APAC Data Center Construction Market – Industry Outlook & Forecast 2026-2031

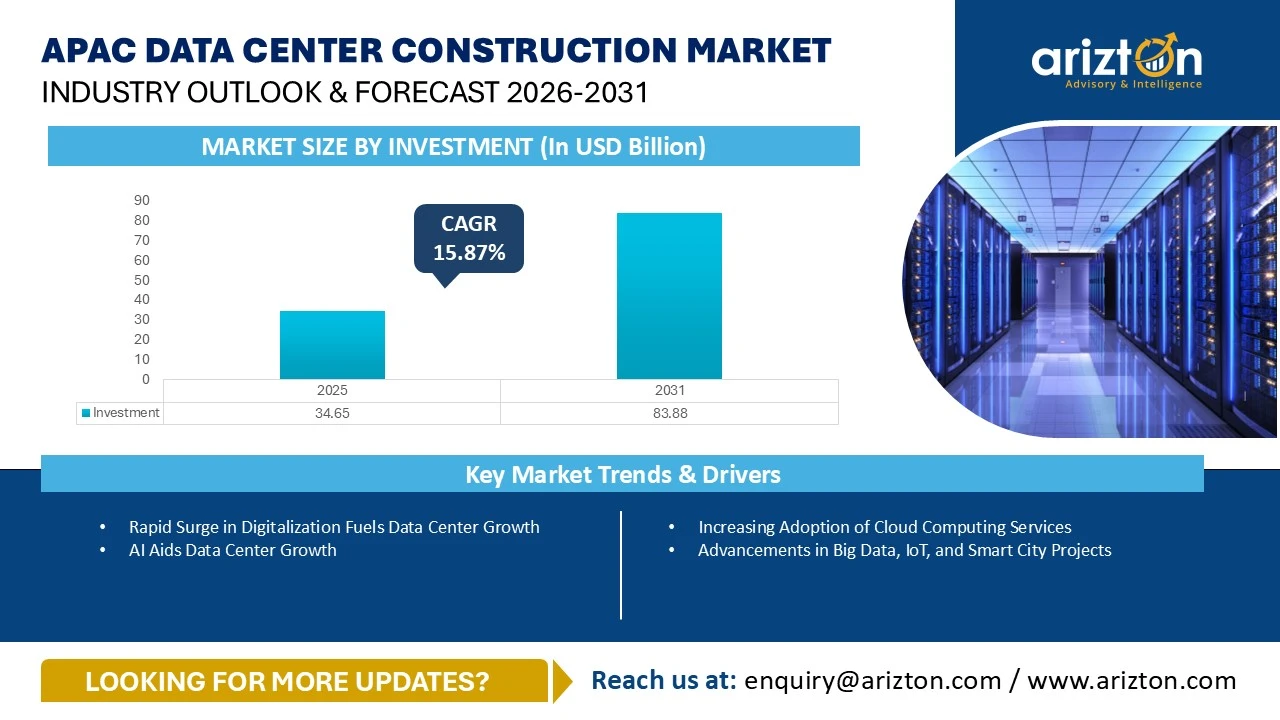

APAC DATA CENTER CONSTRUCTION MARKET SIZE WAS VALUED AT USD 34.65 BILLION IN 2025 AND IS EXPECTED TO REACH USD 83.88 BILLION BY 2031, GROWING AT A CAGR OF 15.87% DURING 2025-2031.

473 pages

319 company

9 segments

1 region

16 countries

Purchase Options

APAC Data Center Construction Market – Industry Outlook & Forecast 2026-2031

APAC DATA CENTER CONSTRUCTION MARKET SIZE WAS VALUED AT USD 34.65 BILLION IN 2025 AND IS EXPECTED TO REACH USD 83.88 BILLION BY 2031, GROWING AT A CAGR OF 15.87% DURING 2025-2031.

The APAC Data Center Construction Market Research Report Includes Size, Share, and Growth in Terms of

- Facility Type: Hyperscale Data Centers, Colocation Data Centers, and Enterprise Data Centers

- Infrastructure: Electrical Infrastructure, Mechanical Infrastructure, and General Construction

- Electrical Infrastructure: UPS Systems, Generators, Transfer Switches & Switchgears, PDUs, and Other Electrical Infrastructure

- Mechanical Infrastructure: Cooling Systems, Racks, and Other Mechanical Infrastructure

- Cooling System: CRAC & CRAH Units, Chillers Units, Cooling Towers, Condensers, and Dry Coolers, and Other Cooling Units

- Cooling Techniques: Air-based Cooling and Liquid-based Cooling

- General Construction: Core & Shell Development, Installation & Commissioning Services, Engineering & Building Design, Fire Detection & Suppression, Physical Security, and DCIM/BMS Solutions

- Tier Standards: Tier I & Tier II, Tier III, and Tier IV

- Geography: China, Hong Kong, Australia, New Zealand, Japan, India, South Korea, Taiwan, Rest of APAC, and Southeast Asia (Singapore, Indonesia, Malaysia, Thailand, Philippines, Vietnam, and Other Southeast Asian Countries)

Industry Analysis Report, Regional Outlook, Growth Potential, Price Trends, Competitive Market Share & Forecast 2026–2031.

