Global Battery Separator Market Research Report 2026-2031

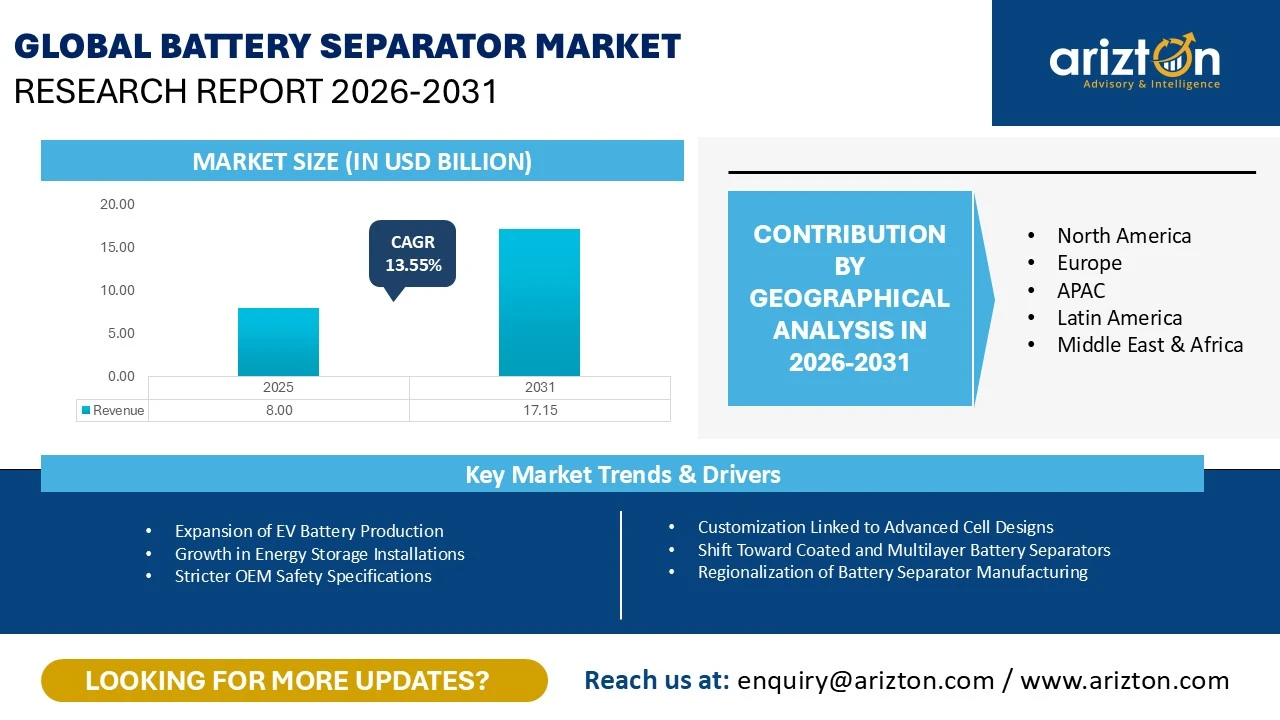

THE GLOBAL BATTERY SEPARATOR MARKET WAS VALUED AT USD 8.00 BILLION IN 2025 AND IS EXPECTED TO REACH USD 17.15 BILLION BY 2031, GROWING AT A CAGR OF 13.55%.

196 pages

30 company

7 segments

5 region

25 countries

Purchase Options

Global Battery Separator Market Research Report 2026-2031

THE GLOBAL BATTERY SEPARATOR MARKET WAS VALUED AT USD 8.00 BILLION IN 2025 AND IS EXPECTED TO REACH USD 17.15 BILLION BY 2031, GROWING AT A CAGR OF 13.55%.

