Global Hyperscale Data Center Market Landscape 2025-2030

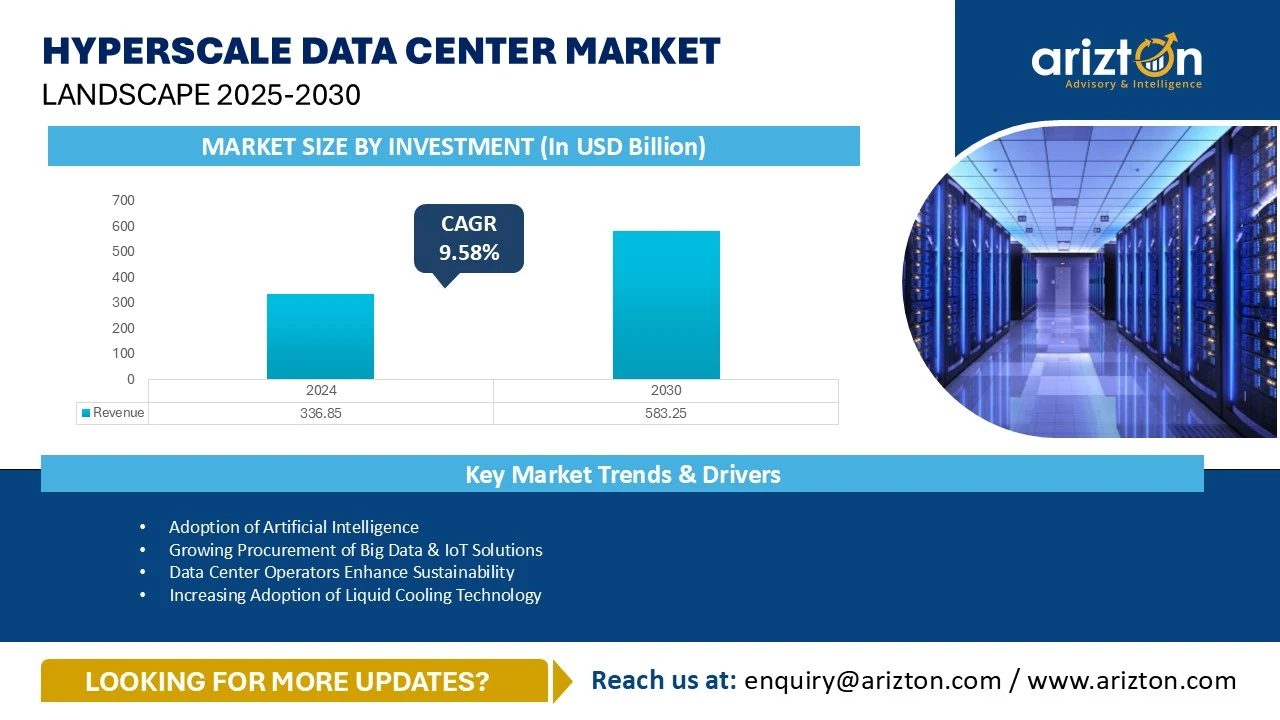

GLOBAL HYPERSCALE DATA CENTER MARKET SIZE WITNESSED INVESTMENTS OF USD 336.85 BILLION IN 2024 AND WILL WITNESS INVESTMENTS OF USD 583.25 BILLION BY 2030, GROWING AT A CAGR OF 9.58% DURING THE FORECAST PERIOD.

Hyperscale Data Center Market Size, Share, Trends Analysis By Infrastructure, IT Infrastructure, Mechanical Infrastructure, Electrical Infrastructure, Cooling Systems, Cooling Technique, General Construction, Tier Standards, & Geography

Published Date : October 2025

Last Updated : October 2025

format: PDF

edition : Second Edition

545 pages

231 company

9 segments

9 region

38 countries

Purchase Options

Global Hyperscale Data Center Market Landscape 2025-2030

GLOBAL HYPERSCALE DATA CENTER MARKET SIZE WITNESSED INVESTMENTS OF USD 336.85 BILLION IN 2024 AND WILL WITNESS INVESTMENTS OF USD 583.25 BILLION BY 2030, GROWING AT A CAGR OF 9.58% DURING THE FORECAST PERIOD.

