Europe Hyperscale Data Center Market – Industry Outlook & Forecast 2026-2031

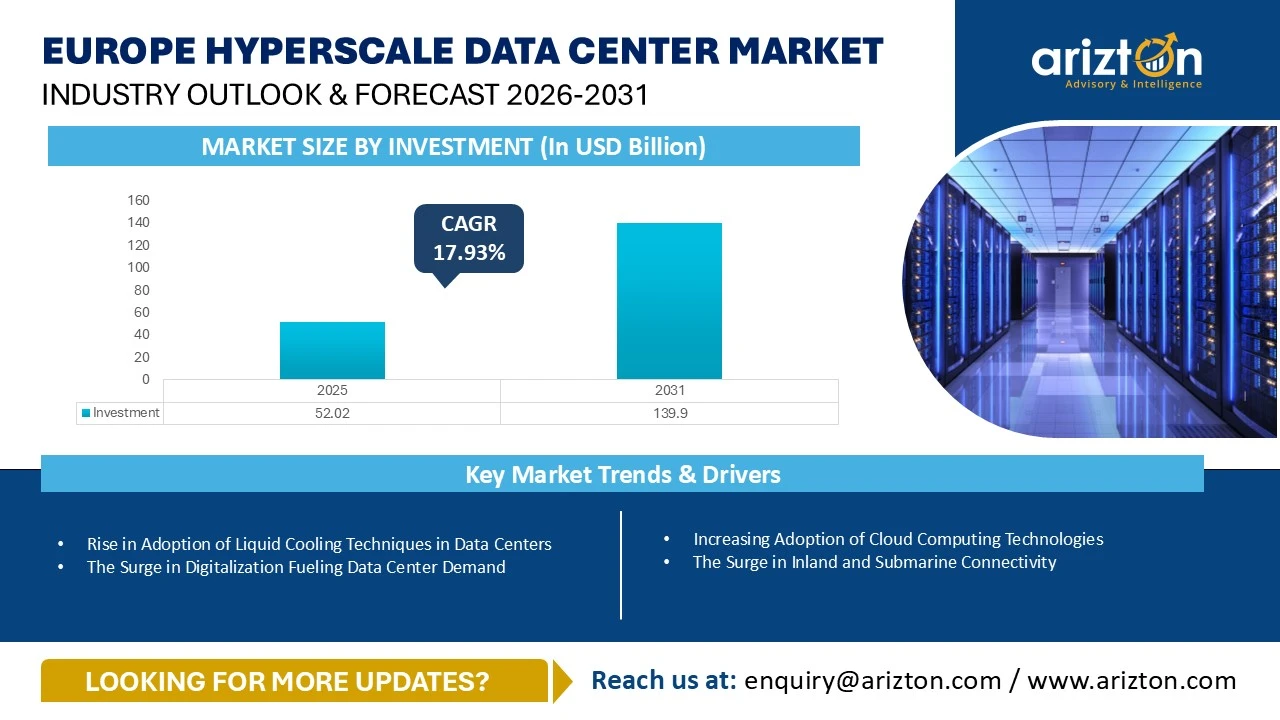

EUROPE HYPERSCALE DATA CENTER MARKET SIZE WITNESSED INVESTMENTS OF USD 52.02 BILLION IN 2025 AND WILL WITNESS INVESTMENTS OF USD 139.90 BILLION BY 2031, GROWING AT A CAGR OF 17.93% DURING 2025-2031.

Europe Hyperscale Data Center Market Growth Insights – Market Area to Reach 14.45 Million Sq. Ft. and Power Capacity to Exceed 3,824 MW by 2031, Driven by AI Adoption, Liquid Cooling, Cloud Expansion, Sustainability Initiatives, District Heating Integration, and Rising Hyperscale Investments Across Europe (2026–2031)

Published Date : July 2026

Last Updated : July 2026

format: PDF

edition : Fourth Edition

453 pages

343 company

9 segments

3 region

15 countries

Purchase Options

Europe Hyperscale Data Center Market – Industry Outlook & Forecast 2026-2031

EUROPE HYPERSCALE DATA CENTER MARKET SIZE WITNESSED INVESTMENTS OF USD 52.02 BILLION IN 2025 AND WILL WITNESS INVESTMENTS OF USD 139.90 BILLION BY 2031, GROWING AT A CAGR OF 17.93% DURING 2025-2031.

The Europe Hyperscale Data Center Market Size, Share, & Trends Analysis By

- Infrastructure: IT Infrastructure, Electrical Infrastructure, Mechanical Infrastructure, and General Construction

- IT Infrastructure: Server Infrastructure, Storage Infrastructure, and Network Infrastructure

- Electrical Infrastructure: UPS Systems, Generators, Transfer Switches & Switchgear, PDUs, and Other Electrical Infrastructure

- Mechanical Infrastructure: Cooling Systems, Racks, and Other Mechanical Infrastructure

- Cooling System: CRAC & CRAH Units, Chiller Units, Cooling Towers, Condensers & Dry Coolers, Economizers & Evaporative Coolers, and Other Cooling Units

- Cooling Technique: Air-based and Liquid-based

- General Construction: Core & Shell Development, Installation & Commissioning Services, Engineering & Building Design, Fire Detection & Suppression, Physical Security, and DCIM/BMS Solutions

- Tier Standards: Tier I & Tier II, Tier III, and Tier IV

- Geography: Western Europe (The U.K., Germany, France, Netherlands, Ireland, Italy, Spain, and Other Western European Countries), Nordics (Denmark, Sweden, Norway, Finland & Iceland), and Central & Eastern European Countries (Russia, Poland, Austria, and Other Central & Eastern European Countries)

Industry Analysis Report, Regional Outlook, Growth Potential, Price Trends, Competitive Market Share & Forecast 2026–2031.

