Global Automotive Fasteners Market Research Report 2026-2031

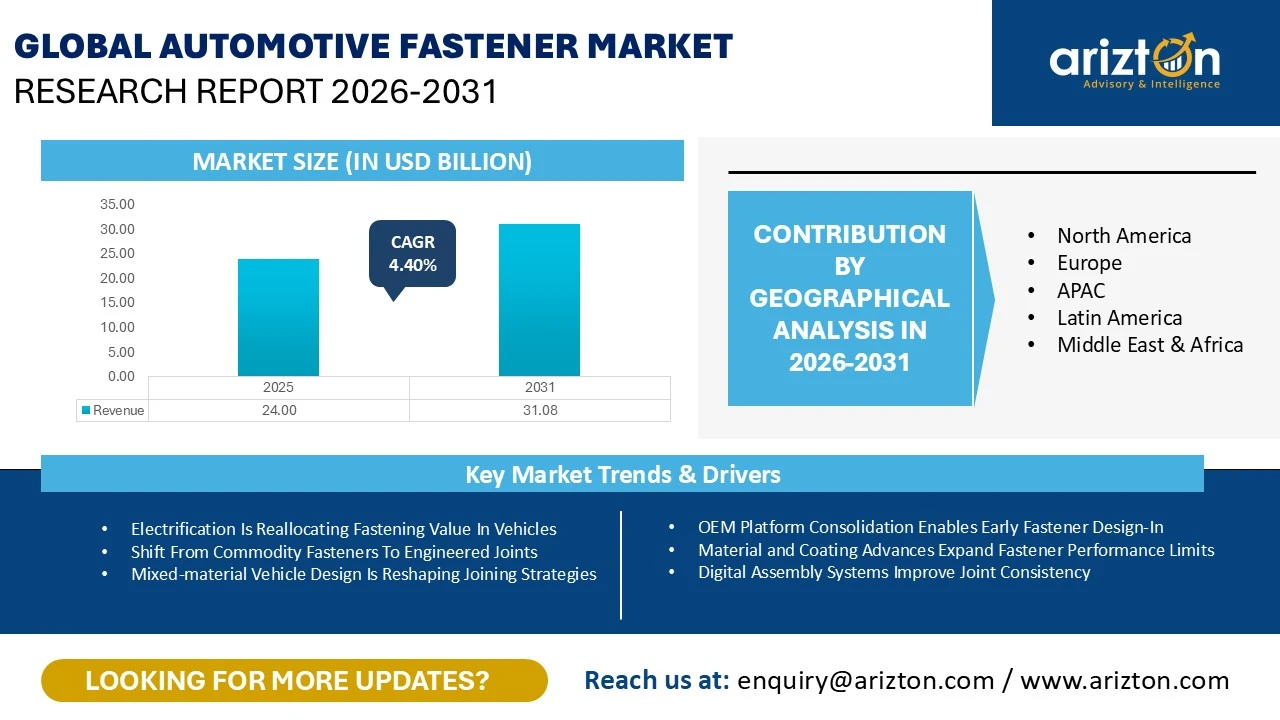

THE GLOBAL AUTOMOTIVE FASTENERS MARKET WAS VALUED AT USD 24 BILLION IN 2025 AND IS EXPECTED TO REACH USD 31.08 BILLION BY 2031, GROWING AT A CAGR OF 4.40% DURING THE FORECAST PERIOD.

Global Automotive Fasteners Market Research Report 2026-2031

THE GLOBAL AUTOMOTIVE FASTENERS MARKET WAS VALUED AT USD 24 BILLION IN 2025 AND IS EXPECTED TO REACH USD 31.08 BILLION BY 2031, GROWING AT A CAGR OF 4.40% DURING THE FORECAST PERIOD.

