Europe HVAC Market Research Report 2026-2031

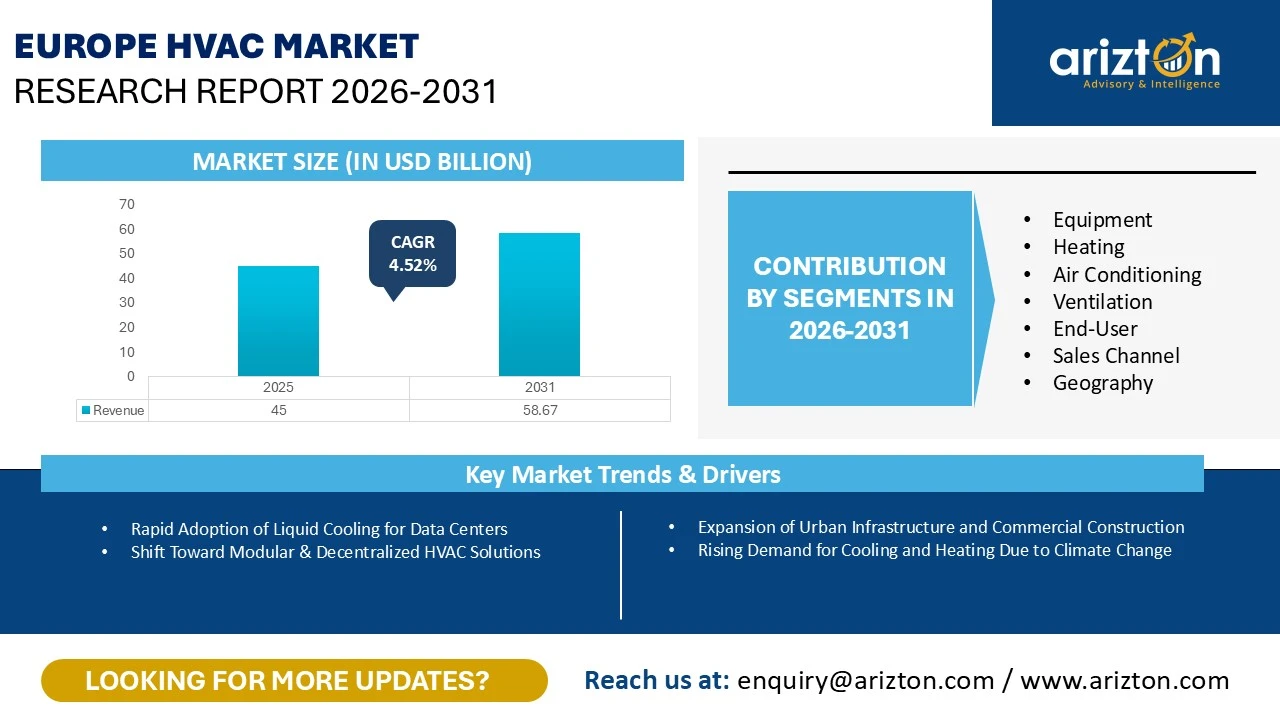

THE EUROPE HVAC MARKET SIZE WAS VALUED AT USD 45 BILLION IN 2025 AND IS EXPECTED TO REACH USD 58.67 BILLION BY 2031, GROWING AT A CAGR OF 4.52% DURING THE FORECAST PERIOD.

Europe HVAC Market Growth Insights – Driven by Steady Construction Activity, Rising Building Renovations, Energy-Efficient HVAC Upgrades, and Growing Demand Across Residential and Non-Residential Infrastructure (2026–2031)

Published Date : June 2026

Last Updated : July 2026

format: PDF

edition : Fifth Edition

223 pages

57 company

7 segments

3 region

23 countries

Purchase Options

Europe HVAC Market Research Report 2026-2031

THE EUROPE HVAC MARKET SIZE WAS VALUED AT USD 45 BILLION IN 2025 AND IS EXPECTED TO REACH USD 58.67 BILLION BY 2031, GROWING AT A CAGR OF 4.52% DURING THE FORECAST PERIOD.

