also analyses the Portugal data center market share. It elaborately analyses the existing and upcoming facilities and investments in IT, electrical, mechanical infrastructure, general construction, and tier standards. It discusses market sizing and investment estimation for different segments.

The segmentation includes:

- IT Infrastructure

- Servers

- Storage Systems

- Network Infrastructure

- Electrical Infrastructure

- UPS Systems

- Generators

- Transfer Switches & Switchgears

- PDUs

- Other Electrical Infrastructure

- Mechanical Infrastructure

- Cooling Systems

- Rack Cabinets

- Other Mechanical Infrastructure

- Cooling Systems

- CRAC & CRAH Units

- Chiller Units

- Cooling Towers, Condensers & Dry Coolers

- Other Cooling Units

- General Construction

- Core & Shell Development

- Installation & Commissioning Services

- Engineering & Building Design

- Fire Detection & Suppression Systems

- Physical Security

- Data Center Infrastructure Management (DCIM)

- Tier Standard

- Tier I & Tier II

- Tier III

- Tier IV

VENDOR LANDSCAPE

IT Infrastructure Providers

- Cisco

- Dell Technologies

- Everpure

- Fujitsu

- Hewlett Packard Enterprise

- IBM

- Inspur

- Lenovo

- NEC Corporation

- NVIDIA

- NetApp

- Oracle

Data Center Construction Contractors & Sub-Contractors

- ARSMAGNA

- Arcadis

- ARX Portugal Arquitectos

- ACA

- Afaconsult

- CAP DC

- Conduril

- DST Group

- Gleeds

- J.AGOSTINHO SILVA ENGENHARIA

- O/M

- Proef

- Quark

- SOMA PARALELA

Support Infrastructure Providers

- ABB

- Caterpillar

- Daikin Applied

- Ebm-Papst

- Johnson Controls

- Legrand

- Schneider Electric

- Siemens

Data Center Investors

- Altice Portugal

- AR Telecom

- Equinix

- NOS Sistemas

- REN

- Start Campus

New Entrants

- AtlasEdge

- Digital Realty

- EDC One

- Edged

- FF Ventures

- Quetta Data Centers

- Templus

PORTUGAL DATA CENTER MARKET FAQs

How much MW of power capacity will be added across Portugal in 2031?

How big is the Portugal data center market?

What factors are driving the Portugal data center market?

For more details, please reach us at [email protected]

1. CHAPTER 1: EXISTING AND UPCOMING THIRD-PARTY DATA CENTERS IN PORTUGAL

• Data Center Snapshot

• Data Center Snapshot by Cities

• Existing and Upcoming Data Center Supply

• List of Upcoming Data Center Projects in Portugal

2. CHAPTER 2: INVESTMENT OPPORTUNITIES IN PORTUGAL

• Microeconomic & Macroeconomic Factors for Portugal Market

• Impact of AI on Data Center Industry in Portugal

• Investment Opportunities in Portugal

• Digital Data in Portugal

• Market Investments by Area

• Market Investments by Power Capacity

3. CHAPTER 3: DATA CENTER COLOCATION MARKET IN PORTUGAL

• Colocation Services Market in Portugal

• Retail Vs Wholesale Data Center Colocation

• Demand Across Several Industries in Portugal

• Industry Demand Share

• Colocation Pricing (Quarter Rack, Half Rack, and Full Rack) and Addons

4. CHAPTER 4: MARKET DYNAMICS

• Market Enablers

• Market Trends

• Market Restraints

5. CHAPTER 5: MARKET SEGMENTATION

• IT Infrastructure: Market Size & Forecast

• Electrical Infrastructure: Market Size & Forecast

• Mechanical Infrastructure: Market Size & Forecast

• General Construction: Market Size & Forecast

6. CHAPTER 6: TIER STANDARDS INVESTMENT

• Tier I & II

• Tier III

• Tier IV

7. CHAPTER 7: KEY MARKET PARTICIPANTS

• IT Infrastructure Providers

• Construction Contractors and Sub-Contractors

• Support Infrastructure Providers

• Data Center Investors

• New Entrants

8. CHAPTER 8: APPENDIX

• Market Derivation

• Site Selection Criteria

• Quantitative Summary

Select a license type that suits your business needs

Single User Licence

- Report accessible by one user only

- Free 10% or 3 days of customization

- Free post-sale service assistance

- Continuous support through email

5 User Licence

- Report accessible by 5 users within the organization

- Free 15% or 4.5 days of customization

- Continuous support through email and telephone

- Free analyst hour

- Free Upgrade: If an updated report published within 180 days of purchase, you will get the revised report free of charge

Corporate Licence

- Free Datasheet worth $1500

- Report accessible by the entire organization

- Free 20% or 6 days of customization

- Free post-sale service assistance

- Continuous support through email and telephone

- Direct access to lead analysts

- Free analyst hour

- Free Upgrade: If an updated report published within 180 days of purchase, you will get the revised report free of charge

Datasheet Licence

- Report accessible by 1 user only

- Free 15% or 32 hours of customization

- Free post-sale service assistance

- Direct access to lead analysts

Frequently Asked Questions

How much MW of power capacity will be added across Portugal in 2031?

How big is the Portugal data center market?

What factors are driving the Portugal data center market?

Other RELATED Reports

Italy Data Center Market - Investment Analysis & Growth Opportunities 2026-2031

Published : May 2026

Spain Data Center Market - Investment Analysis & Growth Opportunities 2026-2031

Published : May 2026

France Data Center Market - Investment Analysis & Growth Opportunities 2026-2031

Published : April 2026

Finland Data Center Market - Investment Analysis & Growth Opportunities 2026-2031

Published : April 2026