The Automotive Fasteners Market Size, Share & Trends Analysis Report By

- Product: Threaded Fasteners and Non-Threaded Fasteners

- Material: Iron, Stainless Steel, Plastic, Aluminium, Brass, Bronze, and Nickel

- Vehicle: Passenger Cars, Low Commercial Vehicles, and Heavy Commercial Vehicles

- Application: Engine, Chassis, Interior Trim, Transmission, Front/ Rear Axle, Steering, Wire Harnessing, and Others

- Distribution Channel: Original Equipment Manufacturers and Aftermarkets

- Fastening Characteristics: Non-Permanent and Permanent

- Geography: North America, Europe, APAC, Latin America, and Middle East & Africa

Industry Analysis Report, Regional Outlook, Growth Potential, Price Trends, Competitive Market Share & Forecast 2026–2031.

This report includes market data points, ranging from trend

analyses to market estimates & forecasts that you can customize

AUTOMOTIVE FASTENERS MARKET REPORT

| REPORT ATTRIBUTE | DETAILS |

|---|---|

| MARKET SIZE (2031) | USD 31.08 Billion |

| MARKET SIZE (2025) | USD 24 Billion |

| CAGR (2025-2031) | 4.40% |

| HISTORIC YEAR | 2022-2024 |

| BASE YEAR | 2025 |

| FORECAST YEAR | 2026-2031 |

| SEGMENTS BY | Product, Material, Fastening Characteristics, Application, Vehicle, Distribution Channel, and Geography |

| GEOGRAPHIC ANALYSIS | North America, Europe, APAC, Latin America, and Middle East & Africa |

| KEY PLAYERS | KAMAX, Würth Group, Nifco, Illinois Tool Works Inc., Araymond, and Gruppo Fontana |

AUTOMOTIVE FASTENER MARKET SIZE & SHARE ANALYSIS

The global automotive fasteners market size is valued at USD 24 billion in 2025 and is projected to reach USD 31.08 billion by 2031, expanding at a CAGR of 4.40% during the forecast period. The market is experiencing steady growth, supported by the rising demand for advanced fastening solutions tailored to electric vehicles (EVs), lightweight vehicle architectures, and increasingly automated manufacturing environments.

As the automotive industry transitions toward modular platforms and scalable vehicle architectures, the need for standardized, high-performance fasteners is accelerating across multiple vehicle programs.

Automotive fasteners remain essential to vehicle assembly, ensuring structural integrity, safety, and durability across mechanical, electrical, and body systems. Major OEMs such as Toyota, Volkswagen, General Motors, and Hyundai emphasize fasteners that meet strict performance, vibration resistance, and load-bearing requirements. Demand spans a wide range of products, including bolts, screws, nuts, rivets, clips, and specialized fastening systems, used across chassis, interiors, body structures, and electrical assemblies.

The increasing adoption of modular vehicle platforms further strengthens demand for standardized fastener families that enable scalability and manufacturing efficiency. A notable example is Volkswagen’s MQB platform, which has supported the production of over 32 million vehicles, highlighting the scale benefits of platform-based architectures.

AUTOMOTIVE FASTENER MARKET TRENDS & GROWTH DRIVERS

The automotive fastener market is evolving from traditional hardware supply to engineered joint solutions. OEMs are placing greater emphasis on joint performance, durability, and lifecycle reliability, particularly for safety-critical and mixed-material applications.

Modern vehicle designs require fasteners that ensure:

- Consistent joint strength and clamping force

- Reliable tightening and assembly outcomes

- Long-term corrosion resistance

This shift is driving stricter technical specifications, early supplier involvement, and enhanced traceability requirements, supported by robust production approval and validation processes.

The rapid growth of electric vehicles is also reshaping fastening demand. Fastener applications are shifting away from traditional engine and exhaust systems toward battery packs, high-voltage components, and power electronics. With global EV sales surpassing 17 million units in 2024 and accounting for over 20% of total vehicle sales, demand for high-performance fastening in battery enclosures and structural components is increasing significantly.

Additionally, platform consolidation is concentrating production volumes into fewer architectures, enabling the reuse of validated fastener designs across models and manufacturing plants. Automakers like Volkswagen, Stellantis, and Toyota are leveraging this strategy to reduce complexity, improve efficiency, and enhance supplier collaboration—further increasing the importance of platform-approved fastening solutions.

