Global Anime Streaming Market Research Report 2025–2030

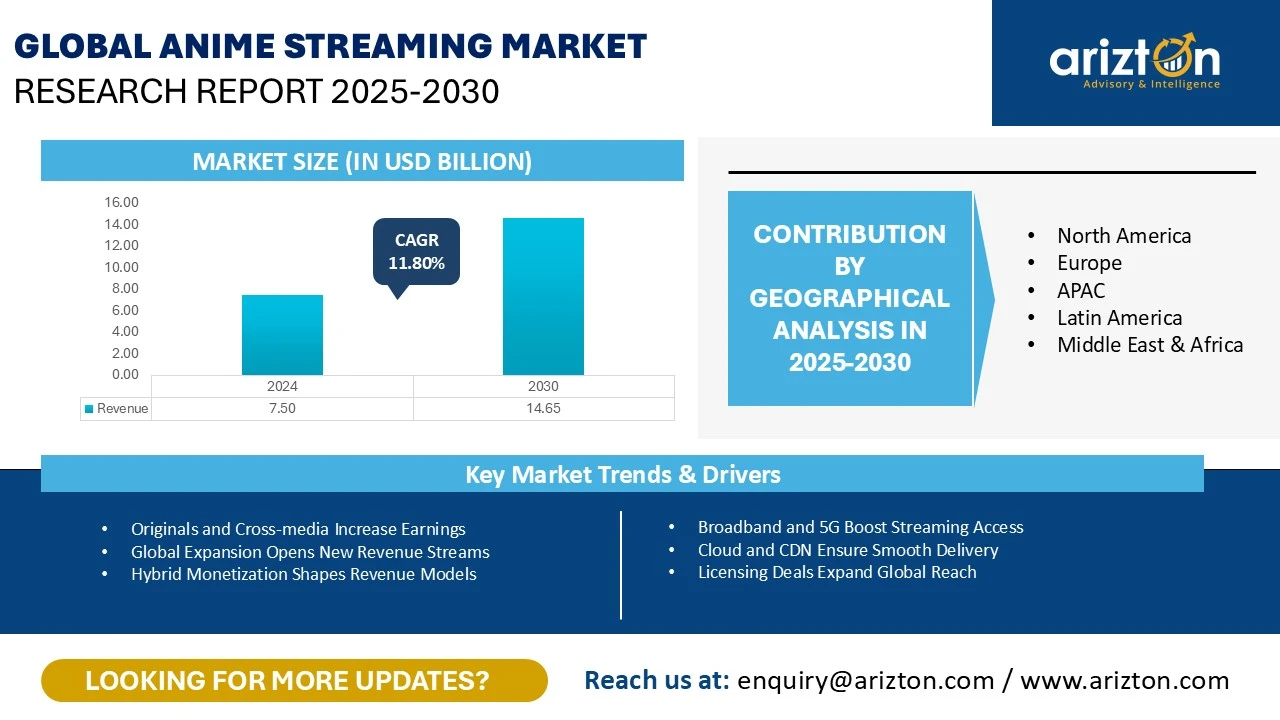

THE GLOBAL ANIME STREAMING MARKET WAS VALUED AT USD 7.50 BILLION IN 2024 AND IS PROJECTED TO REACH USD 14.65 BILLION BY 2030, REFLECTING A CAGR OF 11.80%.

The Anime Streaming Market Size, Share, & Trends By Subscription Model, By Content Format, By Genre, By Platform Type, By Device, By Demographics, & By Geography. Industry Analysis Report, Growth Potential, Price Trends, Competitive Market Share.

Published Date : January 2026

Last Updated : January 2026

format: PDF

193 pages

21 company

07 segments

5 region

24 countries

Purchase Options

Global Anime Streaming Market Research Report 2025–2030

THE GLOBAL ANIME STREAMING MARKET WAS VALUED AT USD 7.50 BILLION IN 2024 AND IS PROJECTED TO REACH USD 14.65 BILLION BY 2030, REFLECTING A CAGR OF 11.80%.

