Europe Data Center Market Landscape 2026-2031

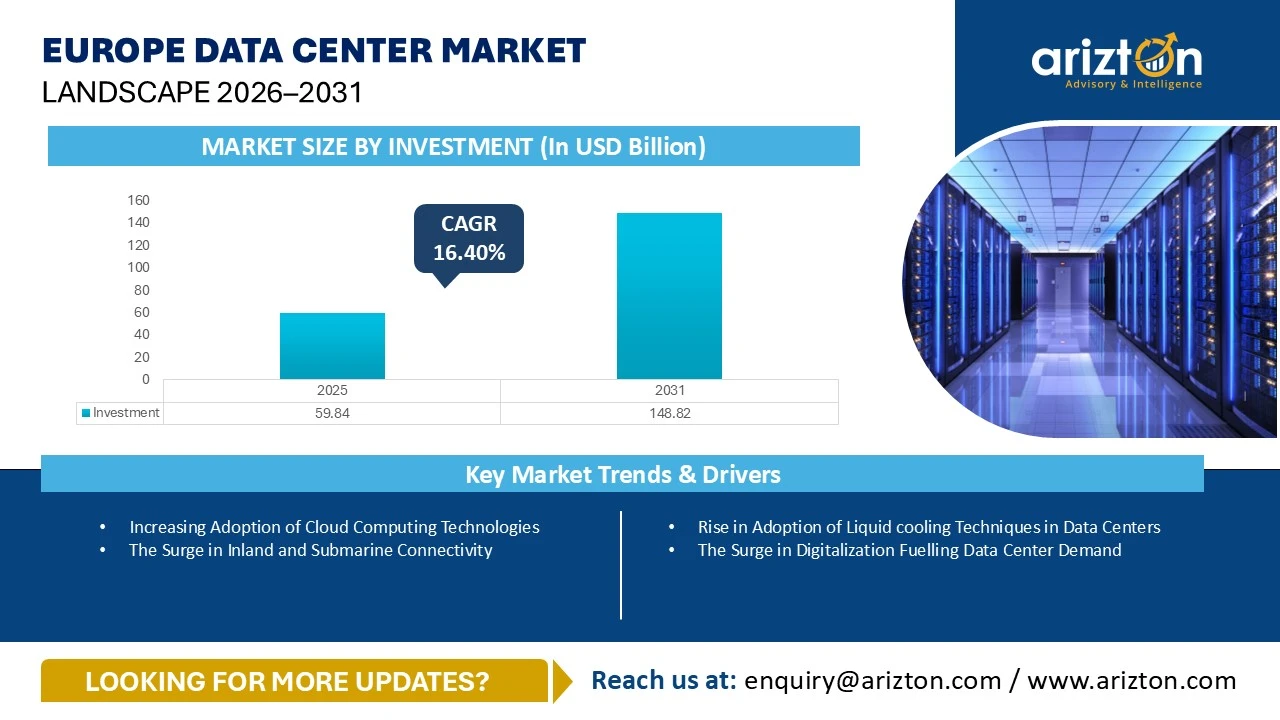

THE EUROPE DATA CENTER MARKET SIZE WITNESSED INVESTMENTS OF USD 59.84 BILLION IN 2025 AND WILL WITNESS INVESTMENTS OF USD 148.82 BILLION BY 2031, GROWING AT A CAGR OF 16.40% DURING THE FORECAST PERIOD

571 pages

419 company

10 segments

3 region

20 countries

Purchase Options

Europe Data Center Market Landscape 2026-2031

THE EUROPE DATA CENTER MARKET SIZE WITNESSED INVESTMENTS OF USD 59.84 BILLION IN 2025 AND WILL WITNESS INVESTMENTS OF USD 148.82 BILLION BY 2031, GROWING AT A CAGR OF 16.40% DURING THE FORECAST PERIOD

The Europe Data Center Market Size, Share, & Trends Analysis By

- Facility Type: Hyperscale Data Centers, Colocation Data Centers, and Enterprise Data Centers

- Infrastructure: IT Infrastructure, Electrical Infrastructure, Mechanical Infrastructure, and General Construction

- IT Infrastructure: Server Infrastructure, Storage Infrastructure, and Network Infrastructure

- Electrical Infrastructure: UPS Systems, Generators, Transfer Switches & Switchgear, PDUs, and Other Electrical Infrastructure

- Mechanical Infrastructure: Cooling Systems, Racks, and Other Mechanical Infrastructure

- Cooling Systems: CRAC & CRAH Units, Chiller Units, Cooling Towers, Condensers, Dry Coolers, and Other Cooling Units

- Cooling Techniques: Air-based and Liquid-based

- General Construction: Core & Shell Development, Installation & Commissioning Services, Engineering & Building Design, Physical Security, Fire Detection & Suppression, and DCIM

- Tier Standard: Tier I & II, Tier III, and Tier IV

- Geography: Western Europe (UK, Germany, France, Netherlands, Ireland, Switzerland, Italy, Spain, Belgium, Portugal, Greece, & Other Western European Countries), Nordics (Denmark, Sweden, Norway, Finland, and Iceland), Central & Eastern Europe (Russia, Poland, Austria, Czechia, & Other Central & Eastern European Countries)

Industry Analysis Report, Regional Outlook, Growth Potential, Price Trends, Competitive Market Share & Forecast 2026–2031.