AUTOMOTIVE FASTENERS MARKET CHALLENGES & INDUSTRY RESTRAINTS

Despite stable demand, the market faces significant pricing pressure due to high-volume procurement practices by OEMs. Automotive manufacturers consistently enforce year-on-year cost reduction targets, even as performance expectations become more demanding.

Standard fasteners such as bolts, nuts, screws, and clips are often treated as commoditized components, allowing OEMs to adopt dual sourcing strategies and limit supplier pricing flexibility. This dynamic continues to constrain supplier margins across the value chain.

For instance, Bosch reported an operating margin of 1.9% in 2025, reflecting ongoing cost pressures in the automotive supply ecosystem. Suppliers are responding by focusing on:

- Manufacturing scale efficiencies

- Automation and optimized production footprints

- Strict quality and cost compliance

Annual cost-reduction expectations typically range between 1% and 4% or higher, reinforcing the need for operational efficiency and differentiation through engineered fastening solutions.

SEGMENTATION ANALYSIS

By Product: Rising Demand for Non-Threaded Fasteners

The market is segmented into threaded and non-threaded fasteners, with the non-threaded segment expected to grow at a CAGR of 4.78% (2026–2031).

This growth is driven by the increasing use of mixed-material vehicle designs, where clips, rivets, and industrial adhesives are widely adopted. Adhesives, often combined with mechanical fasteners, enhance joint strength and durability across metals, plastics, and composites.

A strong example is Jaguar’s aluminum body architecture, where adhesive bonding length was increased by 50% (154 meters), alongside the use of 2,840 rivets in the Jaguar XJ.

Additionally, stringent EU CO₂ regulations (2019/631) are accelerating the adoption of lightweight materials, further boosting demand for non-threaded fastening technologies.

By Material: Steel Dominance with Growing Aluminum Adoption

Iron and steel account for over 45% of the market share in 2025, remaining the preferred materials for high-volume automotive structures. A typical passenger vehicle consists of approximately 65% steel and iron, ensuring continued reliance on steel-based fasteners.

However, aluminum is witnessing strong growth due to increasing lightweighting initiatives, especially in electric vehicles and light trucks. By 2030, battery electric light trucks are expected to contain around 644 pounds of aluminum, driving demand for corrosion-resistant and material-compatible fasteners.

By Vehicle Type: Passenger Cars Lead Market Demand

Passenger cars dominate the market, supported by their large global fleet and diverse model range. The extensive installed base, particularly in regions like Europe, ensures consistent demand for both OEM and replacement fasteners.

This large-scale deployment creates ongoing demand for standardized fastener kits and high-volume production components.

By Application: Engine Segment Remains Significant

The engine segment continues to hold a major market share, as internal combustion and hybrid vehicles still represent a significant portion of global vehicle production.

Fasteners play a critical role in engine assemblies, including mounts, brackets, housings, and auxiliary systems, sustaining demand even as electrification progresses.

Meanwhile, the interior segment is expected to witness strong growth due to increasing integration of electronics and safety systems, including driver monitoring, event data recorders, and intelligent assistance technologies. These advancements are significantly increasing fastening requirements across interior modules.

By Distribution Channel: Aftermarket Gains Momentum

While OEMs dominate the market, the aftermarket segment is projected to grow at the fastest rate. Rising vehicle age and frequent maintenance cycles are driving steady demand for replacement fasteners such as clips, screws, and underbody components.

Regulatory frameworks supporting right-to-repair and open access to spare parts are further strengthening aftermarket growth globally.

By Fastening Type: Non-Permanent Fasteners Dominate

Non-permanent fastening solutions hold the largest share, driven by the need for ease of maintenance, repair, and component replacement.

With the average vehicle age increasing, especially in mature markets, demand for removable and reusable fastening systems continues to rise, supporting long-term serviceability and cost efficiency.

