APAC Data Center Colocation Market – Industry Outlook & Forecast 2026-2031

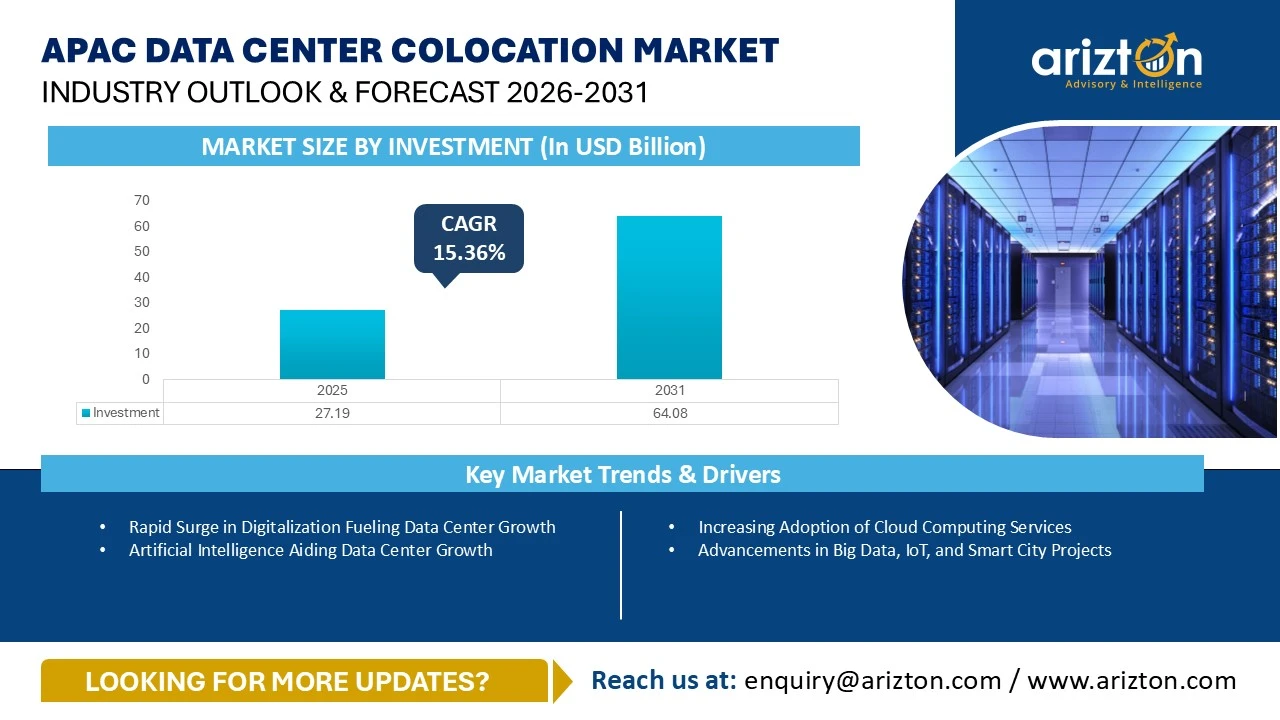

APAC DATA CENTER COLOCATION MARKET SIZE BY INVESTMENT WAS VALUED AT USD 27.19 BILLION IN 2025 AND IS EXPECTED TO REACH USD 64.08 BILLION BY 2031, GROWING AT A CAGR OF 15.36% DURING THE FORECAST PERIOD.

APAC Data Center Colocation Market – Industry Outlook & Forecast 2026-2031

APAC DATA CENTER COLOCATION MARKET SIZE BY INVESTMENT WAS VALUED AT USD 27.19 BILLION IN 2025 AND IS EXPECTED TO REACH USD 64.08 BILLION BY 2031, GROWING AT A CAGR OF 15.36% DURING THE FORECAST PERIOD.