This report includes market data points, ranging from trend

analyses to market estimates & forecasts that you can customize

APAC DATA CENTER CONSTRUCTION MARKET REPORT SCOPE

| REPORT ATTRIBUTE | DETAILS |

|---|---|

| MARKET SIZE BY INVESTMENT (2031) | USD 83.88 Billion |

| MARKET SIZE BY INVESTMENT (2025) | USD 34.65 Billion |

| CAGR BY INVESTMENT (2025-2031) | 15.87% |

| MARKET SIZE - AREA (2031) | 32.57 Million Sq. Ft. |

| POWER CAPACITY (2031) | 8,343 MW |

| HISTORIC YEAR | 2022-2024 |

| BASE YEAR | 2025 |

| FORECAST YEAR | 2026-2031 |

| MARKET SEGMENTS | Facility Type, Infrastructure, Electrical Infrastructure, Mechanical Infrastructure, Cooling Systems, Cooling Technique, General Construction, Tier Standards, and Geography |

| GEOGRAPHICAL ANALYSIS | China, Hong Kong, Australia, New Zealand, Japan, India, South Korea, Taiwan, Rest of APAC, and Southeast Asia (Singapore, Indonesia, Malaysia, Thailand, Philippines, Vietnam, and Other Southeast Asian Countries) |

APAC DATA CENTER CONSTRUCTION MARKET SIZE

The APAC data center construction market size was valued at USD 34.65 billion in 2025 and is expected to reach USD 83.88 billion by 2031, growing at a CAGR of 15.87% during the forecast period. China, Japan, Australia, and India are among the major data center hubs that are increasingly focusing on digital transformation and technological advancements across the APAC region. However, nations like Indonesia, Malaysia, Hong Kong, South Korea, Taiwan, Singapore, and Thailand are also attracting data center operators with several tax incentives and government support for advancing digital infrastructure across these countries.

China is continuing to dominate data center investments in the APAC data center construction market, with over 41.81% of data center investment share in 2025. Following China, Australia, Malaysia, India, South Korea, the Philippines, and Taiwan are positioning themselves as prominent locations for the development of hyperscale and colocation data centers, attracting investments from both local and global data center companies.

Other APAC and Southeast Asian countries like Bhutan, Nepal, Sri Lanka, Pakistan, Bangladesh, Myanmar, Cambodia, Laos, and Brunei are seeing data center investments from colocation and enterprise companies, with IT power capacities of less than 10 MW.

The factors like increasing adoption of Artificial Intelligence, government support for data centers, advancements in emerging technologies like robotics, machine leaning, big data & Internet of Things, rising adoption of sustainability initiatives among data center operators, adoption of liqud cooling technologies in data centers, increasing demand for cloud-computing technologies, rapid digitalization, advancements in smart city projects, and other factors are fuelling the demand for data centers in the APAC data center construction market.

INVESTMENT BY AREA SQ.FT

- In March 2026, EdgeConneX, the global data center operator, initiated the construction of an AI-ready data center campus, spanning around 1.4 million sq ft in Osaka, Japan, in partnership with Kagoya Asset Management. The first phase of the data center is expected to go live in 2028.

- In March 2026, ESR initiated the construction of the second phase of ESR Kwai Chung Data Center (HKDC1), which is anticipated to deliver a white-floor area of around 290 thousand sq ft in Hong Kong. The data center is expected to get ready for service by 2028.

INVESTMENT BY POWER

- In December 2025, AirTrunk, an APAC data center firm, planned to develop the OSK2 data center campus, offering a power capacity of around 100 MW in Osaka, Japan.

- As of 2025, industrial electricity prices in India ranged from $0.07 to $0.12 per kWh. The price was lower than in other APAC countries such as Japan, China, Singapore, Thailand, Taiwan, and South Korea.