The Hyperscale Data Center Market Size, Share, & Trends Analysis By

- Infrastructure: IT Infrastructure, Electrical Infrastructure, Mechanical Infrastructure, and General Construction

- IT Infrastructure: Server Infrastructure, Storage Infrastructure, and Network Infrastructure

- Electrical Infrastructure: UPS Systems, Generators, Transfer Switches & Switchgear, PDUs, and Other Electrical Infrastructure

- Mechanical Infrastructure: Cooling Systems, Racks, and Other Mechanical Infrastructure

- Cooling System: CRAC & CRAH Units, Chiller Units, Cooling Towers, Condensers & Dry Coolers, Economizers & Evaporative Coolers, and Other Cooling Units

- Cooling Technique: Air-based and Liquid-based

- General Construction: Core & Shell Development, Installation & Commissioning Services, Engineering & Building Design, Fire Detection & Suppression, Physical Security, and DCIM/BMS Solutions

- Tier Standards: Tier I & Tier II, Tier III, and Tier IV

- Geography: North America, Latin America, Western Europe, Nordics, Central & Eastern Europe, Middle East, Africa, APAC, and Southeast Asia

Industry Analysis Report, Regional Outlook, Growth Potential, Price Trends, Competitive Market Share & Forecast 2025–2030.

This report includes market data points, ranging from trend

analyses to market estimates & forecasts that you can customize

GLOBAL HYPERSCALE DATA CENTER MARKET REPORT SCOPE

| REPORT ATTRIBUTE | DETAILS |

|---|---|

| MARKET SIZE – INVESTMENT (2030) | USD 583.25 Billion |

| MARKET SIZE – INVESTMENT (2024) | USD 336.85 Billion |

| CAGR - INVESTMENT (2023-2029) | 9.58% |

| MARKET SIZE: AREA (2030) | 72 million sq. Feet |

| MARKET SIZE: POWER CAPACITY (2030) | 17,152 MW (2030) |

| HISTORIC YEAR | 2021-2023 |

| BASE YEAR | 2024 |

| FORECAST YEAR | 2025-2030 |

| SEGMENTS BY | Infrastructure, IT Infrastructure, Electrical Infrastructure, Mechanical Infrastructure, Cooling Systems, Cooling Technique, General Construction, Tier Standards, and Geography |

| GEOGRAPHIC ANALYSIS | North America, Latin America, Western Europe, Nordics, Central & Eastern Europe, the Middle East, Africa, APAC, and Southeast Asia |

HYPERSCALE DATA CENTER MARKET SIZE

The global hyperscale data center market size witnessed investments of USD 336.85 billion in 2024 and will witness investments of USD 583.25 billion by 2030, growing at a CAGR of 9.58% during the forecast period. The global hyperscale data center market is experiencing rapid growth, with many large hyperscale facilities being built. This expansion is likely to result in higher energy consumption and carbon emissions. To mitigate this impact, many data center companies are investing in clean, renewable energy to power both their existing and upcoming facilities, helping to minimize their environmental footprint. Furthermore, the global hyperscale data center market is driven by an increase in the deployment of AI workloads across data centers worldwide, triggered by billions of dollars in annual investments from hyperscale operators, including AWS, Apple, Google, Meta (formerly Facebook), Alibaba, Tencent, and Microsoft.

HYPERSCALE DATA CENTER MARKET TRENDS

Adoption of Artificial Intelligence

- Adoption of AI across various industries for enhanced operations has witnessed significant improvement, and it has also increased demand for computing power and advanced data management.

- In May 2024, Microsoft announced that it had signed an MoU with the government to provide an AI-powered future. It also announced that it has constructed a new cloud and AI infrastructure in Thailand.

Growing Procurement of Big Data & IoT Solutions

- The IoT, which connects the digital and physical worlds using a network of sensors, contributes to the fast development of data traffic. Implementing 5G networks for mobile devices will aid the significant growth of IoT and Big data analytics during the forecast period.

- The rapid adoption of IoT across industries, supported by government initiatives and major tech firms, continues to drive efficiency, sustainability, and innovation worldwide. As 5G and AI integration expand, IoT applications will continue to transform sectors like energy, manufacturing, and smart infrastructure.

Increase in Rack Power Density

- The Uptime Institute’s 2024 survey reveals that the average rack density is around 8 kW, driven by high-power server processors and GPU deployments, and some facilities have even deployed rack densities of over 50 kW to 100 kW to support enterprise, colocation, and cloud segments.

- AI, big data, IoT, and cloud computing increase rack densities by requiring more powerful servers and storage systems. These systems pack higher processing and storage capabilities into compact spaces to handle intensive workloads efficiently.

Deployment of Microgrids in Data Centers

- A microgrid is a localized energy grid that can function independently from the traditional power grid. It connects multiple power sources and data centers, collaborating with the primary grid to support various functions.

- In Europe, the growing trend of using microgrids to power data centers, such as the Google data center in Eemshaven, Netherlands, enhances energy independence, resilience, and sustainability.