The Europe HVAC Market Size, Share & Trends Analysis Report By

- Equipment: Heating, Air Conditioning, and Ventilation

- Heating: Heat Pumps, Boiler Units, Furnaces, and Other Heating Equipment

- Air Conditioning: RAC, CAC, Chillers, VRF/VRV, and Other Air Conditioning Equipment

- Ventilation: AHU, Fan Coil Units, Humidifiers & Dehumidifiers, and Other Ventilation Equipment

- End-User: Residential, Commercial, And Industrial

- Sales Channel: Distributors & Wholesalers, Dealers & Installers, OEM Direct Sales, And Retail & E-Commerce

- Geography: Western Europe (Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Belgium, Austria, Portugal, Greece, and Ireland), Central & Eastern Europe (Poland, Russia, Czech Republic, Romania, Hungary, Slovakia, and Ukraine), and Nordics (Sweden, Norway, Finland, and Denmark)

Industry Analysis Report, Regional Outlook, Growth Potential, Price Trends, Competitive Market Share & Forecast 2026–2031.

This report includes market data points, ranging from trend

analyses to market estimates & forecasts that you can customize

EUROPE HVAC MARKET REPORT SCOPE

| REPORT ATTRIBUTE | DETAILS |

|---|---|

| MARKET SIZE (2031) | USD 58.67 Billion |

| MARKET SIZE (2025) | USD 45 Billion |

| CAGR (2025-2031) | 4.52% |

| HISTORIC YEAR | 2022-2024 |

| BASE YEAR | 2025 |

| FORECAST YEAR | 2026-2031 |

| SEGMENTS BY | Equipment, Heating, Air Conditioning, Ventilation, End-User, Sales Channel, and Geography |

| GEOGRAPHIC ANALYSIS | Western Europe, Nordic, and Central & Eastern Europe (CEE) |

| KEY PLAYERS | Ariston Group, Groupe Atlantic, BDR Therma Group, Carrier, Robert Bosch, Daikin, Glen Dimplex Group, LG Electronics, Mitsubishi Electric Corporation, NIBE Group, Panasonic Group, Samsung, STIEBEL ELTRON, Trane Technologies, and Vaillant Group |

EUROPE HVAC MARKET SIZE & SHARE

The Europe HVAC market size was valued at USD 45 billion in 2025 and is expected to reach USD 58.67 billion by 2031, growing at a CAGR of 4.52% during the forecast period. The market has evolved as a significant component of the region’s building infrastructure and continues to witness steady growth supported by stable new construction activity along with significant replacement and renovation activity across residential and non-residential buildings.

The rapid growth of real estate and infrastructure projects, specifically in economies such as Germany, France, the UK, Spain, the Netherlands, and Poland, is gradually rising the demand for HVAC systems. For instance, projects such as Amsterdam Schiphol Airport in the Netherlands are set to open a major new Pier A in 2027, representing approximately $1.5 billion of expansion aimed at increasing capacity and improving operational efficiency.

The Europe HVAC market is also witnessing a strong shift as governments across the region encourage building decarbonization and electrification initiatives under the European Green Deal and REPowerEU strategy, which increases the replacement of fossil-fuel-based heating systems with energy-efficient heat pumps and low-emission HVAC technologies, thereby significantly supporting the demand for advanced residential and commercial climate-control systems across Germany, France, Italy, the UK, and Nordic countries.

Recent Product Development in the Europe HVAC market

- In 2025, Daikin launched its EWYK-QZ modular air-to-water heat pump at ISH 2025, designed for commercial/industrial applications using low-GWP R-290 (propane) refrigerant.

Mergers & Acquisitions in the Europe HVAC market

- In 2025, Midea Group and Frigicoll announced a joint venture agreement in Spain and France to establish Midea Frigicoll HVAC Spain and Midea HVAC France, expanding their long-running partnership into a new operating model.

- In 2025, Samsung Electronics acquired a Germany-based leading European HVAC solutions provider, FlaktGroup, from private equity firm Triton for approximately $1.7 billion to strengthen Samsung's position in the global data center and commercial cooling markets.

- In 2025, Bosch Group completed the acquisition of Johnson Controls’ residential and light commercial HVAC business on July 31, 2025, for approximately $8 billion.

EUROPE HVAC MARKET TRENDS & DRIVERS

Growth Of AI-Driven Smart HVAC Ecosystems

The adoption of AI-driven smart HVAC ecosystems is improving operational efficiency and reducing energy consumption. As a result, consumers are significantly shifting towards smart HVAC products, which offer automated controls and optimized energy management. Moreover, to stay competitive in the market, manufacturers are advancing AI and other smart technologies into HVAC equipment architectures to improve product differentiation and energy performance. For instance, Samsung Electronics introduced its Bespoke AI WindFree Pro air-conditioner range at the Mostra Convegno Expocomfort 2026, which features AI Energy Mode, which analyzes user patterns and environmental conditions to reduce power consumption by up to 30%.

