Building Construction Glass Market- Global Outlook & Forecast 2026-2031

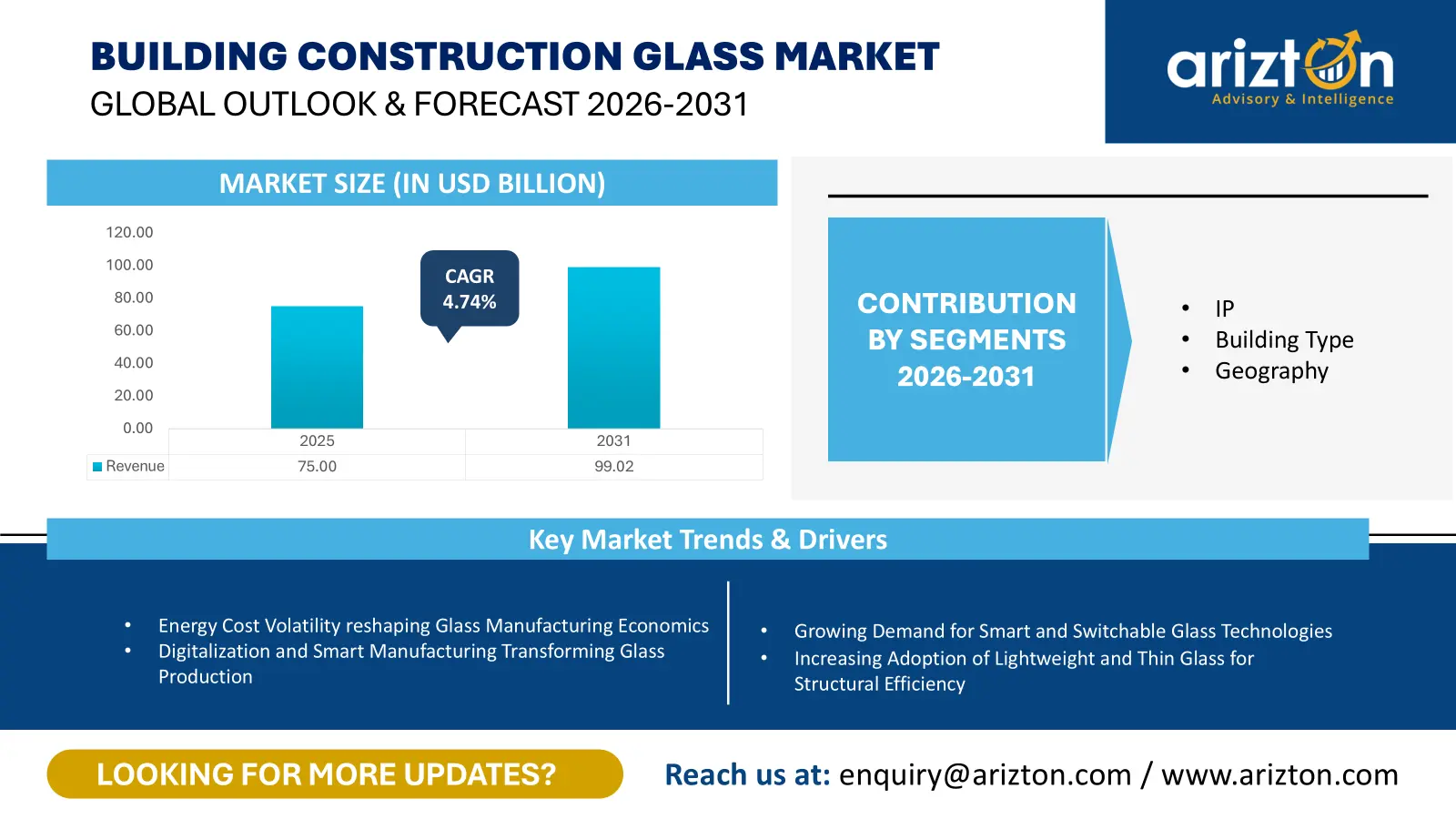

THE GLOBAL BUILDING CONSTRUCTION GLASS MARKET WAS VALUED AT USD 75 BILLION IN 2025 AND IS EXPECTED TO REACH USD 99.02 BILLION BY 2031, GROWING AT A CAGR OF 4.74%.

