Global E-Learning Market Research Report 2026–2031

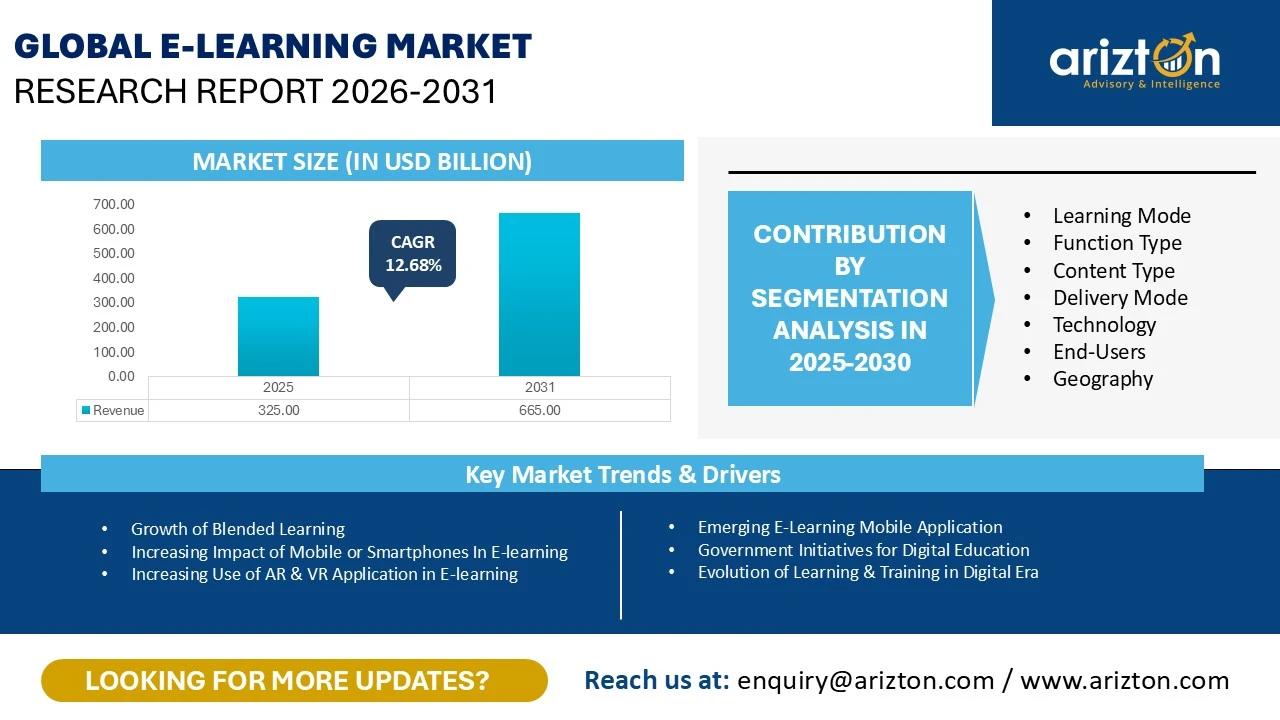

THE GLOBAL E-LEARNING MARKET WAS VALUED AT USD 325 BILLION IN 2025 AND IS EXPECTED TO REACH AROUND USD 665 BILLION BY 2031 GROWING AT A CAGR OF 12.68% DURING THE FORECAST PERIOD.

The E-Learning Market Size, Share, & Trends By Learning Mode, By Function Type, By Content Type, By Delivery Mode, By Technology, By End-Users, & By Geography. This Industry Analysis Covers The Market Size (in USD Billion) For The Above Segments.

Published Date : January 2026

Last Updated : January 2026

format: PDF

edition : Eighth Edition

543 pages

5 region

41 countries

117 company

7 segments

Purchase Options

Global E-Learning Market Research Report 2026–2031

THE GLOBAL E-LEARNING MARKET WAS VALUED AT USD 325 BILLION IN 2025 AND IS EXPECTED TO REACH AROUND USD 665 BILLION BY 2031 GROWING AT A CAGR OF 12.68% DURING THE FORECAST PERIOD.

