U.S. Construction Equipment Market Research Report 2026-2031

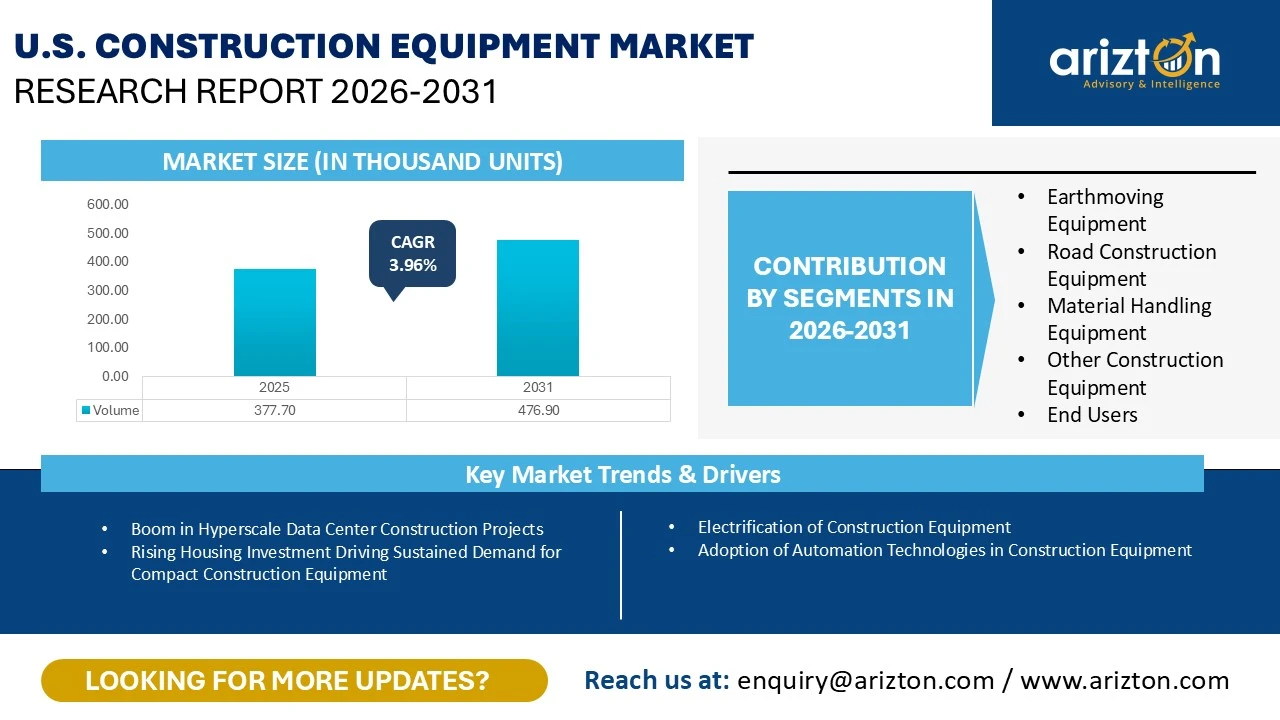

THE U.S. CONSTRUCTION EQUIPMENT MARKET SIZE WAS ESTIMATED AT 377.7 THOUSAND UNITS IN 2025 AND IS EXPECTED TO REACH 476.9 THOUSAND UNITS BY 2031, GROWING AT A CAGR OF 3.96%

U.S. Construction Equipment Market Size & Share By Earthmoving Equipment, Road Construction Equipment, Material Handling Equipment, Other Equipment, End Users. The Report Provides Sales Volume in Thousands of Units and Revenue in USD Million

Published Date : May 2026

Last Updated : May 2026

format: PDF

edition : Third Edition

178 pages

42 company

5 segments

1 region

1 countries

Purchase Options

U.S. Construction Equipment Market Research Report 2026-2031

THE U.S. CONSTRUCTION EQUIPMENT MARKET SIZE WAS ESTIMATED AT 377.7 THOUSAND UNITS IN 2025 AND IS EXPECTED TO REACH 476.9 THOUSAND UNITS BY 2031, GROWING AT A CAGR OF 3.96%

The U.S. Construction Equipment Market Research Report Includes Segments By

- Earthmoving Equipment: Excavator, Backhoe Loaders, Wheeled Loaders, and Other Earthmoving Equipment (Other Loaders, Bulldozers, Trenchers, and Motor Graders)