The Battery Separator Market Size, Share, & Trends Analysis Report By

- Battery Chemistry: Lithium-ion batteries, Lead-acid batteries, Nickel-based batteries, Sodium-ion batteries, and Others

- Separator Material: Polyethylene (PE), Polypropylene (PP), Multilayer polyolefin (PP/PE/PP), Nonwoven materials, Ceramic-based materials, and Others

- Manufacturing Process: Wet process, Dry process, and Others

- Separator Thickness: ≤ 10 µm, 11–15 µm, 16–20 µm, and 20 µm

- Battery Form Factor: Cylindrical cells, Prismatic cells, and Pouch cells

- End-Use Application: Electric vehicles, Consumer electronics, Energy storage systems, and Industrial & other applications

- Geography: North America, Europe, APAC, Latin America, and Middle East & Africa

Industry Analysis Report, Regional Outlook, Growth Potential, Price Trends, Competitive Market Share & Forecast 2026–2031.

This report includes market data points, ranging from trend

analyses to market estimates & forecasts that you can customize

BATTERY SEPARATOR MARKET REPORT SCOPE

| REPORT ATTRIBUTE | DETAILS |

|---|---|

| MARKET SIZE (2031) | USD 17.15 Billion |

| MARKET SIZE (2025) | USD 8.00 Billion |

| CAGR (2025-2031) | 13.55% |

| HISTORIC YEAR | 2022-2024 |

| BASE YEAR | 2025 |

| FORECAST YEAR | 2026-2031 |

| SEGMENTS BY | Battery Chemistry, Separator Material, Manufacturing Process, Separator Thickness, Battery Form Factor, End-Use Application, and Geography |

| GEOGRAPHIC ANALYSIS | North America, Europe, APAC, Latin America, and Middle East & Africa |