The E-Learning Market Size, Share, & Trends Analysis Report By

- Learning Mode: Self-paced and Instructor Led

- Function Type: Training and Testing

- Content Type: Multimedia, Interactive, and Text-based

- Delivery Mode: Web-Based, Packaged Content, Blended, Mobile, and Other Modes

- Technology: Learning Management System (LMS), Mobile-based, Virtual Classroom, Simulation-Based, and Other Technologies

- End-users: Corporates, Academic Institutions, Individual Learners, Government Organizations, Healthcare Sector, Non-Profit Organizations, And Other Users

- Geography: North America, Europe, APAC, Latin America, and Middle East & Africa

Industry Analysis Report, Regional Outlook, Growth Potential, Price Trends, Competitive Market Share & Forecast 2025–2030.

This report includes market data points, ranging from trend

analyses to market estimates & forecasts that you can customize

GLOBAL E-LEARNING MARKET REPORT SCOPE

| REPORT ATTRIBUTE | DETAILS |

|---|---|

| MARKET SIZE (2031) | USD 665 Billion |

| MARKET SIZE (2025) | USD 325 Billion |

| CAGR (2025-2031) | 12.68% |

| HISTORIC YEAR | 2022-2024 |

| BASE YEAR | 2025 |

| FORECAST YEAR | 2026-2031 |

| SEGMENTS BY | Learning Mode, Function Type, Content Type, Delivery Mode, Technology, End-Users, and Geography |

| GEOGRAPHIC ANALYSIS | North America, Europe, APAC, Latin America, and Middle East & Africa |

| KEY PLAYERS | Adobe, Articulate, Aptara, Anthology, British Council, Infor, Citrix Systems Inc., Learning Pool, NIIT, Oracle, Pearson, SAP SE, Skillsoft, MPS, and Novac Technology Solutions |

E-LEARNING MARKET SIZE & SHARE

The global e-learning market size was valued at USD 325 billion in 2025 and is expected to reach around USD 665 billion by 2031, growing at a CAGR of 12.68% during the forecast period. This sector is significantly witnessing growth and transformation, driven by technological advances, evolving educational needs, and increasing internet accessibility.

The adoption of e-learning solutions and platforms is being positioned throughout the educational institution to assess the effectiveness of advanced learning methodologies, thereby contributing significantly to the growth of the e-learning market. The surging focus on childhood education and the growing public-private funding for K-12 education are further driving industry growth during the forecast period.

Furthermore, the market is also gaining momentum as there is a need for constant innovation for vendors to differentiate their products and drive service adoption among a more comprehensive section of end-users. AI and cognitive learning technologies have started to play a decisive role and are poised to be game changers in several learning avenues.

For instance, in 2025 Knowunity raised $29.2 million to scale its personalized AI tutor globally, targeting 1 billion students with adaptive learning technology that provides real-time feedback and customized educational content.

- Technological Advancements: Innovations across artificial intelligence (AI), virtual reality (VR), augmented reality (AR), and machine learning (ML) has transformed the e-learning market environment as these technologies enhance the learning experience by offering personalized, immersive, and interactive content.

- Mobile Learning: Mobile learning or m-learning, allows users to access educational content anywhere as per their busy schedules. The demand for m-learning is significant in regions with high mobile penetration, such as APAC and Africa.

- Gamification: Incorporating game elements into e-learning has also gained traction to increase learner engagement. Gamification uses point scoring, leaderboards, and badges among others to make learning more interactive which is effective in both academic and corporate settings.

- Microlearning: With the growing demand for on-demand learning solutions that cater to individual needs, the demand for microlearning is rising as it is generally effective for busy professionals who need to acquire specific skills quickly.