- Road Construction Equipment: Road Rollers and Asphalt Pavers

- Material Handling Equipment: Crane, Forklift & Telescopic Handlers, and Aerial Platforms (Articulated Boom Lifts, Telescopic Boom lifts, and Scissor lifts)

- Other Construction Equipment: Dumper, Concrete Mixer, and Concrete Pump Truck

- End Users: Construction, Mining, Manufacturing, and Other End Users

Industry Analysis Report, Regional Outlook, Growth Potential, Price Trends, Competitive Market Share & Forecast 2026–2031.

This report includes market data points, ranging from trend

analyses to market estimates & forecasts that you can customize

U.S. CONSTRUCTION EQUIPMENT MARKET REPORT SCOPE

| REPORT ATTRIBUTE | DETAILS |

|---|---|

| MARKET SIZE- VOLUME (2031) | 476.9 Thousand Units |

| MARKET SIZE- VOLUME (2025) | 377.7 Thousand Units |

| CAGR- VOLUME (2025-2031) | 3.96% |

| MARKET SIZE- REVENUE (2031) | USD 83.89 Billion |

| HISTORIC YEAR | 2022-2024 |

| BASE YEAR | 2025 |

| FORECAST YEAR | 2026-2031 |

| EQUIPMENT TYPE | Earthmoving Equipment, Road Construction Equipment, Material Handling Equipment, and Other Equipment |

| END-USERS | Construction, Mining, Manufacturing, and Others |

| KEY VENDORS | Caterpillar, Komatsu, Deere & Company, Volvo CE, Liebherr, Hitachi Construction Machinery, SANY, CNH Industrial, XCMG, HD Hyundai Construction Equipment, Kobelco, Zoomlion, Kubota, and Bobcat |

U.S. CONSTRUCTION EQUIPMENT MARKET SIZE

The U.S. construction equipment market size was estimated at 377.7 thousand units in 2025 and is expected to reach 476.9 thousand units by 2031, growing at a CAGR of 3.96% during the forecast period. Growth over the forecast period is expected to remain steady, supported by substantial public infrastructure spending, private capital investment, and rapid advancements in construction technologies.

In the U.S., in 2026, federal infrastructure funding remains a major driver of demand, particularly through the Infrastructure Investment and Jobs Act (IIJA), also known as the Bipartisan Infrastructure Law, enacted in 2021. In parallel, the market is being significantly boosted by the rapid expansion of AI-driven data center construction

At the same time, sustained activity in residential construction, renewable energy installations, semiconductor fabrication facilities, and port modernization projects is ensuring consistent, multi-year demand across diverse equipment categories.

Despite these strong growth fundamentals, the industry faces several structural headwinds. A persistent skilled labour shortage continues to disrupt project timelines and increase labour costs, compounded by an ageing workforce. Additionally, elevated interest rates are raising borrowing costs, prompting many contractors, especially smaller firms, to delay new equipment purchases or shift toward the used equipment market.

U.S. CONSTRUCTION EQUIPMENT MARKET KEY HIGHLIGHTS

- Earthmoving equipment accounted for the largest market share of around 54% in the U.S. construction equipment market in 2025. Compact earthmoving equipment (skid-steer, track loaders, mini-excavators) in the earthmoving segment accounted for the largest share in 2025.

- Compact track loaders (CTLs) have increasingly overtaken skid-steer loaders as the machine of choice for many U.S. contractors, driven by their superior traction, flotation, and pushing capability on soft or uneven ground. They are widely used in site preparation, grading, land clearing, utility installation, and forestry applications, experiencing strong growth due to rising demand from data center developments, solar farm projects, and residential subdivision grading in 2026.

- Kubota unveiled its largest CTL, the SVL110-3, at ConExpo 2026, expanding its Dash-3 Series lineup. The machine delivers 112.7 gross horsepower, 279.8 lb-ft of torque, 45 gpm hydraulic flow, and a rated operating capacity of 3,700 pounds.

- In addition, in 2026, OTR Engineered Solutions introduced the TrackBoss E5 rubber track for CTLs, engineered to optimise ride comfort, traction, and ground protection.