This report includes market data points, ranging from trend

analyses to market estimates & forecasts that you can customize

EUROPE HYPERSCALE DATA CENTER MARKET REPORT SCOPE

| REPORT ATTRIBUTE | DETAILS |

|---|---|

| MARKET SIZE – INVESTMENT (2031) | USD 139.90 Billion |

| MARKET SIZE – INVESTMENT (2025) | USD 52.02 Billion |

| CAGR - INVESTMENT (2025-2031) | 17.93% |

| MARKET SIZE: AREA (2031) | 14.45 million sq. Feet |

| MARKET SIZE: POWER CAPACITY (2031) | 3,824 MW (2031) |

| HISTORIC YEAR | 2022- 2024 |

| BASE YEAR | 2025 |

| FORECAST YEAR | 2026-2031 |

| SEGMENTS BY | Infrastructure, IT Infrastructure, Electrical Infrastructure, Mechanical Infrastructure, Cooling Systems, Cooling Technique, General Construction, Tier Standards, and Geography |

| GEOGRAPHICAL ANALYSIS | Western Europe, Nordics, and Central and Eastern Europe |

EUROPE HYPERSCALE DATA CENTER MARKET SIZE & SHARE

The Europe hyperscale data center market size witnessed investments of USD 52.02 billion in 2025 and will witness investments of USD 139.90 billion by 2031, growing at a CAGR of 17.93% during the forecast period. The investments in the Europe hyperscale data center market are fueled by various growth factors, including, rise in adoption of liquid cooling techniques in data center industry, surge in digitalization, rise in district heating concept, the surge in adoption of artificial intelligence applications, rising sustainability initiatives among data center operators, surge in adoption of cloud-computing technologies, increasing submarine and inland connectivity, rising government support for data centers, advancements in smart city projects, and other factors.

Hyperscale data center investments in the Europe hyperscale data center market have increased by approximately 26%, compared to 2024, and Western Europe contributed around 68.40% of the market’s hyperscale data center investments in 2025, followed by the Nordics and Central and Eastern Europe. Nations like the UK, Germany, France, the Netherlands, and Ireland have strengthened their positions as some of the leading digital hubs in Europe, attracting significant hyperscale data center investments; among these countries, the FLAP-D market (Frankfurt, London, Amsterdam, Paris, and Dublin) has established itself as a primary destination for hyperscale data center developments.

Owing to the concentration in hyperscale data center developments across the FLAP-D markets, these cities are witnessing a shortage of industrial electricity availability, forcing data center operators to prioritize secondary locations for the development of hyperscale data centers. However, to address the rising demand for digitalization across primary European locations, the governments are establishing Free Trade Zones, Special Economic Zones, and industrial parks to support hyperscale data center development across the primary markets.

Additionally, the secondary markets, including Italy, Spain, Belgium, Portugal, Greece, Norway, Sweden, Denmark, Finland, Iceland, Poland, Austria, and others, are gaining strong momentum for the development of hyperscale data centers across Europe in recent years. Western European countries like Italy, Spain, Belgium, Portugal, Greece, and others are establishing dedicated Artificial Intelligence strategies and digitalization roadmaps to enhance their digital ecosystem, which is slated to significantly increase the demand for digital infrastructure across these countries during the forecast period. Data center operators are increasingly investing in the Nordic region as the Nordic countries provide companies with abundant electricity at affordable prices, and the natural climate across Nordic nations provides an option for free cooling, supporting hyperscalers to minimize their operational costs.

Additionally, the Nordic countries are making substantial efforts to position the region as one among the leading AI hubs in Europe, rising the demand for data center infrastructure across the Nordic countries. The Central and Eastern European countries feature abundant vacant land availability, attracting hyperscalers with lower land prices for the development of hyperscale data centers. The countries including Russia, Poland, and Austria have established themselves as major destinations for hyperscale data center development.

EUROPE HYPERSCALE DATA CENTER MARKET TRENDS

Rising Adoption of Liquid Cooling Techniques in Data Centers

- In the Europe data center industry, the hyperscalers are significantly investing to adopt advanced liquid cooling techniques in their data centers. The multi-gigawatt hyperscale data centers consist of multiple thousands of servers and high-density racks to efficiently process complex Artificial Intelligence (AI) and high-performance computing (HPC) workloads. These units contribute vast amounts of heat, which cannot be handled by traditional air-based cooling techniques. The traditional cooling techniques get strained to manage vast heat, increasing the need for advanced liquid cooling techniques.

- In June 2025, the data center operator, Global Switch, installed advanced liquid cooling techniques, including a single-phase immersion cooling technique, a two-phase immersion cooling technique, as well as a direct-to-chip liquid cooling technique in Global Switch's London East Docklands data center campus.

- The surge in demand for dissipating large amounts of heat generated in hyperscale data centers across European countries, owing to the rising need for processing Artificial Intelligence (AI) and high-performance computing (HPC) workloads, is increasing the need for advanced liquid cooling techniques including immersion cooling and direct-to-chip liquid cooling. The hyperscalers across the European countries are anticipated to invest significantly in installing liquid cooling techniques in their hyperscale data centers during the forecast period.

The Surge in Digitalization Fuelling Data Center Demand

- The European countries, including the UK, Germany, France, Netherlands, Ireland, Spain, Norway, Sweden, Finland, Poland, among others, are consistently witnessing a rapid surge in digitalization as the businesses across wide range of sectors, including, retail, transport, education, government, finance, and others, are investing in digital technologies to enhance their operational efficiency and service offerings.