- Massive Open Online Courses (MOOCs): MOOCs have also democratized access to high-quality education from prestigious institutions as they offer free or low-cost courses to a global audience, making education more inclusive.

E-LEARNING MARKET TRENDS & DRIVERS

Emerging E-Learning Mobile Application

The extensive availability of internet-enabled devices and e-learning mobile applications has made learning more accessible. For instance, Coursera offers online learning via phone app which provides access to courses, specializations, and degree programs from top universities and institutions worldwide. Moreover, Educational institutions and EdTech startups are focusing on localized content and language support to reach broader audiences. For instance, Vidyakul an educational app offering live and recorded classes for Grades 9-12 in Bihar, Uttar Pradesh, and Gujarat across India which caters state board subjects and delivers content in regional languages at a low price point along with features like doubt-solving, mock tests, and notes to make education more accessible.

Government Initiatives for Digital Education

Governments across the world are surging the adoption of digital education through strategic policies, funding, and infrastructure development. For instance, In India PM e-VIDYA is a comprehensive initiative launched by the Ministry of Education to unify all efforts related to digital, online, and on-air education which enables the multi-mode access. Moreover, the EU’s Digital Education Action Plan (2021–2027) is also supporting the demand for e-learning as it promotes the digital transformation in education through improved infrastructure, teacher training, and digital literacy.

Increasing Use of AR & VR Application in E-learning

In recent years, Augmented Reality (AR) and Virtual Reality (VR) technologies have gained popularity in the education and training industry as effective tools for enhancing the learning experience. In 2025 Meta also launched the Meta for Education initiative, which provides educators with managed access to Meta Quest headsets and digital tools that enable the creation of virtual and mixed-reality classrooms across varied range of subjects. Hence, such initiative enhances student engagement, experiential learning, and collaboration by bringing immersive VR environments directly into educational settings.

Growth in Gamification

Gamification has also significantly impact the e-learning market by integrating components such as points, badges, leaderboards, levels, and virtual rewards into educational content which converts the traditional learning into interactive and competitive experience which engages learners to participate actively rather than just passively consuming information. For instance, in 2025, Coursera has introduced AI-powered challenge modules which dynamically adjusted quiz difficulty and rewards based on each user’s performance.

E-LEARNING MARKET SEGMENTATION INSIGHTS

INSIGHT BY LEARNING MODE

The global e-learning market by learning mode is segmented into self-paced and instructor led. In 2025, the self-paced segment accounted for the major market share around 63%, driven by its flexibility, accessibility, and ability to cater to diverse learning schedules. Learners can progress through content at their own speed, making it a preferred choice among working professionals and students seeking personalized education. The growing integration of AI-driven adaptive learning platforms and microlearning modules further enhances engagement in this segment.

Self-paced courses are a type of e-learning where learners complete course work at their speed rather than adhering to a fixed schedule or timeline. This flexible approach allows individuals to engage with educational materials and complete assignments conveniently and conveniently. Self-paced learning is characterized by its adaptability to various learning styles and schedules, making it an attractive option for many learners.

INSIGHT BY FUNCTION TYPE

Based on the function type, the training segment accounted for the largest revenue share of the global e-learning market, driven by its critical role in professional development, academic learning, and corporate skill enhancement. This segment focuses on interactive modules, virtual classrooms, and simulation-based content that enable learners to acquire new skills effectively. Leading e-learning providers such as Coursera, Skillsoft, and Udemy dominate this segment by offering diverse training programs for individuals and organizations worldwide. The training segment focuses on skill development, professional growth, and academic learning through interactive and engaging digital platforms. Organizations and educational institutions widely adopt this segment to upskill employees and students efficiently.