- On the other hand, demand for material handling & lifting equipment is also growing. Forklifts remain the most extensively used material handling equipment in the U.S., with widespread deployment across logistics hubs, manufacturing plants, ports, warehouses, and construction sites. The rapid expansion of e-commerce, along with the development of large-scale distribution networks, has been a primary driver of growth in the U.S. forklift market.

- Forklifts remain the most extensively used material handling equipment in the United States, with widespread deployment across logistics hubs, manufacturing plants, ports, warehouses, and construction sites. The rapid expansion of e-commerce, along with the development of large-scale distribution networks, has been a primary driver of growth in the US forklift market.

- The road construction equipment segment is projected to grow at a CAGR of 3.46% from 2025 to 2031.

- The surge in large-scale U.S. highway projects underway in 2026 is directly translating into rising demand for road construction equipment, as contractors mobilize fleets to meet tight delivery timelines and federally backed infrastructure targets.

- Asphalt pavers rank among the most capital-intensive and specialized machines in road construction, playing a critical role in laying the surface layer that determines pavement quality and durability. In the U.S., demand for paving equipment is closely tied to public sector spending, with government-funded highway projects accounting for the majority of usage.

- In 2026, BOMAG introduced its 8-foot CR802T-2 rubber-track paver at the 2025 World of Asphalt in St. Louis, targeting contractors moving into larger-scale paving jobs. The model features a 10-ton hopper, a 173-horsepower engine, and variable paving widths of up to 16 feet.

- In 2025, the construction segment accounted for around 42% of the construction equipment usage market in the US construction industry. The segment is projected to expand at a CAGR of 4.10%.

- In January 2026, public construction spending reached a seasonally adjusted annual rate of $529.2 billion, marking a 0.6% increase over December 2025 and signalling rising utilization of construction equipment across infrastructure projects. Higher activity levels are driving demand for earthmoving machinery, roadbuilding equipment, and material handling solutions.

- The U.S. manufacturing sector is a key driver of construction equipment demand, supported by factory expansions, reshoring initiatives, and large-scale industrial projects incentivized by policies such as the CHIPS and Science Act. These developments require extensive site preparation, grading, and infrastructure upgrades, thereby increasing demand for heavy machinery, including excavators, loaders, dozers, and cranes.

- The U.S. mining industry is witnessing a steady rise in the use of construction equipment, driven by its scale, diversification, and ongoing technological transformation. According to the United States Geological Survey, the country hosts more than 11,000 active mines, ranging from sand and gravel operations to coal and gold mines—each requiring extensive deployment of heavy equipment for extraction, hauling, and site development.

- Additionally, initiatives such as “Make More in America” and expanded financing from the U.S. International Development Finance Corporation are channelling investment into mining, refining, and smelting projects. These efforts aim to reduce dependence on Chinese supply chains while simultaneously boosting demand for construction and material handling equipment across the mining value chain.

U.S. CONSTRUCTION EQUIPMENT MARKET DRIVERS

Booming Construction Activity-Peak Disbursement of the Bipartisan Infrastructure Law (IIJA)

- The Infrastructure Investment and Jobs Act (IIJA) is significantly boosting demand for construction equipment in the U.S. through nearly $973 billion in infrastructure funding between 2022 and 2026, including $550 billion in new investments.

- Transportation projects, particularly roads, bridges, highways, railways, airports, and ports, are driving strong demand for earthmoving, roadbuilding, and material-handling equipment such as excavators, cranes, bulldozers, and telescopic handlers.

- Additional investments in energy, broadband, water infrastructure, and EV charging networks are expanding demand for compact machinery and utility equipment. As projects enter peak execution in 2026, equipment utilisation and long-term market growth continue to strengthen across diverse infrastructure applications.

Boom in Hyperscale Data Center Construction Projects

- The rapid expansion of AI and cloud computing infrastructure is significantly increasing demand for construction equipment in the U.S. data center sector in 2026.

- Strong investments from major technology companies, including Google, Amazon, OpenAI, Microsoft, Meta, and Oracle, are accelerating large-scale data center construction across both established and emerging markets.

- U.S. data center construction starts reached approximately $103.7 billion through January 2026, following a 190% surge in 2025. This growth is driving higher utilization of earthmoving machinery, cranes, concrete equipment, and power installation systems. Key investment hubs include Virginia, Texas, Louisiana, and Mississippi, supporting sustained long-term growth in construction equipment demand nationwide.