The Anime Streaming Market Size, Share, & Trends Analysis Report By

- Subscription Model: SVOD (Subscription Video-on-Demand), AVOD (Ad-Supported Video-on-Demand), Hybrid Models (Freemium), and TVOD (Transactional Video-on-Demand)

- Content Format: Anime TV Series, Anime Films, and Others

- Genre: Action & Adventure, Fantasy & Sci-Fi, Romance & Drama, Comedy & Slice of Life, Horror & Thriller, Sports & Games, and Historical & Cultural

- Platform Type: Dedicated Anime Platforms, General OTT Platforms, and Free & User-Generated Platforms

- Device: Smartphones & Tablets, Smart TVs & Streaming Devices, PC & Laptops, and Gaming Consoles

- Demographics: Millennials, Gen Z Adults, Gen Xers, and Baby Boomers

- Geography: North America, Europe, APAC, Latin America, and Middle East & Africa

Industry Analysis Report, Regional Outlook, Growth Potential, Price Trends, Competitive Market Share & Forecast 2025–2030.

This report includes market data points, ranging from trend

analyses to market estimates & forecasts that you can customize

ANIME STREAMING MARKET REPORT SCOPE

| REPORT ATTRIBUTE | DETAILS |

|---|---|

| Market Size (2030) | USD 14.65 Billion |

| Market Size (2024) | USD 7.50 Billion |

| CAGR (2024-2030) | 11.80% |

| HISTORIC YEAR | 2021-2023 |

| BASE YEAR | 2024 |

| FORECAST YEAR | 2025-2030 |

| SEGMENTS BY | Subscription Model, Content Format, Genre, Platform Type, Device, Demographics, and Geography |

| GEOGRAPHIC ANALYSIS | North America, Europe, APAC, Latin America, and Middle East & Africa |

| KEY PLAYERS | Netflix, Crunchyroll, Hulu, AMC Networks, and Amazon |

ANIME STREAMING MARKET ANALYSIS

The global anime streaming market size was valued at USD 7.50 billion in 2024 and is projected to reach USD 14.65 billion by 2030, growing at a CAGR of 11.80% during the forecast period. This growth is supported by expanding global fanbases, licensing partnerships between Japanese studios and international platforms, faster broadband and 5G adoption, and cross-media synergies with merchandise, gaming, and theatrical releases.

Anime streaming has moved beyond niche audiences, becoming a mainstream medium for global entertainment. It plays a central role in pop culture, youth engagement, and lifestyle expression, creating digital ecosystems that extend far beyond traditional viewing.

Technology infrastructure forms the backbone of the anime streaming market’s expansion. Cloud services and content delivery networks (CDNs) enable simultaneous releases to millions of viewers worldwide without interruption, while 5G reduces buffering in emerging markets. AI-based recommendation engines enhance personalization, ensuring stronger viewer retention across diverse streaming platforms.

IMPACT OF US & CHINA TRADE WAR

The escalation of the US–China trade war in January 2025 intensified scrutiny on digital media imports and cross-border content distribution agreements. Higher regulatory barriers and tightened digital tariffs indirectly affected anime licensing flows, particularly for Chinese-owned animation studios, distribution aggregators, and cloud-hosting infrastructure supporting anime streaming platforms.

US-based anime streaming services faced increased acquisition costs due to stricter compliance checks on Chinese-origin content libraries, cloud CDN partnerships, and metadata management tools. Licensing fees, subtitling/dubbing workflows, and content-delivery expenses rose sharply, compressing margins for subscription-based and ad-supported anime platforms operating in North America and Europe.

To mitigate exposure to tariff-driven uncertainty, global platforms accelerated diversification of content sourcing away from China. Licensing focus shifted more heavily toward Japan, South Korea, and emerging creators in Southeast Asia. These transitions caused temporary supply gaps, slower contract renewals, and delays in global distribution rights, especially for seasonal simulcasts and localized dubbed releases.