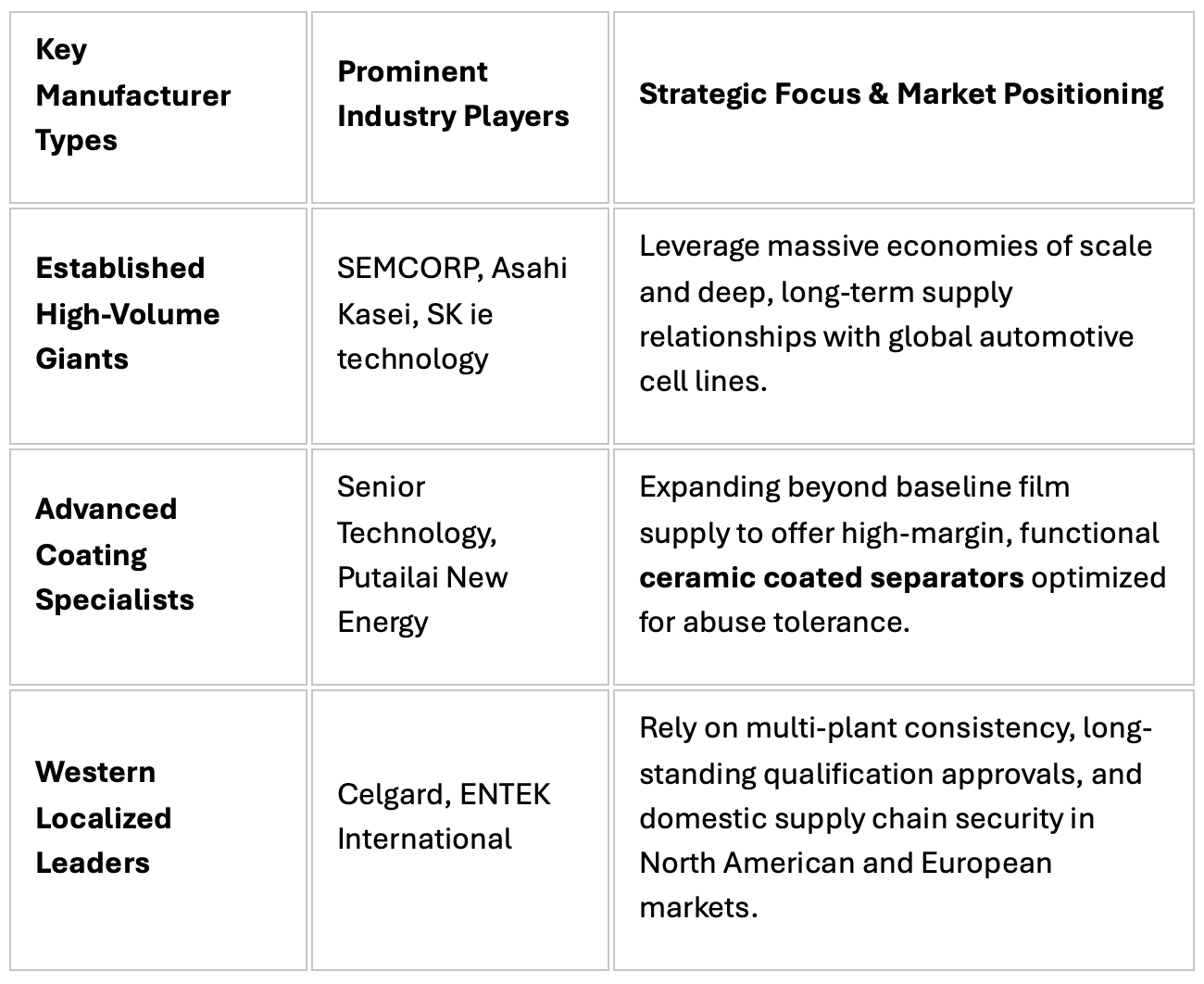

| KEY PLAYERS | SEMCORP, Asahi Kasei Corporation., SK Group, and W-SCOPE Korea |

BATTERY SEPARATOR MARKET ANALYSIS

The global battery separator market is witnessing strong growth, driven by the rapid expansion of electric vehicles (EVs), energy storage systems, and advanced battery technologies. The market was valued at USD 8.00 billion in 2025 and is expected to reach USD 17.15 billion by 2031, growing at a CAGR of 13.55% during the forecast period.

The battery separator industry is undergoing a significant transformation from a volume-focused film manufacturing segment to a performance-oriented materials market. Increasing emphasis on safety standards, product reliability, and long qualification cycles is reshaping industry dynamics. This shift is primarily fueled by rising demand for EV battery separators and stationary energy storage applications, both of which require high-performance separator materials with enhanced thermal stability, durability, and safety characteristics.

What is a Battery Separator?

A separator in lithium-ion battery systems is a microporous membrane that prevents direct contact between electrodes while allowing ion transport. These battery separator materials are essential for ensuring battery safety, cycle life, and operational efficiency.

In modern cell manufacturing, even minor variations in separator properties such as porosity, thickness, or electrolyte wettability can impact yield, safety, and warranty performance. As a result, lithium-ion battery separator procurement is highly qualification-driven, with manufacturers relying on pre-approved suppliers.

MARKET TRENDS & STRATEGIC ENABLERS

EV Expansion Driving Massive Volumes

The global surge in electric vehicle adoption acts as the primary engine for battery separator market growth. As global electric car sales surpassed 17 million units in 2024, the demand for high-performance EV battery separators skyrocketed. Because these components directly influence cell safety and energy delivery, global gigafactory expansions require a stable, high-quality separator supply chain to mitigate thermal risks and meet stringent automotive warranties.

Grid-Scale Energy Storage Infrastructure

Beyond automotive applications, the lithium-ion battery separator market is finding a secondary demand engine in grid-scale energy storage systems (ESS). As renewable energy integration accelerates, developers require long-duration, high-reliability storage. This macro trend is heavily reinforced by policy enablers; for instance, the IRS explicitly states that taxpayers utilizing energy storage technology placed in service after December 31, 2024, may claim the Clean Electricity Investment Credit, locking in long-term demand for high-calendar-life separator designs.

Material Evolution: The Shift to Coatings

The industry is shifting rapidly away from basic base films toward advanced, high-value battery separator market trends. Market participants are heavily prioritizing:

- Ceramic-coated separators

- Multilayer structures

- Functional coated membranes

These materials drastically improve thermal stability, enhance puncture resistance, and prevent localized internal short circuits vital traits for large-format, high-voltage battery designs.