226 pages

5 region

19 countries

32 company

3 segments

Purchase Options

Building Construction Glass Market- Global Outlook & Forecast 2026-2031

THE GLOBAL BUILDING CONSTRUCTION GLASS MARKET WAS VALUED AT USD 75 BILLION IN 2025 AND IS EXPECTED TO REACH USD 99.02 BILLION BY 2031, GROWING AT A CAGR OF 4.74%.

The Global Building Construction Glass Market Size, Share & Trends Analysis Report By

- IP Type: Flat Glass and Glass Fiber

- Building Type: Residential and Non-Residential

- Geography: North America, Europe, APAC, Latin America, & Middle East & Africa

Industry Analysis Report, Regional Outlook, Growth Potential, Price Trends, Competitive Market Share & Forecast 2026–2031.

This report includes market data points, ranging from trend

analyses to market estimates & forecasts that you can customize

BUILDING CONSTRUCTION GLASS MARKET REPORT SCOPE

| REPORT ATTRIBUTE | DETAILS |

|---|---|

| MARKET SIZE (2031) | USD 99.02 Billion |

| MARKET SIZE (2025) | USD 75 Billion |

| CAGR (2025-2031) | 4.74% |

| MARKET SIZE (SHIPMENT VOLUME) | 102.90 Million Tons (2031) |

| HISTORIC YEAR | 2022-2024 |

| BASE YEAR | 2025 |

| FORECAST YEAR | 2026-2031 |

| SEGMENTS BY | IP Type, Building Type, and Geography |

| GEOGRAPHIC ANALYSIS | North America, Europe, APAC, Latin America, & Middle East & Africa |

| KEY PLAYERS | SAINT-GOBAIN, AGC Inc., NSG Group, GUARDIAN GLASS, Şişecam Group, Vitro Architectural Glass, Cardinal Glass Industries, Fuyao Glass Industry Group, Schott AG, and Central Glass Co., Ltd. |

BUILDING CONSTRUCTION GLASS MARKET ANALYSIS

The global building construction glass market is undergoing a profound structural transformation. Once considered a basic, passive material, glass has evolved into a high-performance, multifunctional component critical to modern architectural design. Driven by advancements in material technology, stringent sustainability requirements, and changing regulatory frameworks, the market is shifting toward intelligent building envelopes that enhance energy efficiency, aesthetics, and structural performance.

Market Size and Growth Projections

The global building construction glass market size was valued at USD 75 billion in 2025 and is projected to reach USD 99.02 billion by 2031. This represents a steady compound annual growth rate (CAGR) of 4.74% over the forecast period.

In terms of shipment volume, the overall construction glass market is expected to reach approximately 102.90 million tons by 2031. This massive volume expansion is fueled by continuous innovations in glass manufacturing and processing, which have vastly improved the material's strength, thermal insulation, solar control, and structural safety across residential, commercial, and infrastructure projects.

KEY TAKEAWAYS OF THIS INDUSTRY

Here are the key takeaways from the market analysis structured for clear, at-a-glance scanning:

- Dominant Product Type (IP Type): The flat glass segment anchors the global industry, commanding the largest market share at approximately 79% in 2025 due to its widespread architectural applications in windows, facades, and curtain walls.

- Primary Building Type Sector: The residential segment continues to dominate overall consumption volumes while simultaneously serving as the fastest-growing sector, projecting a market-leading CAGR of 5.19% over the forecast period.

- Leading Geographic Region: The Asia-Pacific (APAC) region retains absolute dominance over the global architectural glass market, securing the largest territorial share at roughly 40% propelled heavily by massive urban construction projects across China and India.

BUILDING CONSTRUCTION GLASS MARKET TRENDS & GROWTH DRIVERS

The building and construction glass market is undergoing a profound structural shift. Driven by stricter regulatory codes, escalating utility costs, and urgent sustainability mandates, glass has evolved from a passive architectural element into a vital, functional asset for thermal insulation and climate control.

The Energy-Efficiency Drive

With physical buildings accounting for 30% to 40% of global energy consumption, energy-efficient glazing systems represent a vital intervention point for developers aiming to slash carbon footprints. Modern architectural designs rely heavily on insulated glass units (IGUs) and low-emissivity (Low-E) configurations to dramatically lower heat transfer while maximizing natural daylight.