- In January 2026, the UK-based bank, namely, the Bank of England, partnered with multiple technology firms, such as Accenture, Cognizant, Capgemini, among others, by signing multiple agreements, worth around $243 million, to boost the Bank of England’s digital transformation and digital service offerings.

- The rapid surge in digitalization across European countries is anticipated to drive the requirement for the development of multiple edge data centers across the European nations, thereby increasing the need for hyperscale data centers to support multiple edge facilities across the region, and to collect, store, and process data closer to end users, to deliver high-speed, low-latency, and real-time digital services.

Rise in District Heating Concept

- Among the European countries, the hyperscalers are increasingly investing to connect their data centers to district heating systems. District heating is an innovative method to repurpose the waste heat generated in data centers. The hyperscale data centers consume huge amounts of power and generate large volumes of heat, which was expelled into the atmosphere in previous years. Currently, most of the hyperscale operators in Europe are prioritizing reusing the waste heat generated in data centers by connecting the facilities to district heating systems.

- In August 2025, the Nordic data center operator, Borealis Data Center, partnered with Loiste Lämpö Oy, the Finnish public utility firm, to capture and repurpose the waste heat generated in Borealis Data Center's data center campus in Kajaani, Finland. The company aims to supply the waste heat to nearby homes and businesses in the Kajaani region for recycling purposes.

- In the European hyperscale data center market, the integration of district heating systems is likely to increase significantly over the next three to five years as the hyperscalers are increasingly focusing on enhancing sustainability across their data centers.

The Rise in Artificial Intelligence Adoption Aiding Data Center Investments

- In European countries, companies across multiple sectors, such as finance, education, government, healthcare, retail, manufacturing, transport, e-commerce, among others, are increasingly investing to adopt Artificial Intelligence (AI) technologies to enhance productivity, digital service offerings, boost operational efficiency, and drive innovation.

- In October 2025, the Italian government revealed that the country has become the first country in the European Union (EU) to establish Artificial Intelligence (AI) law. The law mainly aims to focus on regulating the usage of Artificial Intelligence across various sectors, including finance, healthcare, government, and others, to ensure transparency and security in Artificial Intelligence applications.

- Artificial Intelligence (AI)-optimized data centers require numerous advanced servers and graphics processing units (GPUs) to maintain huge volumes of data and to process complex workloads efficiently; these servers generate significant volumes of heat, rising the requirement for advanced liquid cooling techniques. The surge in adoption of Artificial Intelligence among enterprises across various sectors in the European countries is anticipated to drive the demand for liquid cooling techniques during the forecast period.

Increasing Sustainability Initiatives among Data Center Operators

- The hyperscalers and cloud companies across the European nations are increasingly investing to adopt sustainability practices to reduce carbon impact, greenhouse gas emissions, and environmental effects of their large-scale hyperscale data centers, aligning with the region's broader sustainability objectives to minimize carbon emissions and environmental impact.

- Several hyperscalers are increasingly collaborating with renewable energy suppliers to procure clean, green, and renewable energy to boost sustainable data center operations across European countries. For example, in March 2025, the data center firm Telehouse collaborated with a renewable energy supplier, RWE Group, by signing a 10-year Power Purchase Agreement (PPA) to source wind energy from RWE Group's London Array wind farm in the UK to power Telehouse's London Docklands data center campus.

- The adoption of sustainability practices among the hyperscalers and cloud operators is likely to reduce operational expenses of data centers and reduce greenhouse gas emissions and their carbon footprint. Therefore, the adoption of sustainability practices by hyperscalers and data center operators is anticipated to further increase over the next three to five years in the European data center industry.

Increasing Adoption of Cloud Computing Technologies

- European nations are witnessing a significant surge in the demand for cloud computing services in recent years, driven by increasing digitalization, deployment of 5G connectivity, stringent data regulation practices, advancements in digital technologies, and other factors.

- In July 2025, the cloud services provider, Oracle, revealed its plans to invest approximately $3 billion to enhance Germany’s cloud and Artificial Intelligence infrastructure. The company also aims to expand its existing cloud region in Frankfurt to boost sovereign cloud and Artificial Intelligence service offerings in Germany as part of this investment.

- The surge in adoption of cloud-computing services among enterprises across various sectors in European nations is likely to increase the need for hyperscale data centers across the region over the next three to five years, as the cloud companies demand scalable and low-latency infrastructure to deliver high-speed cloud computing services.

The Surge in Inland and Submarine Cable Connectivity

- European countries are increasingly investing to enhance their digital infrastructure to remain competitive in the digital landscape. The advancements in submarine cable and fiber-optic cable infrastructure play a critical role in boosting data transmission speeds and cross-border connectivity of European countries with other countries worldwide to address the increasing need for cloud computing, Artificial Intelligence, and digitalization across European countries.

- In November 2025, Altibox Carrier, the connectivity and data services provider, planned to develop a new submarine cable, namely, the Verena subsea cable, which is likely to span approximately 391 miles to boost data transmission speeds and digital connectivity between Denmark and the UK.

- The surge in the deployment of submarine cable connectivity across European countries is likely to further rise over the next two to three years, and the deployment of submarine cable and fiber-optic cable infrastructure is crucial to address the rising need for cloud-computing services, digital transformation, and high-speed internet across the European countries, leading to a rise in demand for hyperscale data center infrastructure across the region.