Rising Housing Investment Driving Sustained Demand for Compact Construction Equipment

- The persistent U.S. housing shortage is emerging as a major long-term driver of residential construction and compact construction equipment demand through 2031. Rising public and private investments, combined with population growth and household formation, are sustaining strong housing development activity.

- In 2026, federal support increased significantly through housing-focused legislation and the $77.3 billion HUD allocation under the THUD bill. Housing starts reached an annualized 1.49 million units in January 2026, up 9.5% year-over-year, with multifamily construction remaining strong.

- Affordable housing projects, including Chicago’s $300 million initiative, are further boosting demand for compact machinery used in site preparation, material handling, and urban construction activities.

U.S. CONSTRUCTION EQUIPMENT MARKET TRENDS

Electrification of Construction Equipment

- Electrification is emerging as a major long-term trend in the U.S. construction machinery industry, driven by sustainability goals, regulatory pressure, and cost efficiency benefits. EPA Tier 4 Final standards and Phase 3 greenhouse gas regulations are accelerating the shift toward low- and zero-emission equipment, while California’s proposed Tier 5 standards are expected to further tighten emission requirements.

- OEMs are increasingly commercializing electric machinery, particularly in compact and mid-sized segments. At the 2026 CONEXPO-CON/AGG event, companies such as CASE Construction Equipment, HD Hyundai Construction Equipment and Takeuchi showcased new electric equipment models.

- Advancements in lithium-ion battery technology are further supporting wider adoption across urban and emissions-sensitive construction applications.

Adoption of Automation Technologies in Construction Equipment

- The US construction sector is rapidly adopting automated and autonomous equipment to improve productivity, precision, and jobsite safety amid ongoing labour shortages and rising project complexity.

- Major OEMs are integrating AI, machine learning, computer vision, and real-time monitoring into construction machinery.

- At the 2026 CONEXPO event, Caterpillar introduced autonomous excavators, loaders, haul trucks, dozers, and compactors developed with NVIDIA-powered technologies. John Deere, Hitachi Construction Machinery, Bedrock Robotics, and Built Robotics are also expanding AI-enabled and retrofit autonomy solutions.

- These advancements are accelerating the transition toward digitally connected and autonomous construction operations across the U.S. industry.

Accelerating Adoption of Compact Track Loaders in the U.S. Construction Equipment Market

- The US construction equipment market is experiencing a strong shift toward compact track loaders (CTLs), which are increasingly replacing skid steer loaders due to their superior versatility, lower ground pressure, and improved operator comfort.

- CTL sales grew from about 21,500 units in 2012 to over 90,000 units in 2022, while skid steer demand declined. Financing trends between 2024 and 2025 further confirm a rising preference for CTLs.

- Manufacturers such as Kubota, HD Hyundai Construction Equipment, Yanmar, and Caterpillar are expanding product portfolios and investments, reinforcing CTLs as one of the fastest-growing segments in the U.S. construction equipment market.

INDUSTRY RESTRAINTS

Persistently Elevated Interest Rates and Tightened Financing Conditions

- Elevated interest rates are acting as a major structural constraint on the U.S. construction equipment market by reducing equipment purchases, delaying project launches, and weakening private-sector construction activity.

- Following the Federal Reserve’s aggressive rate hikes since 2022, borrowing costs remain significantly higher in 2026 despite moderate rate cuts. Tight financing conditions and stricter lending standards are particularly affecting multifamily housing and commercial real estate projects, limiting new construction pipelines.

- Higher financing costs are also increasing dealer inventory expenses and reducing purchasing power for small and mid-sized contractors.

- As a result, subdued construction activity and cautious investment decisions are expected to continue placing downward pressure on construction equipment demand through 2026.

Construction Workforce Shortage

- The persistent shortage of skilled labour is emerging as a major structural challenge for the U.S. construction equipment market in 2026, limiting project execution capacity and reducing demand for new machinery.

- According to the Associated Builders and Contractors, the industry will require an additional 349,000 workers in 2026 and 456,000 in 2027 to meet construction demand.

- Ageing workers, rising retirements, demographic imbalances, and immigration uncertainty are further tightening labour availability, particularly for operators of complex machinery. Higher labor costs and workforce instability are also reducing contractor profitability, delaying projects, and encouraging a shift toward equipment rentals rather than direct purchases, thereby suppressing overall construction equipment demand.

