UK Data Center Market - Investment Analysis & Growth Opportunities 2026-2031

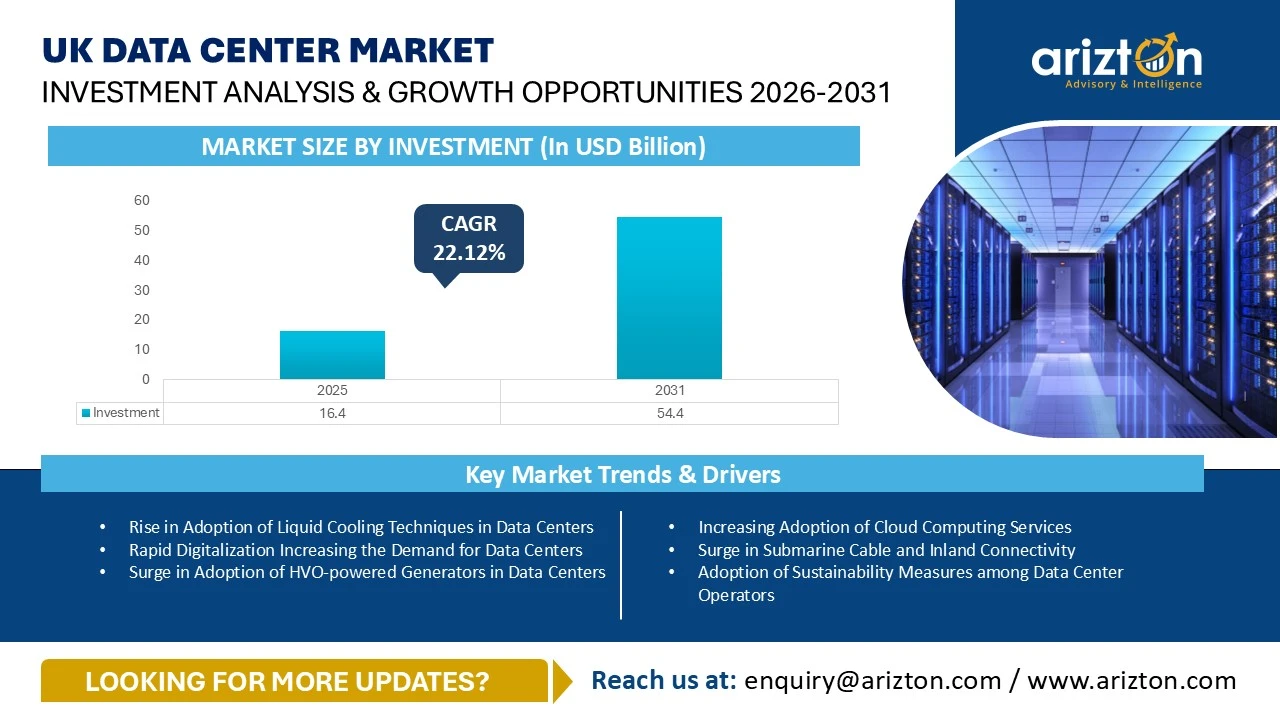

THE UK DATA CENTER MARKET SIZE WAS VALUED AT USD 16.40 BILLION IN 2025 AND IS EXPECTED TO REACH USD 54.40 BILLION BY 2031, GROWING AT A CAGR OF 22.12% DURING THE FORECAST PERIOD.

The UK Data Center Market Size, Share, Trends, & Investments By IT Infrastructure, Electrical Infrastructure, Mechanical Infrastructure, Cooling Systems, General Construction, & Tier Standard. This Industry Analysis Covers The Market Size (in USD Million)

Published Date : April 2026

Last Updated : April 2026

format: PDF

edition : Fourth Edition

187 pages

1 region

1 countries

157 company

7 segments

Purchase Options

UK Data Center Market - Investment Analysis & Growth Opportunities 2026-2031

THE UK DATA CENTER MARKET SIZE WAS VALUED AT USD 16.40 BILLION IN 2025 AND IS EXPECTED TO REACH USD 54.40 BILLION BY 2031, GROWING AT A CAGR OF 22.12% DURING THE FORECAST PERIOD.

