Global Edtech Market Research Report 2026-2031

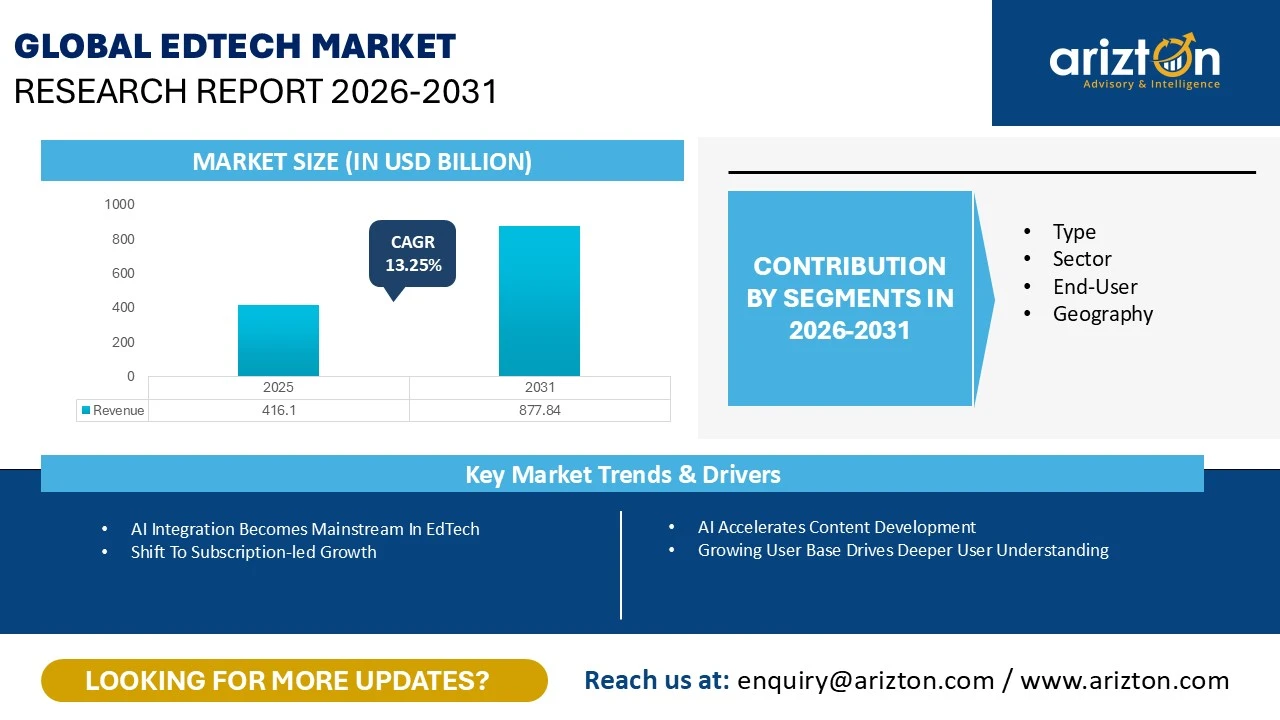

THE GLOBAL EDTECH MARKET SIZE WAS VALUED AT USD 416.10 BILLION IN 2025 AND IS EXPECTED TO REACH USD 877.84 BILLION BY 2031, GROWING AT A CAGR OF 13.25%.

EdTech Market Growth Insights – Driven by AI-Powered Content Development, Expanding Virtual Learning Adoption, Growing Demand for AI & Digital Skills, and Deeper Learner Personalization Through Advanced Analytics (2026–2031)

Published Date : June 2026

Last Updated : June 2026

format: PDF

edition : Fourth Edition

236 pages

7 tables

41 charts

region

countries

110 company

4 segments

Purchase Options

Global Edtech Market Research Report 2026-2031

THE GLOBAL EDTECH MARKET SIZE WAS VALUED AT USD 416.10 BILLION IN 2025 AND IS EXPECTED TO REACH USD 877.84 BILLION BY 2031, GROWING AT A CAGR OF 13.25%.

The Edtech Market Size, Share & Trends Analysis Report By

- Type: Hardware, Software, and Technology-Enabled Services

- Sector: K-12, Higher Education, Competitive Exams, and Certifications

- End-User: Individuals, Institutes, and Enterprises

- Geography: North America, Europe, APAC, Latin America, and Middle East & Africa

Industry Analysis Report, Regional Outlook, Growth Potential, Price Trends, Competitive Market Share & Forecast 2026–2031.