U.S. CONSTRUCTION EQUIPMENT MARKET VENDOR LANDSCAPE

- Caterpillar, Liebherr, Komatsu, John Deere, CNH Industrial, Kubota, Volvo CE, and Bobcat are the front-runners in the country’s construction equipment market. These companies have strong market share and offer a diverse set of equipment in the U.S. market.

- Terex, JLG, Yanmar, Manitowoc Cranes, Manitou Group, Toyota Material Handling, and Wacker Neuson are niche market players in the market. These companies offer low product diversification and have a strong presence in the U.S. market.

- Hitachi Construction Machinery, SANY, Takeuchi, DEVELON, XCMG, JCB, Zoomlion, Kobelco, and HD Hyundai Construction Equipment are emerging in the market. These companies are introducing new technologically advanced products to challenge the market share of market leaders in the US market.

- LiuGong, Ammann Group, Link-Belt Cranes, Mecalac, Tadano, and GEHL have low product diversification; these companies are lagging in adopting new technologies used in construction equipment.

- At the CES 2026, Caterpillar showcased a new generation of AI-powered and autonomous technologies. The company introduced an AI Assistant and unveiled advanced equipment across key categories—including excavators, loaders, haul trucks, dozers, and compactors—leveraging NVIDIA-driven AI and edge computing capabilities.

- In February 2026, Komatsu announced its acquisition of the assets of SRC of Lexington, expanding its remanufacturing footprint in North America. The deal deepens Komatsu's reman capabilities closer to U.S. customers, improving responsiveness and supporting dealers with high-quality, cost-effective lifecycle solutions.

- Volvo Construction Equipment (Volvo CE) announced the launch of the new SD70 soil compactor, the latest addition to its industry-leading soil compaction range, at CONEXPO-CON/AGG 2026.

- The two new Liebherr wheeled excavators, A 909 Compact and A 911 Compact Litronic have been honoured with the world-renowned iF DESIGN AWARD 2026. The A 909 Compact and A 911 Compact are two powerful machines that set new standards in their respective classes and offer customers an optimum solution for demanding applications.

- SANY America was named a recipient of the Specialized Carriers & Rigging Association (SC&RA) 5-Year Longevity Award, recognizing the company’s sustained membership and dedication to the association’s mission.

- SANY America announced new excavator launches (SY135C Fixed Boom Excavator, SY155U Fixed Boom Excavator, SY235H Medium Hydraulic Excavator, SY385C Large Hydraulic Excavator and other) targeting utilities and grade control applications at ConExpo-Con/AGG 2026.

- Kubota Corporation announced the launch of the SVL110-3, the largest model in its compact track loader (CTL) product lineup, for the North American market. The new model was showcased at CONEXPO-CON/AGG 2026.

- In 2025, Caterpillar surpassed Kubota to emerge as the leading seller of newly financed equipment across U.S., expanding its leadership presence from 17 to 24 states. Its Cat 255 and 265 compact track loaders ranked among the top-selling models of the year. The company has also strengthened its innovation capabilities through a recent partnership with a technology firm to develop AI-driven predictive maintenance solutions.

SNAPSHOT

The U.S. construction equipment market size by volume is expected to grow at a CAGR of approximately 3.96% from 2025 to 2031.

The following factors are likely to contribute to the growth of the U.S. construction equipment market during the forecast period:

- Booming Construction Activity-Peak Disbursement of the Bipartisan Infrastructure Law (IIJA)

- Boom in Hyperscale Data Center Construction Projects

- Rising Housing Investment Driving Sustained Demand for Compact Construction Equipment

Base Year: 2025

Forecast Year: 2026-2031

The report considers the present scenario of the U.S. construction equipment market and its market dynamics for 2025−2030. It covers a detailed overview of several market growth enablers, restraints, and trends. The study covers both the demand and supply sides of the market. It also profiles and analyzes leading companies and several other prominent companies operating in the market.

Key Vendors

- Caterpillar

- Komatsu

- Deere & Company

- Volvo CE

- Liebherr

- Hitachi Construction Machinery

- SANY

- CNH Industrial

- XCMG

- HD Hyundai Construction Equipment

- Kobelco

- Zoomlion

- Kubota

- Bobcat

Other Prominent Vendors

- Takeuchi

- DEVELON

- JCB

- Toyota Material Handling

- The Manitowoc Company, Inc.