The Structural Shift in Material Profiles

The transition away from basic glass toward specialized, high-performance variants highlights how the industry is maturing:

- Float / Annealed Glass: This traditional baseline material still commands major raw volume particularly across cost-sensitive regions in India and Southeast Asia. However, intense market competition has squeezed profit margins significantly.

- Tempered (Toughened) Glass: Engineered to offer 4x to 5x the strength of annealed glass, tempered glass is now a baseline safety mandate for high-rise buildings, structural facades, and perimeter railings across major metropolitan cities.

- Laminated Glass: Prized for its ability to hold together upon structural impact, laminated glass is the go-to solution for minimize-failure zones like skylights and curtain walls. It is experiencing rapid adoption in commercial airports, premium malls, and luxury residential projects due to its superior safety and acoustic insulation.

- Coated Glass (Low-E & Solar Control): As one of the market's fastest-growing sub-segments, these advanced coatings are highly favored by commercial developments, such as IT parks in India and office towers in the Middle East, to cut cooling loads by 20% to 30%.

- Tinted and Reflective Glass: These products remain a popular, cost-effective standard for balancing exterior aesthetics with localized glare reduction in high-sunlight regions.

Exponential Demand for Smart & Switchable Glass

The global momentum behind the smart glass market is accelerating as developers transition from traditional glazing to intelligent, responsive materials. Unlike static glass, switchable technologies such as electrochromic and Suspended Particle Device (SPD) systems allow for real-time adjustments to light transmission and solar heat gain.

Core Market Catalysts for Smart Tech:

- Active Climate Control: By dynamically adapting to external sunlight, smart glass directly limits a building's reliance on artificial lighting and energy-heavy HVAC systems, creating healthier indoor environments.

- ESG Alignment: Corporate occupiers, institutional investors, and regulatory bodies are aggressively pushing for building materials that meet Environmental, Social, and Governance (ESG) criteria. Deploying smart glazing is a proven path to securing premium green building certifications and unlocking long-term operational savings.

- Sector Expansion: Beyond traditional office high-rises, smart glass adoption is scaling quickly across healthcare facilities, international airports, and premium residential projects where tailored user comfort is crucial.

KEY MARKET SEGMENT INSIGHTS

The global building construction glass market is characterized by distinct structural demands across different product categories and end-use sectors. Below is a detailed breakdown of the market based on Product Type (IP Type) and Building Type.

Insight by Product Type

The global building construction glass market is divided into two primary product categories: Flat Glass and Glass Fiber.

- Market Dominance: The flat glass segment led the market with a commanding 79% share in 2025.

- Key Drivers: This massive footprint is fueled by the global push for modern architectural designs, urban infrastructure expansion, and high-performance, energy-efficient building envelopes across both developed and emerging economies.

- Functional Distinction: Unlike glass fiber, which is confined to hidden insulation and structural reinforcement, flat glass serves as a visible, dual-purpose material. It optimizes natural lighting, improves thermal insulation, and enhances aesthetic appeal.

Core Applications of Flat Glass

- External Envelopes: Windows, structural facades, curtain walls, and skylights.

- Internal Architecture: Doors, partitions, and custom interior décor applications.

Insight by Building Type

When analyzed by end-use sectors, the market breaks down into Residential and Non-Residential (Commercial & Infrastructure) applications.

- Market Dominance: The residential segment currently dominates the market in terms of sheer consumption volume.

- Growth Velocity: It is projected to be the fastest-growing sector, expanding at a CAGR of 5.19% during the forecast period.

- Key Drivers: This rapid expansion is underpinned by rising global homeownership rates, an expanding middle-class population, and aggressive government-backed affordable housing initiatives.

- Geographic Catalysts: Rapidly urbanizing nations, specifically China, India, Indonesia, and Vietnam, are leading the world in residential construction volumes, significantly boosting the consumption of architectural glass products.

Core Applications in Residential Construction

- Functional Elements: Windows, exterior doors, and balcony enclosures.

- Aesthetic Elements: Skylights, interior partitions, and structural glass facades for modern villas and smart apartment complexes.