INSIGHT BY DELIVERY MODE

Based on the delivery mode, the mobile based segment shows significant growth, with the fastest-growing CAGR of 14.38% during the forecast period. The growth is fueled by the increasing penetration of smartphones, tablets, and mobile applications. The increasing preference for on-the-go learning has accelerated the adoption of bite-sized lessons, gamified modules, and short video tutorials optimized for mobile devices. This mode has gained significant popularity in professional and skills-based training, where flexibility and real-time access to information are essential. Platforms such as BYJU’S, Duolingo, and Khan Academy have played a pivotal role in advancing mobile e-learning, offering engaging, adaptive, and user-friendly interfaces that cater to learners of all ages and skill levels.

INSIGHTS BY CONTENT TYPE

The multimedia content dominates and holds the largest global e-learning market share in 2025. Multimedia content in e-learning encompasses educational materials that integrate diverse media formats such as text, audio, video, animations, and interactive visuals. This approach enhances engagement by stimulating multiple senses and creating an immersive learning environment. Multimedia content includes instructional videos, animated tutorials, podcasts, infographics, and interactive simulations that simplify complex concepts and maintain learner interest. By combining visual and auditory elements, it supports varied learning styles such as visual, auditory, and kinesthetic—making education more inclusive and impactful. Platforms such as Coursera, and edX effectively use multimedia content to promote deeper understanding, improve knowledge retention, and deliver high-quality, interactive learning experiences

INSIGHTS BY TECHNOLOGY TYPE

The learning management systems (LMS) segment accounted for the largest share of the global e-learning market in 2025. Learning Management Systems (LMS) are software platforms that centralize the creation, delivery, and tracking of educational courses and training programs. They enable instructors to manage content, assessments, and learner progress while providing learners easy access to materials and performance insights. Widely used in academic and corporate settings, platforms such as Moodle, Blackboard, Canvas, and TalentLMS enhance organization and efficiency in online education. The LMS market continues to grow, driven by digital adoption, corporate training needs, and the widespread shift toward remote learning.

INSIGHTS BY END USER

The global e-learning market by end user is categorized into corporates, academic institutions, individual learners, government organizations, healthcare sector, non-profit organizations, and other users. The corporate segment accounted for the largest global e-learning market share. The corporate segment in e-learning comprises organizations and businesses that utilizes digital learning platforms to train, upskill, and develop their workforce. It covers professional development, onboarding, compliance training, and continuous learning programs aimed at improving employee performance, efficiency, and knowledge of industry standards. Popular e-learning platforms for corporate training include LinkedIn Learning, Skillsoft, Udemy Business, and Coursera for Business, offering tailored courses, certifications, and interactive learning experiences for professional development.

E-LEARNING MARKET GEOGRAPHICAL ANALYSIS

In 2025, North America is the largest market, and US dominates the market across the region and accounts for a significant share of over 80%. The presence of major e-learning providers such as Coursera, Udemy, Skillsoft, LinkedIn Learning and others has created a strong market for e-learning services.

The North American Learning Institute (NALI) is also contributing to the growth of the region’s e-learning market by offering affordable, self-paced online certification courses in areas such as compliance, professional development, and continuing education. Its accessible, device-friendly platform allows learners to complete courses anytime, supporting the shift toward flexible and career-oriented digital learning. This growing adoption of platforms like NALI reflects the increasing preference for recognized, on-demand online education tailored to modern workforce needs.

The APAC region is accounted for the second largest share and is the fastest growing market of the global e-learning market. Key contributors to this growth include China, Japan, South Korea, and India, with China being the largest consumer and growing at a CAGR of 16.15% during the forecast period.

The development in mobile technology supports the incorporation of interactive elements like gamification, augmented reality, and virtual reality into learning for a more comprehensive experience. The proliferation of mobile learning across APAC is expected to surge the e-learning market, growth because through phones, learning activities are possible outside of school walls, freeing up students. For instance, in 2024, gamified e-learning platform Kahoot! is seeing rapid growth in Asia, with 8 million teachers and 1.6 billion users globally.