This report includes market data points, ranging from trend

analyses to market estimates & forecasts that you can customize

EDTECH MARKET REPORT SCOPE

| REPORT ATTRIBUTE | DETAILS |

|---|---|

| MARKET SIZE (2031) | USD 877.84 Billion |

| MARKET SIZE (2025) | USD 416.10 Billion |

| CAGR (2025-2031) | 13.25% |

| HISTORIC YEAR | 2022-2024 |

| BASE YEAR | 2025 |

| FORECAST YEAR | 2026-2031 |

| SEGMENTS BY | Type, Sector, End-user, and Geography |

| GEOGRAPHIC ANALYSIS | North America, Europe, APAC, Latin America, & Middle East & Africa |

| KEY PLAYERS | Codemao, TAL Education, Elice, Headway Inc., Ten Thousand Coffees, Passage, Stepful, Arduino, Wiley, Vitru, Mathflat, and Ellucian |

EDTECH MARKET SIZE & SHARE

The global edtech market size was valued at USD 416.10 billion in 2025 and is expected to reach USD 877.84 billion by 2031, growing at a CAGR of 13.25 % during the forecast period. The market is experiencing significant growth, driven by several factors, including AI accelerating content development, a growing user base driving deeper user understanding, increasing virtual learning adoption, and rising demand for AI and digital skills.

EdTech companies are shifting from transactional course sales to subscription-led recurring revenue models. AI is becoming mainstream across teaching, learning, and platform operations rather than remaining a standalone feature.

Demand is increasingly driven by institutions and enterprises rather than individual learners, creating longer-term, more stable revenue opportunities. The preference for short, modular, and career-aligned programs is growing, and markets such as China are re-emerging under restructured, regulation-compliant models.

KEY TAKEAWAYS

- Type: The hardware segment accounted for the largest market share of around 50%.

- Sector: The K-12 segment accounted for the largest global edtech market share.

- End-User: The individual segment shows the highest growth, with a CAGR of 13.71% during the forecast period.

- Geography: APAC dominates the global EdTech market with a share of over 45%.

Recent Developments in the Global EdTech Market

- On March 27, 2026, the UNESCO 2026 “AI Day” global event was held in Paris, during which UNESCO announced a 10-year strategic cooperation agreement with Codemao for the period 2026–2035, marking a significant development in global AI education collaboration.

- In December 2025, Elice Inc. (CEO Jae Won Kim) became the first Korean AI education solutions company to secure a digital textbook (Interactive Digital Textbook, IDT) development project led by the Singapore Ministry of Education (MOE), strengthening its presence in the global education market.

- On February 9, 2026, Wiley announced that it had signed over 125 transformational agreements with library consortia and institutions worldwide, strengthening global access to peer-reviewed research and supporting wider knowledge dissemination.

- On October 7, 2025, Qualcomm announced the acquisition of Arduino for its open-source hardware platform widely used by developers and the global maker community.

GLOBAL EDTECH MARKET TRENDS

Shift to Subscription-led Growth

The EdTech sector is undergoing a structural transition from high-growth, discount-driven user acquisition toward more stable, recurring revenue models. Companies are increasingly prioritizing subscription-based offerings that provide continuous access to learning content, tools, and services for individuals, institutions, and enterprises. For instance, subscription penetration rate for Duolingo has risen every single year from 2021 to 2025, even as the business scaled past $1B in total revenue. This shift aligns EdTech business models more closely with software-as-a-service frameworks, emphasizing sustained user engagement, content refresh, and long-term value delivery over one-time course sales. Leading platforms are reinforcing this transformation by pivoting toward subscription-led strategies, improving revenue predictability, and enhancing profitability, even as traditional consumer-driven revenues become less central to growth.

Teacher First Product Thinking in K-12 and Higher Education

The EdTech market in K–12 and higher education is increasingly shifting toward a teacher-first approach, where product design prioritizes reducing educators’ workload and streamlining routine tasks rather than simply expanding student-facing features. Platforms focus on tools that automate content creation, assessment, and classroom management, enabling teachers to allocate more time to instruction, feedback, and student engagement. For instance, Instructure positions Canvas as a teacher‑first platform, marketing features such as pre‑built course templates, time‑saving workflows, and Ignite AI tools as ways to “reclaim time” and reduce everyday admin in K‑12 and higher education. This transition reflects growing institutional demand for solutions that improve efficiency amid resource constraints, making ease of use and time savings critical drivers of adoption and retention. Leading providers are aligning their offerings and messaging around supporting educators, positioning their platforms as tools that integrate seamlessly into existing workflows, enhance instructional effectiveness, and strengthen long-term relationships with schools and universities.