This report includes market data points, ranging from trend

analyses to market estimates & forecasts that you can customize

EUROPE DATA CENTER MARKET REPORT SCOPE

| REPORT ATTRIBUTE | DETAILS |

|---|---|

| MARKET SIZE – INVESTMENT (2031) | USD 148.82 Billion |

| MARKET SIZE – INVESTMENT (2025) | USD 59.84 Billion |

| CAGR - INVESTMENT (2025-2031) | 16.40% |

| MARKET SIZE - AREA (2031) | 16.22 million Square feet |

| POWER CAPACITY (2031) | 4,294 MW |

| HISTORIC YEAR | 2022-2024 |

| BASE YEAR | 2025 |

| FORECAST YEAR | 2026-2031 |

| SEGMENTS BY | Facility Type, Infrastructure, IT Infrastructure, Electrical Infrastructure, Mechanical Infrastructure, Cooling Systems, Cooling Techniques, General Construction, Tier Standard, Geography |

| GEOGRAPHIC ANALYSIS | Western Europe, Nordics, and Central & Eastern Europe |

EUROPE DATA CENTER MARKET SIZE & INSIGHTS

The Europe data center market size witnessed investments of USD 59.84 billion in 2025 and will witness investments of USD 148.82 billion by 2031, growing at a CAGR of 16.40% during the forecast period. The Europe data center market is witnessing rapid growth, fueled by wide range of growth factors like the surge in adoption of advanced technologies such as Artificial Intelligence (AI), Machine Learning, big data, Internet of Things (IoT), and robotics, increasing sustainability practices among data center operators and hyperscalers, surge in demand for digitalization, integration of district heating into data centers, development of smart city projects, rising submarine and inland connectivity, increasing government support for data centers, deployment of 5G connectivity, surge in demand for cloud computing, and other factors.

In Europe, Frankfurt, London, Amsterdam, Paris, and Dublin stand out as prominent destinations for data center development, and these locations have been experiencing a continuous rise in data center investments. The data center expansion in these locations is likely to slow down during the forecast period because of the rising power and land scarcity challenges. On the other hand, the secondary markets like Milan, Madrid, Brussels, Lisbon, Athens, Oslo, Stockholm, Copenhagen, Helsinki, Warsaw, and Vienna are establishing themselves as prominent destinations for data center development.

As the primary markets, including UK, Germany, France, and Netherlands are experiencing rapid digitalization, the governments across these nations are increasingly developing Free Trade Zones, Industrial Parks, and Special Economic Zones to attract enterprises across various sectors, including data centers to develop data centers.

In 2025, the UK accounted for the highest data center investments in the Europe data center market, contributing to generating around 27% of the data center investments, followed by Germany, which accounted for around 12% of the data center investments in the same period. The Nordic countries like Norway, Sweden, Finland and others are positioning themselves as prominent destinations for AI-ready data center development because of the presence of abundant renewable energy sources and cool climate, which is beneficial for data center operations. The nations like Luxembourg, Hungary, Ukraine, Estonia, Romania, Lithuania, and others are likely to gain momentum for data center development gradually over the next five years.

EUROPE DATA CENTER MARKET SEGMENTATION INSIGHTS

- The need for liquid cooling solutions is growing steadily in European data centers, driven by the swift rise in innovations from emerging technologies such as Artificial Intelligence. Data center operators are integrating GPUs in data centers to effectively handle Artificial Intelligence workloads, which will produce increased heat. Conventional air cooling methods are inadequate for dissipating large quantities of heat, requiring companies to adopt liquid cooling solutions. In 2025, liquid cooling technologies accounted for about 30.38% of the cooling technique investments, and this share is expected to rise to around 36.52% of the cooling technique investments by 2031.

- There has been a steady rise in the demand for sustainable data center infrastructure throughout Europe. Companies are increasingly investing in battery energy storage systems and sustainable batteries such as lithium-ion and sodium-ion batteries to replace traditional lead-acid batteries in data centers. For instance, the MAN1-Chester data center, managed by nLighten in Cheshire, UK, has been installed with lithium-ion batteries to reduce the data center's environmental footprint.

- The organizations in various sectors, such as technology, finance, energy, education, and others, are making substantial investments to establish their own data center facilities to handle their digital workloads and digital data. Investments in enterprise data center facilities are expected to rise during the forecast period because of the rapid surge in digitalization. In January 2026, the energy company UK Industrial Fusion Solutions (UKIFS) planned to invest approximately $10.6 million in establishing an enterprise data center in the UK to handle the firm’s digital operations.