Europe is one of the developed and wealthiest economies, with countries like the UK, Germany, France, Italy, and Spain. In 2024, according to Eurostat, in 2024, EU GDP was 1.0% higher in real terms than in 2023. The expansion of the e-learning market in Europe is attributed to a combination of technological advances, widespread mobile device use, and an increasing demand for flexible education solutions.

Moreover, Government assistance, including funding also propels the implementation of e-learning in European universities and improves the educational framework of the area. For instance, in 2024, the OpenEU alliance, led by Universitat Oberta de Catalunya, launched as Europe’s first step toward a pan-European open university that promoted e-learning. It united 14 universities and 13 organizations to drive digital transformation in higher education.

E-LEARNING MARKET COMPETITIVE LANDSCAPE

The global e-learning market is moderately concentrated and highly competitive, featuring a dynamic mix of global and regional players. Prominent market participants such as Adobe, Aptara, Apollo Education Group, Articulate, Blackboard, British Council, Certpoint Systems, Citrix Systems, Learning Pool, NIIT, Oracle, Pearson, SAP SE, Skillsoft, and Tata Interactive Systems hold significant market shares owing to their extensive product portfolios, robust learning management systems, and well-established institutional partnerships.

Moreover, these organizations continue to lead through the deployment of AI-driven personalization tools, analytics-based learning insights, and integrated digital ecosystems that deliver measurable educational outcomes and enhance user satisfaction.

Despite its strong growth, the market continues to face challenges arising from the proliferation of low-cost, open-access, and unregulated content providers, particularly in developing regions. The availability of generic and often low-quality learning material exerts downward pricing pressure, compelling established companies to maintain stringent quality standards, safeguard intellectual property, and ensure content authenticity.

Recent Developments in the Global E-Learning Market

- In 2025, Knowunity raised around $29.2 million for its personalized AI tutor globally, targeting 1 billion students with adaptive learning technology that provides real-time feedback and customized educational content.

- In 2024, Coursera announced the launch of several novel efforts in a bid to improve access to high-quality education in India, including new AI features to comply with the requirements of Indian learners, with over 4,000 courses now available in Hindi.

- In 2023, the Government of Canada raised $17.6 million in investment in the second phase of the Digital Literacy Exchange Program (DLEP) . This significant investment supports organizations in teaching digital literacy skills.

SNAPSHOT

The global e-learning market size is expected to grow at a CAGR of approximately 15.17% from 2025 to 2031.

The following factors are likely to contribute to the growth of the global e-learning market during the forecast period:

- Emerging E-Learning Mobile Application

- Government Initiatives for Digital Education

- Evolution of Learning & Training in Digital Era

- Impact of 5G on Education Technology

Base Year: 2025

Forecast Year: 2026-2031

The report considers the present scenario of the global e-learning market and its market dynamics for 2026−2031. It covers a detailed overview of several market growth enablers, restraints, and trends. The study covers both the demand and supply sides of the market. It also profiles and analyzes leading companies and several other prominent companies operating in the market.

Key Company Profile

- Adobe Systems

- Business Overview

- Product Offerings

- Key Developments

- Key Strategies

- Key Strengths

- Key Opportunities

- Aptara

- Articulate Global LLC

- Anthology

- British Council

- Infor (Certpoint Systems)

- Citrix Systems Inc.

- Learning Pool

- NIIT Ltd

- Oracle

- Pearson

- SAP SE

- Skillsoft

- Novac

- MPS (Tata Interactive Systems (TIS) is accquired by MPS)

Other Prominent Company Profiles

- Cisco Systems Inc.

- Business Overview

- Product Offerings

- Instructure (Canvas LMS)

- GP Strategies

- Thomson Reuters

- Docebo

- McGraw Hill

- Desire2Learn (D2L)

- Cengage

- Macmillan Education

- Duolingo

- Cornerstone OnDemand

- Educomp Solutions

- Cogna Educação

- Telefónica Learning Services

- edX LLC

- Coursera Inc.