Regional Supply Chain Localization

Geopolitical priorities and logistics risks are driving deep regionalization across the supply chain. Governments and automotive OEMs are heavily investing in domestic production ecosystems to secure regional supply resilience, boosting the footprint of localized manufacturers across North America and Europe.

INDUSTRY RESTRAINTS & CAPITAL REALITIES

Despite high market demand, expanding production remains highly capital-intensive and yield-driven. Operating high-performance film-stretching and coating lines demands microscopic control over thickness, pore morphology, cleanliness, and defect rates. Consequently, scaling up capacity is expensive, and production ramp timelines are highly volatile until stable yields are achieved. This capital intensity is highlighted by public-backed financing initiatives, such as the U.S. Department of Energy (DOE) loan support for domestic manufacturing plants.

Furthermore, commercial outcomes are tightly constrained by long qualification cycles, persistent cost-down expectations, and customer concentration. Separators must undergo exhaustive validation at the individual cell level, a process that must be repeated whenever a cell design changes. Because automotive and grid buyers demand long-term supply agreements and volume-based pricing, suppliers face high dependence on a limited pool of Tier-1 cell makers and their specific vehicle platform schedules.

Comprehensive Market Segmentation Insights

By Battery Chemistry

The lithium-ion segment dominates the market, commanding over 65% of the total battery separator market share. Li-ion chemistry remains the dominant architecture for electric vehicles, electronic devices, and utility-scale storage. However, its high energy density and flammable organic electrolytes place stringent performance demands on separators, which must maintain stable ion transport under high-voltage operations.

Three distinct end-user sub-segments drive this chemistry:

- EV Cell Manufacturers: Prioritize physical strength, low thermal shrinkage, and exceptional consistency.

- Energy Storage Producers: Prioritize long calendar life and high abuse tolerance.

- Consumer Electronics Makers: Target ultra-thin gauges, processing throughput, and extreme cost efficiency.

While lithium-ion leads, other chemistries like traditional lead-acid, nickel-based systems, and emerging sodium-ion variations continue to hold dedicated market segments.

By Separator Material

Polyethylene holds the largest market share among baseline materials. Polyethylene battery separators are widely specified across EV cells and stationary storage due to their predictable, repeatable behavior under thermal stress. It is frequently utilized as a standalone film or as the vital "shutdown layer" in advanced multilayer configurations.

Its market dominance is sustained by mature, high-speed film-stretching manufacturing processes that yield tight control over porosity and thickness, successfully balancing high manufacturing yields with automotive-grade safety metrics. Meanwhile, alternative materials like a polypropylene battery separator or hybrid configurations are frequently deployed where specific thermal or tensile properties are required.

By Manufacturing Process

- The Wet Process (Fastest Growing): This segment is expanding at a rapid CAGR of 13.92%. The wet route utilizes phase separation to create a highly interconnected, uniform pore network with controlled tortuosity. The resulting extraction and heat-setting phases provide superior caliper control and reduce roll-to-roll variation. This minimizes localized impedance hotspots, making wet-process films the premium choice for mainstream EV platforms, fast-charging cells, and premium consumer electronics.

- The Dry Process: Supported by solvent-free production routes and attractive, scalable film economics, the dry process remains highly prominent. Manufacturers like ENTEK form these separators via extrusion, controlled heat-setting, and rapid stretching. This results in slit-like pores yielding a consistent 35–45% porosity, appealing to cost-conscious buyers balancing manufacturability with steady performance targets.

By Separator Thickness

The 16–20 µm segment dominates the global marketplace. This specific thickness band offers optimal mechanical handling and repeatable quality control at high processing speeds.