AUTOMOTIVE FASTENER MARKET REGIONAL ANALYSIS

Asia-Pacific: Leading Global Manufacturing Hub

Asia-Pacific holds over 41% of the global market share in 2025, supported by its strong vehicle production base and well-established supplier ecosystem.

The region benefits from:

- High vehicle production volumes

- Localized supply chains

- Faster platform adoption cycles

These factors ensure consistent demand for fasteners across OEM manufacturing programs.

Europe: Strong Regulatory and Manufacturing Base

Europe remains a key market, driven by major automotive hubs such as Germany, France, and Russia. The region’s strong regulatory environment, including Euro 7 standards, is pushing OEMs toward higher quality and durability standards, increasing demand for advanced fastening solutions.

AUTOMOTIVE FASTENER MARKET COMPETITIVE LANDSCAPE & SHARE ANALYSIS

The automotive fasteners market is moderately consolidated, with the top 20 players accounting for nearly half of the global share. The competitive landscape includes a mix of global engineered fastener manufacturers and regional suppliers specializing in cold forming, stamping, and polymer components.

Competition is increasingly based on:

- Engineering capabilities and joint validation

- Production readiness and quality compliance

- Traceability and process consistency

With over 98,000 IATF 16949-certified sites globally, quality standards remain a key differentiator. Companies such as Illinois Tool Works, ARaymond, Nifco, and Acument continue to strengthen their positions through innovation, localization, and strategic acquisitions.

Recent Developments in the Automotive Fasteners Market

- Nifco launched WaOSaFe, a wheel nut indicator designed for quick visual inspection in commercial vehicles, enhancing safety and installation efficiency.

- ARaymond completed the acquisition of FACIL, strengthening its global fastening portfolio and improving integration across OEM programs.

- Agrati expanded its ecosystem presence through TOKBO’s membership in ANEF, enhancing visibility for digital fastening and monitoring solutions.

- Nifco introduced a self-sealing bumper retainer for Toyota, enabling watertight performance without additional components and simplifying assembly.

- Agrati highlighted its MARBEL modular EV battery concept, supporting easier assembly, disassembly, and improved recyclability using standard screwed fasteners.

Automotive Fasteners Market Analysis & Quick Summary

- Market Size & Growth: Valued at USD 24B (2025), projected to reach USD 31.08B by 2031, growing at a CAGR of 4.40%.

- Core Growth Drivers: Rising demand from EV adoption, lightweight vehicle design, and automated manufacturing, along with a shift toward modular vehicle platforms.

- EV Impact: Global EV sales exceeded 17M units in 2024 (>20% share), increasing demand for fasteners in battery packs, high-voltage systems, and power electronics.

- Platform Scaling: Architectures like Volkswagen’s MQB (32M+ vehicles produced) are boosting demand for standardized, reusable fastener solutions.

- Product Trends: Non-threaded fasteners growing faster (4.78% CAGR) due to mixed-material designs (clips, rivets, adhesives).

- Adhesives + mechanical fastening improve joint strength and durability.

- Material Insights: Steel/iron dominate (>45% share); ~65% of a car’s weight is steel/iron.

- Aluminum is rising, especially in EVs (up to 644 lbs per vehicle by 2030).

- Vehicle & Application: Passenger cars lead demand due to a large global fleet.

- Engine segment dominates, but interior applications are growing due to electronics & safety systems.

- Aftermarket Growth: Driven by aging vehicles and repairs, high inspection failure rates (e.g., 27% in the UK) support replacement demand.

- Fastening Type: Non-permanent fasteners dominate due to repairability and service needs (average vehicle age ~12.3 years in the EU).

- Regional Insights: APAC leads (41%+ share) with 54.9M vehicles produced (2024).

- Europe is strong, driven by regulations (e.g., Euro 7) and manufacturing hubs.

- Challenges: Intense price pressure from OEMs, annual cost reductions (1–4%+), and low margins (e.g., Bosch 1.9% in 2025).