TOP COUNTRIES IN APAC DATA CENTER

China Data Center Market Analysis - $101.47 Billion (2031) | CAGR - 8.94%

Japan Data Center Market Analysis - $38.92 Billion (2031) | CAGR - 20.42%

India Data Center Market Analysis - $21.03 Billion (2031) | CAGR - 13.59%

APAC DATA CENTER CONSTRUCTION MARKET SEGMENTATION INSIGHTS

- APAC data center construction market is experiencing hyperscale data center investments from several local and global hyperscale data center companies. In the APAC data center construction market, the hyperscale data center investments have increased by approximately 15.70%, compared to 2024. In December 2025, Amazon Web Services collaborated with the government of Telanana to enhance India’s cloud and data center infrastructure with an investment of around $7 billion.

- Colocation data centers contribute to generating the majority of data center investments in the APAC region. In the APAC data center construction market, the colocation data centers contributed to generating approximately 78.48% of the data center investments in 2025. In October 2025, Equinix, the colocation giant, announced that the company had completed the construction of its JH2 data center facility in Johor, Malaysia, with an investment of around $201 million.

- Data center companies in the APAC region are investing significantly to develop AI-ready data centers, which are equipped with clusters of graphics processing units (GPUs), advanced liquid cooling technologies, high-density racks, and higher IT capacity loads. For instance, in January 2026, the APAC-based data center firm, Digital Edge DC, revealed its plans to develop an AI-optimized data center in Jakarta, Indonesia, with an investment of approximately $4.5 billion. The APAC nations are slated to witness continuous investments in the development of AI read data centers during the forecast period.

- As the demand for sustainable data center infrastructure is increasing rapidly, data center operators are increasingly investing in low-carbon-impact power and cooling infrastructure components. In terms of power infrastructure, data center firms are investing in lithium-ion batteries, Hydrotreated Vegetable Oil (HVO) powered generators, and advanced power distribution units. For example, Microsoft has equipped its data center in South Korea with renewable biofuel-powered backup generators to lower carbon emissions.

- In the APAC data center construction market, the demand for liquid cooling techniques is slated to increase significantly among data centers during the forecast period. Liquid cooling technologies contributed around 55.2% of the cooling technique investments in 2025 in the APAC region; as the demand for processing advanced Artificial Intelligence and high-performance computing workloads is increasing significantly, the liquid cooling techniques are anticipated to contribute approximately 59% of the cooling technique investments in 2031. Multiple data center companies are investing in installing advanced liquid cooling techniques like direct-to-chip liquid cooling and immersion cooling techniques in data centers for improved thermal management.

- To support complex Artificial Intelligence workloads, several data center companies are prioritizing the installation of high-density racks in their data centers. DC Connects, the center company, aims to install high-density racks, which can deliver rack power densities ranging from 60 kW to 200 kW in its Seoul1 data center in South Korea.

- In the APAC data center construction market, the demand for intelligent security systems is slated to increase significantly during the forecast period to protect the facilities against potential physical security threats. In recent years, data center companies have been installing biometric card readers, access control systems, Closed-Circuit Television (CCTV) surveillance, perimeter fencing, and other physical security systems in data centers.

- Data center operators are increasingly investing in DCIM/BMS software in their facilities to minimize power consumption and carbon emissions, along with reducing the operational costs of data centers. The installation of this software simplifies data center management while eliminating the need for human involvement. Open DC, the data center company, has invested in installing a 24/7 BMS monitoring system in its JB1 data center in Johor, Malaysia.

APAC DATA CENTER CONSTRUCTION MARKET TRENDS

Rapid Surge in Digitalization Fuelling Data Center Growth

- The nations across the APAC region are experiencing rapid digital transformation, which is reshaping the economy while driving the demand for data center infrastructure across the APAC countries. The surge in advancements of cloud computing, e-commerce, fintech, Artificial Intelligence, and other digital services is significantly increasing data storage and processing needs, increasing the demand for high-performance and low-latency data center infrastructure.

- In November 2025, the Taiwanese technology company, FPT Software, revealed that the company collaborated with two financial institutions in Taiwan, namely, OBank and E.SUN Commercial Bank, to boost their digital transformation.

- As the enterprises across various sectors continue to adopt digital services, the need for real-time data processing is anticipated to increase, rising the requirement for data centers across the APAC region to process and store large amounts of data to support digital services across the APAC countries.

Artificial Intelligence Aiding Data Center Investments

- The rising adoption of Artificial Intelligence is experiencing significant growth, fueled by technological advancements and increasing focus on technology innovations. Artificial Intelligence plays a pivotal role in driving digital transformation across various sectors. The businesses across a wide range of industries are increasingly integrating Artificial Intelligence into their daily operations to boost operational efficiency and revenue generation.