- Numerous data center operators throughout European nations are prioritizing the development of AI-optimized data centers, featuring advanced liquid cooling systems, high-density racks, Graphics Processing Units (GPUs), and increased IT capacity loads. The demand for AI-optimized data centers is expected to rise significantly during the forecast period. In December 2025, Argyll Infrastructure Holdings (AIH) obtained funding of around $19.97 million to build an AI-optimized data center in Scotland, United Kingdom.

- The growing need for hyperscale data center infrastructure is enhancing investments in the European data center market due to the rising requirements for Artificial Intelligence (AI) and high-performance computing (HPC). In November 2025, the hyperscale company Google announced its intention to invest more than $6.38 billion to enhance its data center capabilities in Germany. The firm plans to establish a new data center in Dietzenbach and enhance its current data center in Hanau as part of its investment.

- Data center operators are investing in chilled-water cooling systems and free cooling systems to minimize water and energy use in data centers, while lowering the facilities’ carbon footprints and environmental impact. For instance, the LON-East data facility, operated by Green Mountain in London, UK, utilizes chilled-water cooling technology to minimize water usage. Moreover, CyrusOne’s FRA1 data center, located in Frankfurt, Germany, features free cooling technology to lower electricity usage.

- The primary contributors to the increase in data center power capacity in the Europe data center market are colocation operators. In 2025, colocation data centers contributed for more than 68% of the power capacity share in the Europe data center market. Colocation providers such as nLighten, EdgeMode, Bulk Infrastructure, Iron Mountain, and various others are entering into power purchase agreements (PPAs) with renewable energy companies to obtain renewable energy for their data center operations, promoting sustainability.

- Multiple data center operators have been utilizing backup generators powered by renewable energy to reduce their environmental footprint. In recent years, the use of Hydrotreated Vegetable Oil (HVO) fueled generators has increased in the European data center sector. This trend is expected to increase further in the next five years. In October 2025, Telehouse, a data center operator, began building a new data center in London, UK, featuring backup generators powered by Hydrotreated Vegetable Oil (HVO).

- Data center operators are focusing on investing in the installation of high-density racks in data centers to effectively accommodate high-performance computing and AI workloads. For example, the data center facility, operated by Lefdal Mine Datacenters in Maloy, Norway, features high-density racks that can support rack densities exceeding 50 kW per rack.

- Implementing BMS/DCIM software in data centers reduces energy use and carbon footprint, helping data center operators lower operational expenses and carbon footprint. Digital Realty’s FRA18 data center in Frankfurt, Germany, offers a 24/7 remote hands service.

EUROPE DATA CENTER MARKET KEY TRENDS & DRIVERS

Rising Adoption of Liquid Cooling Techniques in Data Centers

- Data centers across Europe are progressively utilizing liquid cooling methods since conventional air-based cooling solutions are inadequate for managing the significant heat produced by Artificial Intelligence (AI) and high-performance computing workloads (HPC). Consequently, data center operators are progressively investing in liquid cooling methods since they provide improved thermal management.

- In October 2025, the UK-based company, Spode Works Regeneration Ltd, revealed its plans to build a new data center in Staffordshire, the UK; the facility is likely to be equipped with a direct-to-chip liquid cooling technique.

- The increasing need to dissipate substantial heat in data centers throughout European nations, fueled by AI and HPC workloads, is driving the demand for emerging liquid cooling techniques like direct-to-chip and immersion cooling techniques. Data center companies throughout Europe are expected to significantly invest in implementing advanced liquid cooling technologies in their facilities over the next five years.

The Surge in Digitalization Fuelling Data Center Demand

- The European nations are consistently experiencing a fast rise in digitalization as entities across various sectors, such as government, banking, finance, healthcare, education, and more, are progressively embracing digital technologies, including cloud computing, Artificial Intelligence, big data, Internet of Things, and other digital innovations.

- In May 2025, Sweden's government announced that it had introduced Sweden’s Digitalisation Strategy 2025–2030 to establish a clear vision for enhancing digitalization across the country over the next five years, and the Strategy is likely to focus on five areas, such as digital competence, digitalization of business, digitalization of administration, the digitalization of welfare, and enhancing connectivity infrastructure across the country.

- The expanding digitalization throughout European nations is expected to boost the need for edge data centers in Europe to gather, store, and process data nearer to end users, ensuring low latency and high-speed real-time digital services.

Rise in District Heating Concept

- The idea of district heating, an intelligent method to utilize waste heat produced by data centers, is gaining significant traction in the European data center market. Data center facilities produce large amounts of heat, which in earlier years was merely expelled into the atmosphere. In recent years, many data center operators in European countries have been reusing the waste heat produced in data center facilities and redirecting it to meet the heating demands of nearby residential, commercial, and public facilities via district heating systems.