EDTECH MARKET DRIVERS

Growing User Base Drives Deeper User Understanding

The EdTech industry is increasingly defined by the advantages of scale, where large platforms leverage extensive and continuously growing learner interaction data to enhance personalization, engagement, and product performance. For instance, Duolingo reports over 50 million daily active users and well over 100 million monthly active users on its language platform, and cumulative registrations in the hundreds of millions, giving it one of the largest engaged learner bases in consumer EdTech. The data, generated through diverse user activities across subjects and formats, enables more accurate recommendations, adaptive learning pathways, and faster iteration through experimentation. Integrated with AI and analytics, these capabilities allow leading providers to refine content, optimize user experiences, and deploy improvements efficiently across their ecosystems. As a result, scale is evolving from a by-product of growth into a core strategic asset, reinforcing a cycle where richer data drives better outcomes and stronger platform performance, positioning larger players to maintain a competitive edge over smaller, data-constrained providers.

Rising Demand for AI And Digital Skills

Demand for AI and digital skills is becoming one of the strongest pull factors in the EdTech market, as learners move beyond broad digital literacy toward targeted training in machine learning, data analysis, cybersecurity, and cloud platforms that match specific tools and workflows. For instance, Simplilearn said in July 2025 that enrollments in GenAI courses on its free SkillUP platform had grown 470% year on year, and that it had responded by launching 100+ free GenAI courses. Employers are reinforcing this shift by prioritizing job-ready capabilities, which is driving faster growth in AIfocused courses, micro-credentials, and professional certificates than in many general subjects. Short, modular programs aimed at working professionals are especially prominent because they can be updated frequently and align closely with evolving hiring needs, turning AI and data skills into core elements of employability and career progression. For platforms, this raises the bar on how often content must be refreshed and how closely providers must work with industry partners, favoring those that can keep curricula current while repositioning their offerings around AI-related skilling demand.

INDUSTRY RESTRAINTS

Data Privacy and Cybersecurity Risks

Data privacy and cybersecurity have become some of the most visible and serious challenges for global EdTech, as large platforms handling sensitive student information face repeated breaches and growing regulatory scrutiny. Recent incidents involving K-12 vendors and learning management systems show how weak identityand access controls, poor data minimization, and delayed breach notifications can expose millions of student records and trigger legal and enforcement actions. For instance, in September 2025, Instructure disclosed that it had been targeted in a social engineering attack involving its Salesforce system. The company said no product data was accessed, and the exposed information mainly included public business details such as company names and contact information. High-profile cases and lawsuits highlight that education technology is now treated as critical data infrastructure rather than a purely pedagogical choice, with regulators demanding stronger security programs, clearer data-handling practices, and accurate disclosures. At the same time, the rising volume and sophistication of cyberattacks on schools and universities underline that platforms must invest in robust security, faster incident response, and greater transparency to maintain institutional trust while managing large volumes of sensitive learner data.

EDTECH MARKET SEGMENTATION INSIGHTS

INSIGHT BY TYPE

The global edtech market by type is segmented into hardware, software, and technology-enabled services. The hardware segment accounted for the largest market share of around 50%. EdTech hardware is the foundational layer of smart classrooms, covering all physical devices and infrastructure used to deliver digital learning. Although it holds the largest market share, its growth is slower because spending is driven by one-time or periodic deployments rather than continuous consumption. The segment is pulled between government-led rollouts in emerging markets like India, China, and Saudi Arabia and budget freezes or deferrals in mature markets such as the US.

Major vendors are responding with premium AI-enabled devices for well-funded institutions, budget options for cost‑constrained schools, and an expanded hardware mix that now includes VR headsets as they enter mainstream school procurement.

INSIGHT BY SECTOR

Based on the sector, the K-12 segment accounted for the largest global edtech market share. K‑12, covering kindergarten to Grade 12, is the largest and most widely served segment in global EdTech. School‑level digitization remains the main demand engine, but there is growing tension between widespread deployment and uneven utilization quality, teacher readiness, and learning impact. Districts are consolidating tools and prioritizing proven impact, while generative AI, analytics/adaptive technologies, and untethered broadband emerge as key enablers alongside persistent challenges around staffing, changing teaching practice, and digital equity.