The UK Data Center Market Report Includes Size in Terms of

- IT Infrastructure: Servers, Storage Systems, and Network Infrastructure

- Electrical Infrastructure: UPS Systems, Generators, Transfer Switches & Switchgears, PDUs, and Other Electrical Infrastructure

- Mechanical Infrastructure: Cooling Systems, Rack Cabinets, and Other Mechanical Infrastructure

- Cooling Systems: CRAC & CRAH Units, Chiller Units, Cooling Towers, Condensers & Dry Coolers, and Other Cooling Units

- General Construction: Core & Shell Development, Installation & Commissioning Services, Engineering & Building Design, Fire Detection & Suppression Systems, Physical Security, and Data Center Infrastructure Management (DCIM)

- Tier Standard: Tier I & Tier II, Tier III, and Tier IV

- Geography: Greater London and Other Counties

Get Insights on 243 Existing Data Centers and 81 Upcoming Facilities across UK

This report includes market data points, ranging from trend

analyses to market estimates & forecasts that you can customize

UK DATA CENTER MARKET REPORT SCOPE

| REPORT ATTRIBUTE | DETAILS |

|---|---|

| MARKET SIZE (INVESTMENT) | USD 54.40 Billion (2031) |

| MARKET SIZE (AREA) | 3,563.1 Thousand Sq. feet (2031) |

| MARKET SIZE (POWER CAPACITY) | 963 MW (2031) |

| CAGR - INVESTMENT (2025-2031) | 22.12% |

| COLOCATION MARKET SIZE (REVENUE) | USD 10.60 Billion (2031) |

| HISTORIC YEAR | 2022-2024 |

| BASE YEAR | 2025 |

| FORECAST YEAR | 2026-2031 |

UK DATA CENTER MARKET OUTLOOK

The UK data center market size was valued at USD 16.40 billion in 2025 and is expected to reach USD 54.40 billion by 2031, growing at a CAGR of 22.12% during the forecast period. The UK has positioned itself as one of the well-established and developed markets in the European region for the development of data centers. The market is witnessing data center investments from local, as well as global data center companies, driven by increasing artificial intelligence adoption, rapid surge in digitalization, rise in adoption of liquid cooling techniques, surge in submarine and inland connectivity, adoption of sustainability measures among data center operators, increasing adoption of cloud computing services, growing demand for district heating systems, and other growth factors.

The cumulative data center power capacity of the UK data center market is expected to reach to approximately 3,988 MW from 2026 to 2031, because of the increasing demand for data center infrastructure across the country.

The UK government is actively supporting the growth of the data center industry through multiple initiatives, including investments in artificial intelligence infrastructure, establishing strategies to strengthen the digital economy, and offering financial incentives to data center operators. In March 2026, the UK government announced plans to launch a new venture fund of approximately $672 million to accelerate the deployment of AI infrastructure across the country.

Sustainability has emerged as a key priority in the UK data center market, with data center operators increasingly opting for with operators increasingly opting for to minimize carbon emissions. In January 2026, Global Switch entered into a Power Purchase Agreement with a German renewable energy firm, RWE, to procure around 70 GWh of wind energy annually to power Global Switch’s London Docklands data center operations

The UK hosts a strong network of special economic zones, including around nine Freeports across cities such as Humber, Liverpool, Plymouth, Teesside, and Thames, along with approximately 10 operational Industrial Strategy Zones (ISZs). Additionally, there are more than around 48 Enterprise Zones across England, four in Scotland, and seven in Wales, along with multiple industrial parks that offer wide range of advantages to businesses across multiple sectors, including data centers with tax incentives, VAT exemptions, foreign ownership, and access to essential infrastructure like transport, power, water, and network connectivity

The growing adoption of Artificial Intelligence across multiple industries in the United Kingdom is driving strong demand for high-performance computing infrastructure, leading data center operators and technology firms to invest in AI-focused facilities capable of supporting advanced artificial intelligence workloads. In December 2025, Argyll Infrastructure Holdings secured approximately $19.97 million in funding to develop an AI-ready data center in Scotland.