Increasing Government Support for Data Centers

- The governments across the European countries have understood the significance of hyperscale data center infrastructure to boost Europe's digital economy and advance the technological landscape. Therefore, the European governments are establishing various policies, initiatives, and strategies to support hyperscalers in developing large-scale, multi-gigawatt hyperscale data centers across several locations of the region, while focusing on sustainability.

- In January 2026, the government of the UK invested approximately $283.7 million to launch a new cyber strategy to enhance the security of digital public service offerings and boost the nation's digital infrastructure by strengthening digital security against potential cyber threats in the country.

- The government support for data centers is anticipated to increase during the forecast period as the demand for digital infrastructure is rising significantly across European countries. The governments across various European countries are likely to introduce several new strategies to drive sustainable hyperscale data center development over the next three to five years by encouraging partnerships among data center operators, technology companies, sustainability service providers, and digital infrastructure investment companies. The European nations are likely to experience significant hyperscale data center investments from local and global data center firms during the forecast period.

Advancements in Smart City Initiatives, Big Data, & IoT

- In recent years, the advancements in smart city projects have led to a rise in demand for hyperscale data center infrastructure across the European countries. The development of smart cities generates vast volumes of real-time data to deliver efficient digital public services, optimize traffic management, increase sustainability, and promote urbanization, increasing the need for data center infrastructure to collect, store, and process real-time data to deliver high-speed, low-latency digital services. Additionally, the shift towards digitalization is also increasing the need for emerging technologies like Internet of Things and big data across the European nations.

- In June 2025, the UK-based IoT solutions provider, Kigen, secured funding from SBI Group, the financial services provider, to build advanced large-scale IoT models to boost industrial IoT service offerings across the country.

- The advancements in smart city initiatives and emerging technologies such as big data and Internet of Things play a crucial role in driving Europe's digital landscape, and these advancements are leading to an increase in demand for hyperscale data center infrastructure throughout the region.

EUROPE HYPERSCALE DATA CENTER MARKET SEGMENTATION INSIGHTS

- The hyperscalers and data center operators are prioritizing the installation of advanced graphics processing units (GPUs) and innovative servers in hyperscale data centers to process complex Artificial Intelligence and high-computing workloads. The rising digitalization and surge in adoption of cloud computing and artificial intelligence, along with the deployment of 5G connectivity and rising internet penetration across European countries, are likely to increase the demand for innovative servers across European data centers.

- In the Europe hyperscale data center market, several data center operators are investing in high-performance NVMe and flash storage systems to boost data center performance, storage capacity, and address the demand for high-performance computing. Although some companies still rely on traditional HDDs.

- In recent years, multiple hyperscalers across the Europe data center industry are prioritizing the adoption of high-bandwidth switch ports, which can deliver capacity of approximately 100 GbE. The surge in deployment of 5G connectivity is likely to increase the need for high-bandwidth networking infrastructure, which can deliver capacity of over 400 GbE over the next three to five years.

- As the demand for sustainable digital infrastructure is rising across European countries, the hyperscalers and data center operators are prioritizing investments in installing sustainable power and cooling infrastructure in their facilities. For example, the companies are focusing on replacing lead-acid batteries in the UPS systems with sustainable lithium-ion batteries to reduce the carbon footprint.

- The adoption of sustainable generators like the generators, which will be powered with hydrotreated vegetable oil (HVO), is likely to gain momentum across the Europe data center industry over the next five years, owing to the rapid focus on increasing sustainability in data center operations. In October 2025, Telehouse, the data center firm, planned to develop a new data center in London, the UK, that will be installed with hydrotreated vegetable oil-powered backup generators.

- The hyperscalers are making substantial efforts to replace basic PDUs in their data centers with intelligent and advanced PDUs to minimize power consumption and boost energy efficiency in facilities. The adoption of basic PDUs is likely to reduce across European data centers during the forecast period.

- In the Europe hyperscale data center market, hyperscalers are increasingly investing in innovative cooling technologies like adiabatic cooling and free cooling, specifically in the Nordic countries, to minimize power consumption and greenhouse gas emissions in data centers. For example, NTT DATA has invested in installing the free cooling technique in its Vienna 1 data center in Austria to minimize electricity consumption by utilizing natural cold air for cooling purposes without relying on additional cooling infrastructure to dissipate heat generated in the facility.

- The data center operators and hyperscale companies are increasingly investing to install racks, which can offer rack power densities of over 50 kW per rack in their data centers to support advanced GPUs and high-capacity servers. The DEN01 data center operated by atNorth in Copenhagen, Denmark, is equipped with high-density racks, which can deliver rack power capacity ranging between 40 kW and 100 kW per rack.

- Owing to the rapid surge in demand for processing artificial intelligence and high-performance computing workloads, data center companies and hyperscalers are increasingly adopting liquid cooling techniques as traditional air-cooling techniques are not sufficient to dissipate vast volumes of heat generated in hyperscale data centers. Advanced liquid cooling techniques like immersion cooling techniques and direct-to-chip liquid cooling techniques are gaining traction in the Europe hyperscale data center market. For instance, in March 2025, Kao Data planned to build a new data center in the UK that will be installed with the direct-to-chip liquid cooling technique.

- In the Europe hyperscale data center market, the hyperscalers are increasingly investing in innovative fire detection systems and fire suppression systems to protect the facilities against potential fire threats. CyrusOne has invested in installing three-stage fire detection systems, including very early smoke detection apparatus, and double knock gas suppression systems in its FRA3 data center in Frankfurt, Germany, to protect the facility against potential fire threats.