The APAC Data Center Colocation Market Report Includes

- Colocation Type: Retail Colocation and Wholesale Colocation

- Infrastructure: Electrical Infrastructure, Mechanical Infrastructure, and General Construction

- Electrical Infrastructure: UPS Systems, Generators, Transfer Switches & Switchgear, PDUs, and Other Electrical Infrastructure

- Mechanical Infrastructure: Cooling Systems, Racks, and Other Mechanical Infrastructure

- Cooling Systems: CRAC & CRAH Units, Chiller Units, Cooling Towers, Condensers & Dry Coolers, Economizers & Evaporative Coolers, and Other Cooling Units

- Cooling Techniques: Air-based Cooling and Liquid-based Cooling

- General Construction: Core & Shell Development, Installation & Commissioning Services, Engineering & Building Design, Fire Detection & Suppression, Physical Security, and DCIM/BMS Solutions

- Tier Standard: Tier I & II, Tier III, and Tier IV

- Geography: APAC (China, Hong Kong, Australia, New Zealand, Japan, India, South Korea, Taiwan, & Rest of APAC) and Southeast Asia (Singapore, Indonesia, Malaysia, Thailand, Philippines, Vietnam, & Rest of Southeast Asia)

Get Insights on 870 Existing Data Center Facilities and 905 Upcoming Facilities across Asia Pacific

This report includes market data points, ranging from trend

analyses to market estimates & forecasts that you can customize

APAC DATA CENTER COLOCATION MARKET REPORT SCOPE

| REPORT ATTRIBUTE | DETAILS |

|---|---|

| MARKET SIZE BY INVESTMENT (2031) | USD 64.08 Billion |

| MARKET SIZE BY INVESTMENT (2025) | USD 27.19 Billion |

| CAGR - INVESTMENT (2025-2031) | 15.36% |

| MARKET SIZE - COLOCATION REVENUE (2031) | USD 69.78 Billion |

| MARKET SIZE AREA (2031) | 23.80 million sq. feet |

| POWER CAPACITY (2031) | 6,177 MW (2031) |

| BASE YEAR | 2025 |

| FORECAST YEAR | 206-2031 |

| MARKET SEGMENTS | Colocation Service, Infrastructure, Electrical Infrastructure, Mechanical Infrastructure, Cooling Systems, Cooling Techniques, General Construction, Tier Standards, and Geography |

| GEOGRAPHICAL ANALYSIS | APAC (China, Hong Kong, Australia, New Zealand, Japan, India, South Korea, Taiwan, & Rest of APAC) and Southeast Asia (Singapore, Indonesia, Malaysia, Thailand, Philippines, Vietnam, & Rest of Southeast Asia) |

ASIA-PACIFIC DATA CENTER COLOCATION MARKET - SIZE & SHARE ANALYSIS

The APAC data center colocation market was valued at USD 27.19 billion in 2025 and is projected to reach USD 64.08 billion by 2031, growing at a CAGR of 15.36% from 2025 to 2031.

The market is expanding significantly due to several factors, such as the adoption of Artificial Intelligence (AI) and the demand for edge computing. China accounted for a share of around 37% of the APAC data center colocation market investments in 2025, with Southeast Asia contributing approximately 21% to the region’s data center colocation market investments during the same period. Hyperscalers, AI workloads, and a wave of digital-first economies are driving an unprecedented surge in demand for secure, scalable infrastructure across the region.

The data center colocation market in the APAC region is registering fast growth worldwide, fueled by rising cloud adoption, the expansion of edge computing, and the increasing use of technologies such as AI, big data, and IoT.

From China's province-level mega-campuses to Southeast Asia's fast-emerging hubs in Malaysia, Indonesia, and Vietnam, operators and investors are racing to claim a position in one of the world's highest-growth infrastructure sectors. This report gives you the data, competitive intelligence, and forward-looking forecasts to navigate it — covering 870 existing facilities, 905 upcoming projects, 174 companies, and 9 market segments across 17 countries.

Whether you're a colocation provider benchmarking your strategy, a hyperscaler scouting expansion markets, or an investor evaluating the next wave of digital infrastructure plays — this is the definitive market map for APAC data center colocation through 2031.

APAC DATA CENTER COLOCATION MARKET OPPORTUNITIES & TRENDS

Rapid Surge in Digitalization Fueling Data Center Growth

- In 2025, we observe that the APAC nations are experiencing rapid digital transformation, which is reshaping the region’s economy and driving the demand for data center development across the region. The rapid expansion of cloud computing, e-commerce, fintech, artificial intelligence, and other digital services is rapidly increasing data generation and storage needs, creating a strong demand for secure, high-performance, low-latency infrastructure.

- As organizations continue to adopt digital services, the demand for real-time data processing is accelerating, and data centers are becoming more crucial to support APAC’s digital economy. Therefore, with the surge in digitalization across the APAC countries, the demand for data centers will continuously increase during the forecast period.

- In January 2025, the South Korean Ministry of Science and ICT planned to establish a joint project worth approximately $30 million with the Association of Southeast Asian Nations (ASEAN) to promote digital transformation across South Korea and ASEAN by 2029.