- JLG Industries

- Terex Corporation

- Manitou Group

- Wacker Neuson SE

- LiuGong

- Ammann Group Holding AG

- Tadano Ltd.

- Link-Belt Cranes

- Mecalac

- Gehl Company

- Yanmar

Distributor Profiles

- National Equipment Dealers (NED), LLC

- Kirby-Smith Machinery, Inc.

- Landmark Equipment

- Associated Supply Company, Inc. (ASCO Equipment)

- ROMCO, Inc.

- B-C Equipment Sales, Inc.

- Bane Machinery, Inc.

- McClung-Logan Equipment Company

- Mico Equipment Company

- Cowin Equipment Company, Inc.

- Scott Companies (operating as Scott Equipment Company, LLC)

- Doggett Equipment Services Group

Segmentation by Type

Earthmoving Equipment

- Excavator

- Backhoe Loaders

- Wheeled Loaders

- Other Earthmoving Equipment (Other loaders, Bulldozers, Trenchers, Motor Graders)

Road Construction Equipment

- Road Rollers

- Asphalt Pavers

Material Handling Equipment

- Crane

- Forklift & Telescopic Handlers

- Aerial Platforms (Articulated Boom Lifts, Telescopic Boom lifts, Scissor lifts)

Other Construction Equipment

- Dumper

- Concrete Mixer

- Concrete Pump Truck

Segmentation by End Users

- Construction

- Mining

- Manufacturing

- Others (Power Generation, Utilities, Municipal Corporations, Oil & Gas, Cargo Handling, Power Generation Plants, Waste Management)

U.S. CONSTRUCTION EQUIPMENT MARKET FAQs

How big is the U.S. construction equipment market?

What is the growth rate of the U.S. construction equipment market?

What are the trends in the U.S. construction equipment market?

Who are the key players in the U.S. construction equipment market?

Which are the major distributor companies in the U.S. construction equipment market?

LIST OF GRAPHS

Graph 1 Top Construction Equipment Manufacturer By State

Graph 2 Construction Equipment Market Volume (Units)

Graph 3 Construction Equipment Market 2025 (%)

Graph 4 Equipment Type (2025)

Graph 5 End-user (2025)

Graph 6 US Construction Equipment Market 2022–2031 (Units)

Graph 7 US Construction Equipment Market 2022–2031 ($ Million)

Graph 8 BIL By Infrastructure Funding

Graph 9 Transportation: Funding By Federal Agency

Graph 10 New Privately-owned Housing Units Started By Region

Graph 11 New Privately-owned Housing Units Under Construction At End Of 2026

Graph 12 Earthmoving Construction Equipment Market 2022–2031 (Units)

Graph 13 Earthmoving Construction Equipment Market 2022–2031 ($ Million)

Graph 14 Excavator Market 2022–2031 (Units)

Graph 15 Excavator Market 2022–2031 ($ Million)

Graph 16 Backhoe Loaders Market 2022–2031 (Units)

Graph 17 Backhoe Loaders Market 2022–2031 ($ Million)

Graph 18 Wheeled Loaders Market 2022–2031 (Units)

Graph 19 Wheeled Loaders Market 2022–2031 ($ Million)

Graph 20 Bulldozer Market 2022–2031 (Units)

Graph 21 Bulldozer Market 2022–2031 ($ Million)

Graph 22 Motor Grader Market 2022–2031 (Units)

Graph 23 Motor Grader Market 2022–2031 ($ Million)

Graph 24 Compact Earthmoving Equipment Market 2022–2031 (Units)

Graph 25 Compact Earthmoving Equipment Market 2022–2031 ($ Million)

Graph 26 Road Construction Equipment Market 2022–2031 (Unit)

Graph 27 Road Construction Equipment Market 2022–2031 ($ Million)

Graph 28 Road Rollers Market, 2022–2031 (Unit Sales)

Graph 29 Road Rollers Market, 2022–2031 ($ Million)

Graph 30 Asphalt Pavers Market 2022–2031 (Units)

Graph 31 Asphalt Pavers Market 2022–2031 ($ Million)

Graph 32 Material-handling Equipment Market 2022–2031 (Units)