INSIGHT BY END-USER

The global edtech market by end-user is segmented into individuals, institutes, and enterprises. The individuals segment shows significant growth, with the fastest-growing CAGR of 13.71% during the forecast period. Individual learners represent the largest end‑user segment in the global EdTech market. This reflects strong uptake of self‑paced learning apps, test‑prep platforms, upskilling tools, certification programs, and subscription‑based products among students, professionals, and lifelong learners who want to study at their own pace and convenience.

Most users are adults seeking to upskill, reskill, or supplement university learning, often using short videos, quizzes, hands‑on projects, and peer forums, and then sharing digital certificates with employers or on LinkedIn. Many platforms rely on freemium models, allowing learners to access course videos for free while charging for graded assignments, certificates, or full program features.

EDTECH MARKET GEOGRAPHICAL ANALYSIS

APAC dominates the global EdTech market by emerging as both the largest and fastest-growing regional hub. It accounts for over 45% of the market share. The region’s leadership is underpinned by its massive scale in China and India, complemented by more mature, policy-driven markets such as Japan, South Korea, Singapore, and Australia, and high-growth but execution-sensitive opportunities in Indonesia.

Among the countries, China is the largest EdTech market by revenue. Despite the Double Reduction policy, China remains the largest EdTech market by revenue within APAC, driven by its massive, policy-shaped education system, deep digital penetration, and the scale effects of state-backed platforms like the Smart Education of China. India, meanwhile, is the fastest‑growing major market in the region, supported by its large school and college‑age population, strong private‑sector participation, and rising government focus on digital skilling and employability, which together drive a higher compound annual growth rate from a smaller base.

North America’s edtech market is among the most structurally advanced globally, supported by strong digital infrastructure, high institutional spending capacity, and demand spanning K–12, higher education, workforce skilling, and adult learning.

Unlike in emerging markets, growth here is no longer driven by access expansion but by improving learning effectiveness, integrating AI into education systems, and meeting increasingly complex institutional procurement and compliance requirements.

US dominates North America’s edtech market as it is structurally attractive for edtech because demand is spread across K-12, higher education, adult learning, and workforce skilling rather than depending on one age cohort alone. That makes the market less about population growth and more about institutional budgets, learner outcomes, and workforce transitions.

The US education system is unusually fragmented for EdTech. Federal guidance matters, but curriculum, procurement, platform choice, and implementation decisions are spread across states, districts, schools, and institutions. This fragmentation is one of the most important market realities because vendors scale through thousands of buyers, not one ministry.

EDTECH MARKET COMPETITIVE LANDSCAPE

The global EdTech market is highly fragmented, with tens of thousands of providers and even the largest public companies capturing only a limited share. The United States, India, and the United Kingdom host the highest concentration of EdTech originations, and homegrown players dominate their domestic markets thanks to deeper alignment with local curricula, languages, user behavior, and regulation. Buyer power is high: institutions impose centralized, outcomes-focused procurement, while individuals can switch easily among low-cost or free options such as MOOCs, open courseware, and AI-based learning tools, driving pricing pressure and content commoditization. Traditional tutoring and classroom instruction remain strong competitors in many regions, and the rise of generative AI assistants further reduces the perceived need for paid platforms. Combined with high-profile failures and policy shocks that can rapidly reshape national markets, these dynamics create a landscape where scale and funding do not guarantee survival, and localization, differentiation, and regulatory resilience are critical.

SNAPSHOT

The global edtech market size is expected to grow at a CAGR of approximately 4.80% from 2025 to 2031.

The following factors are likely to contribute to the growth of the global edtech market during the forecast period:

- AI Accelerates Content Development

- Growing User Base Drives Deeper User Understanding

- Increasing Virtual Learning Adoption

- Rising Demand For AI And Digital Skills

Base Year: 2025

Forecast Year: 2026-2031

The report examines the current state of the global edtech market and its market dynamics through 2026−2031. It covers a detailed overview of several market growth enablers, restraints, and trends. The study covers both the demand and supply sides of the market. It also profiles and analyses leading companies and several other prominent companies operating in the market.

Key Vendors

- Codemao

- Business Overview

- Product Offerings

- Key Developments

- Key Strategies

- Key Opportunities

- Key Strengths

- TAL Education

- Elice

- Headway Inc.