- In January 2026, the Chinese company, Alibaba Group, revealed its plans to invest approximately $69.05 billion to boost China’s Artificial Intelligence infrastructure over the next three years.

- Multiple servers are needed to process huge volumes of data generated by AI workloads; the operation of such huge advanced servers will generate more amounts of heat, requiring the need for continuous power supply and high-density racks. The rise in Artificial Intelligence advancements will increase the demand for liquid cooling techniques to manage thermal workloads efficiently in data centers.

Rising Adoption of Liquid Cooling Technologies in Data Centers

- APAC is one of the prominent hubs that is increasingly adopting advanced technologies such as Artificial Intelligence, big data, Internet of Things, and others. The governments across the APAC countries are establishing various measures to increase advancements in emerging technologies to drive the digital economy. Therefore, the demand for AI-optimized data centers is increasing significantly across the APAC nations. AI data centers require advanced cooling techniques like direct-to-chip liquid cooling and immersion cooling for efficient thermal management.

- In November 2025, Princeton Digital Group, the APAC-based data center company, initiated the construction of the JC3 data center campus, which will be equipped with advanced liquid cooling technologies.

- In the APAC region, the adoption of liquid cooling in data centers is still in early phases. The surge in advancements of emerging technologies is likely to increase the demand for liquid cooling technologies in the forecast period to dissipate huge volumes of heat generated to process Artificial Intelligence and high-performance computing workloads.

APAC DATA CENTER CONSTRUCTION MARKET ENABLERS

Increasing Adoption of Cloud Computing Technologies

- The need for cloud computing technologies across the APAC nations is significantly increasing, creating more growth opportunities for cloud service providers, fuelled by the rising digitalization, advancements in 5G connectivity, and strict data regulation laws.

- In November 2025, Microsoft, the hyperscale company, revealed its plans to establish new cloud regions across multiple Asian countries, including India, Taiwan, and others, in 2026. Microsoft’s new cloud region in India is likely to be in Hyderabad.

- The surge in adoption of cloud-computing services across the APAC nations will increase the demand for data center infrastructure as the cloud companies will require low-latency and scalable data center infrastructure to host cloud computing workloads, and support the expanding digital ecosystem, while increasing data sovereignty.

Advancements in Big Data, Internet of Things (IoT), and Smart City Projects

- Emerging technologies like big data and the Internet of Things are becoming essential tools for enterprises to collect, process, and manage huge volumes of data. Through IoT, the enterprises can gain access to cost-efficient data management, scalable storage, and real-time analytics. The rising adoption of big data and the Internet of Things is slated to promote digital transformation and renewable energy generation across the APAC countries.

- Osaka and Tokyo secured 99th and 108th ranks globally according to the IMD Smart City Index 2025. These ranks highlight various factors like digital infrastructure development, technological advancements, and quality of life across Osaka and Tokyo. Japan’s Society 5.0 Smart City plan intends to create a large super-smart society by leveraging digital technologies and focusing on addressing societal challenges through technological innovation.

- The surge in adoption of emerging technologies like big data and Internet of Things, and advancements in smart city projects, are likely to increase the demand for edge data centers across the APAC countries during the forecast period to store data closer to the end users.

Surge in Submarine Cable Connectivity Fuels Data Center Growth

- The rising development of submarine cables and inland fiber connectivity is transforming the digital infrastructure across APAC nations, and increasing the demand for data center infrastructure. Submarine cables are responsible for carrying around 95% of the global data traffic, and these cables enable high-capacity and low-latency data transfer among global markets. As the submarine cable operators continue to invest in transoceanic routes, the demand for regional landing stations and edge data centers is likely to increase significantly across the APAC countries.

- In November 2025, Google revealed its plans to develop the TalayLink submarine cable, which is likely to increase digital connectivity and data transmission speeds between Melbourne and Perth in Australia and Thailand.

- The increasing investments in submarine and inland connectivity across the APAC nations are slated to boost the region’s connectivity with Europe, the Middle East, and American countries, while strengthening the region’s international bandwidth capacity and increasing network resilience to position APAC as one of the leading digital hubs.

APAC DATA CENTER CONSTRUCTION MARKET GEOGRAPHICAL ANALYSIS

- In the APAC data center construction market, China led the market in terms of power capacity in 2025, with a share of approximately 53.25%, followed by Southeast Asia with a share of around 16.65%. This dominance is expected to continue during the forecast period, with China projected to account for over 52.98% of the APAC data center construction market’s power capacity in 2031, followed by South Asia, which is anticipated to contribute around 17.20% of the market’s power capacity share during the same period.