Graph 33 Material-handling Equipment Market 2022–2031 ($ Million)

Graph 34 Cranes Market 2022–2031 (Units)

Graph 35 Cranes Market 2022–2031 ($ Million)

Graph 36 Forklifts And Telehandlers Market 2022–2031 (Units)

Graph 37 Forklifts And Telehandlers Market 2022–2031 ($ Million)

Graph 38 US Aerial Working Platforms Market 2022–2031 (Unit Sales)

Graph 39 US Aerial Working Platforms Market 2022–2031 ($ Million)

Graph 40 Other Construction Equipment Market 2022–2031 (Units)

Graph 41 Other Construction Equipment Market 2022–2031 ($ Million)

Graph 42 Articulated Dump Trucks Market 2022–2031 (Units)

Graph 43 Articulated Dump Trucks Market 2022–2031 ($ Million)

Graph 44 Concrete Mixers Market 2022–2031 (Units)

Graph 45 Concrete Mixers Market 2022–2031 ($ Million)

Graph 46 Concrete Pump Trucks 2022–2031 (Units)

Graph 47 Concrete Pump Trucks 2022–2031 ($ Million)

Graph 48 Construction Equipment Usage Market In Construction Industry 2022–2031 (Units)

Graph 49 Construction Equipment Usage Market In Construction Industry 2022–2031 ($ Million)

Graph 50 Construction Equipment Usage Market In Manufacturing Industry 2022–2031 (Units)

Graph 51 Construction Equipment Usage Market In Manufacturing Industry 2022–2031 ($ Million)

Graph 52 Construction Equipment Usage Market In Mining Industry 2022–2031 (Units)

Graph 53 Construction Equipment Usage Market In Mining Industry 2022–2031 ($ Million)

Graph 54 Construction Equipment Usage Market In Other End-user Industries 2022–2031 (Units)

Graph 55 Construction Equipment Usage Market In Other End-user Industries 2022–2031 ($ Million)

Graph 56 Market Shares Of Leading Vendors (2025)

Graph 57 Caterpillar: Sales By Region 2025 (%)

Graph 58 Caterpillar: Sales By Business Segment 2025 (%)

Graph 59 Komatsu: Sales By Region In 2025 (%)

Graph 60 Komatsu: Sales By Business Segment 2025 (%)

Graph 61 John Deere: Sales By Business Segment 2025 (%)

Graph 62 Volvo: Sales By Region 2025 (%)

Graph 63 Volvo: Sales By Segment 2025 (%)

Graph 64 Liebherr: Sales By Region 2025 (%)

Graph 65 Liebherr: Sales By Product Segment 2025 (%)

Graph 56 Hitachi: Sales By Region 2025 (%)

Graph 67 SANY: Net Sales 2025 ($ Billion)

Graph 68 CNH Industrial: Sales By Region 2025 (Construction) (%)

Graph 69 CNH Industrial: Sales By Business Segment 2025 (%)

Graph 70 CNH Industrial: Net Sales 2023-2025 ($ Billion)

Graph 71 XCMG: Net Sales 2024 ($ Billion)

Graph 72 Zoomlion: Net Sales 2024 ($ Billion)

Graph 73 Kubota: Net Sales 2021-2025 ($ Billion)

Graph 74 Bobcat: Net Sales 2022-2025 ($ Billion) (Doosan Bobcat)

LIST OF TABLES

Table 1 Top 15 Construction Equipment Manufacturers in the US in 2025 by New Financed Sales

Table 2 Prominent Construction Equipment Models in the US in 2025

Table 3 Ongoing Construction Projects in the US 2025

Table 4 Electric Construction Equipment Launched in the US Market in 2025

Table 5 Infrastructure Projects Under IIJA

Table 6 Major Data Center Projects Underway in 2026

Table 7 Tariffs in Effect as of April 2026

Table 8 Import Data

Table 9 Export Data

Table 10 Total Incremental Opportunities 2026–2031 (Equipment Type)

Table 11 New Excavators Launched in the US Market (2024–2025)

Table 12 New Financed Backhoe Loaders Sold (July 2024–June 2025)

Table 13 Top Selling Wheel Loaders (2024–2025)

Table 14 Top Selling New Motor Grader Models (2024–2025)

Table 15 Key Ongoing Road Construction Projects in the US in 2026

Table 16 Top Selling Road Roller Brands (December 2024–November 2025)