Artificial Intelligence Aiding Data Center Growth

- The governments across APAC nations are increasingly focusing on AI development as well as encouraging public and private organizations to adopt AI applications to enhance their operational efficiency and boost productivity.

- In November 2025, the government of Taiwan announced the allocation of around $3.2 million to build a strong AI infrastructure in Taiwan in the process of becoming a global AI leader by 2040. Additionally, this initiative focuses on three main technologies: photonics, quantum computing, and AI robotics.

- APAC is boosting the development of AI with various initiatives, such as focusing on the development of AI-ready data centers, increasing government support, and promoting the adoption of AI across various industries, including healthcare, finance, and technology, to enhance digital transformation and sustainability.

Rise in Adoption of Liquid Cooling Techniques in Data Centers

- In the APAC region, most data centers use traditional air-cooling technologies; however, some facilities have adopted liquid cooling technologies. Liquid cooling is more effective than traditional cooling technologies owing to its higher efficiency and lower energy costs compared with traditional air-cooling technologies.

- In November 2025, Princeton Digital Group started the construction of JC3, a new data center campus, in Jakarta. The data center buildings on the campus will support both liquid and air-cooling solutions.

- We observe that the adoption of liquid cooling in APAC is in the initial phase, and we believe that the demand for liquid cooling will increase across the APAC countries during the upcoming years.

Government Initiatives Driving Data Center Investments

- The governments across APAC countries are promoting data center growth through different initiatives, such as investing in AI infrastructure, offering tax incentives for data center operators, and providing financial support for data center companies.

- In March 2025, the government established the Data Center Task Force (DCTF) to strengthen and regulate the nation’s data center industry. This initiative, co-chaired by the Minister of Investment, Trade and Industry as well as the Minister of Digital, highlights Malaysia’s commitment to building a sustainable digital future. The DCTF is tasked with formulating key policy decisions, enhancing coordination among industry stakeholders, and developing strategic measures to support the continued growth of the country’s data center sector.

APAC DATA CENTER COLOCATION MARKET SEGMENTATION INSIGHTS

- Data center operators in the APAC region are making significant efforts to adopt various sustainability practices in their data center operations. Companies are integrating renewable energy to power their data center operations, replacing lead-acid UPS systems with lithium-ion batteries and diesel generators with HVO-powered generators, as well as installing advanced liquid cooling technologies in data centers to reduce electricity consumption, thereby lowering the environmental impact of data centers and greenhouse gas emissions.

- The adoption of the liquid cooling technique is emerging as a key trend in the APAC data center market, driven by the rapidly rising rack power densities. According to insights from NEXTDC, Vertiv, and NVIDIA, the average data center rack densities are expected to grow from approximately 15–25 kW to over 50 kW by 2029. As AI workloads intensify, peak rack densities are projected to reach 250–500 kW, making traditional air cooling insufficient and accelerating the shift toward liquid cooling techniques.

- Digital Realty installed liquid-cooled servers in its SIN11 data center in Singapore. This reduces power consumption by up to 29%.

APAC DATA CENTER COLOCATION MARKET - REGIONAL ANALYSIS

- In the APAC data center colocation market, China is expected to have the largest APAC data center colocation market share in 2031 in terms of investment, followed by Japan, Australia, Malaysia, and India, among others.

- In China, provinces such as Fujian, Guangdong, Guizhou, Hainan, Hebei, Hunan, Ningxia, Shandong, and Shanghai are some of the primary hubs in China for the development of data centers. In recent years, Jiangsu, Anhui, Guangxi, Inner Mongolia, Sichuan, Shaanxi, and Zhejiang have gained momentum for data center development in China.

- In Hong Kong, Tseung Kwan O remains one of the key locations witnessing substantial growth in data center capacity, with major operators such as SUNeVision Holdings (iAdvantage), Digital Realty, Global Switch, and Telehouse expanding their presence. The area continues to attract strong investment driven by the rising demand for cloud adoption, colocation, and digital infrastructure.

- In Australia, Sydney and Melbourne remained the primary hubs for data center expansion, with major operators such as Equinix, AirTrunk, NEXTDC, Global Switch, Digital Realty, and STACK Infrastructure actively announcing new projects and capacity upgrades.

- Auckland is the major destination that is witnessing rapid data center development in New Zealand, as the city is one of the prominent business hubs in the country, offering lower latency and higher connectivity to support digital services in the country. Other New Zealand cities, including Christchurch, Hamilton, Invercargill, Palmerston, and Wellington, have gained momentum for data center development in the country in recent years.