Expansion of Urban Infrastructure and Commercial Construction

The rising construction across Europe is gradually supporting the demand for HVAC, as they are one of the crucial components across residential and commercial buildings for ensuring indoor comfort, ventilation, and energy efficiency. For instance, massive projects such as Nantes University Hospital, one of Europe's largest 230,000-square-meter projects, is expected to be completed by the end of 2026, with full operational opening and transfer of activities planned for early to mid-2027, emphasizing the steady expansion of construction activities worldwide, thereby supporting the demand for HVAC systems.

Growth in Renovation and Home Improvement Programs

The rising initiatives for home improvement and renovation activities are substantially supporting the demand for HVAC systems as the ageing building stock accelerates the large-scale replacement and retrofit activities worldwide. For instance, the European Commission’s Renovation Wave Strategy (launched in 2020 and scaled through 2024–2026 implementation phases) aims to double building renovation rates by 2030.

INDUSTRY RESTRAINTS

High Upfront Cost

The high capital requirement significantly slows adoption in price-sensitive European households because it remains a major challenge in the Europe HVAC market, usually for advanced smart systems such as heat pumps and VRF-based heating and cooling solutions. The total installation costs for residential heating equipment are approximately $8,000–$10,000 per unit, depending on system size, efficiency rating and labour cost.

EUROPE HVAC MARKET SEGMENTATION INSIGHTS

INSIGHT BY EQUIPMENT

The Europe HVAC market by equipment is segmented into heating, air conditioning, and ventilation. In 2025, the heating segment accounted for the largest market share of around 50%. There is a strong dependence on space-heating systems across residential and commercial infrastructure in Europe. HVAC manufacturers are increasingly focusing on low-emission heating systems, high-efficiency heat pumps and hybrid heating technologies to align with Europe’s long-term carbon-neutrality targets. For instance, in 2025, Daikin Industries inaugurated a new heat pump production facility in Poland to strengthen regional manufacturing capacity.

Based on the heating, the heat pumps segment accounted for the largest revenue share because of rising decarbonization targets, fossil-fuel boiler replacement, building electrification policies, and rising energy-efficiency requirements across Europe’s residential and commercial heating infrastructure.

Government regulations and policy mandates continue to accelerate heat pump adoption across Europe in 2025. Germany’s Heating Act requires newly installed heating systems to operate using at least 65% renewable energy, significantly increasing demand for air-to-water heat pumps and hybrid heating systems. Multiple European countries are also expanding subsidies, tax rebates, and low-interest financing programs for residential heat pump installations.

INSIGHT BY AIR CONDITIONING

In 2025, the residential air conditioning (RAC) segment accounted for a significant share of the Europe HVAC market. The RAC segment in Europe is witnessing strong demand due to increasing summer temperatures and more frequent heatwaves. Southern Europe leads adoption, while Western and Northern regions are gradually catching up. Historically low AC penetration is changing as cooling becomes essential rather than optional, driving steady growth in residential split and multi-split air conditioning systems across urban households.

Urbanization and growth in apartment-based living are supporting RAC adoption across Europe. Smaller housing units and high-density residential developments create stronger reliance on compact and efficient cooling systems. Split AC systems are preferred due to easy installation and space efficiency. Rising demand from rental housing and real estate developers is further accelerating the penetration of residential air conditioning systems in major European cities.

INSIGHT BY VENTILATION

Based on the ventilation, the air handling units (AHU) segment accounted for the largest Europe HVAC market share. The AHU segment includes commercial, industrial, modular, rooftop, and packaged air-handling units integrated within centralized HVAC systems. These systems combine fans, filters, coils, and dampers to condition and distribute air across buildings. In Europe, AHUs remain critical in offices, hospitals, and airports, ensuring controlled airflow, indoor air quality, and consistent thermal comfort in large-scale infrastructure environments.

AHUs are widely deployed in large commercial and institutional facilities requiring centralized air distribution. In 2025, hospitals in Germany, universities in France, and airports such as Schiphol continue expanding AHU-based systems for zoned airflow management. Their ability to handle high occupancy loads and maintain hygiene standards makes them essential in healthcare, education, and transport infrastructure across Europe.