Table 17 Top Selling ADT Model (October 2024–September 2025)

Table 18 Total Incremental Opportunities 2026–2031

1. SECTION 1 – RESEARCH METHODOLOGY

2. SECTION 2 – RESEARCH OBJECTIVES

3. SECTION 3 – RESEARCH PROCESS

4. SECTION 4 – INTRODUCTION

4.1 Market Coverage

4.2 Report Scope

5. SECTION 5 – MARKET AT A GLANCE

5.1 Market Overview

5.2 Market Snapshot

6. SECTION 6 – EXECUTIVE SUMMARY

7. SECTION 7 – MARKET LANDSCAPE

7.1 PESTEL Analysis

7.2 Economic Scenario

7.3 Key Projects

7.4 Market Dynamics

7.5 Geographic Analysis

7.6 Import & Export Trend Analysis

7.7 Supply Chain Analysis

8. SECTION 8 – SEGMENTATION

8.1 Equipment Type

8.1.1 Equipment Definition (Earthmoving)

8.1.1.1 Earthmoving Equipment (Volume & Value)

8.1.1.2 Excavators

8.1.1.3 Backhoe Loaders

8.1.1.4 Wheel Loaders

8.1.1.5 Bulldozers

8.1.1.6 Motor Graders

8.1.1.7 Compact Earthmoving Equipment

(Skid-steer Loaders, Compact Track Loaders, Mini-excavators)

8.1.2 Equipment Definition (Road Construction)

8.1.2.1 Road Construction (Volume & Value)

8.1.2.2 Road Rollers

8.1.2.3 Asphalt Pavers

8.1.3 Equipment Definition (Material Handling & Lifting Equipment)

8.1.3.1 Material Handling & Lifting Equipment (Volume & Value)

8.1.3.2 Cranes

8.1.3.3 Forklifts & Telehandlers

8.1.3.4 Aerial Platforms

8.1.4 Equipment Definition (Other Construction Equipment)

8.1.4.1 Other Construction Equipment (Volume & Value)

8.1.4.2 Articulated Dump Trucks

8.1.4.3 Concrete Mixers

8.1.4.4 Concrete Pump Trucks

8.2 End–users

8.2.1 End–user Definition

8.2.2 Construction

8.2.3 Manufacturing

8.2.4 Mining

8.2.5 Others (Waste Management, Agriculture, Oil & Gas Extraction, Power Generation, Disaster Management, and Water Management)

9. SECTION 9 – TECHNOLOGICAL DEVELOPMENT

10. SECTION 10– COMPETITIVE LANDSCAPE

10.1 Competitive Landscape Overview

10.2 Prominent Vendors

10.3 Other Prominent Vendors

10.4 Distributor Profiles

11. SECTION 11 – REPORT SUMMARY

11.1 Key Insights

11.2 Abbreviations

11.3 Exhibits

11.4 Related Reports

11.5 Database

11.6 Global Reach

11.7 Offerings

Select a license type that suits your business needs

Single User Licence

- Report accessible by one user only

- Free 10% or 3 days of customization

- Free post-sale service assistance

- Continuous support through email

5 User Licence

- Report accessible by 5 users within the organization

- Free 15% or 4.5 days of customization

- Continuous support through email and telephone

- Free analyst hour

- Free Upgrade: If an updated report published within 180 days of purchase, you will get the revised report free of charge

Corporate Licence

- Free Datasheet worth $1500

- Report accessible by the entire organization

- Free 20% or 6 days of customization

- Free post-sale service assistance

- Continuous support through email and telephone

- Direct access to lead analysts

- Free analyst hour

- Free Upgrade: If an updated report published within 180 days of purchase, you will get the revised report free of charge

Datasheet Licence

- Report accessible by 1 user only

- Free 15% or 32 hours of customization

- Free post-sale service assistance

- Direct access to lead analysts

Frequently Asked Questions

How big is the U.S. construction equipment market?

What is the growth rate of the U.S. construction equipment market?

What are the trends in the U.S. construction equipment market?

Who are the key players in the U.S. construction equipment market?

Which are the major distributor companies in the U.S. construction equipment market?

Other RELATED Reports

Southeast Asia Construction Equipment Market Research Report 2025-2030

Published : January 2026