Why the 16–20 µm Band Dominates:

Increased physical thickness enhances puncture and tear resistance, protecting the cell from electrode roughness, burrs, and microscopic particle contamination. It also provides excellent dimensional stability under high stack pressure and thermal excursions, minimizing the risk of wrinkling, edge damage, or micro-tearing during high-speed cell winding and stacking operations.

By Battery Form Factor

Pouch cells accounted for the largest share of the market, favored in applications demanding slim packaging profiles and flexible form-factor sizing (ranging from premium smartphones and drones up to large automotive packs).

Pouch-format separators demand exceptional flexibility and conformability to prevent creasing during large-area cell stacking. They also require high puncture resistance and ultra-low thermal shrinkage to avoid localized pressure gradients and heating as the pouch expands and contracts during prolonged cycling.

By End-Use Application

- Electric Vehicles: This represents the largest and most demanding application segment. EV separators are treated as highly engineered safety components rather than generic commodities, given that they must perform flawlessly for a decade or more under harsh climate and driving conditions.

- Energy Storage Systems (ESS): Showing significant growth due to clear regulatory and tax incentive frameworks globally that improve project economics.

- Consumer Electronics & Industrial: Steady, high-volume segments focused heavily on ultra-thin profiles, high throughput, and manufacturing cost efficiencies.

GEOGRAPHICAL ANALYSIS

APAC: The Manufacturing Powerhouse

The Asia-Pacific (APAC) region commands the largest portion of the global market, accounting for approximately 55% of the total share. APAC’s leadership is anchored by a dense, highly integrated EV and battery manufacturing ecosystem.

- China holds the majority share within the region, propelled by domestic leaders like SEMCORP and sustained policy support, including the extension of New Energy Vehicle (NEV) purchase tax incentives through 2027. China is also lifting safety benchmarks via ongoing revisions to its mandatory traction battery safety standard (GB 38031-2025), accelerating the transition toward high-performance ceramic and coated films.

- Japan and South Korea serve as key technology exporters, contributing advanced film-stretching and functional coating know-how to supply premium global cell platforms.

North America: The Fastest-Growing Hub

North America is projected as the fastest-growing region over the 2026–2031 forecast window. Growth is heavily accelerated by localization initiatives and federal policy, such as the Inflation Reduction Act (IRA) Advanced Manufacturing Production Credit. Major capital injections, including DOE financial backing for ENTEK’s lithium-ion separator facility in Terre Haute, Indiana, alongside massive regional cell capacity rollouts (such as Panasonic Energy’s mass production facility in Kansas), are establishing a robust domestic demand pull for qualified separator materials.

COMPETITIVE VENDOR LANDSCAPE

The global battery separator market is highly competitive yet deeply concentrated. Leadership is defined not by the sheer number of market participants, but by deep integration and historical qualification with Tier-1 battery cell producers. Because separators are vital to cell safety, battery manufacturers are highly reluctant to switch suppliers once a cell chemistry is validated and commercialized.

Strategic M&A and Reshoring Movements

The industry is experiencing notable consolidation and ownership realignments to fund large-scale localized expansions:

- Daramic Acquisition: Kingswood Capital Management acquired Daramic (a global lead-acid battery separator manufacturer) from Asahi Kasei, establishing it as a focused, independent player in automotive and industrial lead-acid markets.

- ENTEK Capital Backing: I Squared Capital acquired a majority stake in ENTEK to directly finance and scale domestic U.S. separator output, strengthening North American supply chain reshoring efforts.

Industry Innovation & Corporate Restructuring

- ZIMT (Zhongxing Innovative Materials): Awarded the 2025 Gaogong Lithium Battery “Product of the Year” for its advanced functional coated separators, validating the market's strong customer pull toward highly differentiated, safety-enhanced coatings.

- Sumitomo Chemical: Announced a major structural reorganization of its Pervio heat-resistant separator business. The company is ceasing production at its Ohe Works facility in Japan and consolidating manufacturing at its SSLM subsidiary in South Korea to maximize production scalability and cost competitiveness, while retaining core next-generation R&D functions within Japan.