Increasing Adoption of Liquid Cooling Technology

- The rising use of the internet, digital technologies, AI, and the Internet of Things (IoT) is driving the need for data centers and higher rack power density. As the demand for advanced technology increases, the load on data centers will also increase. With more IT power, the heat generated in these data centers rises. To address this issue, many data centers are turning to liquid-cooling systems as they are more efficient than traditional air-cooling methods. This trend is expected to continue, with the demand for liquid-based cooling systems increasing in the coming years.

- In December 2024, AWS introduced hybrid cooling systems combining air and direct-to-chip liquid cooling to efficiently manage the high power and thermal demands of AI workloads in all its data center facilities, supporting advanced processors like Trainium2 and Nvidia GB200 NVL72.

Data Center Operators Enhance Sustainability

- The rising demand for data centers is leading to an increase in power. To meet this demand, data center operators and the government are adopting green energy. Over the next few years, the demand for green energy is expected to grow, with the government taking steps to ensure its use in data centers across the globe.

- Data center operators are adopting renewable energy in their facilities across the globe. Many data center operators are signing PPA for their facility. For instance, Google signed three major PPAs in India to achieve a carbon-free energy grid. The first PPA was signed with Adani Energy, derived from the Khavda solar-wind hybrid project in Gujarat, offering 30 GW of total capacity for three PPAs, and it is set to be completed by 2026. The second PPA is with CleanMax, with 125.4 MW and 66 MW of solar in Rajasthan and 59.4 MW of onshore wind energy in Karnataka.

Rising Demand for Cloud-based Services

- The adoption of cloud computing services and applications continues to rise rapidly, leading to the establishment of vast hyperscale cloud-based data centers. Cloud computing changes the dynamics of data center facilities, leading to several innovations and the inculcation of modern infrastructure.

- The adoption of cloud-based services is a significant driver for the growth and transformation of data centers. As organizations continue to migrate their operations to the cloud, they get access to several benefits, including enhanced scalability, improved operational efficiency, and access to advanced technologies.

US TARIFF IMPACT ON GLOBAL HYPERSCAL DATA CENTER MARKET

- A trade war refers to an economic conflict in which countries impose tariffs or other trade barriers against each other, typically as a response to similar actions taken by the opposing party. Currently, the world is witnessing the emergence of a global trade war, sparked by the US’s imposition of tariffs on a growing list of countries.

- On April 2, 2025, the US President Donald Trump introduced new tariffs, referred to as reciprocal tariffs, on imports from approximately. 90 countries. Described by the president as “Liberation Day,” the move aims to address the US's trade deficit with countries from China to the EU. The tariffs, which include an across-the-board 10% tax on all imports, mark a significant escalation in the ongoing trade tensions between the US and other countries.

- However, on April 9, 2025, President Trump backtracked on parts of his tariff plan, announcing a 90-day pause on the reciprocal tariffs. Therefore, the general tariff rate was reduced to 10% for most countries. The significant exception remains China, as on April 16, 2025, China faced 245% tariffs on most of its exports to the US, based on the most recent revisions in Trump’s trade policies. China responded with 125% tariffs on US products.

- The recent tariff war has posed a challenge for data center infrastructure, particularly in sourcing raw materials, as increased import and export taxes are expected to raise overall infrastructure costs. For example, the United States has imposed tariffs of around 245% on China, which will increase the cost of equipment imported from China and nearby regions. In response, China has imposed tariffs of around 125% on the United States, which will raise the cost of materials such as electronic equipment that China imports from the U.S.

- The recent increase in tariffs has started to threaten both the rising cost and lead time of data center construction. Some of the construction-related materials that may be impacted include iron and steel, aluminum, and other materials that are crucial to data center development.

HYPERSCALE DATA CENTER MARKET SEGMENTATION INSIGHTS

- The global hyperscale data center market continues to witness significant growth in terms of IT infrastructure investment, with an absolute growth rate of around 190% between 2021 and 2024. In addition, the market is expected to witness significant growth in terms of IT infrastructure, with an absolute growth rate of around 44% between 2025 and 2030.

- The use of advanced technologies, such as cloud, IoT, big data, quantum computing, and AI, by businesses is expected to increase the adoption of HPC infrastructure in the coming years across the globe.

- The global hyperscale data center market continues to witness the adoption of liquid cooling in data centers, which is continuously increasing and is expected to witness an absolute growth rate of 142% between 2025 and 2030.