Many enterprises across wide range of sectors are increasingly migrating their workloads to cloud platforms to improve efficiency and enhance their digital service capabilities. For instance, in August 2025, BT Group signed an agreement with Amazon Web Services to transition its legacy systems to AWS’s cloud platform to enhance its digital transformation

Conventional air-cooling systems are unable to handle the intense heat generated by high-density AI racks, leading data center operators to shift toward more advanced cooling solutions. As a result, modern data centers are being designed with liquid cooling technologies for efficient thermal management. For example, the KLON-03 facility of Kao Data will incorporate direct-to-chip liquid cooling, while the LON-East data center operated by Green Mountain has been designed with the flexibility to integrate liquid cooling systems in the future based on customer requirements.

UK DATA CENTER MARKET - KEY HIGHLIGHTS

- The UK consists of around 243 operational third-party data centers, of which around 74 data centers are located in the Greater London County. The country is also witnessing the development of around 82 new data centers, which are either in planned or under construction stages

- The cloud market in the UK is projected to experience strong growth over the forecast period, driven by the continuous investments from major global cloud service providers such as Amazon Web Services, Microsoft, Google, Oracle Cloud, and Tencent. For instance, in December 2025, Amazon Data Services, a subsidiary of Amazon Web Services, acquired a former coal plant site in the UK from RWE for approximately $265 million to develop a new data center

- The rack density of traditional data center racks is inadequate for supporting modern AI and high-performance computing workloads. Therefore, data center operators are shifting toward high-density infrastructure, deploying racks exceeding 100 kW to efficiently handle advanced computing requirements. For example, the KLON-03 facility being developed by Kao Data in Harlow is designed to support rack power densities of over 130 kW per rack

- In the UK, data protection and privacy compliance are regulated by the Information Commissioner's Office, which ensures that data center operators and cloud providers strictly follow legal frameworks such as the UK’s General Data Protection Regulation to implement robust data privacy standards. Following Brexit, the UK developed its own independent data protection framework, based on the Data Protection Act 2018.

- In the UK, several data center operators are connecting data centers to the district heating networks to repurpose the waste heat generated in data centers to enhance sustainability across the nation. For example, In July 2025, Deep Green, the data center operator planned to develop two-story data center in Bradford, West Yorkshire that will be connected to the Yorkshire’s district heating network to repurpose data center’s waste heat.

- In July 2025, the Home Office in the UK introduced the Home Office 2030 Digital Strategy to enhance public safety and strengthen digital infrastructure security by encouraging enterprises to adopt digital technologies, data, and artificial intelligence.

- In March 2024, the Foreign, Commonwealth & Development Office in the United Kingdom launched the Digital Development Strategy 2024–2030 to strengthen the country’s global position in digital infrastructure by promoting digital transformation, expanding connectivity, and encouraging adoption of artificial intelligence among individuals and businesses.

- In January 2026, insurance providers in the UK, such as, FM Global and Aon, expanded their coverage offerings to support the growing data center sector. During the same period, Advanced Technology Assurance introduced an AI-focused insurance facility, which has been designed to support risks such as system failures, data loss, performance issues, and liabilities associated with AI operations in UK data centers

- In January 2026, parliaments in the UK established the Data Centres APPG (All-Party Parliamentary Group), a cross-party initiative to enhance understanding of the data center sector and evaluate its role in driving economic growth, strengthen digital infrastructure resilience, and support the country’s net zero sustainability objectives

WHY SHOULD YOU BUY THIS RESEARCH?

- Market size available in the investment, area, power capacity, and UK colocation market revenue.

- An assessment of the data center investment in UK by colocation, hyperscale, and enterprise operators.

- Data center investments in the area (square feet) and power capacity (MW) across counties in the country.

- A detailed study of the existing UK data center market landscape, an in-depth industry analysis, and insightful predictions about the UK data center market size during the forecast period.

- Snapshot of existing and upcoming third-party data center facilities in UK

- Facilities Covered (Existing): 243

- Facilities Identified (Upcoming): 81

- Coverage: 34+ Locations

- Existing vs. Upcoming (Data Center Area)

- Existing vs. Upcoming (IT Load Capacity)

- Data center colocation market in UK

- Colocation Market Revenue & Forecast (2022-2031)

- Retail & Wholesale Colocation Revenue (2022-2031)

- Retail & Wholesale Colocation Pricing

- UK data center landscape market investments are classified into IT, power, cooling, and general construction services with sizing and forecast.