GEOGRAPHICAL ANALYSIS

Asia-Pacific (APAC)

APAC dominates the global market with a commanding 40% share. This leadership position is anchored by massive economies like China and India, alongside rapidly expanding markets in Indonesia and Vietnam. The region benefits from faster construction cycles and unprecedented investments in smart cities, high-rise commercial developments, transport infrastructure, and affordable housing initiatives.

Note on Historical Context: Looking back at the trajectory of the building construction glass market in India in 2022, the region was characterized by high-volume float glass consumption. By 2026, it will mature rapidly, with commercial IT parks and metro infrastructure aggressively adopting advanced solar-control and tempered glass solutions.

Europe

The European market is undergoing a regulatory and structural transformation. Driven by stringent net-zero mandates and aggressive government retrofit programs, the European sectors are focused heavily on upgrading existing building stock with high-performance insulated glass units (IGUs) and low-carbon, recyclable glass products.

North America

North America operates a highly advanced, specification-driven architectural ecosystem. In the United States and Canada, stringent local building codes and green building frameworks treat advanced glazing not as a luxury add-on, but as a core compliance requirement. The market heavily favors high-performance, coated, and multi-functional architectural glass optimized for long-term energy mitigation.

VENDOR LANDSCAPE

The global building construction glass market is undergoing a significant structural transformation, driven by the increasing demand for energy-efficient buildings, rapid urbanization, growth in high-rise construction, and stricter environmental regulations. The market encompasses a wide range of products, including float glass, tempered glass, laminated glass, Insulated Glass Units (IGUs), Low-E glass, solar control glass, and advanced façade glazing systems.

Competition in the building construction glass sector is shaped by the convergence of three major forces:

- Regulatory Compliance: Rising demand for energy-efficient and high-performance glazing solutions, aligned with global building energy codes and green certification standards.

- Eco-Innovation: Increasing adoption of sustainable and low-carbon glass manufacturing technologies, along with recyclable and energy-saving glass products.

- Collaborative Supply: Expansion of integrated façade solutions and project-based supply models, supported by strong relationships with architects, contractors, and developers.

Large global manufacturers and vertically integrated glass producers dominate the competitive landscape through control over float glass production, advanced coating technologies, extensive distribution networks, and long-term project partnerships. Meanwhile, regional fabricators and specialized processors are gaining traction by offering customized glazing solutions, design flexibility, and localized service capabilities tailored to specific building requirements and climatic conditions.

STRATEGIC IMPLICATIONS AND FUTURE OUTLOOK

Shift toward performance-driven building envelopes

The building construction glass market is increasingly evolving from a basic material supply industry into a performance-driven building envelope segment. Developers and architects are prioritizing glass not just for transparency but for its role in thermal insulation, energy efficiency, acoustic performance, and occupant comfort.

Regionalization and climate-specific product strategies

Future competitive advantage in the global building construction glass market will be shaped by the ability to address climate-specific performance requirements across different geographies. Products increasingly need to be optimized for:

- Cold climates: Enhanced thermal insulation through double/triple glazing and Low-E coatings

- Hot and tropical regions: Solar control glass with high heat rejection and UV protection

- Coastal and high-risk zones: Laminated and impact-resistant glass for safety and durability

This regionalization trend is encouraging manufacturers and distributors to diversify production and processing capabilities, invest in localized fabrication facilities, and develop customized product solutions in alignment with regional building codes and environmental conditions.

SNAPSHOT

The global building construction glass market size is expected to grow at a CAGR of approximately 4.74% from 2025 to 2031.

The following factors are likely to contribute to the growth of the building construction glass market during the forecast period:

- Increasing Residential Housing Completions and Urban Infrastructure Projects driving Higher Glass Installation Volumes

- Rising Retrofit and Renovation Activities driving Replacement Demand for Advanced Glass

- Growing Demand for Smart and Switchable Glass Technologies

- Increasing Adoption of Lightweight and Thin Glass for Structural Efficiency

Base Year: 2025

Forecast Year: 2026-2031

The report examines the current state of the global building construction glass market and its market dynamics through 2026−2031. It covers a detailed overview of several market growth enablers, restraints, and trends. The study covers both the demand and supply sides of the market. It also profiles and analyses leading companies and several other prominent companies operating in the building & construction glass market.