- Competitive Landscape: Top 20 players hold ~50% market share; competition driven by engineering capabilities, validation support, and quality compliance (98K+ IATF-certified sites).

SNAPSHOT

The global automotive fastener market size is expected to grow at a CAGR of approximately 4.40% from 2025 to 2031.

The following factors are likely to contribute to the growth of global automotive fastener market during the forecast period:

- OEM Platform Consolidation Enables Early Fastener Design-In

- Material and Coating Advances Expand Fastener Performance Limits

- Digital Assembly Systems Improve Joint Consistency

- Safety and Recycling Regulations Elevate Specification Consistency

Base Year: 2025

Forecast Year: 2026-2031

The report examines the current state of the global automotive fastener market and its market dynamics through 2026−2031. It covers a detailed overview of several market growth enablers, restraints, and trends. The study covers both the demand and supply sides of the market. It also profiles and analyses leading companies and several other prominent companies operating in the market.

Key Company Profiles

- KAMAX

- Business Overview

- Product Offerings

- Key Developments

- Key Strategies

- Key Strengths

- Key Opportunities

- Würth Group

- Nifco

- Illinois Tool Works Inc.

- Araymond

- Gruppo Fontana

Other Prominent Company Profiles

- Stanley Black & Decker

- Business Overview

- Product Offerings

- NORMA Group SE

- Agrati

- SFS Group

- Aoyama Seisakusho

- LISI Group

- Shanghai Prime Machinery Co., Ltd. (PMC)

- Bulten

- RIBE Group’s

- Boellhoff

- MacLean-Fogg

- PIOLAX, INC.

- Sundram Fasteners Limited

- MEIDOH Co., Ltd.

- Sterling Tools Limited

- Westfield Fasteners Limited

- Changshu Standard Parts Factory Co., Ltd

- Koninklijke Nedschroef

- BOLTUN Corporation

- The Phillips Screw Company

- KOVA Fasteners Pvt Ltd

- TOPURA Co., Ltd.

- KPF

- Trifast Plc Fastenings

- Norm Fasteners

- Infasco

- Ciser

- CELO

- PT Garuda Metalindo

- APISA Fasteners

Segmentation by Product

- Threaded Fasteners

- Non-Threaded Fasteners

Segmentation by Material

- Iron

- Stainless Steel

- Plastic

- Aluminium

- Brass

- Bronze

- Nickel

Segmentation by Fastening Characteristics

- Non-Permanent

- Permanent

Segmentation by Application

- Engine

- Chassis

- Interior Trim

- Transmission

- Front/ Rear Axle

- Steering

- Wire Harnessing

- Others

Segmentation by Vehicle

- Passenger Cars

- Low Commercial Vehicles

- Heavy Commercial Vehicles

Segmentation by Distribution Channel

- Original Equipment Manufacturers

- Aftermarkets

Segmentation by Geography

- APAC

- China

- Japan

- India

- South Korea

- Thailand

- Indonesia

- Malaysia

- Taiwan

- Europe

- Germany

- Russia

- France

- Italy

- UK

- Spain

- Poland

- Netherlands

- North America

- U.S.

- Canada

- Latin America

- Brazil

- Mexico

- Argentina

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

AUTOMOTIVE FASTENER MARKET FAQs

How big is the global automotive fastener market?

Which region dominates the global automotive fastener market?

Who are the major players in the global automotive fastener market?

What are the key trends in the global automotive fastener market?

What is the growth rate of the global automotive fastener market?