- Hyperscale operators such as AWS, Google, Meta, and Microsoft are actively developing their data center projects across the globe. These operators focus more on the deployment of OCP-scale infrastructure in their data center facilities. This drives the investments for OCP infrastructure across the globe. For instance, in May 2025, Google announced that it had joined Meta and Microsoft in the "Mount Diablo" project. This project aims to develop a new power rack system that can support data center racks with power density up to 1MW at OCP MEA.

GEOGRAPHICAL ANALYSIS

- In the global hyperscale data center market, the US and China are continuously dominating the market in terms of investment and power capacity. However, there are many countries across the globe witnessing exponential growth due to AI, including countries across APAC, Europe, Latin America, and MEA regions. For instance, the US and China contribute to around 70% of the hyperscale data center investments in 2024.

- In the Global hyperscale data center market, North America dominates in terms of investment and power capacity. This is driven by the increasing demand for AI and the expansion of cloud services across North America, along with favorable regulatory, government support, and power support. However, some areas of North America face some power constraints.

- In North America, the US has contributed the highest market share in terms of investments & power capacity in 2024, followed by Canada.

- APAC is one of the fastest-growing data center markets in terms of investment and power capacity after North America. Over the past two or three years, the region has witnessed an explosion in the demand for digitalization, AI, and cloud computing. The government has taken the initiative to develop proper infrastructure for the data center, which has helped attract global as well as local data center investors to the APAC region. However, some countries within APAC, such as Hong Kong & Singapore, face land and power constraints as well as regulatory & permitting delays.

- In APAC, China dominates the data center market in terms of investment, followed by Malaysia, Australia, Japan, India, Singapore, South Korea, Indonesia, Thailand, Hong Kong, New Zealand, the Philippines, Taiwan, and Vietnam.

- The Malaysian data center market is growing due to the spillover demand from Singapore, and we expect that Malaysia will surpass Singapore's capacity in the next three to four years, owing to the significant rise in investments.

- Europe ranks third in the global hyperscale data center market in terms of investment and power capacity after North America & APAC region. The European region has its own data privacy law and regulatory system, which helps to drive investment in data centers across the European region. Additionally, Europe has strong infrastructure connectivity through land and sea. However, the region also faces some challenges, such as high land and power costs.

- The Middle East & Africa is one of the fastest-growing hyperscale data center markets, ranking fourth globally in terms of investment and power capacity. The MEA region offers ample land, abundant solar and wind renewable energy resources, and government support through Various initiatives and programs.

- South Africa leads in investment in the MEA region, followed by Saudi Arabia, the UAE, Israel, and Kenya.

- Latin America ranks fifth in the global hyperscale data center market in terms of investment and power capacity. Brazil leads in terms of investment, followed by Mexico and Chile.

HYPERSCALE DATA CENTER MARKET VENDOR LANDSCAPE

- The global hyperscale data center market has the presence of IT infrastructure providers such as Arista Networks, Atos, Broadcom, Cisco Systems, DataDirect Networks (DDN), Dell Technologies, Extreme Networks, Fujitsu, Hewlett Packard Enterprise, itachi Vantara, Huawei Technologies, IBM, Infortrend Technology, Inspur, Intel, Lenovo, NetApp, Nimbus Data, NVIDIA, Toshiba, Wiwynn, and others that provide advanced IT infrastructure across the globe.

- Key players in the support infrastructure for the data centers market include 3M, ABB, Airedale, Alfa Laval, Asetek Carrier, Caterpillar, Condair Group, Cummins, Cyber Power Systems, Dakin Applied, Eaton, Generac Power Systems, Green Revolution Cooling, Honeywell, Johnson Controls, Legrand, Rehlko, Rittal, and others.

- The market has a presence of global contractors and subcontractors, such as AECOM, Arup, AtkinsRéalis, Aurecon Group, Basler & Hofmann, Benthem Crouwel Architects, Bouygues Construction, CAP INGELEC, Collen Construction, Corgan, COWI, DPR Construction, DSCO Group, Edarat Group, EMCOR Group, Gensler, HDR Architecture, Turner & Townsend, Sterling and Wilson, and others.

- The increase in hyperscale data center construction is aiding in millions of dollars in revenues from the sector to the major civil contractors and subcontractors in the global hyperscale data center market.

- The market has witnessed new hyperscale data center operators such as 247 Data Centers, Ada Infrastructure, Anan, Apto Data Centre, Beacon AI Centers, Bluestar Data Centre, BW Digital, Colovore, DATA CASTLE, CloudBurst Data Centers, Desert Dragon Data Centers, Digital Reef, Elementica Epoch Digital Evroc, Gatineau Data Hub (GDH), Layer 9 Data Centers, Surfix Data Center, and others.