SNAPSHOT

The global battery separator market size is expected to grow at a CAGR of approximately 13.55% from 2025 to 2031.

The following factors are likely to contribute to the growth of global battery separator market during the forecast period:

- Expansion of EV Battery Production

- Growth in Energy Storage Installations

- Stricter OEM Safety Specifications

- Gigafactory Led Capacity Expansion

Base Year: 2025

Forecast Year: 2026-2031

The report examines the current state of the global battery separator market and its market dynamics through 2026−2031. It covers a detailed overview of several market growth enablers, restraints, and trends. The study covers both the demand and supply sides of the market. It also profiles and analyses leading companies and several other prominent companies operating in the market.

Key Company Profiles

- SEMCORP

- Business Overview

- Product Offerings

- Key Developments

- Key Strategies

- Key Strengths

- Key Opportunities

- Asahi Kasei Corporation.

- SK Group

- W-SCOPE Korea

Other Prominent Company Profiles

- Shenzhen Senior Technology Material Co., Ltd.

- Business Overview

- Product Offerings

- Toray Industries, Inc.

- Sumitomo Chemical

- Celgard LLC

- ENTEK

- Sinoma Science & Technology Co., Ltd.

- ZIMT

- Cangzhou Mingzhu Plastic Co., Ltd.

- Shanghai Putailai New Energy Technology Co., Ltd. (PTL)

- Hebei Gellec New Energy Technology Co., Ltd.

- UBE Corporation

- Teijin Limited

- Freudenberg Performance Materials

- Huiqiang New Energy

- Microporous

- Daramic

- Hollingsworth & Vose

- Ahlstrom

- Maxell, Ltd.

- Mitsubishi Paper Mills Limited

- Jiangsu Horizon New Energy Technology Co., Ltd.

- Beijing SOJO Electric Co., Ltd.

- Delfortgroup AG

- SWM International

- Yingkou Zhongjie Shida Separator Co., Ltd.

- Nippon Paper PAPYLIA Co., Ltd.

- Segmentation by Battery Chemistry

- Lithium-ion batteries

- Lead-acid batteries

- Nickel-based batteries

- Sodium-ion batteries

- Others

- Segmentation by Separator Material

- Polyethylene (PE)

- Polypropylene (PP)

- Multilayer polyolefin (PP/PE/PP)

- Nonwoven materials

- Ceramic-based materials

- Others

Segmentation by Manufacturing Process

- Wet process

- Dry process

- Others

Segmentation by Separator Thickness

- ≤ 10 µm

- 11–15 µm

- 16–20 µm

- 20 µm

Segmentation by Battery Form Factor

- Cylindrical cells

- Prismatic cells

- Pouch cells

Segmentation by End-Use Application

- Electric vehicles

- Consumer electronics

- Energy storage systems

- Industrial & other applications

Segmentation by Geography

- APAC

- China

- South Korea

- Japan

- India

- Thailand

- Indonesia

- Vietnam

- Malaysia

- Australia

- North America

- U.S.

- Canada

- Europe

- Poland

- Germany

- Hungary

- France

- UK

- Italy

- Spain

- Latin America

- Brazil

- Mexico

- Argentina

- Middle East & Africa

- Saudi Arabia

- UAE

- South Africa

- Morocco

BATTERY SEPARATOR MARKET FAQs

How big is the global battery separator market?

What is the growth rate of the global battery separator market?

Which region dominates the global battery separator market?

Who are the major players in the global battery separator market?

What are the key trends in the global battery separator market?