- The increasing adoption of Artificial Intelligence (AI) among enterprises and individuals across China is revolutionizing data center investments in the country. In China, more than 515 million individuals rely on Artificial Intelligence (AI) for their daily operations, and the country aims to further increase Artificial Intelligence adoption over the next three to five years. The government of China is committed to increasing the adoption of Artificial Intelligence to approximately 70% of the Chinese population by 2027, and to over 90% by 2030.

- In the APAC region, India and Australia are among the largest data center markets after China, contributing around 12.39% and 12.16% of the APAC data center investments, respectively, in 2025. These nations are experiencing rapid growth in data center investments from domestic as well as global data center companies.

- In the APAC region, the costs of constructing data centers vary significantly from one nation to another. Japan and Singapore are among the most expensive markets in terms of data center construction costs, in which the average costs of constructing a data center stood at approximately $15 per watt as of December 2025. However, the data center construction costs in countries like China, India, South Korea, Indonesia, Malaysia, and other countries are comparatively lower than those in Japan and Singapore.

- Japan contributed approximately 7.68% of the data center investments in the APAC data center construction market in 2025. The increasing government support for the data center industry and rising demand for Artificial Intelligence are playing a crucial role in driving data center investments in the country. The government of Japan intends to invest approximately $65 billion to enhance the country’s Artificial Intelligence Infrastructure by 2030.

- Hong Kong serves as a gateway to China, owing to the country’s strategic location and digital connectivity with China. Hong Kong resulted in generating over 1.83% of the overall investments in the APAC data center construction market in 2025.

- Owing to the surge in land and power availability challenges across the primary hubs of the APAC region, data center companies have been prioritizing developing data centers in emerging and secondary locations of the region, such as Malaysia, Indonesia, New Zealand, Taiwan, India, and other countries are continuing to witness a surge in data center investments in recent years. The data center saturated locations like Singapore, Tokyo, Osaka, Sydney, and Hong Kong are experiencing a significant rise in land and power availability challenges. Meanwhile, locations like Jakarta, Cyberjaya, Johor, Auckland, Canberra, and others are gaining momentum for the development of data centers.

- In 2025, Indonesia contributed around 14.42% of the Southeast Asia data center construction market’s data center investments, and the country generated approximately 2.74% of the data center investments in the APAC data center construction market during the same period.

- The Taiwanese government is making substantial efforts to support industrial development. It has established multiple technology and industrial parks across the country. Some of the prominent industrial parks in Taiwan include the Nangang Software Park, Neihu Technology Park, the Yunlin technology-based industrial park, and others.

- The nations across the APAC region are making significant strides to reduce their climate impact. For instance, Japan is committed to achieving carbon neutrality by 2050. The country aims to minimize carbon emissions by approximately 70% by 2040. Additionally, New Zealand aims to achieve a net-zero greenhouse gas emissions target by 2050.

APAC DATA CENTER CONSTRUCTION MARKET VENDOR LANDSCAPE

- In the APAC data center construction market, colocation companies account for majority of data center investments. Some of the prominent colocation companies in the market include, AirTrunk, BDx Data Centers, CDC, China Telecom Corporation, China Mobile International, China Unicom, Chindata Group, DayOne, Digital Realty, Equinix, GDS Holdings, Keppel Data Centres, NEXTDC, NTT DATA, Princeton Digital Group, ST Telemedia Global Data Centres, AdaniConneX, Anant Raj Cloud Data Center, BRIGHTRAY, CapitaLand, Chayora, Chunghwa Telecom, Colt Data Centre Services, CtrlS Datacenters, DCI Data Centers, EdgeConneX, Fujitsu, Global Switch, Iron Mountain, LG CNS, LG Uplus, Nxtra by Airtel, Pure Data Centres Group, Sify Technologies, STACK Infrastructure, Telehouse, Vantage Data Centers, Yondr Group, and others.

- Several local and global hyperscale companies are investing significantly to enhance hyperscale data center infrastructure in the APAC region. Alibaba Group, Amazon Web Services, Apple, Google, Meta, and Microsoft are some of the prominent hyperscale data center companies expanding their operations across the APAC nations.

- The APAC data center construction market hosts numerous local and global support infrastructure providers. The companies like ABB, Airedale, Aksa Power Generation, Alfa Laval, Baudouin, Carrier, Caterpillar, Cummins, Cyber Power Systems, Delta Electronics, ENGIE, Eaton, Fuji Electric, Hitachi Energy, HITEC Power Protection, Honeywell, Legrand, Mitsubishi Electric, Rehlko, Rittal, Rolls-Royce, Schneider Electric, Siemens, STULZ, Vertiv, and other support infrastructure companies offer power, cooling, and general infrastructure components to data centers.