- Ten Thousand Coffees

- Passage

- Stepful

- Arduino

- Wiley

- Vitru

- Mathflat

- Ellucian

Other Prominent Vendors

- Udacity

- Business Overview

- Product Offerings

- Thinkfic

- Emeritus

- UpGrad

- Memrise

- Articulate

- Plural Sight

- Age of Learning

- Instructure

- 360 Learning

- Civitas

- Future Learn

- Docebo

- Xello

- Degreed

- 2U

- Goodwall

- Treehouse

- Classover

- Lecturio

- Instride

- Boxlight

- Matific

- 3P Learning

- Classdojo

- Xuetangx

- Panopto

- Codesignal

- AcadeMedia

- Loft Dynamics

- Noredink

- Cengage

- Pickatale

- Yuanfudao

- Pebble

- Formative

- Morressier

- Mocking Bird

- Atom Learning

- Red Shelf

- Embrace

- Skilljar

- Brio

- Flywire

- Kahoot

- Mindstone

- AMOpportunities

- Bettermarks

- Knowbe4

- Collegevine

- NewTedu

- ST Unitas

- Curriculum Associates

- Influential

- Education.com

- Nerdy

- 17 Zuoye

- Kiddom

- Interview Kickstart

- Sanoma

- Reselia

- Cyberguru

- Turnitin

- Tutored by Teachers

- Agora

- Acadeum

- Digischool

- Cake

- Offee

- Arco

- Google Education

- Strivr

- Lingokids

- Hoxhunt

- Quizlet

- Pearson

- Medway

- Forta

- Chegg

- Skillsoft

- Coursera

- Udemy

- Acorns

- Bright Horizons

- Duolingo

- Great Minds

- Techwolf

- Xueleyun

- Xeropan

- Seismic

- Coach Hub

- Allen

- Creative Live

- Intuitivo

- Uolo

- Applyboard

- Klaxoon

- Compass Education

Segmentation by Type

- Hardware

- Software

- Technology-Enabled Services

Segmentation by Sector

- K-12

- Higher Education

- Competitive Exams

- Certifications

Segmentation by End-User

- Individuals

- Institutes

- Enterprises

Segmentation by Geography

- North America

- US

- Canada

- APAC

- China

- India

- Japan

- South Korea

- Australia

- Indonesia

- Singapore

- Europe

- Germany

- UK

- Italy

- Spain

- Netherlands

- Latin America

- Brazil

- Mexico

- Argentina

- Middle East & Africa

- South Africa

- Nigeria

- Kenya

- GCC

EDTECH MARKET FAQs

How big is the global edtech market?

What is the growth rate of the global edtech market?

What are the key trends in the global edtech market?

Which type segment provides more business opportunities in the global edtech market?

Who are the key vendors in the global edtech market?

Which region dominates the global edtech market?

EXHIBIT 1 Global EdTech Market 2022-2031 ($ billion)

EXHIBIT 2 Global EdTech Market by Type 2022-2031 ($ billion)

EXHIBIT 3 Market by Hardware 2022-2031 ($ billion)

EXHIBIT 4 Market by Software 2022-2031 ($ billion)

EXHIBIT 5 Market by Technology-enabled Services 2022-2031 ($ billion)

EXHIBIT 6 Global EdTech Market by Sector 2022-2031 ($ billion)

EXHIBIT 6 Market by K-12 2022-2031 ($ billion)

EXHIBIT 8 Market by Higher Education 2022-2031 ($ billion)

EXHIBIT 9 Market by Competitive Exams 2022-2031 ($ billion)

EXHIBIT 10 Market by Certifications 2022-2031 ($ billion)

EXHIBIT 11 Global EdTech Market by End-User 2022-2031 ($ billion)

EXHIBIT 12 Market by Individuals 2022-2031 ($ billion)

EXHIBIT 13 Market by Institutes 2022-2031 ($ billion)

EXHIBIT 14 Market by Enterprises 2022-2031 ($ billion)

EXHIBIT 15 Global EdTech Market by Geography 2022-2031 ($ billion)

EXHIBIT 16 North America EdTech Market 2022-2031 ($ billion)

EXHIBIT 17 US EdTech Market 2022-2031 ($ billion)

EXHIBIT 18 Canada EdTech Market 2022-2031 ($ billion)

EXHIBIT 19 APAC EdTech Market 2022-2031 ($ billion)

EXHIBIT 20 China EdTech Market 2022-2031 ($ billion)