INSIGHT BY END-USER

Based on end users, the residential segment accounted for the largest share because of the increased demand from new housing construction as well as renovation and replacement activities. HVAC systems in residential buildings such as single-family homes, apartments, condominiums, duplex houses, and residential towers are primarily used to ensure thermal comfort, indoor air quality, and energy efficiency in living spaces, with growing emphasis on sustainability and lifecycle cost optimization.

Additionally, the commercial segment is expected to witness a CAGR of 5.33% during the forecast period. HVAC demand in this segment is driven by the need for large-scale climate control systems that ensure occupant comfort, ventilation efficiency, and compliance with strict indoor environmental and energy performance standards. The increasing adoption of smart building technologies, building automation systems, and energy optimization solutions is further accelerating the deployment of advanced HVAC systems across commercial infrastructure in Europe.

INSIGHT BY SALES CHANNEL

The Europe HVAC market by sales channel is segregated into distributors & wholesalers, dealers & installers, OEM direct sales, and retail & e-commerce. The distributors & wholesalers accounted for the largest market share in 2025, supported by their extensive regional supply networks, strong relationships with contractors, and ability to provide a wide portfolio of HVAC equipment, spare parts, and aftermarket services across Europe. These channels play a critical role in ensuring product availability and timely delivery for residential, commercial, and industrial projects.

Additionally, distributors are becoming increasingly important in supporting Europe’s decarbonization and retrofit initiatives by ensuring faster product delivery and localized service coverage. Large distributor networks help manufacturers respond efficiently to rising demand for heat pumps and low-emission HVAC solutions across residential renovation and commercial modernization projects throughout Germany, France, Italy, and the Nordics.

EUROPE HVAC MARKET GEOGRAPHICAL ANALYSIS

In 2025, Western and Southern Europe are the largest market for the Europe HVAC, accounting for more than 53%. Western and Southern Europe market is driven by strong residential and commercial construction activity, high air-conditioning penetration in Southern Europe, a large installed boiler replacement base, and rapid adoption of heat pumps and energy-efficient HVAC systems across Germany, France, Italy, Spain, and the UK.

The Central and Eastern Europe region is the second-largest market, and Poland dominates the market across the region and accounts for a significant revenue share in 2025, characterized by a strong mix of replacement-driven residential demand and cyclical new construction activities. Moreover, the Nordics is the fastest-growing segment of the Europe HVAC market, supported by the rising hospitality development activities, which are also contributing to incremental HVAC demand across the Nordic region. For instance, hospitality brands are expanding into Sweden through new property openings planned by 2027, reflecting continued investment in premium tourism infrastructure.

EUROPE HVAC MARKET COMPETITIVE LANDSCAPE

The Europe HVAC market is a mature yet rapidly evolving industry, characterized by the presence of multinational HVAC manufacturers, regional heating specialists, and ventilation-focused engineering companies competing across residential, commercial, and industrial applications.

Leading manufacturers such as Daikin, Mitsubishi Electric, Panasonic, LG Electronics, Trane Technologies, and Samsung HVAC maintain strong positions across Europe through broad product portfolios, advanced inverter and heat pump technologies, and extensive distribution and service networks. These companies compete primarily on energy-efficient HVAC systems, VRF technologies, smart controls, and low-GWP refrigerant adoption. For instance, Daikin continues to strengthen its European heat pump manufacturing and R&D footprint, while Panasonic maintains a strong market presence in high-efficiency residential and commercial HVAC systems.

SNAPSHOT

The Europe HVAC market size is expected to grow at a CAGR of approximately 4.52% from 2025 to 2031.

The following factors are likely to contribute to the growth of the Europe HVAC market during the forecast period:

- Expansion of Urban Infrastructure and Commercial Construction

- Rising Demand for Cooling and Heating Due to Climate Change

- Growth in Renovation and Home Improvement Programs

- Implementation of Strict EU Energy and F-Gas Regulations

- Increase in Government Subsidies and Green Financing Programs

Base Year: 2025

Forecast Year: 2026-2031

The report examines the current state of the Europe HVAC market and its market dynamics through 2026−2031. It covers a detailed overview of several market growth enablers, restraints, and trends. The study covers both the demand and supply sides of the market. It also profiles and analyses leading companies and several other prominent companies operating in the market.

Key Vendors

- Ariston Group

- Business Overview

- Product Offerings

- Key Developments

- Key Strategies

- Key Strengths

- Key Opportunities

- Groupe Atlantic

- BDR Therma Group

- Carrier

- Robert Bosch

- Daikin

- Glen Dimplex Group

- LG Electronics

- Mitsubishi Electric Corporation

- NIBE Group

- Panasonic Group

- Samsung

- STIEBEL ELTRON

- Trane Technologies

- Vaillant Group

Other Prominent Vendors

- Aldes

- Business Overview

- Product Offerings

- Alfa Laval

- Biddle Air Systems

- Camfil

- CIAT

- Elco Bruners

- Ferroli

- Gree Electric Appliances, INC.