- The APAC data center construction market is anticipated to witness the entry of several new entrants to address the rising demand for data center infrastructure across the APAC nations. The market is witnessing the entry of new entrants like Asia Pacific Land (APL), Aslan Energy Capital, BW DIGITAL, CloudHQ, DAMAC Digital, Datagrid New Zealand, Evolution Data Centres, FIR HILLS, GreenSquareDC, Haoyang Data, i-Berhad, Kakao Corp, KOSCOM, THOMSON Computing - METAVISIO, Megaspeed AI, Nautilus Data Technologies, OKESTRO, Saigontel, SC Zeus Data Centers, Trifalga, ZDATA Group, and others.

- The construction contractors like AECOM, Arup, AtkinsRéalis, Beca, China Electronics Engineering Design Institute, Corgan, DPR Construction, DSCO Group, Fortis Construction, Gammon Construction, HDR, Heerim Architects & Planners, Hyundai Engineering & Construction, Icon Construction, JSLA Architects, Kienta Engineering Construction, Larsen & Toubro, Linesight, Megawide Construction Corporation, PT Jaya Karya Integrasi (JKI), Ramboll, RED Engineering Design, Sterling and Wilson, Turner & Townsend, NTT Facilities, and others deliver construction, installation, commissioning, architectural, and engineering services to data center operators for the construction of data centers across the APAC nations.

SNAPSHOT

The APAC data center construction market size by investment will reach USD 83.88 billion by 2031, growing at a CAGR of 15.87% from 2025 to 2031.

The following factors are likely to contribute to the growth of the APAC data center construction market during the forecast period:

- Increasing Adoption of Cloud Computing Services

- Advancements in Big Data, IoT, and Smart City Projects

- Surge in Submarine Cable Connectivity Fuels Data Center Growth

- Increasing Joint Ventures in the Market

- Adoption of Sustainability Measures Among Data Center Operators

Base Year: 2025

Forecast Year: 2026-2031

The study considers the present scenario of the APAC data center construction market and its market dynamics for 2026−2031. It covers a detailed overview of several market growth enablers, restraints, and trends. The report offers both the demand and supply aspects of the market. It profiles and examines leading companies and other prominent ones operating in the market.

The report includes the investment in the following areas:

- Facility Type

- Hyperscale Data Centers

- Colocation Data Centers

- Enterprise Data Centers

- Infrastructure

- Electrical Infrastructure

- Mechanical Infrastructure

- General Construction

- Electrical Infrastructure

- UPS Systems

- Generators

- Transfer Switches & Switchgears

- PDUs

- Other Electrical Infrastructure

- Mechanical Infrastructure

- Cooling Systems

- Racks

- Other Mechanical Infrastructure

- Cooling System

- CRAC & CRAH Units

- Chillers Units

- Cooling Towers, Condensers, and Dry Coolers

- Other Cooling Units

- Cooling Techniques

- Air-based Cooling Technique

- Liquid-based Cooling Technique

- General Construction

- Core & Shell Development

- Installation & Commissioning Services

- Engineering & Building Design

- Fire Detection & Suppression

- Physical Security

- DCIM/BMS Solutions

- Tier Standards

- Tier I & Tier II

- Tier III

- Tier IV

- Geography

- China

- Hong Kong

- Australia

- New Zealand

- Japan

- India

- South Korea

- Taiwan

- Rest of APAC

- Southeast Asia

- Singapore

- Indonesia

- Malaysia

- Thailand

- Philippines

- Vietnam

- Other Southeast Asian Countries

VENDOR LANDSCAPE

Key Data Center Support Infrastructure Providers

- ABB

- Caterpillar

- Cummins

- Eaton

- Rittal

- Schneider Electric

- STULZ

- Vertiv

Other Data Center Support Infrastructure Providers

- 3M

- Aggreko

- Airedale

- AIRSYS

- Aksa Power Generation

- Alfa Laval

- Baudouin

- Bosch

- Canovate Group

- Carrier

- Condair Group

- Cyber Power Systems

- Danfoss

- Delta Electronics

- EAE Group

- EAST GROUP

- ENGIE

- ENVICOOL

- EVADA (Xiamen) Technology

- Fuji Electric

- Green Revolution Cooling (GRC)