- Installation of DCIM and BMS software in data centers minimizes energy consumption and greenhouse gas emissions, supporting data center firms to minimize operational expenses and environmental impact. VIRTUS Data Centres has invested in installing DCIM software as well as a 24/7 remote hands facility in its Sauderton data center campus.

EUROPE HYPERSCALE DATA CENTER MARKET REGIONAL ANALYSIS

- The UK, Germany, Sweden, and Spain are among the biggest hyperscale data center markets in the European region, that resulted to generate substantial hyperscale data center investments in 2025. The UK contributed approximately 20% of the Europe hyperscale data center investment share in 2025, followed by Germany, Sweden, and Spain. These nations are likely to remain competitive during the forecast period, attracting significant hyperscale data center investments from local and global data center operators.

- In the UK, the costs of constructing data centers vary significantly from one location to another, and Switzerland is likely to be among the most expensive locations in the region, in terms of data center construction costs. The costs of constructing large-scale hyperscale data centers across Switzerland, Norway, the UK, Germany, Finland, and Sweden are comparatively higher than in other European countries like Portugal, Ireland, Spain, Greece, France, and others.

- In the Netherlands, Amsterdam has positioned itself as one of the prominent locations for the development of hyperscale data centers. However, the city's 2019 moratorium halted the development of data centers across the city owing to the rising power, land, and sustainability concerns. The city was experiencing a recovery from the 2019 moratorium post 2023, but a new moratorium, which was introduced in 2025, further restricts the development of large-scale hyperscale data centers across the city, limiting data center operators from land and power. The Netherlands is gradually slated to strengthen its position as one of the prominent data center hubs in Europe over the next five years, owing to the continuous surge in demand for digital services and data center infrastructure across the nation.

- In Switzerland, the Swiss Data Center Association (SDCA) is a prominent entity that represents ICT companies and commercial data center operators across the country. It serves as a unified voice for the data center sector, advocating data center operators' interests with political authorities, standard committees, and regulatory bodies. The entity is responsible for raising awareness regarding the economic and systemic significance of data centers to drive Switzerland’s digital infrastructure.

- In Denmark, the data center sector is represented by a non-profit association, namely, Danish Data Center Industry (DDI), which represents data center operators, utility companies, technology vendors, and other stakeholders in the sector to promote Denmark's position as one of the attractive locations for the development of sustainable data center infrastructure. The association advocates for the interests of data center companies by collaborating with policymakers, regulators, and public authorities to introduce favourable legal frameworks to support data center development across the nation.

- Numerous prominent destinations across Europe, including the UK, Germany, France, the Netherlands, Ireland, and others, are witnessing a scarcity of electricity to support continuous and uninterrupted data center operations, forcing data center operators and hyperscalers to explore secondary markets like Norway, Sweden, Spain, Italy, Finland, Poland, Austria, and others to develop large-scale, multi-gigawatt hyperscale data centers.

- The government of Sweden is introducing various policies and initiatives to boost digitalization and artificial intelligence infrastructure across the country. For example, in May 2025, the Swedish government revealed that it has introduced Sweden’s Digitalisation Strategy 2025–2030 to establish a clear roadmap and directions to reshape the country's digital infrastructure over the next five years.

- Norway is experiencing a gradual surge in Artificial Intelligence (AI) adoption due to the advancements in cloud computing, data analytics, and automation. Therefore, several companies are investing in the development of AI-optimized data centers across the country. In September 2025, ASP Data Center purchased the former Dale factory and crypto mining site in Norway for the development of an AI-ready data center, with an investment of approximately $151 million.

- Finland is known as one of the most favourable business destinations owing to its strategic location between Western Europe and Asia, and the nation offers strong digital connectivity with multiple countries worldwide, through a network of approximately 12 operational submarine cables. The country is witnessing hyperscale data center investments from various data center operators. In January 2026, Prime Data Centers revealed its plans to invest around $2 billion for the development of an AI-ready data center outside Helsinki.

- In Austria, the data center sector is represented by the Austrian Data Center Association (ADCA); the Association was established in 2023, and it is an independent, non‑profit association that collaborates with companies and professionals involved in the design, construction, operation, and management of data centers to promote advanced data center development across the country.

- The UK has the presence of approximately nine Freeports (Free Trade Zones) across diverse locations, such as Humber, Liverpool, Plymouth, Teesside, Thames, among others. The nation also has the presence of around 10 Industrial Strategy Zones (ISZs). Moreover, the country has the presence of around 48 Enterprise Zones, which are located across England, four Enterprise Zones in Scotland, and seven Enterprise Zones in Wales. The UK consists of various industrial parks across multiple cities, including in Manchester, Liverpool, Plymouth, Teesside, among others.

- The French government is increasingly supporting hyperscalers and data center operators to invest in the development of large-scale, multi-gigawatt hyperscale data centers. In February 2025, the French energy company EDF revealed that the company would offer ready-to-use land spaces, which are connected to the electrical grid, for the development of data centers in France

- Zurich has established itself as one of the prominent destinations for the development of hyperscale data centers in Switzerland. The city has the presence of approximately five hyperscale data center facilities, and it is also experiencing the development of around three new hyperscale data centers.

- Italy consists of approximately eight Special Economic Zones (SEZs) across multiple locations, including in Abruzzo, Campania, Adriatic, Ionian, Calabria, Eastern Sicily, Western Sicily, and Sardinia, that offer wide range of advantages like tax incentives, sector-specific growth opportunities, custom duty exemptions, reduced taxes, and other benefits to establish and operate businesses, including data centers across these Special Economic Zones, to promote innovation, and international investment.