- LFB Group

- Hisense HVAC

- Midea Group

- Nuaire

- Ostberg

- Riello Group

- Soler & Palau (S&P)

- Swegon

- Trox GMBH

- Clivet

- Vent-Axia

- VTS Group

- Wolf GMBH

- Zehnder Group AG

- Haier HVAC Solutions

- Modine HVAC

- Blue Star Europe B.V.

- H.Stars Group

- GENERAL HVAC Solutions Euro GMBH

- Baxi

- Brink Climate Systems

- Brotje

- Thermoscreens

- Powrmatic

- CoolTherm

- Chiller LTD.

- Dogu Iklimlendirme

- FlowAir

- Cooper&Hunter

- Frico

- Galletti

- HiRef

- Inventor

- Imbat

Segmentation by Equipment

- Heating

- Air Conditioning

- Ventilation

Segmentation by Heating

- Heat Pumps

- Boiler Units

- Furnaces

- Other Heating Equipment

Segmentation by Air Conditioning

- RAC

- CAC

- Chillers

- VRF/VRV

- Other Air Conditioning Equipment

Segmentation by Ventilation

- AHU

- Fan Coil Units

- Humidifiers & Dehumidifiers

- Other Ventilation Equipment

Segmentation by End-User

- Residential

- Commercial

- Industrial

Segmentation by Sales Channel

- Distributors & Wholesalers

- Dealers & Installers

- OEM Direct Sales

- Retail & E-Commerce

Segmentation by Geography

Western Europe

- Germany

- France

- UK

- Italy

- Spain

- Netherlands

- Switzerland

- Belgium

- Austria

- Portugal

- Greece

- Ireland

Central & Eastern Europe

- Poland

- Russia

- Czech Republic

- Romania

- Hungary

- Slovakia

- Ukraine

Nordics

- Sweden

- Norway

- Finland

- Denmark

EUROPE HVAC MARKET FAQs

How big is the Europe HVAC market?

What is the growth rate of the Europe HVAC market?

Who are the major players in the Europe HVAC market?

What are the key trends in the Europe HVAC market?

Which region dominates the Europe HVAC market?

For more details, please reach us at [email protected]