The current US–India trade dispute, marked by heightened scrutiny on digital services and technology flows, has increased compliance and operational costs for US-based platforms operating in India. This has raised the burden of cloud hosting, app-store operations, payment gateway integrations, and telecom-linked OTT bundles, resulting in slower content rollout cycles, tighter monetization conditions for ad-supported anime services, and delayed updates for India-specific delivery, without affecting the global licensing or availability of anime produced in Japan or other key markets.

ANIME STREAMING MARKET TRENDS & GROWTH DRIVERS

- Expanding global demand for Japanese and anime-inspired content is opening new revenue streams across North America, Europe, Latin America, and fast-growing Asian markets. As platforms broaden their local market presence through localized catalogs, dubbed releases, and culturally adapted marketing, global expansion is accelerating subscription uptake and unlocking new monetization avenues.

- Original productions, exclusive partnerships, and cross-media franchises are emerging as high-value growth drivers. Platform-funded originals, anime–game integrations, light-novel adaptations, and multimedia IP ecosystems enhance differentiation and extend earnings through recurring seasons, character merchandising, theatrical spin-offs, and event-driven engagement.

- Hybrid monetization models are reshaping revenue structures across the anime ecosystem. Flexible subscription choices, ad-supported plans, microtransactions, fan-club memberships, and transactional streaming allow platforms to diversify income while matching varied price sensitivities and consumption preferences across global audiences.

- Simulcasts and weekly episode drops are strengthening real-time engagement and retention. Day-and-date releases with Japan, seasonal lineups, and community-driven viewing cycles amplify platform stickiness, sustain subscriber activity between major premieres, and reinforce fan participation across social media, forums, and creator communities.

- Broadband expansion, 5G deployment, and advanced cloud-CDN infrastructure are enhancing the quality and reliability of anime streaming. Improved connectivity supports high-resolution playback, rapid content delivery, and seamless global distribution of licensed titles, while strong licensing pipelines and merchandise-theatrical synergies encourage deeper investment in premium anime catalogs.

INDUSTRY RESTRAINTS

- The anime streaming market faces significant cost pressures due to high licensing fees for popular titles, simulcasts, and exclusivity agreements. As competition intensifies, platforms allocate larger budgets to secure premium content, tightening margins and making it challenging for mid-sized services to expand their libraries or offer competitive subscription pricing.

- Persistent piracy and unauthorized distribution continue to undermine revenue potential for legal platforms. Despite stronger enforcement and anti-piracy measures, many viewers still access free, illegal alternatives, reducing conversion rates for paid subscriptions and discouraging long-term investment in localized dubbing, broader title availability, and platform-specific content enhancements.

ANIME STREAMING MARKET SEGMENTATION INSIGHTS

INSIGHT BY SUBSCRIPTION MODEL

The global anime streaming market by subscription model is segmented into SVOD (Subscription Video-on-Demand), AVOD (Ad-Supported Video-on-Demand), Hybrid Models (Freemium), and TVOD (Transactional Video-on-Demand). The SVOD model dominates and holds the largest market share of around 51%. Subscription Video on Demand (SVOD) platforms provide unlimited ad-free anime access for a fixed monthly fee, making them the dominant monetization model for anime streaming. Examples include Crunchyroll, Netflix, Disney+, Prime Video, Hulu and HiDive, all offering licensed libraries and simulcast releases.

SVOD consumption has surged, with Netflix’s anime viewing hours tripling over the past five years (2019–2024). Content exclusivity, simulcasts and tiered plans continue to attract new users and differentiate platforms.

SVOD subscribers are highly engaged and subscribe to nearly twice as many streaming services as non-anime viewers. Their demand for early simulcasts and exclusive titles pushes platforms to release episodes quickly and keep adding fresh content to maintain loyalty.

Hybrid or freemium models are projected to show significant growth during 2025–2030. Services such as YouTube, Crunchyroll’s free tier, and regional platforms like Bilibili attract price-sensitive audiences with free episodes supported by ads while offering premium upgrades for early access, dubs, and higher video quality. This dual monetization model gains traction in India, Indonesia, Brazil, and other mobile-first markets, where users gradually transition from ad-supported viewing to paid tiers as their platform engagement increases.