- In February 2026, nLighten, the European company, announced its intention to supply waste heat from its data center located in Stuttgart, Germany, to the regional district heating system. The initiative is expected to provide around 1.8MW of heat, aiding the city’s efforts in decarbonization and sustainable energy.

- The development of integrated district heating systems in data centers is anticipated to rise substantially in the Europe data center market during the forecast period as data center firms are focusing on sustainability and energy efficiency initiatives.

Increasing Adoption of Cloud Computing Technologies

- The demand for cloud computing technologies in European nations has been rising swiftly due to the strict data regulation policies in the region, a surge in digitalization, the rollout of 5G connectivity services, and other factors.

- In November 2025, the cloud services provider OVHcloud launched a third cloud region in Berlin, Germany, enhancing resilience and security for European digital infrastructure. The company introduced the OVHcloud AI EndPoint inference platform in partnership with SambaNova Systems to provide high-performance AI inference solutions.

- The rising use of cloud-computing services in European nations is expected to boost the demand for data centers in the region during the forecast period, as cloud providers need low-latency and scalable infrastructure to facilitate the growing digital landscape of Europe.

The Surge in Inland and Submarine Cable Connectivity

- Europe is enhancing its digital infrastructure through investments in submarine cable connectivity, which significantly improves the region's data transmission speeds and cross-border connectivity to meet the rising demands for Artificial Intelligence, cloud computing, and digitalization throughout European nations.

- Amazon Web Services intends to establish a new cable landing station (CLS) in Cork, Ireland, in January 2026. The cable landing station is expected to be situated at Tullyneasky West, and the project will include building a cable landing station, a substation, a switch room building, and external plant infrastructure, such as generators and fuel tanks.

- The growth of submarine cable connectivity development among European nations is expected to increase during the forecast period, which is crucial to meet the growing demand for high-speed internet, cloud services, and digital transformation throughout Europe, resulting in higher demand for data centers across European countries.

Increasing Government Support for Data Centers

- The governments throughout Europe have understood the importance of data centers in boosting digital economies and promoting technological progress. Consequently, governments throughout European nations are launching different initiatives to promote data center growth, enhance digital infrastructure, and support sustainable data center practices across Europe.

- In January 2026, UK lawmakers formed the Data Centres APPG (All-Party Parliamentary Group), an initiative aimed at improving awareness of the UK's data center industry. The team seeks to investigate the contribution of data centers to economic development, enhance digital infrastructure resilience, and aid the UK's net-zero goals.

- During the forecast period, we anticipate that the government support for data centers will increase significantly via initiatives that promote renewable energy use and partnerships with international technology firms. Europe is expected to witness more investments from local and global stakeholders in the data center industry during the forecast period.

EUROPE DATA CENTER MARKET GEOGRAPHICAL ANALYSIS

- The UK accounted for the highest power capacity share in the Europe data center market in 2025, representing approximately 17.46% of the market's power capacity share. In December 2025, the Renewable Energy Association in the UK launched a new Data Center Coalition to assist data center firms in obtaining clean electricity for their operations throughout the UK.

- In the European data center market, most of the investments come from Western Europe, as the region houses robust digital hubs. In 2025, Western Europe accounted for about 76.75% of the total investments in the market, followed by the Nordics and Central & Eastern Europe. In Western Europe, the FLAP-D market has been leading data center investments for many years.

- Several data center firms are focusing on investing in the Nordic countries to establish data centers due to the existence of huge renewable resources in the region, helping them reduce their environmental footprint. Furthermore, the area's cool climate enables companies to utilize free-cooling technologies to lower electricity usage in data centers, thus decreasing operational expenses. The Nordic region is becoming a leading AI hub globally, attracting both local and international data center firms to invest in the development of AI-optimized data center facilities. Countries such as Sweden, Norway, and Finland are establishing themselves as key locations for the growth of data centers throughout the Nordic region.

- In 2025, Sweden held the largest hyperscale data center power capacity in the Europe data center market. The Swedish government is investing significantly in developing Artificial Intelligence (AI) and digital infrastructure nationwide to enhance the country's digital economy. In May 2025, the Swedish government launched the Digitalization Strategy 2025-2030 aimed at enhancing the digital infrastructure of the country.

- Various key markets in Europe, such as the UK, Germany, France, the Netherlands, Ireland, and others are experiencing electricity shortages, making data center firms to focus on developing data centers in emerging markets like Norway, Sweden, Spain, Italy, Finland, Poland, Austria, and others in recent years.

- France has pledged to lower its greenhouse gas emissions by 55% by 2030, to reach carbon neutrality by 2050. Data center operators are working hard to minimize their environmental footprint. In December 2025, the data center operator nLighten entered into a contract with renewable energy firm Axpo to procure renewable energy for nLighten's data center operations in France.