Chapter 1- Scope & Coverage

MARKET DEFINITION

- INCLUSION

- EXCLUSIONS

- MARKET ESTIMATION CAVEATS

MARKET DERIVATION

- MARKET SEGMENTATION BY EQUIPMENT

- MARKET SEGMENTATION BY HEATING

- MARKET SEGMENTATION BY AIR CONDITIONING

- MARKET SEGMENTATION BY VENTILATION

- MARKET SEGMENTATION BY END-USER

- MARKET SEGMENTATION BY SALES CHANNEL

Chapter 2- Premium Insights

Chapter 3- Market Dynamics

INTRODUCTION

- OVERVIEW

- REGULATIONS & SUSTAINABILITY DRIVE EUROPE HVAC MARKET

- INNOVATION DRIVEN BY REGULATION AND ELECTRIFICATION IN THE EUROPEAN HVAC MARKET

- HEAT PUMP MARKET DYNAMICS IN EUROPE

- PROS AND CONS OF SMART HVAC SYSTEMS

MARKET OPPORTUNITIES & TRENDS

- GROWTH OF AI-DRIVEN SMART HVAC ECOSYSTEMS

- RAPID ADOPTION OF LIQUID COOLING FOR DATA CENTERS

- SHIFT TOWARD LOW-GWP REFRIGERANTS & SUSTAINABLE COOLING TECHNOLOGIES

- SHIFT TOWARD MODULAR & DECENTRALIZED HVAC SOLUTIONS

- SURGE IN VRF & HIGH-EFFICIENCY HVAC TECHNOLOGIES

MARKET GROWTH ENABLERS

- EXPANSION OF URBAN INFRASTRUCTURE AND COMMERCIAL CONSTRUCTION

- RISING DEMAND FOR COOLING AND HEATING DUE TO CLIMATE CHANGE

- GROWTH IN RENOVATION AND HOME IMPROVEMENT PROGRAMS

- IMPLEMENTATION OF STRICT EU ENERGY AND F-GAS REGULATIONS

- INCREASE IN GOVERNMENT SUBSIDIES AND GREEN FINANCING PROGRAMS

MARKET RESTRAINTS

- HIGH UPFRONT EXPENDITURE

- SUPPLY-CHAIN INFLATION PRESSURES PROFITABILITY

- SHORTAGE OF SKILLED WORKFORCE

- OEM RE-TOOLING PRESSURE FROM REFRIGERANT TRANSITION UNCERTAINTY

MARKET LANDSCAPE

- MARKET OVERVIEW

- MARKET SIZE & FORECAST

- FIVE FORCES ANALYSIS

- VALUE CHAIN ANALYSIS

CHAPTER 4- MARKET SEGMENTATION

EQUIPMENT (MARKET SIZE & FORECAST: 2022-2031)

- HEATING

- AIR CONDITIONING

- VENTILATION

HEATING (MARKET SIZE & FORECAST: 2022-2031)

- HEAT PUMPS

- BOILER UNITS

- FURNACES

- OTHER HEATING EQUIPMENT

AIR CONDITIONING (MARKET SIZE & FORECAST: 2022-2031)

- RAC

- CAC

- CHILLERS

- VRF/VRV

- OTHER AIR CODITIONING EQUIPMENT

VENTILATION (MARKET SIZE & FORECAST: 2022-2031)

- AHU

- FAN COIL UNITS

- HUMIDIFIERS & DEHUMIDIFIERS

- OTHER VENTILATION EQUIPMENT

END-USER (MARKET SIZE & FORECAST: 2022-2031)

- RESIDENTIAL

- COMMERCIAL

- INDUSTRIAL

SALES CHANNEL (MARKET SIZE & FORECAST: 2022-2031)

- DISTRIBUTOS & WHOLESALERS

- DEALERS & INSTALLERS

- OEM DIRECT SALES

- RETAIL & E-COMMERCE

CHAPTER 5- GEOGRAPHY SEGMENTATION

GEOGRAPHY SEGMENTATION (MARKET SIZE & FORECAST: 2022-2031)

WESTERN & SOUTHERN EUROPE

- GERMANY

- FRANCE

- UK

- ITALY

- SPAIN

- NETHERLANDS

- SWITZERLAND

- BELGIUM

- AUSTRIA

- PORTUGAL

- GREECE

- IRELAND

CENTRAL & EASTERN EUROPE

- POLAND

- RUSSIA

- CZECH REPUBLIC

- ROMANIA

- HUNGARY

- SLOVAKIA

- UKRAINE

NORDICS

- SWEDEN

- NORWAY

- FINLAND

- DENMARK

CHAPTER 6- COMPETITIVE LANDSCAPE

COMPETITIVE LANDSCAPE

- COMPETITION OVERVIEW

- RECENT DEVELOPMENTS

- BUYER DECISION FACTORS

- KEY GROWTH STRATEGIES ADOPTED BY HVAC VENDORS

KEY COMPANY PROFILES

OTHER PROMINENT COMPANY PROFILES

REPORT SUMMARY

- KEY TAKEAWAYS

- STRATEGIC RECOMMENDATIONS

Select a license type that suits your business needs

Single User Licence

- Report accessible by one user only

- Free 10% or 3 days of customization

- Free post-sale service assistance

- Continuous support through email

5 User Licence

- Report accessible by 5 users within the organization

- Free 15% or 4.5 days of customization

- Continuous support through email and telephone

- Free analyst hour

- Free Upgrade: If an updated report published within 180 days of purchase, you will get the revised report free of charge

Corporate Licence

- Free Datasheet worth $1500

- Report accessible by the entire organization

- Free 20% or 6 days of customization

- Free post-sale service assistance

- Continuous support through email and telephone

- Direct access to lead analysts

- Free analyst hour

- Free Upgrade: If an updated report published within 180 days of purchase, you will get the revised report free of charge

Datasheet Licence

- Report accessible by 1 user only

- Free 15% or 32 hours of customization

- Free post-sale service assistance

- Direct access to lead analysts

Frequently Asked Questions

How big is the Europe HVAC market?

What is the growth rate of the Europe HVAC market?

Who are the major players in the Europe HVAC market?

What are the key trends in the Europe HVAC market?

Which region dominates the Europe HVAC market?

Other RELATED Reports

Europe HVAC Maintenance and Services Market - Industry Outlook & Forecast 2024-2029

Published : May 2024