- Hyperscale operators like Meta (Facebook), Google, Microsoft, AWS, Alibaba, Tencent, and Apple are the major contributors to the global hyperscale data center market in terms of investment & power capacity.

SNAPSHOT

The global hyperscale data center market size is expected to grow at a CAGR of approximately 8.53% from 2024 to 2030.

The following factors are likely to contribute to the growth of the global hyperscale data center market during the forecast period:

- Enhanced Connectivity Through Submarine Cables

- Data Center Investments Backed by Governments

- Renewable Energy Initiatives by Hyperscale & Cloud Operators

Base Year: 2024

Forecast Year: 2025-2030

The report considers the present scenario of the global hyperscale data center market and its market dynamics for 2025−2030. It covers a detailed overview of several market growth enablers, restraints, and trends. The study covers both the demand and supply sides of the market. It also profiles and analyzes leading companies and several other prominent companies operating in the market.

The report includes the investment in the following areas:

Segmentation by Infrastructure

- IT Infrastructure

- Electrical Infrastructure

- Mechanical Infrastructure

- General Construction

Segmentation by IT Infrastructure

- Server Infrastructure

- Storage Infrastructure

- Network Infrastructure

Segmentation by Electrical Infrastructure

- UPS Systems

- Generators

- Transfer Switches & Switchgear

- PDUs

- Other Electrical Infrastructure

Segmentation by Mechanical Infrastructure

- Cooling Systems

- Racks

- Other Mechanical Infrastructure

Segmentation by Cooling System

- CRAC & CRAH Units

- Chiller Units

- Cooling Towers, Condensers & Dry Coolers

- Economizers & Evaporative Coolers

- Other Cooling Units

Segmentation by Cooling Technique

- Air-based

- Liquid-based

Segmentation by General Construction

- Core & Shell Development

- Installation & Commissioning Services

- Engineering & Building Design

- Fire Detection & Suppression

- Physical Security

- DCIM/BMS Solutions

Segmentation by Tier Standards

- Tier I & Tier II

- Tier III

- Tier IV

Segmentation by Geography

- North America

- The U.S.

- Canada

- Latin America

- Brazil

- Mexico

- Chile

- Other Latin American Countries

- Western Europe

- The U.K.

- Germany

- France

- Netherlands

- Ireland

- Italy

- Spain

- Other Western European Countries

- Nordics

- Denmark

- Sweden

- Norway

- Finland & Iceland

- Central & Eastern Europe

- Poland

- Austria

- Other Central & Eastern European Countries

- Middle East

- UAE

- Saudi Arabia

- Israel

- Other Middle East Countries

- Africa

- South Africa

- Kenya

- Other African Countries

- APAC

- China

- Hong Kong

- Australia

- New Zealand

- Japan

- India

- South Korea

- Taiwan

- Southeast Asia

- Singapore

- Indonesia

- Malaysia

- Thailand

- Philippines

- Vietnam

VENDORS LANDSCAPE

IT Infrastructure Provider

- Arista Networks

- Atos

- Broadcom

- Cisco Systems

- DataDirect Networks (DDN)