- In Europe, the costs of constructing data centers differ significantly from country to country. Switzerland ranks among the most expensive nations in Europe in terms of data center construction costs. The costs for building data centers in Switzerland, Norway, Sweden, Finland, the UK, and Germany are relatively higher compared to those in France, Portugal, Spain, Italy, Poland, Greece, and various other European nations.

- The Danish Data Center Industry (DDI) is a non-profit entity that represents the complete data center sector in Denmark, encompassing data center operators, technology firms, utility suppliers, local governments, and various industry stakeholders. It seeks to establish Denmark as a prominent location for the development of sustainable data centers. It collaborates closely with government entities, regulators, and policymakers to assist the Danish data center industry.

- In the Netherlands, the Dutch Data Center Association (DDA) manages the expansion of data centers nationwide, promoting companies to develop sustainable data centers to establish the Netherlands as a pivotal hub for digital infrastructure in Europe.

- The Swiss Data Center Association is a prominent association that represents data center operators and ICT firms throughout Switzerland. It serves as a shared platform for the data center sector by assisting data center operators and ICT firms. It collaborates with government and regulatory bodies to advance the development of data centres across Switzerland and enhance the country's digital infrastructure.

- In Austria, data center businesses and tech companies are moving towards sustainability, in line with the country's overall sustainability objectives to reach carbon neutrality by 2040. In Austria, the price of industrial electricity ranges from $0.15 to $0.25 for each kWh

- The Ministry of Digital Development in Russia assists data center firms by providing favourable loans for purchasing locally-produced engineering infrastructure, such as cooling systems, fire suppression technologies, and other elements for data center installation. The Russian government is aiding local companies in developing vital data center equipment domestically to reduce dependence on foreign nations for critical infrastructure.

- Italy comprises roughly eight Special Economic Zones (SEZs) situated in various areas, such as Abruzzo, Campania, Adriatic, Ionian, Calabria, Eastern Sicily, Western Sicily, and Sardinia. These Special Economic Zones provide enterprises in multiple sectors, including data centers, with various advantages such as tax incentives, vital infrastructure including water, power, and connectivity, along with additional benefits to effectively establish and operate their businesses.

EUROPE DATA CENTER MARKET VENDOR LANDSCAPE

- In the Europe data center market, most of the data center investments come from colocation firms. The prominent colocation service providers in Europe include Equinix, Vantage Data Centers, atNorth, Digital Realty, Green Mountain, CyrusOne, AtlasEdge, NTT DATA, Data4, Telehouse, Pure Data Centres Group, Bulk Infrastructure, Iron Mountain, VIRTUS Data Centres, Colt Data Centre Services, Yondr Group, Keppel Data Centres, Global Switch, Borealis Data Center, QTS Data Centers, STACK Infrastructure, maincubes SECURE DATACENTERS, Ark Data Centres, EdgeConneX, and others.

- The Europe data center market consists of a wide range of companies that deliver IT infrastructure for data centers. Some of the important IT infrastructure providers in the European market include Arista Networks, Atos, Broadcom, Cisco, Dell Technologies, Extreme Networks, Fujitsu, Hewlett Packard Enterprise, Hitachi Vantara, Huawei Technologies, IBM, Inspur Group, Lenovo, MiTAC International, NEC Corporation, NetApp, Everpure, Quanta Cloud Technology, Supermicro, Wiwynn, and NVIDIA.

- Numerous new entrants are expanding their presence in the Europe data center sector to meet the increasing demand for data center services throughout European nations. Some of the recent new entrants in the market include Prime Data Centers, Latos Data Centres, DAMAC Digital, GARBE Data Centers, Deep Green, DayOne, Sierra DC, Prologis, Ada Infrastructure, Digital Reef, NXN Datacenters, Compass Datacenters, Portland Trust, Art Data Centres, GreenScale Data Centres, Apto, Corscale Data Centers, Blue Star, EdgeNebula, Apatura, Form8tion Data Centers, Data Center Partners, Asia Pacific Land, FCDC Corp, Greystoke, and others.

- Various cloud and hyperscale data center service providers, including Amazon Web Services (AWS), Alibaba Group, Apple, Google, Meta, Microsoft, and others, are expanding their cloud, Artificial Intelligence, and hyperscale data center service offerings throughout European nations. In March 2026, Amazon Web Services announced its intention to invest about $39.5 billion to expand its service offerings.