- A comprehensive analysis of the latest trends, growth rate, potential opportunities, growth restraints, and prospects for the industry.

- Business overview and product offerings of prominent IT infrastructure providers, construction contractors, support infrastructure providers, and investors operating in the industry.

UK DATA CENTER MARKET VENDOR LANDSCAPE

- The UK has the presence of major global cloud service providers, including, Alibaba Group, Amazon Web Services, Google, Microsoft, Oracle, OVHcloud, and other cloud companies. The cloud companies have been expanding their service offerings across the UK to address increasing demand for cloud and artificial intelligence infrastructure. In September 2025, Google inaugurated a new data center in Hertfordshire, the UK to enhance UK’s cloud infrastructure.

- The colocation companies account for majority of data center investments in the country. The UK has the presence of multiple local and global colocation service providers, including, Ark Data Centres, AtlasEdge, Colt Data Centre Services, CyrusOne, Datum Datacentres, Digital Realty, Echelon Data Centres, Equinix, Global Switch, Global Technical Realty, Green Mountain, Iron Mountain, Kao Data, Lunar Digital, nLighten, NTT DATA, Pure Data Centres Group, Telehouse, Vantage Data Centers, VIRTUS Data Centres, Yondr Group, and others.

- Several new entrants are expanding their footprints in the UK data center market to address the increasing demand for data center infrastructure in the nation. Some of the new entrants in the UK include, Ada Infrastructure, SWI Group, Apatura, Caineal LLP, CloudHQ, Corscale Data Centers, Deep Green, Digital Reef, Drax Group, EID LLP, Greystoke, Latos Data Centres, Northtree Investment Management, Nscale, Pinewood Group, QTS Data Centers, SineQN, Valore Group, Wilton International, Wycombe Film Studios, and others.

- The UK has the presence of multiple local, as well as global support infrastructure providers that supply power, cooling, and general infrastructure components to data centers. Some of the prominent support infrastructure providers operating in the UK include, ABB, AF Switchgear, Airedale, Alfa Laval, AVK, Baudouin, Caterpillar, Cummins, Cyber Power Systems, Delta Electronics, Eaton, Hitachi Energy, Honeywell, Legrand, Mitsubishi Electric, Piller Power Systems, Rittal, Rolls Royce, Schneider Electric, Siemens, STULZ, Trane, Vertiv, Submer, and others.

- The country hosts multiple construction contractors that provide construction, installation, commissioning, designing, architectural, and engineering services for the construction of data centers. Some of the prominent construction contractors in the UK data center market include, 2bm, AECOM, Acies Civil and Structural, Arup, AtkinsRéalis, BladeRoom Data Centres, Future-tech, JCA Engineering, JSM Group Services, Kirby Group Engineering, Laing O'Rourke, Mace, Mercury, Ramboll, RED Engineering Design, Skanska, STO Building Group, studioNWA, Sweet Projects, Turner & Townsend, and McLaren Construction Group.

- The UK consists of multiple IT infastructure providers that offer servers, storage systems, and networking equipment to data centers. Multiple IT infrastructure providers, including Arista Networks, Atos, Broadcom, Cisco, Dell Technologies, Fujitsu, Hewlett Packard Enterprise, Huawei Technologies, IBM, Lenovo, NetApp, NVIDIA, and other companies have a strong presence across the UK.

EXISTING VS. UPCOMING DATA CENTERS

- Existing Facilities in the region (Area and Power Capacity)

- Greater London

- Berkshire

- Greater Manchester

- Other Counties

- List of Upcoming Facilities in the region (Area and Power Capacity)

- Greater London

- Berkshire

- Greater Manchester

- Other Counties

REPORT COVERAGE:

This report analyses the UK data center market share. It elaboratively analyses the existing and upcoming facilities and investments in IT, electrical, mechanical infrastructure, cooling systems, general construction, and Tier standards. It discusses market sizing and investment estimation for different segments. The segmentation includes:

- IT Infrastructure

- Server Infrastructure

- Storage Infrastructure

- Network Infrastructure

- Electrical Infrastructure

- UPS Systems

- Generators

- Switches & Switchgears

- PDUs

- Other Electrical Infrastructure

- Mechanical Infrastructure

- Cooling Systems

- Rack Cabinets

- Other Mechanical Infrastructure

- Cooling Systems

- CRAC and CRAH

- Chillers

- Cooling Towers, Condensers and Dry Coolers

- Other Cooling Units

- General Construction

- Core & Shell Development

- Installation & commissioning Services

- Building & Engineering Design

- Fire Detection & Suppression Systems

- Physical Security

- Data Center Infrastructure Management (DCIM)

- Tier Standard

- Tier I & Tier II

- Tier III

- Tier IV

- Geography

- Greater London

- Other Counties

VENDOR LANDSCAPE

- IT INFRASTRUCTURE PROVIDERS: Arista Networks, Atos, Broadcom, Cisco, Dell Technologies, Fujitsu, Hewlett Packard Enterprise, Huawei Technologies, IBM, Lenovo, NetApp, and NVIDIA.

- DATA CENTER CONSTRUCTION CONTRACTORS & SUB-CONTRACTORS: 2bm, Acies Civil and Structural, AECOM, ARC:MC, Arup, AtkinsRéalis, BladeRoom Data Centres, Bouygues Construction, Collen Construction, Colliers, Deerns UK, Flynn, Future-tech, HDR, H&MV Engineering, INFINITI IT, JCA Engineering, John Paul Construction, JSM Group Services, Kirby Group Engineering, Laing O'Rourke, Mace, Mercury, MiCiM, Ramboll, RED Engineering Design, Skanska, Dalkia UK, STO Building Group, studioNWA, Sudlows, Sweet Projects, TTSP, Turner & Townsend, Morson Praxis, and McLaren Construction Group.

- SUPPORT INFRASTRUCTURE PROVIDERS: ABB, AF Switchgear, Aggreko, Airedale, Alfa Laval, AVK, Baudouin, Caterpillar, Cummins, Cyber Power Systems, Delta Electronics, Dew Point Systems, Eaton, Hitachi Energy, Honeywell, Legrand, Mitsubishi Electric, Piller Power Systems, Rehlko, Riello Elettronica Group, Rittal, Rolls Royce, Schneider Electric, Siemens, Socomec Group, STULZ, Trane, Vertiv, Submer, Castrol, ENGIE, and Flex-Tek.

- DATA CENTER INVESTORS: Amazon Web Services, Ark Data Centers, AtlasEdge, Castleforge & Galaxy Data Centers, Colt Data Centre Services, CyrusOne, DataVita, Datum Datacentres, Digital Realty, Echelon Data Centres, Equinix, Global Switch, Global Technical Realty, Google, Green Mountain, Iron Mountain, Kao Data, Lunar Digital, Microsoft, Netwise, nLighten, NTT DATA, Pure Data Centres Group, SUB1 Data Centres, Telehouse, Vantage Data Centers, VIRTUS Data Centres, and Yondr Group.

- NEW ENTRANTS: Ada Infrastructure, AI Pathfinder, SWI Group (AiOnX platform), Anglesey Land Holdings, Apatura, Caineal LLP, Era4 (Carbon3.ai), CloudHQ, Corscale Data Centers, Dante Group, Deep Green, Digital Reef, Digital Land & Development, Drax Group, EdgeNebula, EID LLP, Elite UK REIT, Greenweaver, Greystoke, ILI Group, Kennedy Wilson, Latos Data Centres, Link Park Heathrow, MSAI - Media StreamAI, Northtree Investment Management, Norwich Research Park, Nscale, Origin Energy Services & Woodlands Investment Management, Pathfinder Clean Energy (PACE), PATRIZIA SE, Pinewood Group, QTS Data Centers, SEGRO plc, Shelborn, SineQN, Teesworks, Tritax Big Box, Truman Estates, Valore Group, WESTERN BIO-ENERGY, Wilton International, and Wycombe Film Studios.

SNAPSHOT

The UK data center market size is projected to reach USD 54.40 billion by 2031, growing at a CAGR of 22.12% from 2025 to 2031.

The following factors are likely to contribute to the growth of the UK data center market

- Increasing Adoption of Cloud Computing Services

- Surge in Submarine Cable and Inland Connectivity

- Adoption of Sustainability Measures among Data Center Operators

Base Year: 2025

Forecast Year: 2026-2031

The report considers the present scenario of the UK data center market and its market dynamics for 2026-2031. It covers a detailed overview of several market growth enablers, restraints, and trends. The study includes the demand and supply aspects of the market.