EXHIBIT 21 India EdTech Market 2022-2031 ($ billion)

EXHIBIT 22 Japan EdTech Market 2022-2031 ($ billion)

EXHIBIT 23 South Korea EdTech Market 2022-2031 ($ billion)

EXHIBIT 24 Australia EdTech Market 2022-2031 ($ billion)

EXHIBIT 25 Indonesia EdTech Market 2022-2031 ($ billion)

EXHIBIT 26 Singapore EdTech Market 2022-2031 ($ billion)

EXHIBIT 27 Europe EdTech Market 2022-2031 ($ billion)

EXHIBIT 28 Germany EdTech Market 2022-2031 ($ billion)

EXHIBIT 29 UK EdTech Market 2022-2031 ($ billion)

EXHIBIT 30 Italy EdTech Market 2022-2031 ($ billion)

EXHIBIT 31 Spain EdTech Market 2022-2031 ($ billion)

EXHIBIT 32 Netherlands EdTech Market 2022-2031 ($ billion)

EXHIBIT 33 Latin America EdTech Market 2022-2031 ($ billion)

EXHIBIT 34 Brazil EdTech Market 2022-2031 ($ billion)

EXHIBIT 35 Mexico EdTech Market 2022-2031 ($ billion)

EXHIBIT 36 Argentina EdTech Market 2022-2031 ($ billion)

EXHIBIT 37 Middle East & Africa EdTech Market 2022-2031 ($ billion)

EXHIBIT 38 South Africa EdTech Market 2022-2031 ($ billion)

EXHIBIT 39 Nigeria EdTech Market 2022-2031 ($ billion)

EXHIBIT 40 Kenya EdTech Market 2022-2031 ($ billion)

EXHIBIT 41 GCC EdTech market 2022-2031 ($ billion)

LIST OF TABLES

TABLE 1Global EdTech Market 2022-2031 ($ billion)

TABLE 2Global EdTech Market by Type Segmentation 2022-2031 ($ billion)

TABLE 3Global EdTech Market by Sector Segmentation 2022-2031 ($ billion)

TABLE 4Global EdTech Market by End-User Segmentation 2022-2031 ($ billion)

TABLE 7Global EdTech Market by Geography 2022-2031 ($ billion)

CHAPTER – 1: Global EdTech Market Overview

- Executive Summary

- Key Findings

- Key Developments

CHAPTER – 2: Global EdTech Market Segmentation Data

- Type Market Insights (2022-2031)

- Hardware

- Software

- Technology-Enabled Services

- Sector Market Insights (2022-2031)

- K-12

- Higher Education

- Competitive Exams

- Certifications

- End-User Market Insights (2022-2031)

- Individuals

- Institutes

- Enterprises

CHAPTER – 3: Global EdTech Market Prospects & Opportunities

- Global EdTech Market Drivers

- Global EdTech Market Trends

- Global EdTech Market Constraints

CHAPTER – 4: Global EdTech Market Overview

- Global EdTech Market -Competitive Landscape

- Global EdTech Market - Key Players

- Global EdTech Market - Key Company Profiles

CHAPTER – 5: Appendix

- Research Methodology

- Abbreviations

- Arizton

Select a license type that suits your business needs

Single User Licence

- Report accessible by one user only

- Free 10% or 3 days of customization

- Free post-sale service assistance

- Continuous support through email

5 User Licence

- Report accessible by 5 users within the organization

- Free 15% or 4.5 days of customization

- Continuous support through email and telephone

- Free analyst hour

- Free Upgrade: If an updated report published within 180 days of purchase, you will get the revised report free of charge

Corporate Licence

- Free Datasheet worth $1500

- Report accessible by the entire organization

- Free 20% or 6 days of customization

- Free post-sale service assistance

- Continuous support through email and telephone

- Direct access to lead analysts

- Free analyst hour

- Free Upgrade: If an updated report published within 180 days of purchase, you will get the revised report free of charge

Datasheet Licence

- Report accessible by 1 user only

- Free 15% or 32 hours of customization

- Free post-sale service assistance

- Direct access to lead analysts

Frequently Asked Questions

How big is the global edtech market?

What is the growth rate of the global edtech market?

What are the key trends in the global edtech market?

Which type segment provides more business opportunities in the global edtech market?

Who are the key vendors in the global edtech market?

Which region dominates the global edtech market?

Other RELATED Reports

U.S. Continuing Medical Education (CME) Market Research Report 2025-2030

Published : August 2025