- The market comprises various construction firms that focus on providing construction, installation, commissioning, architectural, and engineering services for building data centers throughout European nations. Notable construction contractors in the Europe data center market include Mercury, Arup, Turner & Townsend, Collen Construction, Ramboll, AECOM, PM Group, AtkinsRéalis, DPR Construction, RED Engineering Design, Ethos Engineering, Kirby Group Engineering, Linesight, Fluor Corporation, Bouygues Construction, CapIngelec, Skanska, Eiffage, Designer Group, Gleeds, HDR, McLaren Construction Group, Deerns UK, COWI, Dornan, Sudlows, Future-tech, Hill International, Granlund Group, Colliers, ACS Group, Basler & Hofmann, AEON Engineering, ARC:MC, Ariatta, Astron Buildings, BladeRoom Data Centres, Elecnor Group, Haka Moscow, LPI Group, NORMA Engineering, APL Data Center, 2bm, and others.

- The Europe data center market houses numerous local and international support infrastructure providers, including Schneider Electric, Vertiv, Cummins, ABB, STULZ, Legrand, Carrier, Siemens, Alfa Laval, Eaton, Rolls-Royce, Munters, Rittal, Delta Electronics, Trane, Caterpillar, Socomec Group, Airedale, Hitachi Energy, GE Vernova, Cyber Power Systems, Honeywell, Daikin Applied, Toshiba, Aggreko, ENGIE, Baudouin, INNIO Group, Condair Group, Saft, Mitsubishi Electric, GESAB, Systemair Group, Rehlko, DEIF, HITEC Power Protection, AVK, 3M, Submer, and others that provide power, cooling, and general infrastructure for data centers.

SNAPSHOT

The Europe data center market size by investment will reach USD 148.82 billion by 2031, growing at a CAGR of 16.40% from 2025 to 2031.

The following factors are likely to contribute to the growth of the Europe data center market during the forecast period:

- Rise in Adoption of Liquid Cooling Techniques in Data Centers

- The Surge in Digitalization Fuelling Data Center Demand

- Rise in District Heating Concept

- The Rise in Artificial intelligence Adoption Aiding Data Center Investments

- Increasing sustainability Initiatives among Data Center Operators

Base Year: 2025

Forecast Year: 2026-2031

The study considers the present scenario of the Europe data center market and its market dynamics for 2026−2031. It covers a detailed overview of several market growth enablers, restraints, and trends. The report offers both the demand and supply aspects of the market. It profiles and examines leading companies and other prominent ones operating in the market.