- Dell Technologies

- Extreme Networks

- Fujitsu

- Hewlett Packard Enterprise

- Hitachi Vantara

- Huawei Technologies

- IBM

- Infortrend Technology

- Inspur

- Intel

- Inventec Data Center Solutions

- Lenovo

- Micron Technology

- MiTAC Holdings

- NEC Corporation

- NetApp

- Nimbus Data

- NVIDIA

- Oracle

- Pure Storage

- QNAP Systems

- Quanta Cloud Technology

- Quantum

- Seagate Technology

- Silk

- Synology

- Toshiba

- Western Digital

- Wiwynn

Data Center Support Infrastructure Providers

- 3M

- ABB

- Airedale

- Alfa Laval

- Asetek

- Asperitas

- Assa Abloy

- Bloom Energy

- Carrier

- Caterpillar

- Condair Group

- CoolIT Systems

- Cormant

- Cummins

- Cyber Power Systems

- Daikin Applied

- DCX LIQUID COOLING SYSTEMS

- Delta Electronics

- Eaton

- Enlogic

- FNT Software

- Generac Power Systems

- GIGABYTE

- Green Revolution Cooling

- HITEC Power Protection

- Honeywell

- Iceotope

- Johnson Controls

- KyotoCooling

- Legrand

- LiquidStack

- Mitsubishi Electric

- Munters

- Natron Energy

- NetZoom

- Nlyte Software

- Panduit

- Pillar Power Systems

- Rehlko

- Rittal

- Rolls-Royce

- Schneider Electric

- Siemens

- STULZ

- Submer

- Trane

- Vertiv

- Yanmar

- ZincFive

Data Center Construction Contractors

- AECOM

- Arup

- AtkinsRéalis

- Aurecon Group

- Basler & Hofmann

- Benthem Crouwel Architects

- Bouygues Construction

- CAP INGELEC

- Collen Construction

- Corgan

- COWI

- DAR

- Deerns

- Dornan

- DPR Construction

- DSCO Group

- Edarat Group

- EMCOR Group

- Ethos Engineering

- EYP Mission Critical Facilities

- Flour Corporation

- Fortis Construction

- Gensler

- Gilbane Building Company

- HDR Architecture

- HITT Contracting

- Hoffmann Construction

- Holder Construction

- ISG

- Jacobs

- Kirby Group Engineering

- Laing O’Rourke

- Larsen & Toubro

- Linesight

- M+W Group (Exyte)

- Mace

- Mercury

- Mortenson

- NTT Facilities

- Quark Unlimited Engineering

- RED Engineering Design

- Haskoning

- Skanska

- STO Building Group

- Syska Hennessy Group

- Sterling and Wilson

- Turner Construction Company

- Structure Tone

- Turner & Townsend

- Winthrop Technologies

Data Center Investors

- AdaniConneX

- Africa Data Centres

- AirTrunk

- Aligned Data Centers

- Apple

- AtNorth

- AWS

- Big Data Exchange (BDx)

- CDC Data Centres

- center3

- Chindata Group

- CloudHQ

- Cologix

- Compass Data Centers

- CoreSite

- CyrusOne

- Data4

- DataBank

- Digital Realty

- EdgeConneX

- Equinix

- Meta (Facebook)

- Flexential

- GDS Services

- Global Switch

- Green Mountain

- Gulf Data Hub

- Iron Mountain

- iXAfrica Data Centre

- Keppel Data Centres

- Khazna Data Centers

- Microsoft

- NEXTDC

- Novva Data Centers

- NTT DATA

- Nxtra by Airtel

- Rostelecom

- Scala Data Centers

- Sify Technologies

- ST Telemedia Global Data Centres

- SUNeVison Holdings

- T5 Data Centers

- Turkcell

- Vantage Data Centers

- Yondr

New Entrants

- 247 Data Centers

- Ada Infrastructure

- Anan

- Apto Data

- Ardent Data Centers

- Beacon AI Centers

- Bluestar Data Centre

- BW Digital

- CloudBurst Data Centers

- Colovore

- Crane Data Centers

- DATA CASTLE

- DataGrid

- DataVolt

- Desert Dragon Data Centers

- Digital Halo

- Digital Reef

- Doma Infrastructure Group

- Eclairion

- Edged Energy

- DAMAC Digital

- Elementica

- Energia Group

- Epoch Digital

- Evolution Data Centres

- Evroc

- Form8tion Data Centers

- Gatineau Data Hub (GDH)

- Gaw Capital

- GreenScale

- GreenSquareDC

- Kasi Cloud

- Latos

- Layer 9 Data Centers

- Mediterra Datacenters

- NE Edge

- PHOCEA DC

- PolarDC

- Prometheus Hyperscale

- Qareeb Data Centres

- Quantum Loophole

- Quetta Data Centers

- Rowan Digital Infrastructure

- Sahayeb Datacenters

- SC Zeus Data Centers

- SDC Capital Partners

- Serverz Data Center

- Surfix Data Center

- Techtonic

- Tract

- Trifalga

- YCO Cloud

GLOBAL HYPERSCALE DATA CENTER MARKET FAQs

How big is the global hyperscale data center market in terms of investments?

Which region holds the most significant global hyperscale data center market share?

What is the estimated market size in terms of area in the global hyperscale data center market by 2030?

How many MW of power capacity is expected to reach the global hyperscale data center market by 2030?

What is the growth rate of the global hyperscale data center market?