- Sweden has set a target of achieving net-zero greenhouse gas emissions by 2045. The country already generates a significant share of its electricity from renewable energy sources, including hydropower, wind, solar, and bioenergy, and aims to transition to a fully renewable electricity system by 2040.

- The Danish Energy Agency oversees and regulates the power sector in Denmark, and the agency operates under the Ministry of Climate, Energy and Utilities. It is responsible for developing and implementing national energy policies and regulations. The country's electricity transmission network is managed by Energinet, the state-owned Transmission System Operator (TSO), which oversees the operation of the high-voltage grid and ensures the reliability and stability of electricity supply.

EUROPE HYPERSCALE DATA CENTER MARKET VENDOR LANDSCAPE

- The prominent data center operators, such as, Amazon Web Services, Apple, AQ Compute, Ark Data Centres, AZUR DATACENTER, Borealis Data Center, Bulk Infrastructure, CloudHQ, Colt Data Centre Services, CyrusOne, Data4, DataPro, Digital Realty, EcoDataCenter, EdgeConneX, Equinix, Global Switch, Goodman, Google, Green Mountain, Iron Mountain, IXcellerate, Kao Data, Lefdal Mine Data Centers, maincubes SECURE DATACENTERS, Meta, Microsoft, Nscale, NTT DATA, Orange Business, Pure Data Centres Group, QTS Data Centers, Rostelecom, STACK Infrastructure, Telehouse, Vantage Data Centers, VIRTUS Data Centres, Yandex, Yondr Group, and other data center companies are investing significantly to develop large-scale hyperscale data center campuses across the European countries.

- The Europe hyperscale data center market has the presence of diverse IT infrastructure companies, which offer core data center infrastructure components including innovative and advanced servers, high-capacity storage systems, as well as networking infrastructure. Some of the prominent IT infrastructure companies operating across European countries include Dell Technologies, Cisco, Hewlett Packard Enterprise, Huawei Technologies, IBM, Lenovo, NVIDIA, Broadcom, Arista Networks, Atos, Fujitsu, NetApp, Supermicro, Extreme Networks, Hitachi Vantara, Inspur Group, MiTAC International, NEC Corporation, Everpure, Quanta Cloud Technology, and Wiwynn, among others.

- The Europe hyperscale data center market is witnessing the entry of several new entrants like 1911 Data Centers, Ada Infrastructure, AI Pathfinder, Apatura, Apto, Argaman Group, Art Data Centres, AVAIO Digital Partners, Bitdeer, Blue Star, Compass Datacenters, Corscale Data Centers, DAMAC Digital, DATA CASTLE, DayOne, Digital Reef, ECO-LocaXion, EngineNode, evroc, Fossefall, G42, GARBE.DC, GreenScale Data Centres, Greystoke, Heim Datacenter, ILI Group, Karatzis Group of Companies, Latos Data Center, Mistral AI, Nostrum Group, Panattoni, PGIM Real Estate, Polarnode, Portland Trust, Prime Data Centers, SANY Group, SEGRO plc, Sierra DC, sineQN, T1 Energy, Tritax Group, XTX Markets, and others.

- The cloud operators and hyperscalers, including, such as Amazon Web Services (AWS), Microsoft, Google, Alibaba Group, Meta, Apple, and other firms, are continuously investing to expand their cloud and Artificial Intelligence infrastructure across European countries by developing numerous hyperscale data centers to collect, store, and process excess data generated by cloud and Artificial Intelligence applications. For instance, in September 2025, the hyperscale giant, Google, invested approximately $6.81 billion to establish a new hyperscale data center in Waltham Cross, Hertfordshire, the UK, to boost the country’s digital capabilities.

- The European region houses numerous construction contractors that provide data center operators and hyperscalers with design, engineering, architectural, commissioning, installation, and construction management services to build large-scale hyperscale data centers. Some of the key data center construction players, operating across European countries, include ACS Group, AECOM, AEON Engineering, ARC:MC, Ariatta, Arup, AtkinsRéalis, BladeRoom Data Centres, Bouygues Construction, Designer Group, Ethos Engineering, Future-tech, Granlund Group, Haka Moscow, Kirby Group Engineering, Linesight, McLaren Construction Group, Mercury, NORMA Engineering, PM Group, Ramboll, RED Engineering Design, Skanska, Sweet Projects, Turner & Townsend, Winthrop Technologies, ZAUNERGROUP, among others.

- The support infrastructure providers, which deliver power, cooling, and general infrastructure components to install in data centers, have a strong presence across European countries. The companies such as ABB, Baudouin, Carrier, Caterpillar, Cummins, Cyber Power Systems, Delta Electronics, Eaton, Hitachi Energy, HITEC Power Protection, Honeywell, Legrand, Mitsubishi Electric, Munters, Rittal, Rolls-Royce, Schneider Electric, Siemens, Socomec, STULZ, Systemair, Toshiba, Trane, Vertiv, among others manufacture and supply support infrastructure components like UPS systems, generators, switches, cooling systems, racks, fire suppression systems, physical security equipment, and other infrastructure components to efficiently support data center operations.

SNAPSHOT

The Europe hyperscale data center market size is expected to grow at a CAGR of approximately 17.93% from 2025 to 2031.

The following factors are likely to contribute to the growth of the Europe hyperscale data center market during the forecast period:

- Increasing Adoption of Cloud Computing Technologies

- The Surge in Inland and Submarine Connectivity

- Increasing Government Support for Data Centers

- Advancements in Smart City Initiatives, Big Data, IoT

Base Year: 2025

Forecast Year: 2026-2031

The report considers the present scenario of the Europe hyperscale data center market and its market dynamics for 2026−2031. It covers a detailed overview of several market growth enablers, restraints, and trends. The study covers both the demand and supply sides of the market. It also profiles and analyzes leading companies and several other prominent companies operating in the market.