- Hitachi Energy

- HITEC Power Protection

- Honeywell

- Hongbao Power Supply

- INVT Power

- KSTAR

- Legrand

- Mitsubishi Electric

- Nanjing Jialitu Data Center Environment Technology

- Narada

- Nortek Data Center Cooling

- Piller Power Systems

- Rehlko

- Rolls-Royce

- Shenling

- Siemens

- Socomec

- Submer

- Systermair Group

- Thycon

- Toshiba

- Trane

- ZTE Corporation

Key Data Center Construction Contractors

- AECOM

- Arup

- Aurecon

- CSF Advisors

- DSCO Group

- Gammon Construction

- Larsen & Tourbo

- NTT Facilities

- PM Group

- Studio One Design

Other Data Center Construction Contractors

- ADIK

- AEON SERVICES

- AHLUWALIA CONTRACTS

- Asima Architects

- AtkinsRéalis

- AWP Architects

- ARWADE INFRASTRUCTURE

- Beca

- B-Global Tech

- BYME Engineering

- China Electronics Engineering Design Institute (CEEDI)

- China State Construction Engineering Corporation (CSCEC)

- Chung Hing Engineers Group

- Corgan

- Critical Holdings

- CTCI

- Cundall

- DAIWA HOUSE INDUSTRY

- Design Coordinates

- DL E&C

- DPR Construction

- Exyte

- FDC Construction & Fitout

- Finishing Touch Design Studio

- Fortis Construction

- GAMUDA

- Gensler

- GS E&C

- HanmiGlobal

- Hanwha Corporation E&C Division

- HDR

- Heerim Architects & Planners

- Hutchinson Builders

- Hyundai Engineering & Construction

- Icon Construction

- ISG

- Infraset Public Company

- JSLA Architects

- Kienta Engineering Construction

- Leighton Asia

- Linesight

- LSK Engineering

- Mace

- Megawide Construction Corporation

- Meinhardt Group

- MES Group

- MN Holdings

- Nakano Construction

- Nikken Sekkei

- Obayashi Corporation

- Powerware Systems (PWS)

- PT. Aesler Group International Tbk

- PT AtoZ Teknik Sejahtera

- PT Berca Buana Sakti

- PT Jaya Karya Integrasi

- PT Jaya Teknik Indonesia

- PT Jaya Obayashi

- PT KAJIMA INDONESIA

- PT PP (Persero) Tbk

- PT Sumaraja Indah

- Ramboll

- RED Engineering Design

- Rider Levett Bucknall RLB

- SAMOO Architects & Engineers

- Samsung C&T

- Sterling & Wilson

- Syntec Construction Public Company

- Sunway Construction Group

- Taisei Corporation

- Takenaka Corporation

- TODA CORPORATION

- Turner & Townsend

- WT

Prominent Data Center Investors

- AirTrunk

- Alibaba Group

- Amazon Web Services

- Apple

- BDx Data Centers

- CDC

- China Mobile International

- China Telecom Corporation

- China Unicom

- Chindata Group

- DayOne

- Digital Realty

- Equinix

- GDS Holdings

- Keppel Data Centres

- Microsoft

- NEXTDC

- NTT DATA

- Princeton Digital Group

- ST Telemedia Global Data Centres

Other Data Center Investors

- AdaniConneX

- A-FLOW

- AIMS Data Centre

- Anant Raj Cloud Data Center

- @Tokyo

- Beeinfotech PH

- Beijing Sinnet Technology

- Lumina CloudInfra

- BRIGHTRAY

- BSNL

- CapitaLand

- Centuria Capital Group

- Chayora

- Chief Telecom

- Chunghwa Telecom

- CMC Telecom

- Colt Data Centre Services

- Converge ICT Solutions

- Ctrl SDatacenters

- DCI Data Centers

- DCI Indonesia

- Digital Edge DC

- Digital Halo

- DITO Telecommunity

- Dr. Peng Telecom & Media Group

- EdgeConneX

- Empyrion Digital

- ePLDT

- ESDS Software Solution

- FPT Telecom

- Fujitsu

- Gaw Capital

- Global Switch

- Goodman

- GSA DATA CENTER

- Hotwon Network Group

- Huawei

- IDC Frontier

- Internet Initiative Japan

- Iron Mountain

- iTech Towers Data Centre Services

- KORAMCO Asset Management

- KT Corp.