For more details, please reach us at [email protected]

1. ABOUT ARIZTON

2. ABOUT OUR DATA CENTER CAPABILITIES

3. WHAT’S INCLUDED

4. SEGMENTS INCLUDED

5. RESEARCH METHODOLOGY

6. MARKET AT GLANCE

7. PREMIUM INSIGHTS

8. IMPACT OF TARIFF ON GLOBAL HYPERSCAL DATA CENTER MARKET

9. INVESTMENT OPPORTUNITIES

9.1. INVESTMENT: MARKET SIZE & FORECAST

9.2. AREA: MARKET SIZE & FORECAST

9.3. POWER CAPACITY: MARKET SIZE & FORECAST

10. MARKET DYNAMICS

10.1. MARKET OPPORTUNITIES & TRENDS

10.2. MARKET GROWTH ENABLERS

10.3. MARKET RESTRAINTS

11. SITE SELECTION CRITERIA

12. INFRASTRUCTURE SEGMENTATION

12.1. IT INFRASTRUCTURE

12.2. ELECTRICAL INFRASTRUCTURE

12.3. MECHANICAL INFRASTRUCTURE

12.4. COOLING SYSTEMS

12.5. COOLING TECHNIQUES

12.6. GENERAL CONSTRUCTION

13. TIER STANDARDS SEGMENTATION

14. GEOGRAPHY SEGMENTATION

15. NORTH AMERICA

15.1. MARKET SNAPSHOT & KEY HIGHLIGHTS

15.2. DATA CENTER MARKET BY INVESTMENT

15.3. DATA CENTER MARKET BY INFRASTRUCTURE

15.4. DATA CENTER MARKET BY AREA

15.5. DATA CENTER MARKET BY POWER CAPACITY

15.6. DATA CENTER MARKET BY SUPPORT INFRASTRUCTURE

15.7. DATA CENTER MARKET BY IT INFRASTRUCTURE

16. US

16.1. INVESTMENT

16.2. MARKET BY INVESTMENT

16.3. AREA

16.4. MARKET BY AREA

16.5. POWER CAPACITY

16.6. MARKET BY POWER CAPACITY

16.7. KEY SUPPORT INFRASTRUCTURE ADOPTION

16.8. MARKET BY INFRASTRUCTURE

16.9. LIST OF UPCOMING DATA CENTER PROJECTS IN THE US

17. CANADA

17.1. INVESTMENT

17.2. MARKET BY INVESTMENT

17.3. AREA

17.4. MARKET BY AREA

17.5. POWER CAPACITY

17.6. MARKET BY POWER CAPACITY

17.7. KEY SUPPORT INFRASTRUCTURE ADOPTION

17.8. MARKET BY INFRASTRUCTURE

17.9. LIST OF UPCOMING DATA CENTER PROJECTS IN CANADA

18. LATIN AMERICA

18.1. MARKET SNAPSHOT & KEY HIGHLIGHTS

18.2. DATA CENTER MARKET BY INVESTMENT

18.3. DATA CENTER MARKET BY INFRASTRUCTURE

18.4. DATA CENTER MARKET BY AREA

18.5. DATA CENTER MARKET BY POWER CAPACITY

18.6. DATA CENTER MARKET BY SUPPORT INFRASTRUCTURE

18.7. DATA CENTER MARKET BY IT INFRASTRUCTURE

18.8. LIST OF UPCOMING DATA CENTER PROJECTS IN LATIN AMERICA

19. BRAZIL

19.1. INVESTMENT

19.2. MARKET BY INVESTMENT

19.3. AREA

19.4. MARKET BY AREA

19.5. POWER CAPACITY

19.6. MARKET BY POWER CAPACITY

19.7. KEY SUPPORT INFRASTRUCTURE ADOPTION

19.8. MARKET BY INFRASTRUCTURE

20. MEXICO

20.1. INVESTMENT

20.2. MARKET BY INVESTMENT

20.3. AREA

20.4. MARKET BY AREA

20.5. POWER CAPACITY

20.6. MARKET BY POWER CAPACITY

20.7. KEY SUPPORT INFRASTRUCTURE ADOPTION

20.8. MARKET BY INFRASTRUCTURE

21. CHILLE

21.1. INVESTMENT

21.2. MARKET BY INVESTMENT

21.3. AREA

21.4. MARKET BY AREA

21.5. POWER CAPACITY

21.6. MARKET BY POWER CAPACITY

21.7. KEY SUPPORT INFRASTRUCTURE ADOPTION

21.8. MARKET BY INFRASTRUCTURE

22. REST OF LATIN AMERICA

22.1. INVESTMENT

22.2. MARKET BY INVESTMENT

22.3. AREA

22.4. MARKET BY AREA

22.5. POWER CAPACITY

22.6. MARKET BY POWER CAPACITY

22.7. KEY SUPPORT INFRASTRUCTURE ADOPTION