For more details, please reach us at [email protected]

- Chapter 1- Scope & Coverage

- Market Definition

- Inclusion

- Exclusions

- Market Estimation Caveats

- Market Derivation

- Market Segmentation by Battery Chemistry

- Market Segmentation by Separator Material

- Market Segmentation by Manufacturing Process

- Market Segmentation by Separator Thickness

- Market Segmentation by Battery Form Factor

- Market Segmentation by End-Use Application

- Chapter 2- Premium Insights

- Chapter 3- Market Dynamics

- Introduction

- Value Chain Analysis

- Product Architecture & Selection Logic

- Patent Activity Shaping Coating and Process Differentiation in Separators

- Government Regulations Shaping Battery Separators

- Market Opportunities & Trends

- Shift Toward Coated and Multilayer Battery Separators

- Customization Linked to Advanced Cell Designs

- Regionalization of Battery Separator Manufacturing

- Increasing Process Expertise and IP Concentration

- Market Growth Enablers

- Expansion of EV Battery Production

- Growth in Energy Storage Installations

- Stricter OEM Safety Specifications

- Gigafactory Led Capacity Expansion

- Market Restraints

- High Capital Intensity of Battery Separator Manufacturing

- Lengthy Qualification and Validation Cycles

- Persistent Pricing Pressure Across the Battery Value Chain

- Dependence on a Concentrated Customer Base

- Market Landscape

- Five Forces Analysis

- Chapter 4- Market Segmentation

- Battery Chemistry (Market Size & Forecast: 2022-2031)

- Lithium-ion batteries

- Lead-acid batteries

- Nickel-based batteries

- Sodium-ion batteries

- Others

- Separator Material (Market Size & Forecast: 2022-2031)

- Polyethylene (PE)

- Polypropylene (PP)

- Multilayer polyolefin (PP/PE/PP)

- Nonwoven materials

- Ceramic-based materials

- Others

- Manufacturing Process (Market Size & Forecast: 2022-2031)

- Wet process

- Dry process

- Others

- Separator Thickness (Market Size & Forecast: 2022-2031)

- ≤ 10 µm

- 11–15 µm

- 16–20 µm

- 20 µm

- Battery Form Factor (Market Size & Forecast: 2022-2031)

- Cylindrical cells

- Prismatic cells

- Pouch cells

- End-Use Application (Market Size & Forecast: 2022-2031)

- Electric vehicles

- Consumer electronics

- Energy storage systems

- Industrial & other applications

- Chapter 5- Geography Segmentation

- Geography Segmentation (Market Size & Forecast: 2022-2031)

- Geographic Overview – Market Maturity Index

- APAC

- China

- South Korea

- Japan

- India

- Thailand

- Indonesia

- Vietnam

- Malaysia

- Australia

- North America

- US

- Canada

- Europe

- Poland

- Germany

- Hungary

- France

- UK

- Italy

- Spain

- Latin America

- Brazil

- Mexico

- Argentina

- MEA

- Saudi Arabia

- UAE

- South Africa

- Morocco

- Chapter 6- Competitive Landscape

- Competitive Landscape

- Competition Overview

- Key Developments

- Key Company Profiles

- Other Prominent Company Profiles

- Report Summary

- Key Takeaways

- Strategic Recommendations

Select a license type that suits your business needs

Single User Licence

- Report accessible by one user only

- Free 10% or 3 days of customization

- Free post-sale service assistance

- Continuous support through email

5 User Licence

- Report accessible by 5 users within the organization

- Free 15% or 4.5 days of customization

- Continuous support through email and telephone

- Free analyst hour

- Free Upgrade: If an updated report published within 180 days of purchase, you will get the revised report free of charge

Corporate Licence

- Free Datasheet worth $1500

- Report accessible by the entire organization

- Free 20% or 6 days of customization

- Free post-sale service assistance

- Continuous support through email and telephone

- Direct access to lead analysts

- Free analyst hour

- Free Upgrade: If an updated report published within 180 days of purchase, you will get the revised report free of charge

Datasheet Licence

- Report accessible by 1 user only

- Free 15% or 32 hours of customization

- Free post-sale service assistance

- Direct access to lead analysts

Frequently Asked Questions

How big is the global battery separator market?

What is the growth rate of the global battery separator market?

Which region dominates the global battery separator market?

Who are the major players in the global battery separator market?

What are the key trends in the global battery separator market?

Other RELATED Reports

Global Electric Vehicle Battery Technology Market Research Report 2026-2031

Published : January 2026