Segmentation by Facility Type

- Hyperscale Data Centers

- Colocation Data Centers

- Enterprise Data Centers

Segmentation by Infrastructure

- IT Infrastructure

- Electrical Infrastructure

- Mechanical Infrastructure

- General Construction

Segmentation by IT Infrastructure

- Server Infrastructure

- Storage Infrastructure

- Network Infrastructure

Segmentation by Electrical Infrastructure

- UPS Systems

- Generators

- Transfer Switches & Switchgear

- PDUs

- Other Electrical Infrastructure

Segmentation by Mechanical Infrastructure

- Cooling Systems

- Racks

- Other Mechanical Infrastructure

Segmentation by Cooling Systems

- CRAC & CRAH Units

- Chiller Units

- Cooling Towers, Condensers, and Dry Coolers

- Other Cooling Units

Segmentation by Cooling Techniques

- Air-based

- Liquid-based

Segmentation by General Construction

- Core & Shell Development

- Installation & Commissioning Services

- Engineering & Building Design

- Physical Security

- Fire Detection & Suppression

- DCIM

Segmentation by Tier Standard

- Tier I & II

- Tier III

- Tier IV

Segmentation by Geography

- Western Europe

- UK

- Germany

- France

- Netherlands

- Ireland

- Switzerland

- Italy

- Spain

- Belgium

- Portugal

- Greece

- Other Western European Countries

- Nordics

- Denmark

- Sweden

- Norway

- Finland

- Iceland

- Central & Eastern Europe

- Russia

- Poland

- Austria

- Czechia

- Other Central & Eastern European Countries

Prominent Data Center IT Infrastructure Providers

- Arista Networks

- Atos

- Broadcom

- Cisco

- Dell Technologies

- Extreme Networks

- Fujitsu

- Hewlett Packard Enterprise

- Hitachi Vantara

- Huawei Technologies

- IBM

- Inspur Group

- Lenovo

- MiTAC International

- NEC Corporation

- NetApp

- Everpure

- Quanta Cloud Technology

- Supermicro

- Wiwynn

- NVIDIA

Prominent Support Infrastructure Providers

- 3M

- ABB

- AERMEC

- Aggreko

- Airedale

- Alfa Laval

- Aksa Power Generation

- AVK

- Baudouin

- Carrier

- Caterpillar

- Condair

- Cummins

- Cyber Power Systems

- D’Hondt Thermal Solutions

- Daikin Applied

- Danfoss

- DEIF

- Delta Electronics

- Eaton

- EMICON

- ENGIE

- Enrogen

- GE Vernova

- GESAB

- GRUNDFOS

- Güntner

- HiRef S.p.A

- Hitachi Energy

- HITEC Power Protection

- Honeywell

- INNIO Group

- KyotoCooling

- Legrand

- Mitsubishi Electric

- Munters

- NetNordic Group AS

- Piller Power Systems

- Rehlko

- Rittal

- Rolls-Royce

- Saft

- Schneider Electric

- Siemens

- Socomec

- STULZ

- Submer

- Systermair Group

- Toshiba

- Trane

- Vertiv

- ZIEHL-ABEGG

- Bosch

- FläktGroup

Prominent Data Center Contractors & Subcontractors

- 2bm

- ACIES Civil and Structural

- ACS Group

- AECOM

- AEON Engineering

- Altron

- AODC

- APL Data Center

- ARC:MC

- Arcadis

- Ariatta

- ARSMAGNA

- Artelia

- Arup

- Astron Buildings

- AtkinsRéalis

- Aurora Group

- Basler & Hofmann

- Benthem Crouwel Architects

- BladeRoom Data Centres

- Bouygues Construction

- Bravida

- CapIngelec

- Caverion

- Collen Construction

- Colliers

- Coromatic AB

- COWI

- CREATE Architecture

- CTS Group

- DataDome

- Deerns UK

- Designer Group

- Dipl-Ing.H.C. Höllige

- Dornan

- DPR Construction

- EIDA Solutions

- Eiffage

- Elecnor Group

- Engexpor

- Ethos Engineering

- Ferrovial

- Fluor Corporation

- Flynn

- Future-tech

- Generale Prefabbricati S.p.A.

- Gleeds

- Gottlieb Paludan Architects

- Granlund Group

- Green MDC

- GSE Group

- H&MV Engineering

- Haka Moscow

- Hanley Pepper Consulting Engineers

- HDR

- Hill International

- HOCHTIEF

- ICT Facilities

- IDOM

- IMOS

- INFINITI IT

- JCA Engineering

- JERLAURE

- John Sisk & Son

- Kirby Group Engineering

- KKCG Group

- Laing O'Rourke

- Linesight

- LPI Group

- M+W Group (Exyte)

- Mace

- Marsh

- McLaren Construction Group

- Metnor Construction

- Mercury

- MiCiM

- MT Højgaard Danmark

- NORMA Engineering

- PM Group

- PORR Group

- PQC

- Quark Unlimited Engineering

- Ramboll

- RED Engineering Design

- Reid Brewin Architects

- Renco

- Rider Levett Bucknall RLB

- RKD

- Rosenberger

- Royal HaskoningDHV

- RWO Associates

- Salboheds

- Skanska

- SPIE

- Starching

- STO Building Group

- STRABAG

- STS Group

- studioNWA

- Sudlows

- Sweco

- Sweet Projects

- Techbau

- Techko

- Tetra Tech

- TPF Ingenierie

- TTSP

- Turner & Townsend

- Warbud

- Winthrop Technologies

- YIT

- ZAUNERGROUP

Data Center Investors

- 3data Premium Data Centers

- P4 Group

- Aire Networks

- Amazon Web Services

- Apple

- AQ Compute

- Ark Data Centres

- Artnet

- Aruba SpA

- AtlasEdge

- Atman

- atNorth

- Atomdata

- Bahnhof

- Beyond.pl

- Borealis Data Center

- Box2Bit

- Bulk Infrastructure

- CapitaLand

- China Mobile International

- CloudHQ

- Colt Data Centre Services

- Conapto

- CyrusOne

- DataCenter United

- DataPro

- DENV-R

- Data4

- Datum Datacentres

- Digital Realty

- Echelon Data Centres

- EcoDataCenter

- EdgeConneX

- Eni

- Equinix

- Etix

- FirstColo

- Global Switch

- Global Technical Realty

- GlobalConnect

- Goodman

- Green

- Green Mountain

- GREYKITE

- Iron Mountain

- IXcellerate

- K2 STRATEGIC

- Kao Data

- Keppel Data Centres

- Kolo DC

- LCL Data Centers

- Lefdal Mine Data Centers

- Linxdatacenter

- Lumen Technologies

- Magnora ASA

- maincubes SECURE DATACENTERS

- Mainova WebHouse

- MERLIN Properties

- Meta

- Microsoft

- MTS

- Nabiax

- Nation Data Center

- nLighten

- NorthC

- NTT DATA

- OpCore

- Orange Business

- Penta Infra

- Portus Data Centers

- Pure Data Centres Group

- QTS Data Centers

- Rostelecom

- Selectel

- Servecentric

- Serverfarm

- STACK Infrastructure

- STACKIT

- Switch Datacenters

- Sparkle

- Telehouse

- Thésée DataCenter

- Telia

- Vantage Data Centers

- Verne

- VIRTUS Data Centres

- Yandex

- Yondr Group

New Entrants

- 1911 Data Centers

- Ada Infrastructure

- Adriatic DC

- AI Pathfinder

- SWI Group

- AmpTank & Greensky Energy

- Anglesey Land Holdings

- Apatura

- Apto

- Arcem

- Argaman Group

- Aroundtown SA

- Art Data Centres

- TechRE Consulting & Ashfield Land

- Asia Pacific Land (APL)