INSIGHT BY CONTENT FORMAT

Based on the content format, the anime TV series are projected to show the fastest-growing CAGR of 12.23% during 2025–2030. Their momentum is driven by continuous seasonal releases, strong simulcast demand on platforms like Crunchyroll and Hulu, and the popularity of multi-arc franchises such as Demon Slayer and My Hero Academia. The episodic structure encourages sustained weekly engagement, while shorter 8–13-episode seasons enable platforms to refresh homepages more frequently and improve discovery through regular new-title rotations.

Fans also engage deeply with serialized content, bingeing multiple episodes in single sessions while also returning weekly for simulcasts. High completion rates and community engagement show that long-form series drive stronger recurring logins compared to one-off films or shorts, thus helping segment growth.

INSIGHT BY GENRE

Based on the genre, fantasy and sci-fi held a significant share of the global anime streaming market. The growth is supported by a strong appeal for isekai, supernatural, and futuristic storylines such as Re:Zero and Sword Art Online. These genres deliver high visual impact, long-term fan retention, and strong merchandising and gaming crossover potential. Their global resonance keeps them heavily featured on top rows and curated genre hubs across major platforms.

Comedy and slice-of-life titles are projected to show significant growth, with the fastest-growing CAGR during 2025–2030. Shows like Spy x Family, Komi Can’t Communicate, and Horimiya attract younger audiences seeking light, relatable storytelling suited for short viewing windows on mobile devices. High shareability of comedic moments, reaction clips, and everyday scenes drives discovery on TikTok, YouTube Shorts, and Instagram Reels, supporting repeat viewing and multi-season popularity.

INSIGHT BY PLATFORM TYPE

By platform type, the dedicated platforms segment accounted for the largest global anime streaming market share. Dedicated anime platforms are services designed exclusively for streaming Japanese animation, covering television series, films, OVAs and web-only releases. This category includes global names like Crunchyroll and HiDive, alongside regionally strong services such as NicoNico, Bilibili anime and Muse Asia.

These platforms use a mix of subscription and free access models, where premium simulcasts and dubs are paywalled but portions of back catalogs remain ad-supported or free. This ensures broader entry points while retaining exclusive appeal for committed fans.

Audiences on dedicated platforms show long-term loyalty, often subscribing for years and maintaining high watch times per session. Free users also engage heavily and frequently upgrade to paid tiers, encouraged by limited-time access or seasonal anime releases.

INSIGHT BY DEVICE

The smartphones and tablets segment dominates and holds the largest global anime streaming market share in 2024. Their growth is reinforced by mobile-first viewing habits across APAC and Latin America, where platforms like Crunchyroll, Netflix, and regional apps offer offline downloads, adaptive bitrate streaming, and personalized notifications. Shorter episodic formats and clip-based discovery on social media make smartphones the most convenient screen for everyday anime viewing.

Smart TVs and streaming devices also held a significant anime streaming market share in 2024. Users prefer watching visually rich titles like Attack on Titan, Bleach, or anime films in HD or 4K formats on large screens. Devices such as Roku, Fire TV, and Android TV enhance the cinematic experience, while built-in OTT integrations support family or group viewing of simulcast premieres, season finales, and anime movie releases.

INSIGHT BY DEMOGRAPHICS

The global anime streaming market by demographics is segregated into millennials, Gen Z adults, Gen Xers, and baby boomers. Millennials form a steady and reliable audience across global platforms. Many in this subsegment built familiarity with anime through early television broadcasts and the rise of online streaming in the late 2000s. They follow long-running franchises, prefer high-quality dubbing and often watch across multiple devices. Their willingness to pay for premium features and complete catalog access contributes significantly to the strength of subscription-based models.

The Gen Z segment shows significant growth, with the highest CAGR during the forecast period. Gen Z Adults remain deeply connected to anime culture, influenced by constant discovery through social platforms, creator communities and fast-moving online trends. Their viewing style revolves around quick exploration of new titles, frequent episode consumption and strong interest in fresh weekly releases. This group naturally gravitates toward simulcasts, seasonal drops and platform-exclusive titles.