- Racks Central

- LG CNS

- LG Uplus

- Macquarie Data Centres

- Mapletree

- Meta

- MettaDC

- Singtel (Nxera)

- Nxtra by Airtel

- OneAsia Network

- Open DC

- Pure Data Centres Group

- Reliance Jio

- Samsung SDS

- Secom Trust Systems

- Sify Technologies

- SK Broadband

- SK ecoplant

- SKYY Development

- SM+

- ST Engineering

- STACK Infrastructure

- T4 NZ Data Centres

- Techno Electric & Engineering Company (TEECL)

- Telehouse

- VADS Berhad

- Telkom Indonesia

- Tenglong Holding Group

- TenPeaks Data Centres

- WHA Group

- True IDC

- Vantage Data Centers

- Viettel IDC

- VNET Group

- VNTT

- YCO Cloud

- Yondr Group

- Yotta Data Services

- YTL Data Center

- Ada Infrastructure

- @hub

- SUNeVision Holdings

- Etix Everywhere

- Epoch Digital

- RackBank

- VNPT

- CAT Telecom Public Company (National Telecom)

- RailTel Corporation

- Pi Data Centers

New Entrants

- AIZO Group Berhad

- AM Green Group

- Aqylon Nexus

- AREA Group of Companies

- Asia Pacific Land (APL)

- Aslan Energy Capital

- BW Digital

- Changhae Development

- Chinachem Group

- CloudHQ

- Create Capital Viet Nam Joint-stock Company + haimaker+ Vietnam Data Gen

- CURRENC Group

- CyrusOne

- Da Nang International Data Centre Joint Stock Company (JSC)

- Daewoo Engineering & Construction

- DAMAC Digital

- Data Center First

- Datagrid New Zealand

- DC Connects

- Doma Infrastructure Group

- Dongyang

- Diode Ventures

- Endec

- ESR

- Everstone Group

- Evolution Data Centres

- FIR HILLS

- FLOW Digtal Infrastructure

- FutureData

- GIBO Holdings

- GigaStream Toyama

- Global Telecommunications

- GreenSquareDC

- Haoyang Data

- Henox IT And Datacenters

- Hyosung Corporation

- i-Berhad

- IGIS Asset Management

- Infracrowd Capital

- Inuverse

- ISPT

- IPTP Networks

- Kakao Corp.

- KinhBacCity Group +Accelerated Infrastructure Capital +VietinBank

- KOSCOM

- Lehr Consultants International

- LG Electronics +KEPK + Hanwha Corporation E&C Division

- MaNaDr Mobile Health

- THOMSON Computing – METAVISIO

- MARKHAM

- Megaspeed AI

- MyTelehaus

- Nautilus Data Technologies

- NES DATA

- OKESTRO

- Perri Group

- Supernode by Quinbrook Infrastructure Partners

- Rovision Tech Hub

- Siagon Asset Management

- Saigontel

- SC Zeus Data Centers

- SEAX Global

- SGC Energy

- Stecon Group Public Company +SC Zeus Data Centers +Freyr Technology

- Tata Consultancy Services & OpenAI

- Toyota Tsusho Corporation

- TPG Angelo Gordon

- Trifalga

- UPC Volt

- ZDATA Group

- Zr Power Holdings

APAC DATA CENTER CONSTRUCTION MARKET FAQs

What is the growth rate of the APAC data center construction market?

What is the estimated market size in terms of area in the APAC data center construction market by 2031?

How many MW of power capacity is expected to reach the APAC data center construction market by 2031?

What are the key trends in the APAC data center construction market?

How big is the APAC data center construction market?

For more details, please reach us at [email protected]

For more details, please reach us at [email protected]

Select a license type that suits your business needs

Single User Licence

- Report accessible by one user only

- Free 10% or 3 days of customization

- Free post-sale service assistance

- Continuous support through email

5 User Licence

- Report accessible by 5 users within the organization

- Free 15% or 4.5 days of customization

- Continuous support through email and telephone

- Free analyst hour

- Free Upgrade: If an updated report published within 180 days of purchase, you will get the revised report free of charge

Corporate Licence

- Free Datasheet worth $1500

- Report accessible by the entire organization

- Free 20% or 6 days of customization

- Free post-sale service assistance

- Continuous support through email and telephone

- Direct access to lead analysts

- Free analyst hour

- Free Upgrade: If an updated report published within 180 days of purchase, you will get the revised report free of charge

Datasheet Licence

- Report accessible by 1 user only

- Free 15% or 32 hours of customization

- Free post-sale service assistance

- Direct access to lead analysts

Frequently Asked Questions

What is the growth rate of the APAC data center construction market?

What is the estimated market size in terms of area in the APAC data center construction market by 2031?

How many MW of power capacity is expected to reach the APAC data center construction market by 2031?

What are the key trends in the APAC data center construction market?

How big is the APAC data center construction market?

Other RELATED Reports

APAC Data Center Colocation Market - Industry Outlook & Forecast 2025-2030

Published : August 2025

Southeast Asia Data Center Construction Market – Industry Outlook & Forecast 2026-2031

Published : April 2026