Key Company Profiles

- SAINT-GOBAIN

- Business Overview

- Product Offerings

- Key Developments

- Key Strategies

- Key Strengths

- Key Opportunities

- AGC Inc.

- NSG Group

- GUARDIAN GLASS

- Şişecam Group

- Vitro Architectural Glass

- Cardinal Glass Industries

- Fuyao Glass Industry Group

- Schott AG

- Central Glass Co., Ltd.

Other Prominent Company Profiles

- Asahi India Glass Ltd.

- Business Overview

- Product Offerings

- China Glass Holdings Ltd

- Xinyi Glass Holdings Ltd.

- Jinjing Group

- Taiwan Glass Industry Corp.

- CSG Holding Co., Ltd.

- Qingdao Creation Classic Glass

- Qingdao Migo Glass Co. Ltd.

- Arcon Flachglas-Veredlung

- Romag Ltd.

- Oldcastle BuildingEnvelope

- Bendheim Glass

- Press Glass Holding SA

- Viridian Glass

- Gulf Glass Industries

- Sejal Glass Ltd.

- Fuso Glass India Pvt Ltd

- Euroglass GmbH

- SEDAK GMBH

- TVITEC System Glass

- Jeber Kowitz LP

- Gold Plus Glass Industry Ltd

Segmentation by IP Type

- Flat Glass

- Glass Fiber

Segmentation by Building Type

- Residential

- Non-Residential

Segmentation by Geography

- North America

- U.S.

- Canada

- Europe

- Western & Southern Europe

- Central & Eastern Europe

- Nordics

- APAC

- China

- India

- Japan

- South Korea

- Australia

- Indonesia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Argentina

- Chile

- Rest of Latin America

- Middle East & Africa

- Saudi Arabia

- Turkey

- UAE

- South Africa

- Rest of Middle East & Africa

BUILDING CONSTRUCTION GLASS MARKET FAQs

What is the growth rate of the global building construction glass market?

How big is the global building construction glass market?

What are the trends in the global building construction glass market?

What is the shipment volume of the global building construction glass market in 2031?

Which region dominates the global building construction glass market?

Who are the major players in the global building construction glass market?

For more details, please reach us at [email protected]