- Litmos

- Open Education

- Veduca

- LinkedIn (Microsoft)

- Simplilearn

- BYJUS

- upGrad

- FutureLearn

- Chegg Inc.

- Blinkist

- Age of Learning (ABCmouse)

- 360Learning

- Udemy

- Skillshare

- Udacity

- Pluralsight

- Alison

- Babbel

- Treehouse

- Unacademy

- IGNOU

- Legosta

- BenchPrep

- Coassemble

- Codecademy

- CrossKnowledge

- GoSkills

- iHASCO

- Khan Academy

- MasterClass

- OpenSesame

- Rosetta Stone

- Teachlr

- DataCamp

- BrainStation

- LearnUpon

- Thinkific

- Elucidat

- Moodle

- TalentLMS

- iSpring Solutions

- Ruzuku

- Kajabi

- WizIQ

- Xyleme

- Learning Paths (Cognitia)

- Socratic

- ITPro

- Go1

- Elliot

- Noodle

- eFront

- Pathwright

- ProProfs

- EduMe

- Mitratech (Trakstar)

- Gnowbe

- Vubiz

- Kaltura

- Mosaic

- Lumi Eductaiom

- Paradiso

- Zezus Laerning

- GeM

- Swift E-Learning

- Enyota

- Umami

- Acadecraft

- Kyteway

- Elearn Australia

- Aula

- Bright

- Learnatic

- Whitehat

- EWYSE

- SKILLBEST

- RWS

- MIND SPRING

- SANOMA

- PWC

- CAE

- Great Learning

- ENYOTA

- SIFY

- Pural Sight

- Stylus

Segmentation by Learning Mode

- Self-paced

- Instructor Led

Segmentation by Function Type

- Training

- Testing

Segmentation by Content Type

- Multimedia

- Interactive

- Text-based

Segmentation by Delivery Mode

- Web-based

- Packaged content

- Blended

- Mobile

- Other modes

Segmentation by Technology

- Learning management system (LMS)

- Mobile-based

- Virtual classroom

- Simulation-based

- Other Technologies

Segmentation by End-Users

- Corporates

- Academic institutions

- Individual learners

- Government organizations

- Healthcare sector

- Non-profit organizations

- Other users

Segmentation by Geography

- North America

- US

- Canada

- APAC

- China

- India

- Japan

- South Korea

- Australia

- Indonesia

- Malaysia

- Vietnam

- Thailand

- Philippines

- Singapore

- New Zealand

- Europe

- UK

- Germany

- France

- Italy

- Spain

- Russia

- Netherlands

- Sweden

- Poland

- Belgium

- Nordic

- Portugal

- Switzerland

- Latin America

- Brazil

- Mexico

- Argentina

- Chile

- Colombia

- Peru

- Ecuador

- Middle East & Africa

- Saudi Arabia

- UAE

- South Africa

- Turkey

- Egypt

- Israel

- Kenya

GLOBAL E-LEARNING MARKET FAQs

How big is the global e-learning market?

What is the growth rate of the global e-learning market?

What are the key trends in the global e-learning market?

Which region dominates the global e-learning market?

Who are the key players in the global e-learning market?

For more details, please reach us at [email protected]