The report includes the investment in the following areas:

Segmentation by Infrastructure

- IT Infrastructure

- Electrical Infrastructure

- Mechanical Infrastructure

- General Construction

Segmentation by IT Infrastructure

- Server Infrastructure

- Storage Infrastructure

- Network Infrastructure

Segmentation by Electrical Infrastructure

- UPS Systems

- Generators

- Transfer Switches & Switchgear

- PDUs

- Other Electrical Infrastructure

Segmentation by Mechanical Infrastructure

- Cooling Systems

- Racks

- Other Mechanical Infrastructure

Segmentation by Cooling System

- CRAC & CRAH Units

- Chiller Units

- Cooling Towers, Condensers & Dry Coolers

- Economizers & Evaporative Coolers

- Other Cooling Units

Segmentation by Cooling Technique

- Air-based

- Liquid-based

Segmentation by General Construction

- Core & Shell Development

- Installation & Commissioning Services

- Engineering & Building Design

- Fire Detection & Suppression

- Physical Security

- DCIM/BMS Solutions

Segmentation by Tier Standards

- Tier I & Tier II

- Tier III

- Tier IV

Geography

- Western Europe

- The U.K.

- Germany

- France

- Netherlands

- Ireland

- Italy

- Spain

- Other Western European Countries

- Nordics

- Denmark

- Sweden

- Norway

- Finland & Iceland

- Central & Eastern European Countries

- Russia

- Poland

- Austria

- Other Central & Eastern European Countries

Prominent Data Center IT Infrastructure Providers

- Arista Networks

- Atos

- Broadcom

- Cisco

- Dell Technologies

- Extreme Networks

- Fujitsu

- Hewlett Packard Enterprise

- Hitachi Vantara

- Huawei Technologies

- IBM

- Inspur Group

- Lenovo

- MiTAC International

- NEC Corporation

- NetApp

- Everpure

- Quanta Cloud Technology

- Supermicro

- Wiwynn

- NVIDIA

Prominent Support Infrastructure Providers

- 3M

- ABB

- AERMEC

- Aggreko

- Airedale

- Alfa Laval

- Aksa Power Generation

- AVK

- Baudouin

- Carrier

- Caterpillar

- Condair

- Cummins

- Cyber Power Systems

- D’Hondt Thermal Solutions

- Daikin Applied

- Danfoss

- DEIF

- Delta Electronics

- Eaton

- EMICON

- ENGIE

- Enrogen

- GE Vernova

- GESAB

- GRUNDFOS

- Güntner

- HiRef S.p.A

- Hitachi Energy

- HITEC Power Protection

- Honeywell

- INNIO Group

- KyotoCooling

- Legrand

- Mitsubishi Electric

- Munters

- NetNordic Group AS

- Piller Power Systems

- Rehlko

- Rittal

- Rolls-Royce

- Saft

- Schneider Electric

- Siemens

- Socomec

- STULZ

- Submer

- Systermair Group

- Toshiba

- Trane

- Vertiv

- ZIEHL-ABEGG

- Bosch

- FläktGroup

Prominent Data Center Contractors & Subcontractors

- ACS Group

- AECOM

- AEON Engineering

- AODC

- APL Data Center

- ARC:MC

- Arcadis

- Ariatta

- ARSMAGNA

- Artelia

- Arup

- AtkinsRéalis

- Aurora Group

- Basler & Hofmann

- Benthem Crouwel Architects

- BladeRoom Data Centres

- Bouygues Construction

- Bravida

- CapIngelec

- Collen Construction

- Colliers

- Coromatic AB

- Deerns UK

- Designer Group

- Dipl-Ing.H.C. Höllige

- Dornan

- DPR Construction

- Engexpor

- Ethos Engineering

- Ferrovial

- Fluor Corporation

- Flynn

- Future-tech

- Generale Prefabbricati S.p.A.

- Gottlieb Paludan Architects

- Granlund Group

- Green MDC

- H&MV Engineering

- Haka Moscow

- ICT Facilities

- IDOM

- JCA Engineering

- JERLAURE

- Kirby Group Engineering

- Laing O'Rourke

- Linesight

- LPI Group

- M+W Group (Exyte)

- Mace

- McLaren Construction Group

- Mercury

- Metnor Construction

- MT Højgaard Danmark

- NORMA Engineering

- PM Group

- PQC

- Quark

- Ramboll

- RED Engineering Design

- Reid Brewin Architects

- Renco

- Royal HaskoningDHV

- RWO Associates

- Skanska

- Starching

- STO Building Group

- STRABAG

- STS Group

- studioNWA

- Sweco

- Sweet Projects

- Techbau

- TPF Ingenierie

- TTSP

- Turner & Townsend

- Warbud

- Winthrop Technologies

- YIT

- ZAUNERGROUP

Data Center Investors

- 3data Premium Data Centers

- Amazon Web Services

- Apple

- AQ Compute

- Ark Data Centres

- Aruba SpA

- Asp Data Center

- AtlasEdge

- atNorth

- Atomdata

- AZUR DATACENTER

- Beyond.pl

- Borealis Data Center

- Box2Bit

- Bulk Infrastructure

- CapitaLand

- CloudHQ

- Colt Data Centre Services

- CyrusOne

- Data4

- DataPro

- Digital Realty

- Echelon Data Centres

- EcoDataCenter

- EdgeConneX

- EdgeMode

- Eni

- Equinix

- FirstColo

- Global Switch

- Global Technical Realty

- Goodman

- Green

- Green Mountain

- GREYKITE

- Iron Mountain

- IXcellerate

- JCD Group

- K2 STRATEGIC

- Kao Data

- Kevlinx Data Centers

- LCL Data Centers

- Lefdal Mine Data Centers

- Magnora ASA

- maincubes SECURE DATACENTERS

- Mainova WebHouse

- MERLIN Properties

- Meta

- Microsoft

- Nabiax

- Nebius

- noris network AG

- Nscale

- NTT DATA

- OpCore

- Orange Business

- Penta Infra

- Polcom

- Pure Data Centres Group

- QTS Data Centers

- Rai Way S.p.A.