This report also analyses the UK data center market share. It elaborately analyses the existing and upcoming facilities and investments in IT, electrical, mechanical infrastructure, general construction, and tier standards. It discusses market sizing and investment estimation for different segments.

The segmentation includes:

- IT Infrastructure

- Servers

- Storage Systems

- Network Infrastructure

- Electrical Infrastructure

- UPS Systems

- Generators

- Transfer Switches & Switchgears

- PDUs

- Other Electrical Infrastructure

- Mechanical Infrastructure

- Cooling Systems

- Rack Cabinets

- Other Mechanical Infrastructure

- Cooling Systems

- CRAC & CRAH Units

- Chiller Units

- Cooling Towers, Condensers & Dry Coolers

- Other Cooling Units

- General Construction

- Core & Shell Development

- Installation & Commissioning Services

- Engineering & Building Design

- Fire Detection & Suppression Systems

- Physical Security

- Data Center Infrastructure Management (DCIM)

- Tier Standard

- Tier I & Tier II

- Tier III

- Tier IV

- Geography

- Greater London

- Other Cities

VENDOR LANDSCAPE

IT Infrastructure Providers

- Arista Networks

- Atos

- Broadcom

- Cisco

- Dell Technologies

- Fujitsu

- Hewlett Packard Enterprise

- Huawei Technologies

- IBM

- Lenovo

- NetApp

- NVIDIA

Data Center Construction Contractors & Sub-Contractors

- 2bm

- Acies Civil and Structural

- AECOM

- ARC:MC

- Arup

- AtkinsRéalis

- BladeRoom Data Centres

- Bouygues Construction

- Collen Construction

- Colliers

- Deerns UK

- Flynn

- Future-tech

- HDR

- H&MV Engineering

- INFINITI IT

- JCA Engineering

- John Paul Construction

- JSM Group Services

- Kirby Group Engineering

- Laing O'Rourke

- Mace

- Mercury

- MiCiM

- Ramboll

- RED Engineering Design

- Skanska

- Dalkia UK

- STO Building Group

- studioNWA

- Sudlows

- Sweet Projects

- TTSP

- Turner & Townsend

- Morson Praxis

- McLaren Construction Group

Support Infrastructure Providers

- ABB

- AF Switchgear

- Aggreko

- Airedale

- Alfa Laval

- AVK

- Baudouin

- Caterpillar

- Cummins

- Cyber Power Systems

- Delta Electronics

- Dew Point Systems

- Eaton

- Hitachi Energy

- Honeywell

- Legrand

- Mitsubishi Electric

- Piller Power Systems

- Rehlko

- Riello Elettronica Group

- Rittal

- Rolls-Royce

- Schneider Electric

- Siemens

- Socomec Group

- STULZ

- Trane

- Vertiv

- Submer

- Castrol

- ENGIE

- Flex-Tek

Data Center Investors

- Amazon Web Services

- Ark Data Centers

- AtlasEdge

- Castleforge & Galaxy Data Centers

- Colt Data Centre Services

- CyrusOne

- DataVita

- Datum Datacentres

- Digital Realty

- Echelon Data Centres

- Equinix

- Global Switch

- Global Technical Realty

- Green Mountain

- Iron Mountain

- Kao Data

- Lunar Digital

- Microsoft

- Netwise

- nLighten

- NTT DATA

- Pure Data Centres Group

- SUB1 Data Centres

- Telehouse

- Vantage Data Centers

- VIRTUS Data Centres

- Yondr Group

New Entrants

- Ada Infrastructure

- AI Pathfinder

- SWI Group (AiOnX platform)

- Anglesey Land Holdings

- Apatura

- Caineal LLP

- Era4 (Carbon3.ai)

- CloudHQ

- Corscale Data Centers

- Dante Group

- Deep Green

- Digital Reef

- Digital Land & Development

- Drax Group

- EdgeNebula

- EID LLP

- Elite UK REIT

- Greenweaver

- Greystoke

- ILI Group

- Kennedy Wilson

- Latos Data Centres

- Link Park Heathrow

- MSAI – Media StreamAI

- Northtree Investment Management

- Norwich Research Park

- Nscale

- Origin Energy Services & Woodlands Investment Management

- Pathfinder Clean Energy (PACE)

- PATRIZIA SE

- Pinewood Group

- QTS Data Centers

- SEGRO plc

- Shelborn

- SineQN

- Teesworks

- Tritax Big Box

- Truman Estates

- Valore Group

- WESTERN BIO-ENERGY

- Wilton International

- Wycombe Film Studios

UK DATA CENTER MARKET FAQs

How big is the UK data center market?