- In 2025, in terms of data center development in Japan, Tokyo and Osaka are the major locations that witnessed the addition of data center space from operators such as AT TOKYO, Colt Data Centre Services, Digital Edge, Equinix, IDC Frontier, MC Digital Realty, NTT Communications, Telehouse, and AirTrunk

- Mumbai, Navi Mumbai, Hyderabad, Chennai, and Pune are the preferred locations in India, with major investments from colocation service providers such as ST Telemedia Global Data Centres, NTT DATA, CtrlS, Equinix, Sify Technologies, and Airtel (Nxtra Data).

- In South Korea, Seoul is the major center for the development of data centers. In recent years, cities such as Incheon, Bucheon-si, Paju, Pohang, Daegu, Busan, Namyangju, Sejong, Goyang, Jeollanam-do Province, Gyeonggi, Seongnam, Anyang, Gimhae, Cheonan, Daejeon, Cheongju, Gimpo, and Pyeongchon have gained momentum for data center development.

- Taipei is the preferred location in Taiwan, with major investments from data center operators such as Keppel Data Centers, Epoch Digital (Actis), Chunghwa Telecom, Empyrion Digital, SC Zeus Data Centers, and others.

- Singapore is one of the most expensive markets in the world for developing data center facilities. In addition, land availability for data center development is very limited. Operators continue to purchase industrial plots to convert into data centers; however, such activities remain relatively low in the market.

- Jakarta is the preferred location in Indonesia, with major investments from colocation service providers such as ST Telemedia Global Data Centres, EdgeConneX, Princeton Digital Group, NTT DATA, DAMAC Digital, and MettaDC.

- Cyberjaya is the most established and preferred hub for data centers in Malaysia; it is known for its robust power infrastructure, connectivity, and government support. It hosts major players such as AIMS Data Centre, Bridge Data Centres, Telekom Malaysia, and NTT DATA, making it the primary data center cluster of the country.

- Thailand offers foreign ownership flexibility, access to pre-approved energy and fiber infrastructure, as well as various incentives through its EEC, which makes it the perfect location to invest in Southeast Asia. Bangkok is the preferred location in Thailand, with major investments from colocation service providers such as ST Telemedia Global Data Centres, AIS Business (CSL), OneAsia Network, True IDC, Internet Thailand, Telehouse, and SUPERNAP Thailand.

- Manila remains the primary data center hub in the Philippines, accounting for the largest concentration of operational facilities in the Philippines.

- Hanoi and Ho Chi Minh City are the most preferred locations for data center operators in Vietnam. Hanoi accounts for the highest number of data center facilities in the country.

DATA CENTER COLOCATION MARKET VENDORS IN APAC

- In 2025, the APAC data center colocation market is driven by major colocation operators such as, China Telecom, China Mobile, China Unicom, Equinix, GDS Services, Chindata Group, AirTrunk, VNET, NTT DATA, ST Telemedia Global Data Centres, Digital Realty, CDC Data Centres, CDC Data Centres, SUNeVision Holdings, LG Uplus, NEXTDC, Shanghai Atrium, Nxera (Singtel), CtrlS Datacenters, Keppel Data Centres, Sify Technologies, Telkom Indonesia, and DCI Indonesia.

- In 2025, the growing demand from customers across various verticals, especially cloud service providers, as well as the increasing digitalization efforts by private and public sector organizations across the region, is set to propel the entry of several new investors. New entrants include AM Green Group, Aqylon Nexus, AREA Group of Companies, Asia Pacific Land, BW DIGITAL, Chinachem Group, CloudHQ, CURRENC Group, CyrusOne, Daewoo Engineering & Construction, DAMAC Digital, Data Center First, DC Connects, Doma Infrastructure Group, Diode Ventures, Endec, ESR, Everstone Group, Evolution Data Centres, FIR HILLS, FLOW Digital Infrastructure, FutureData, Global Telecommunications, GreenSquareDC, Haoyang Data, i-Berhad, Trifalga, and ZDATA Group.

- In terms of colocation revenue, China Telecom dominated the APAC data center colocation market in 2025. China Telecom was followed by China Mobile, China Unicom, GDS Services, Equinix, AirTrunk, among others.

SNAPSHOT

The APAC data center colocation market by investment is projected to reach USD 64.08 billion by 2031, growing at a CAGR of 15.36% from 2025 to 2031.