ANIME STREAMING MARKET GEOGRAPHICAL ANALYSIS

North America held the largest revenue share of over 38% in the global anime streaming market, supported by the concentration of headquarters and licensing operations of major anime streaming platforms, including Netflix, Crunchyroll (Sony), Amazon Prime Video, and Disney+. Centralized content acquisition, early monetization windows, and strong subscription uptake across the region reinforce North America’s leadership and make it the core commercial hub for global anime distribution.

Canada is becoming a strong high-growth market in North America, projected to grow at a CAGR of 12.18% during 2025–2030. Simultaneous availability of major titles such as Attack on Titan: The Final Chapters, Chainsaw Man, and Frieren: Beyond Journey’s End has accelerated conversion from casual viewing to paid subscriptions. Nationwide theatrical participation, including The First Slam Dunk, Suzume, and Studio Ghibli anniversary screenings, continues to deepen engagement among young adults and uplift both subscription and ad-supported tiers.

Asia-Pacific is the fastest-growing anime streaming region, supported by the world’s largest viewer base, strong mobile-first consumption, and the region’s foundational role in anime creation. Despite its scale, regional revenue lags North America due to lower subscription pricing, widespread free-viewing alternatives, and varied platform monetization maturity across major markets.

ANIME STREAMING MARKET IN JAPAN

Japan led APAC with the largest revenue share in 2024, driven by its role as the production origin and earliest distribution hub for leading titles. Its dominance is supported by the immediate digital availability of hits such as Spy x Family, Attack on Titan, Chainsaw Man, and Jujutsu Kaisen on services like dAnime Store and established studio–platform partnerships. Theatrical successes, including Suzume, The First Slam Dunk, and Blue Giant, continue to convert cinema demand into streaming growth, while China and South Korea follow due to rising demand for Japanese anime and regional hits such as Solo Leveling and Link Click.

ANIME STREAMING MARKET SHARE & VENDOR LANDSCAPE

The global anime streaming market includes major platforms like Crunchyroll, Netflix, Amazon Prime Video, and HIDIVE, alongside regional services such as D-anime Store, Ani-One Asia, and Muse Asia, creating a competitive, diverse digital landscape.

Key players differentiate through exclusive licensing, simulcasts, original productions, and dubbed/subtitled catalogs, focusing on user engagement, cross-device accessibility, and personalized recommendations to maintain subscriber loyalty and expand audience reach. Regional platforms strengthen positions by localizing content, offering mobile-first experiences, and enabling community engagement through watch parties or curated collections tailored to local languages and cultural preferences.

Groups operating multiple brands, such as the Crunchyroll-Funimation merger, expand libraries through joint licensing and co-productions, offering simulcasts and dubbed series to reach audiences across North America, Europe, and Asia-Pacific. Content licensing, copyright enforcement, and regional availability drive innovation, pushing platforms toward high-definition streaming, smart-device integration, and algorithmic personalization to enhance the viewer experience.

The market is shaped by the scale, exclusive content, and production investment of global platforms, balanced by localization, cultural adaptation, and flexible services offered by regional players targeting specific audiences.

Recent Developments in the Anime Streaming Market

- In September 2025, Hulu expanded its anime catalog with new releases such as DAN DA DAN, Dr Stone, and One Piece, continuing to diversify its anime content for subscribers. This broadens Hulu’s appeal internationally, contributing to the global growth of licensed anime streaming.

- In April 2025, Cineverse's RetroCrush acquired exclusive streaming rights to the classic sci-fi anime series Future Boy Conan from GKIDS, expanding its classic anime offerings. This strengthens RetroCrush’s position in niche anime content, increasing global competition for classic and legacy titles.

- In March 24, 2025, HIDIVE expanded its distribution by launching on Amazon Prime Video Channels as a monthly ad-free add-on in the UK, Canada, Australia, and New Zealand, while also increasing availability on CTV partners in the U.S., including Samsung, LG, and VIZIO devices.