- Rostelecom

- Selectel

- Serverfarm

- STACK Infrastructure

- Start Campus

- SUB1 Data Centres

- STACKIT

- Switch Datacenters

- Sparkle

- Telehouse

- Telia

- Vantage Data Centers

- Verne

- VIRTUS Data Centres

- Yandex

- Yondr Group

New Entrants

- 1911 Data Centers

- Ada Infrastructure

- Adriatic DC

- AI Pathfinder

- SWI Group

- AmpTank & Greensky Energy

- Anglesey Land Holdings

- Apatura

- Apto

- Arcem

- Argaman Group

- Aroundtown SA

- Art Data Centres

- TechRE Consulting & Ashfield Land

- Asia Pacific Land (APL)

- AVAIO Digital Partners

- Azora

- Bitdeer

- Bitzero Holdings

- Blue Star

- Brookfield

- CGE SA

- Claesson & Anderzén AB

- Compass Datacenters

- Compute Nordic

- Corscale Data Centers

- DAMAC Digital

- DATA CASTLE

- Data Center Partners

- DATA for MED

- DayOne

- Digital Reef

- DL Invest Group

- Drax Group

- ECO-LocaXion

- EDC One

- EID LLP

- Elite UK REIT

- Energia Group

- EngineNode

- Era4

- evroc

- FCDC Corp

- FF Ventures

- Firebird.ai

- FlexBase Group

- Form8tion Data Centers

- Fossefall

- Futureal Group

- G42

- GARBE.DC

- GreenScale Data Centres

- Greenweaver

- Greystoke

- Grupo Samca

- G.S.M. S.r.l.

- Heim Datacenter

- Herbata

- Hillwood

- ICADE

- IDC Nova

- ILI Group

- Karatzis Group of Companies

- Kauri CAB Digital Infrastructure

- Kennedy Wilson

- Latos Data Centres

- Link Park Heathrow

- Mistral AI

- NEOEN

- NEOIX

- Nostrum Group

- Osae

- Panattoni

- PATRIZIA SE

- PGIM Real Estate

- Polarise

- Polarnode

- Portland Trust

- PPC

- Prime Data Centers

- Prologis

- REIKNA

- RheinEnergie AG

- SANY Group

- Scale42

- Scranton Enterprises B.V.

- SDC Capital Partners

- SEGRO plc

- Shelborn

- Sierra DC

- sineQN

- Skygard

- Solano Renovables España

- Solaria Energía y Medio Ambiente

- Stoneshield Capital

- Sunly

- T1 Energy

- Telis Energie Deutschland

- Thylander

- Tritax Big Box

- Unidata

- Valore Group

- VALOREM

- VDR

- VITALI SPA Società Benefit

- WBS Power

- Wilton International

- Winda Energy

- WS Computing AS

- Wycombe Film Studios

- XTX Markets

EUROPE HYPERSCALE DATA CENTER MARKET FAQs

How big is the Europe hyperscale data center market?

What is the growth rate of the Europe hyperscale data center market?

How much MW of power capacity is expected to reach the Europe hyperscale data center market by 2031?

What are the key trends in the Europe hyperscale data center market?

What is the estimated market size in terms of area in the Europe hyperscale data center market by 2031?

For more details, please reach us at [email protected]

For more details, please reach us at [email protected]

Select a license type that suits your business needs

Single User Licence

- Report accessible by one user only

- Free 10% or 3 days of customization

- Free post-sale service assistance

- Continuous support through email

5 User Licence

- Report accessible by 5 users within the organization

- Free 15% or 4.5 days of customization

- Continuous support through email and telephone

- Free analyst hour

- Free Upgrade: If an updated report published within 180 days of purchase, you will get the revised report free of charge

Corporate Licence

- Free Datasheet worth $1500

- Report accessible by the entire organization

- Free 20% or 6 days of customization

- Free post-sale service assistance

- Continuous support through email and telephone

- Direct access to lead analysts

- Free analyst hour

- Free Upgrade: If an updated report published within 180 days of purchase, you will get the revised report free of charge

Datasheet Licence

- Report accessible by 1 user only

- Free 15% or 32 hours of customization

- Free post-sale service assistance

- Direct access to lead analysts

Frequently Asked Questions

How big is the Europe hyperscale data center market?

What is the growth rate of the Europe hyperscale data center market?

How much MW of power capacity is expected to reach the Europe hyperscale data center market by 2031?

What are the key trends in the Europe hyperscale data center market?

What is the estimated market size in terms of area in the Europe hyperscale data center market by 2031?

Other RELATED Reports

Europe Data Center Colocation Market – Industry Outlook & Forecast 2026-2031

Published : July 2026

Europe Data Center Construction Market – Industry Outlook & Forecast 2026-2031

Published : June 2026