- 3E Network Technology Company

- AVAIO Digital Partners

- Azora

- Bitdeer

- Bilt Technology

- Bitzero Holdings

- Blue Star

- Brookfield

- CGE SA

- Caineal LLP

- Era4

- Claesson & Anderzén AB

- Cegeka

- Compass Datacenters

- Compute Nordic

- Corscale Data Centers

- DAMAC Digital

- Dante Group

- DATA CASTLE

- Data Center Partners

- DATA for MED

- DataHall

- dataR GmbH

- DayOne

- Deep Green

- Digital Reef

- Digital Land & Development

- Domyn

- DL Invest Group

- Drax Group

- ECO-LocaXion

- EDC One

- EdgeNebula

- Edora

- EID LLP

- Elite UK REIT

- Energia Group

- EngineNode

- evroc

- BADEN CLOUD

- FCDC Corp

- FF Ventures

- Firebird.ai

- FlexBase Group

- Form8tion Data Centers

- Fossefall

- Futureal Group

- G42

- GARBE Data Centers

- GreenScale Data Centres

- Greenweaver

- Greystoke

- Grupo Samca

- G.S.M. S.r.l.

- Heim Datacenter

- Herbata

- Hillwood

- House of Data

- ICADE

- IDC Nova

- ILI Group

- Karatzis Group of Companies

- Kauri CAB Digital Infrastructure

- Kennedy Wilson

- Keysource and Namsos DataSenter

- Latos Data Centres

- Liberum Navitas

- Link Park Heathrow

- MSAI - Media StreamAI

- Mistral AI

- NEOEN

- NEOIX

- Nostrum Group

- NETHITS IT SOLUTIONS

- Northtree Investment Management

- Norwich Research Park

- NXN Datacenters

- Origin Energy Services & Woodlands Investment Management

- Osae

- Panattoni

- PATRIZIA SE

- PGIM Real Estate

- Polarise

- Polarnode

- Portland Trust

- Prime Data Centers

- Prologis

- PPC

- REIKNA

- Red Admiral DC

- RheinEnergie AG

- Regant

- SANY Group

- Scale42

- Scranton Enterprises B.V.

- SDC Capital Partners

- SEGRO plc

- Sesterce

- Shelborn

- Sierra DC

- sineQN

- Skygard

- Solano Renovables España

- Solaria Energía y Medio Ambiente

- Stoneshield Capital

- Suomen Energiainsinöörit Oy

- Sunly

- T1 Energy

- Teesworks

- Telis Energie Deutschland

- Thylander

- Tritax Big Box

- Truman Estates

- Unidata

- Valencia Digital Port Connect

- Valore Group

- VALOREM

- VDR

- VITALI SPA Società Benefit

- VSDATA

- WBS Power

- Wilton International

- Winda Energy

- WS Computing AS

- Wycombe Film Studios

- X5 Group

- XTX Markets

EUROPE DATA CENTER MARKET FAQs

How big is the Europe data center market?

What is the growth rate of the Europe data center market?

What is the estimated market size in terms of area in the Europe data center market by 2030?

What are the key trends in the Europe data center market?

How much MW of power capacity is expected to reach the Europe data center market by 2030?

For more details, please reach us at [email protected]

For more details, please reach us at [email protected]

Select a license type that suits your business needs

Single User Licence

- Report accessible by one user only

- Free 10% or 3 days of customization

- Free post-sale service assistance

- Continuous support through email

5 User Licence

- Report accessible by 5 users within the organization

- Free 15% or 4.5 days of customization

- Continuous support through email and telephone

- Free analyst hour

- Free Upgrade: If an updated report published within 180 days of purchase, you will get the revised report free of charge

Corporate Licence

- Free Datasheet worth $1500

- Report accessible by the entire organization

- Free 20% or 6 days of customization

- Free post-sale service assistance

- Continuous support through email and telephone

- Direct access to lead analysts

- Free analyst hour

- Free Upgrade: If an updated report published within 180 days of purchase, you will get the revised report free of charge

Datasheet Licence

- Report accessible by 1 user only

- Free 15% or 32 hours of customization

- Free post-sale service assistance

- Direct access to lead analysts

Frequently Asked Questions

How big is the Europe data center market?

What is the growth rate of the Europe data center market?

What is the estimated market size in terms of area in the Europe data center market by 2030?

What are the key trends in the Europe data center market?

How much MW of power capacity is expected to reach the Europe data center market by 2030?

Other RELATED Reports

Europe Data Center Construction Market – Industry Outlook & Forecast 2026-2031

Published : June 2026

Central & Eastern Europe Data Center Construction Market - Industry Outlook & Forecast 2024-2029

Published : July 2024