For more details, please reach us at [email protected]

- Chapter 1- Scope & Coverage

- Market Definition

- Inclusion

- Exclusions

- Market Estimation Caveats

- Market Derivation

- Market Segmentation by Product

- Market Segmentation by Material

- Market Segmentation by Fastening Characteristic

- Market Segmentation by Application

- Market Segmentation by Vehicle

- Market Segmentation by Distribution Channel

- Chapter 2- Premium Insights

- Chapter 3- Market Dynamics

- Introduction

- Value Chain Analysis

- Automotive Fastener Market by Electric Vehicle Type

- Comparison of Innovative Fastening and Fixing Technologies

- Technology Development Roadmap and Innovation Opportunities

- Propulsion Type Shapes Fastener Specifications

- Next Gen Materials and Coatings for Fasteners

- Market Opportunities & Trends

- Shifts from Commodity Fasteners to Engineered Joints

- Electrification is Re-allocating Fastening Value in Vehicles

- Mixed-Material Vehicle Design is Reshaping Joining Strategies

- Assembly Automation is Tightening Fastener Installation Windows

- Market Growth Enablers

- OEM Platform Consolidation Enables Early Fastener Design In

- Material and Coating Advances Expand Fastener Performance Limits

- Digital Assembly Systems Improve Joint Consistency

- Safety and Recycling Regulations Elevate Specification Consistency

- Market Restraints

- OEM Cost Pressure Limits Fastener Value Capture

- Raw Material Volatility Disrupts Cost Stability

- Lengthy Qualification Cycles Slow Innovation Adoption

- Market Landscape

- Five Forces Analysis

- Chapter 4- Market Segmentation

- Product (Market Size & Forecast: 2022-2031)

- Threaded Fasteners

- Non-Threaded Fasteners

- Material (Market Size & Forecast: 2022-2031)

- Iron

- Stainless Steel

- Plastic

- Aluminium

- Brass

- Bronze

- Nickel

- Fastening Characteristics (Market Size & Forecast: 2022-2031)

- Non-Permanent

- Permanent

- Application (Market Size & Forecast: 2022-2031)

- Engine

- Chassis

- Interior Trim

- Transmission

- Front/ Rear Axle

- Steering

- Wire Harnessing

- Others

- Vehicle (Market Size & Forecast: 2022-2031)

- Passenger Cars

- Low Commercial Vehicles

- Heavy Commercial Vehicles

- Distribution Channel (Market Size & Forecast: 2022-2031)

- Original Equipment Manufacturers

- Aftermarkets

- Chapter 5- Geography Segmentation

- Geography Segmentation (Market Size & Forecast: 2022-2031)

- Geographic Overview – Market Maturity Index

- APAC

- China

- Japan

- India

- South Korea

- Thailand

- Indonesia

- Malaysia

- Taiwan

- Europe

- Germany

- Russia

- France

- Italy

- UK

- Spain

- Poland

- Netherlands

- North America

- US

- Canada

- Latin America

- Brazil

- Mexico

- Argentina

- MEA

- South Africa

- Saudi Arabia

- UEA

- Chapter 6- Competitive Landscape

- Competitive Landscape

- Competition Overview

- Key Developments

- Key Company Profiles

- Other Prominent Company Profiles

- Report Summary

- Key Takeaways

- Strategic Recommendations

Select a license type that suits your business needs

Single User Licence

- Report accessible by one user only

- Free 10% or 3 days of customization

- Free post-sale service assistance

- Continuous support through email

5 User Licence

- Report accessible by 5 users within the organization

- Free 15% or 4.5 days of customization

- Continuous support through email and telephone

- Free analyst hour

- Free Upgrade: If an updated report published within 180 days of purchase, you will get the revised report free of charge

Corporate Licence

- Free Datasheet worth $1500

- Report accessible by the entire organization

- Free 20% or 6 days of customization

- Free post-sale service assistance

- Continuous support through email and telephone

- Direct access to lead analysts

- Free analyst hour

- Free Upgrade: If an updated report published within 180 days of purchase, you will get the revised report free of charge

Datasheet Licence

- Report accessible by 1 user only

- Free 15% or 32 hours of customization

- Free post-sale service assistance

- Direct access to lead analysts

Frequently Asked Questions

How big is the global automotive fastener market?

Which region dominates the global automotive fastener market?

Who are the major players in the global automotive fastener market?

What are the key trends in the global automotive fastener market?

What is the growth rate of the global automotive fastener market?

Other RELATED Reports

Global Automotive Premium Audio Systems Market Research Report 2026- 2031

Published : March 2026