Chapter 1- Scope & Coverage

MARKET DEFINITION

- INCLUSION

- EXCLUSIONS

- MARKET ESTIMATION CAVEATS

MARKET DERIVATION

- MARKET SEGMENTATION BY SIZE

- MARKET SEGMENTATION BY END-USER

- MARKET SEGMENTATION BY RESIDENTIAL

- MARKET SEGMENTATION BY NON-RESIDENTIAL

Chapter 2- Premium Insights

Chapter 3- Market Dynamics

INTRODUCTION

- OVERVIEW

- GLOBAL WINDOW MARKET CLASSIFICATION FRAMEWORK

- BUYER DECISION FACTORS

- IMPACT OF REGULATIONS: GLOBAL WINDOWS MARKET

- STRATEGIC INDUSTRY OUTLOOK

- IMPACT OF TECHNOLOGY INTEGRATION ON PRODUCT VARIATION

REGULATORY AND TRADE ANALYSIS

- GLOBAL REGULATORY FRAMEWORK – IMPACT ANALYSIS

- REGIONAL REGULATORY ANALYSIS – IMPACT COMPARISON

- TRADE POLICIES AND TARIFFS

FUTURE OUTLOOK – GLOBAL WINDOWS MARKET

- FUTURE OUTLOOK – OVERVIEW

MARKET OPPORTUNITIES & TRENDS

- TRANSITION TOWARD INTELLIGENT, CONNECTED FENESTRATION SOLUTIONS

- SHIFT FROM PASSIVE ARCHITECTURAL ELEMENT TO ACTIVE, RESPONSIVE COMPONENT IN MODERN HOMES

- STRICT BUILDING AND ENVIRONMENTAL REGULATIONS DRIVING ENERGY-EFFICIENT WINDOW DEMAND

- INCREASING SHIFT TOWARD uPVC-BASED WINDOW SYSTEMS

MARKET GROWTH ENABLERS

- INCREASE IN GLOBAL CONSTRUCTION AND URBANIZATION ACTIVITIES

- INCREASING INCLINATION TO INTEGRATE ARCHITECTURAL AESTHETICS AND DESIGN ELEMENTS

- GROWTH IN RENOVATION AND HOME IMPROVEMENT PROGRAMS

- INCREASE IN PERSONALIZATION AND DIGITAL CUSTOMIZATION TRENDS

MARKET RESTRAINTS

- VOLATILITY IN RAW MATERIAL PRICES AND ENERGY PRICES

- MARKET FRAGMENTATION AND PRICING PRESSURES

- ENVIRONMENTAL CONCERNS AROUND PLASTICS

- HIGH INITIAL COSTS OF ADVANCED & SMART WINDOWS

MARKET LANDSCAPE

- MARKET OVERVIEW

- MARKET SIZE & FORECAST

- FIVE FORCES ANALYSIS

- PEST ANALYSIS

- VALUE CHAIN ANALYSIS

CHAPTER 5- MARKET SEGMENTATION

SIZE (MARKET SIZE & FORECAST: 2022-2031)

- SMALL

- MEDIUM

- LARGE

END-USER (MARKET SIZE & FORECAST: 2022-2031)

- RESIDENTIAL

- NON-RESIDENTIAL

RESIDENTIAL (MARKET SIZE & FORECAST: 2022-2031)

- MULTI-FAMILY HOMES

- SINGLE-FAMILY HOMES

NON-RESIDENTIAL (MARKET SIZE & FORECAST: 2022-2031)

- OFFICES

- HOSPITAL & HEALTHCARE

- EDUCATION

- HOTEL

- OTHERS

CHAPTER 6- GEOGRAPHY SEGMENTATION

GEOGRAPHY SEGMENTATION (MARKET SIZE & FORECAST: 2022-2031)

GEOGRAPHIC OVERVIEW – MARKET MATURITY INDEX

APAC

- CHINA

- INDIA

- JAPAN

- SOUTH KOREA

- AUSTRALIA

- INDONESIA

NORTH AMERICA

- US

- CANADA

EUROPE

- WESTERN & SOUTHERN EUROPE

- CENTRAL & EASTERN EUROPE

- NORDICS

LATIN AMERICA

- BRAZIL

- MEXICO

- ARGENTINA

- CHILE

MIDDLE EAST & AFRICA

- SAUDI ARABIA

- TURKEY

- UAE

- SOUTH AFRICA

CHAPTER 7- COMPETITIVE LANDSCAPE

COMPETITIVE LANDSCAPE

- COMPETITION OVERVIEW

- MARKET SHARE ANALYSIS

KEY COMPANY PROFILES

OTHER PROMINENT COMPANY PROFILES

REPORT SUMMARY

- KEY TAKEAWAYS

- STRATEGIC RECOMMENDATIONS

Select a license type that suits your business needs

Single User Licence

- Report accessible by one user only

- Free 10% or 3 days of customization

- Free post-sale service assistance

- Continuous support through email

5 User Licence

- Report accessible by 5 users within the organization

- Free 15% or 4.5 days of customization

- Continuous support through email and telephone

- Free analyst hour

- Free Upgrade: If an updated report published within 180 days of purchase, you will get the revised report free of charge

Corporate Licence

- Free Datasheet worth $1500

- Report accessible by the entire organization

- Free 20% or 6 days of customization

- Free post-sale service assistance

- Continuous support through email and telephone

- Direct access to lead analysts

- Free analyst hour

- Free Upgrade: If an updated report published within 180 days of purchase, you will get the revised report free of charge

Datasheet Licence

- Report accessible by 1 user only

- Free 15% or 32 hours of customization

- Free post-sale service assistance

- Direct access to lead analysts

Frequently Asked Questions

What is the growth rate of the global building construction glass market?

How big is the global building construction glass market?

What are the trends in the global building construction glass market?

What is the shipment volume of the global building construction glass market in 2031?

Which region dominates the global building construction glass market?

Who are the major players in the global building construction glass market?

Other RELATED Reports

Building and Construction Tapes Market - Global Outlook & Forecast 2024-2029

Published : April 2024