The following factors are likely to contribute to the growth of the APAC data center colocation market during the forecast period:

- Increasing Adoption of Cloud Computing Services

- Advancements in Big Data, IoT, and Smart City Projects

- Surge in Submarine Cable Connectivity Fuelling Data Center Growth

- Increasing Joint Ventures in the Market

- Adoption of Sustainability Measures among Data Center Operators

Base Year: 2025

Forecast Year: 2026-2031

The report considers the present scenario of the APAC data center colocation market and its market dynamics for 2026−2031. It covers a detailed overview of several market growth enablers, restraints, and trends. The study includes the demand and supply aspects of the APAC data center colocation industry.

Prominent Colocation Operators

- AirTrunk

- CDC

- China Mobile International

- China Telecom Corporation

- China Unicom

- Chindata Group

- Digital Realty

- Equinix

- GDS Holdings

- Keppel Data Centres

- NEXTDC

- NTT DATA

- Princeton Digital Group

- ST Telemedia Global Data Centres

- Telkom Indonesia

- Vantage Data Centers

Other Prominent Colocation Operators

- AdaniConneX

- A-FLOW

- AIMS Data Centre

- Anant Raj Cloud Data Center

- Athub

- @Tokyo

- BDx Data Centers

- Beeinfotech PH

- Beijing Sinnet Technology

- BRIGHTRAY

- BSNL

- CapitaLand

- CAT Telecom Public Company

- Centuria Capital Group

- Chayora

- Chief Telecom

- Chunghwa Telecom

- CMC Telecom

- Colt Data Centre Services

- Converge ICT Solutions

- CtrlS Datacenters

- DayOne

- DCI Data Centers

- DCI Indonesia

- Digital Edge DC

- Digital Halo

- DITO Telecommunity

- Dr. Peng Telecom & Media Group

- EdgeConneX

- Empyrion Digital

- ePLDT

- Epoch Digital

- ESDS Software Solution

- Etix Everywhere

- FPT Telecom

- Fujitsu

- Gaw Capital

- Global Switch

- Goodman

- GSA DATA CENTER

- Hotwon Network Group

- Internet Initiative Japan

- Iron Mountain

- iTech Towers Data Centre Services

- KORAMCO Asset Management

- KT Corp

- LG CNS

- LG Uplus

- Macquarie Data Centres

- Mapletree

- MettaDC

- Nxera

- Nxtra by Airtel

- OneAsia Network

- Open DC

- Pi Data Centers

- Pure Data Centres Group

- RackBank

- Racks Central

- RailTel Corporation of India

- Reliance Jio

- Samsung SDS

- Secom Trust Systems

- Sify Technologies

- SK Broadband

- SK ecoplant

- SKYY Development,

- SM+

- ST Engineering

- STACK Infrastructure,

- SUNeVision Holdings

- T4 NZ Data Centres

- Techno Electric & Engineering Company (TEECL)

- Telehouse

- Tenglong Holding Group

- VADS Berhad

- TenPeaks Data Centres

- True Internet Data Center (True IDC)

- Viettel IDC

- VNET Group

- VNPT

- VNTT

- YCO Cloud

- Yondr Group

- Yotta Data Services

- YTL Data Center

- Ada Infrastructure

New Entrants

- AIZO Group Berhad

- AM Green Group

- Aqylon Nexus

- AREA Group Of Companies

- Asia Pacific Land (APL)

- Aslan Energy Capital (AEC)

- BW DIGITAL

- Changhae Development

- Chinachem Group (CCG)

- CloudHQ

- Create Capital Viet Nam Joint-stock Company + haymaker+ Vietnam Data Gen

- CURRENC Group

- CyrusOne

- Da Nang International Data Centre Joint Stock Company (JSC),

- Daewoo Engineering & Construction

- DAMAC Digital

- Data Center First

- Datagrid New Zealand

- DC Connects

- Doma Infrastructure Group

- Dongyang

- Diode Ventures

- Endec,

- ESR

- Everstone Group

- Evolution Data Centres

- FIR HILLS

- FLOW Digital Infrastructure

- FutureData

- GIBO Holdings

- GigaStream Toyama

- Global Telecommunications

- GreenSquareDC

- Haoyang Data

- Henox IT And Datacenters

- Hyosung Corporation

- i-Berhad

- IGIS Asset Management

- Infracrowd Capital

- Inuverse

- ISPT

- IPTP Networks

- Kakao Corp.