- On March 15, 2025, Netflix unveiled its upcoming anime slate at AnimeJapan 2025, highlighting new co-productions and exclusive global releases, reinforcing its commitment to expanding anime content for international audiences.

- In March 2025, Amazon secured rights to stream Gundam GQuuuuuuX (dubbed and subbed versions) in 2025 in over 240 countries, as part of expanding its Japanese anime offerings.

- On January 7, 2025, Crunchyroll, Aniplex, Sony Music, and PlayStation Productions announced the production of an anime adaptation of Ghost of Tsushima: Legends, bringing the popular video game mode to a global audience through Crunchyroll.

SNAPSHOT

The global anime streaming market size is expected to grow at a CAGR of approximately 3.96% from 2024 to 2030.

The following factors are likely to contribute to the growth of the global anime streaming market during the forecast period:

- Broadband and 5G Boost Streaming Access

- Cloud and CDN Ensure Smooth Delivery

- Licensing Deals Expand Global Reach

- Merchandise and Movies Support Investment

Base Year: 2024

Forecast Year: 2025-2030

The report considers the present scenario of the global anime streaming market and its market dynamics for 2025−2030. It covers a detailed overview of several market growth enablers, restraints, and trends. The study covers both the demand and supply sides of the market. It also profiles and analyzes leading companies and several other prominent companies operating in the market.

Key Company Profile

- Netflix

- Business Overview

- Product Offerings

- Key Developments

- Key Strategies

- Key Strengths

- Key Opportunities

- Crunchyroll

- Hulu

- AMC Networks

- Amazon

Other Prominent Company Profiles

- Tubi

- Business Overview

- Product Offerings

- Cineverse

- JioHotstar

- Disney+

- U-NEXT

- Ani.ME

- BiliBili

- ABEMA

- HBO Max

- Pluto TV

- Muse Communication

- Anime-Planet

- Anime Digital Network (ADN)

- OceanVeil

- D-anime Store

- YouTube

Segmentation by Subscription Model

- SVOD (Subscription Video-on-Demand

- AVOD (Ad-Supported Video-on-Demand)

- Hybrid Models (Freemium)

- TVOD (Transactional Video-on-Demand)

Segmentation by Content Format

- Anime TV Series

- Anime Films

- Others

Segmentation by Genre

- Action & Adventure

- Fantasy & Sci-Fi

- Romance & Drama

- Comedy & Slice of Life

- Horror & Thriller

- Sports & Games

- Historical & Cultural

Segmentation by Platform Type

- Dedicated Anime Platforms

- General OTT Platforms

- Free & User-Generated Platforms

Segmentation by Device

- Smartphones & Tablets

- Smart TVs & Streaming Devices

- PC & Laptops

- Gaming Consoles

Segmentation by Demographics

- Millennials

- GenZ Adults

- Gen Xers

- Baby Boomers

Segmentation by Geography

- North America

- US

- Canada

- APAC

- Japan

- China

- South Korea

- India

- Indonesia

- Thailand

- Philippines

- Vietnam

- Australia

- Europe

- Germany

- France

- UK

- Italy

- Spain

- Russia

- Poland

- Middle East & Africa

- Saudi Arabia

- South Africa

- UAE

- Latin America

- Brazil

- Mexico

- Argentina

ANIME STREAMING MARKET FAQs

How big is the global anime streaming market?

What is the growth rate of the global anime streaming market?

What are the key trends in the global anime streaming market?

Which region dominates the global anime streaming market?

Who are the major players in the global anime streaming market?