How much MW of power capacity will be added across UK during 2026-2031?

Which all geographies are included in UK data center market report?

What factors are driving the UK data center market?

For more details, please reach us at [email protected]

1. CHAPTER 1: EXISTING & UPCOMING THIRD-PARTY DATA CENTERS IN THE UK

• Data Center Snapshot

• Data Center Snapshot by Counties

• Existing & Upcoming Data Center Supply

• List of Upcoming Data Center Projects in the UK

2. CHAPTER 2: INVESTMENT OPPORTUNITIES IN THE UK

• Microeconomic & Macroeconomic Factors for the UK Market

• Impact of AI in Data Center Industry in UK

• Investment Opportunities in UK

• Digital Landscape in UK

• Government Support for Data Centers

• Government Rules & Regulations

• Market Investment by Area

• Market Investment by Power Capacity

3. CHAPTER 3: DATA CENTER COLOCATION MARKET IN THE UK

• Colocation Services Market in The UK

• Retail vs Wholesale Data Center Colocation

• Colocation Pricing (Quarter Rack, Half Rack & Full Rack) & Addons

4. CHAPTER 4: MARKET DYNAMICS

• Market Enablers

• Market Trends

• Market Restraints

5. CHAPTER 5: MARKET SEGMENTATION

• IT Infrastructure: Market Size & Forecast

• Electrical Infrastructure: Market Size & Forecast

• Mechanical Infrastructure: Market Size & Forecast

• General Construction: Market Size & Forecast

• Break-up of Construction Cost

6. CHAPTER 6: TIER STANDARDS INVESTMENT

• Tier I & II

• Tier III

• Tier IV

7. CHAPTER 7: GEOGRAPHY SEGMENTATION

• Greater London

• Other Counties

8. CHAPTER 8: KEY MARKET PARTICIPANTS

• IT Infrastructure Providers

• Construction Contractors & Sub-Contractors

• Support Infrastructure Providers

• Data Center Investors

• New Entrants

9. CHAPTER 9: APPENDIX

• Market Derivation

• Site Selection Criteria

• Quantitative Summary

• Abbreviations

Select a license type that suits your business needs

Single User Licence

- Report accessible by one user only

- Free 10% or 3 days of customization

- Free post-sale service assistance

- Continuous support through email

5 User Licence

- Report accessible by 5 users within the organization

- Free 15% or 4.5 days of customization

- Continuous support through email and telephone

- Free analyst hour

- Free Upgrade: If an updated report published within 180 days of purchase, you will get the revised report free of charge

Corporate Licence

- Free Datasheet worth $1500

- Report accessible by the entire organization

- Free 20% or 6 days of customization

- Free post-sale service assistance

- Continuous support through email and telephone

- Direct access to lead analysts

- Free analyst hour

- Free Upgrade: If an updated report published within 180 days of purchase, you will get the revised report free of charge

Datasheet Licence

- Report accessible by 1 user only

- Free 15% or 32 hours of customization

- Free post-sale service assistance

- Direct access to lead analysts

Frequently Asked Questions

How big is the UK data center market?

How much MW of power capacity will be added across UK during 2026-2031?

Which all geographies are included in UK data center market report?

What factors are driving the UK data center market?

Other RELATED Reports

France Data Center Market - Investment Analysis & Growth Opportunities 2026-2031

Published : April 2026

Ireland Data Center Market – Investment Analysis & Growth Opportunities 2026-2031

Published : April 2026

Finland Data Center Market - Investment Analysis & Growth Opportunities 2026-2031

Published : April 2026

Sweden Data Center Market - Investment Analysis & Growth Opportunities 2026-2031

Published : April 2026