- KinhBacCity Group (KBC)

- KOSCOM

- Lehr Consultants International (LCI Consultants)

- LG Electronics, KEPKO, & Hanwha Corporation E&C Division’s

- MaNaDr Mobile Health

- THOMSON Computing – METAVISIO

- MARKHAM

- Megaspeed AI

- MyTelehaus

- Nautilus Data Technologies

- NES DATA

- OKESTRO

- Perri Group

- Supernode by Quinbrook Infrastructure Partners

- Rovision Tech Hub

- Siagon Asset Management

- Saigontel

- SC Zeus Data Centers

- SEAX Global

- SGC Energy

- Stellar DC

- Tata Consultancy Services & OpenAI’s

- Toyota Tsusho Corporation

- TPG Angelo Gordon

- Trifalga

- UPC Volt

- ZDATA Group

- Zr Power Holdings

Segmentation by Colocation Type

- Retail Colocation

- Wholesale Colocation

Segmentation by Infrastructure

- Electrical Infrastructure

- Mechanical Infrastructure

- General Construction

Segmentation by Electrical Infrastructure

- UPS Systems

- Generators

- Transfer Switches & Switchgear

- PDUs

- Other Electrical Infrastructure

Segmentation by Mechanical Infrastructure

- Cooling Systems

- Racks

- Other Mechanical Infrastructure

Segmentation by Cooling Systems

- CRAC & CRAH Units

- Chiller Units

- Cooling Towers, Condensers & Dry Coolers

- Economizers & Evaporative Coolers

- Other Cooling Units

Segmentation by Cooling Techniques

- Air-based Cooling

- Liquid-based Cooling

Segmentation by General Construction

- Core & Shell Development

- Installation & Commissioning Services

- Engineering & Building Design

- Fire Detection & Suppression

- Physical Security

- DCIM/BMS Solutions

Segmentation by Tier Standard

- Tier I & II

- Tier III

- Tier IV

Segmentation by Geography

- APAC

- China

- Hong Kong

- Australia

- New Zealand

- Japan

- India

- South Korea

- Taiwan

- Rest of APAC

- Southeast Asia

- Singapore

- Indonesia

- Malaysia

- Thailand

- Philippines

- Vietnam

- Other Southeast Asian Countries

APAC DATA CENTER COLOCATION MARKET FAQs

How big is the APAC data center colocation market?

What is the growth rate of the APAC data center colocation market?

What are the key trends in the APAC data center colocation market?

What is the estimated market size in terms of area in the APAC data center colocation market by 2031?

How much MW of power capacity is expected to reach the APAC data center colocation market by 2031?

What are the key trends in the APAC data center colocation market?

What is the growth rate of the APAC data center colocation market?

For more details, please reach us at [email protected]

For more details, please reach us at [email protected]

Select a license type that suits your business needs

Single User Licence

- Report accessible by one user only

- Free 10% or 3 days of customization

- Free post-sale service assistance

- Continuous support through email

5 User Licence

- Report accessible by 5 users within the organization

- Free 15% or 4.5 days of customization

- Continuous support through email and telephone

- Free analyst hour

- Free Upgrade: If an updated report published within 180 days of purchase, you will get the revised report free of charge

Corporate Licence

- Free Datasheet worth $1500

- Report accessible by the entire organization

- Free 20% or 6 days of customization

- Free post-sale service assistance

- Continuous support through email and telephone

- Direct access to lead analysts

- Free analyst hour

- Free Upgrade: If an updated report published within 180 days of purchase, you will get the revised report free of charge

Datasheet Licence

- Report accessible by 1 user only

- Free 15% or 32 hours of customization

- Free post-sale service assistance

- Direct access to lead analysts

Frequently Asked Questions

How big is the APAC data center colocation market?

What is the growth rate of the APAC data center colocation market?

What are the key trends in the APAC data center colocation market?

What is the estimated market size in terms of area in the APAC data center colocation market by 2031?

How much MW of power capacity is expected to reach the APAC data center colocation market by 2031?

What are the key trends in the APAC data center colocation market?

What is the growth rate of the APAC data center colocation market?

Other RELATED Reports

Latin America Data Center Colocation Market – Industry Outlook & Forecast 2026-2031

Published : June 2026

Southeast Asia Data Center Colocation Market – Industry Outlook & Forecast 2026-2031

Published : June 2026

Middle East Data Center Colocation Market – Industry Outlook & Forecast 2025-2030

Published : November 2025

Europe Data Center Colocation Market – Industry Outlook & Forecast 2025-2030

Published : January 2026