For more details, please reach us at [email protected]

- Chapter 1- Scope & Coverage

- Market Definition

- Inclusion

- Exclusions

- Market Estimation Caveats

- Market Derivation

- Market Segmentation by Subscription Model

- Market Segmentation by Content Format

- Market Segmentation by Genre

- Market Segmentation by Platform Type

- Market Segmentation by Device

- Market Segmentation by Demographics

- Chapter 2- Premium Insights

- Chapter 3- Market Dynamics

- Introduction

- Value Chain Analysis

- Gender-Driven Opportunities And Streaming Patterns

- Key Factors Driving Anime Streaming Adoption

- Impact Of Global Manga Readership

- New Viewer Habits Powering Market Expansion

- Impact of The Ongoing Tariff War

- Market Opportunities & Trends

- Global Expansion Opens New Revenue Streams

- Originals and Cross-Media Increase Earnings

- Hybrid Monetization Shapes Revenue Models

- Simulcast and Weekly Releases Drive Engagement

- Market Growth Enablers

- Broadband and 5G Boost Streaming Access

- Cloud and CDN Ensure Smooth Delivery

- Licensing Deals Expand Global Reach

- Merchandise and Movies Support Investment

- Market Restraints

- High Licensing Costs and Piracy Risks

- Market Fragmentation and Tech Barriers

- Market Landscape

- Five Forces Analysis

- Chapter 4- Market Segmentation

- Subscription Model (Market Size & Forecast: 2021-2030)

- SVOD (Subscription Video-on-Demand

- AVOD (Ad-Supported Video-on-Demand)

- Hybrid Models (Freemium)

- TVOD (Transactional Video-on-Demand)

- Content Format (Market Size & Forecast: 2021-2030)

- Anime Tv Series

- Anime Films

- Others

- Genre (Market Size & Forecast: 2021-2030)

- Action & Adventure

- Fantasy & Sci-Fi

- Romance & Drama

- Comedy & Slice of Life

- Horror & Thriller

- Sports & Games

- Historical & Cultural

- Platform Type (Market Size & Forecast: 2021-2030)

- Dedicated Anime Platforms

- General OTT Platforms

- Free & User-Generated Platforms

- Device (Market Size & Forecast: 2021-2030)

- Smartphones & Tablets

- Smart TVs & Streaming Devices

- PC & Laptops

- Gaming Consoles

- Demographics (Market Size & Forecast: 2021-2030)

- Millennials

- GenZ Adults

- Gen Xers

- Baby Boomers

- Chapter 5- Geography Segmentation

- Geography Segmentation (Market Size & Forecast: 2021-2030)

- Geographic Overview – Market Maturity Index

- North America

- US

- Canada

- APAC

- Japan

- China

- South Korea

- India

- Indonesia

- Thailand

- Philippines

- Vietnam

- Australia

- Europe

- Germany

- France

- UK

- Italy

- Spain

- Russia

- Poland

- MIDDLE EAST & AFRICA

- Saudi Arabia

- South Africa

- UAE

- Latin America

- Brazil

- Mexico

- Argentina

- Chapter 6- Competitive Landscape

- Competitive Landscape

- Competition Overview

- Key Developments

- Key Company Profiles

- Other Prominent Company Profiles

- Report Summary

- Key Takeaways

- Strategic Recommendations

Select a license type that suits your business needs

Single User Licence

- Report accessible by one user only

- Free 10% or 3 days of customization

- Free post-sale service assistance

- Continuous support through email

5 User Licence

- Report accessible by 5 users within the organization

- Free 15% or 4.5 days of customization

- Continuous support through email and telephone

- Free analyst hour

- Free Upgrade: If an updated report published within 180 days of purchase, you will get the revised report free of charge

Corporate Licence

- Free Datasheet worth $1500

- Report accessible by the entire organization

- Free 20% or 6 days of customization

- Free post-sale service assistance

- Continuous support through email and telephone

- Direct access to lead analysts

- Free analyst hour

- Free Upgrade: If an updated report published within 180 days of purchase, you will get the revised report free of charge

Datasheet Licence

- Report accessible by 1 user only

- Free 15% or 32 hours of customization

- Free post-sale service assistance

- Direct access to lead analysts

Frequently Asked Questions

How big is the global anime streaming market?

What is the growth rate of the global anime streaming market?

What are the key trends in the global anime streaming market?

Which region dominates the global anime streaming market?

Who are the major players in the global anime streaming market?