- Chapter 1- Scope & Coverage

- Market Definition

- Inclusion

- Exclusions

- Market Estimation Caveats

- Market Derivation

- Market Segmentation by Learning Mode

- Market Segmentation by Function Type

- Market Segmentation by Content Type

- Market Segmentation by Delivery Mode

- Market Segmentation by Technology

- Market Segmentation by End-users

- Chapter 2- Premium Insights

- Chapter 3- Market Dynamics

- Introduction

- Overview

- Significant E-learning Trends

- Gaming Influence on E-Learning

- Key Market Findings

- Growth & Competitive Strategies

- Strategic Market Entry Recommendations

- Varied Market Revenue Models

- Integration of Technology & Education

- E-Learning Service Enhancement Analysis

- Value Chain Analysis

- Impact of The Ongoing Tariff War

- Market Opportunities & Trends

- Increasing Impact of Mobile or Smartphones In E-learning

- Growth of Blended Learning

- Increasing Use of AR & VR Application in E-learning

- Growth in Gamification

- Market Growth Enablers

- Emerging E-Learning Mobile Applications

- Evolution of Learning & Training in Digital Era

- Impact of 5G on Education Technology

- Government Initiatives for Digital Education

- Market Restraints

- Variability in Hardware & Software

- Inadequate Internet Bandwidth in Developing Countries

- Lack of Viable Revenue & Monetization Models

- Limited Access to Closed Markets & Platforms

- Market Landscape

- Five Forces Analysis

- Chapter 4- Market Segmentation

- Learning Mode (Market Size & Forecast: 2022-2031)

- Self-paced

- Instructor Led

- Function Type (Market Size & Forecast: 2022-2031)

- Training

- Testing

- Content Type (Market Size & Forecast: 2022-2031)

- Multimedia

- Interactive

- Text-based

- Delivery Mode (Market Size & Forecast: 2022-2031)

- Web-based

- Packaged content

- Blended

- Mobile

- Other modes

- Technology (Market Size & Forecast: 2022-2031)

- Learning management system (LMS)

- Mobile-based

- Virtual classroom

- Simulation-based

- Other Technologies

- End-users (Market Size & Forecast: 2022-2031)

- Corporates

- Academic institutions

- Individual learners

- Government organizations

- Healthcare sector

- Non-profit organizations

- Other users

- Chapter 5- Geography Segmentation

- Geography Segmentation (Market Size & Forecast: 2022-2031)

- Geographic Overview – Market Maturity Index

- North America

- US

- Canada

- APAC

- China

- India

- Japan

- South Korea

- Australia

- Indonesia

- Malaysia

- Vietnam

- Thailand

- Philippines

- Singapore

- New Zealand

- Europe

- UK

- Germany

- France

- Italy

- Spain

- Russia

- Netherlands

- Sweden

- Poland

- Belgium

- Nordic

- Portugal

- Switzerland

- Latin America

- Brazil

- Mexico

- Argentina

- Chile

- Colombia

- Peru

- Ecuador

- Middle East & Africa

- Saudi Arabia

- UAE

- South Africa

- Turkey

- Egypt

- Israel

- Kenya

- Chapter 6- Competitive Landscape

- Competitive Landscape

- Competition Overview

- Recent Developments

- Key Company Profiles

- Other Prominent Company Profiles

- Report Summary

- Key Takeaways

- Strategic Recommendations

Select a license type that suits your business needs

Single User Licence

- Report accessible by one user only

- Free 10% or 3 days of customization

- Free post-sale service assistance

- Continuous support through email

5 User Licence

- Report accessible by 5 users within the organization

- Free 15% or 4.5 days of customization

- Continuous support through email and telephone

- Free analyst hour

- Free Upgrade: If an updated report published within 180 days of purchase, you will get the revised report free of charge

Corporate Licence

- Free Datasheet worth $1500

- Report accessible by the entire organization

- Free 20% or 6 days of customization

- Free post-sale service assistance

- Continuous support through email and telephone

- Direct access to lead analysts

- Free analyst hour

- Free Upgrade: If an updated report published within 180 days of purchase, you will get the revised report free of charge

Datasheet Licence

- Report accessible by 1 user only

- Free 15% or 32 hours of customization

- Free post-sale service assistance

- Direct access to lead analysts

Frequently Asked Questions

How big is the global e-learning market?

What is the growth rate of the global e-learning market?

What are the key trends in the global e-learning market?

Which region dominates the global e-learning market?

Who are the key players in the global e-learning market?

Other RELATED Reports

U.S. Continuing Medical Education (CME) Market Research Report 2025-2030

Published : August 2025