22.8. MARKET BY IT INFRASTRUCTURE

23. WESTERN EUROPE

23.1. MARKET SNAPSHOT & KEY HIGHLIGHTS

23.2. DATA CENTER MARKET BY INVESTMENT

23.3. DATA CENTER MARKET BY INFRASTRUCTURE

23.4. DATA CENTER MARKET BY AREA

23.5. DATA CENTER MARKET BY POWER CAPACITY

23.6. DATA CENTER MARKET BY SUPPORT INFRASTRUCTURE

23.7. DATA CENTER MARKET BY IT INFRASTRUCTURE

23.8. LIST OF UPCOMING DATA CENTER PROJECTS IN WESTERN EUROPE

24. UK

24.1. INVESTMENT

24.2. MARKET BY INVESTMENT

24.3. AREA

24.4. MARKET BY AREA

24.5. POWER CAPACITY

24.6. MARKET BY POWER CAPACITY

24.7. KEY SUPPORT INFRASTRUCTURE ADOPTION

24.8. MARKET BY INFRASTRUCTURE

25. GERMANY

25.1. INVESTMENT

25.2. MARKET BY INVESTMENT

25.3. AREA

25.4. MARKET BY AREA

25.5. POWER CAPACITY

25.6. MARKET BY POWER CAPACITY

25.7. KEY SUPPORT INFRASTRUCTURE ADOPTION

25.8. MARKET BY INFRASTRUCTURE

26. FRANCE

26.1. INVESTMENT

26.2. MARKET BY INVESTMENT

26.3. AREA

26.4. MARKET BY AREA

26.5. POWER CAPACITY

26.6. MARKET BY POWER CAPACITY

26.7. KEY SUPPORT INFRASTRUCTURE ADOPTION

26.8. MARKET BY INFRASTRUCTURE

27. NETHERLANDS

27.1. INVESTMENT

27.2. MARKET BY INVESTMENT

27.3. AREA

27.4. MARKET BY AREA

27.5. POWER CAPACITY

27.6. MARKET BY POWER CAPACITY

27.7. KEY SUPPORT INFRASTRUCTURE ADOPTION

27.8. MARKET BY INFRASTRUCTURE

28. IRELAND

28.1. INVESTMENT

28.2. MARKET BY INVESTMENT

28.3. AREA

28.4. MARKET BY AREA

28.5. POWER CAPACITY

28.6. MARKET BY POWER CAPACITY

28.7. KEY SUPPORT INFRASTRUCTURE ADOPTION

28.8. MARKET BY INFRASTRUCTURE

29. ITALY

29.1. INVESTMENT

29.2. MARKET BY INVESTMENT

29.3. AREA

29.4. MARKET BY AREA

29.5. POWER CAPACITY

29.6. MARKET BY POWER CAPACITY

29.7. KEY SUPPORT INFRASTRUCTURE ADOPTION

29.8. MARKET BY INFRASTRUCTURE

30. SPAIN

30.1. MARKET OVERVIEW

31.2. MARKET BY INVESTMENT

31.3. AREA

31.4. MARKET BY AREA

31.5. POWER CAPACITY

31.6. MARKET BY POWER CAPACITY

31.7. KEY SUPPORT INFRASTRUCTURE ADOPTION

31.8. MARKET BY INFRASTRUCTURE

32. OTHER WESTERN EUROPEAN COUNTRIES

32.1. INVESTMENT

32.2. MARKET BY INVESTMENT

32.3. AREA

32.4. MARKET BY AREA

32.5. POWER CAPACITY

32.6. MARKET BY POWER CAPACITY

32.7. KEY SUPPORT INFRASTRUCTURE ADOPTION

32.8. MARKET BY INFRASTRUCTURE

33. NORDIC

33.1. MARKET SNAPSHOT & KEY HIGHLIGHTS

33.2. DATA CENTER MARKET BY INVESTMENT

33.3. DATA CENTER MARKET BY INFRASTRUCTURE

33.4. DATA CENTER MARKET BY AREA

33.5. DATA CENTER MARKET BY POWER CAPACITY

33.6. DATA CENTER MARKET BY SUPPORT INFRASTRUCTURE

33.7. DATA CENTER MARKET BY IT INFRASTRUCTURE

33.8. LIST OF UPCOMING DATA CENTER PROJECTS IN NORDIC

34. DENMARK

34.1. INVESTMENT

34.2. MARKET BY INVESTMENT

34.3. AREA

34.4. MARKET BY AREA

34.5. POWER CAPACITY

34.6. MARKET BY POWER CAPACITY

34.7. KEY SUPPORT INFRASTRUCTURE ADOPTION

34.8. MARKET BY INFRASTRUCTURE

35 SWEDEN

35.1. INVESTMENT

35.2. MARKET BY INVESTMENT

35.3. AREA

35.4. MARKET BY AREA

35.5. POWER CAPACITY

35.6. MARKET BY POWER CAPACITY

35.7. KEY SUPPORT INFRASTRUCTURE ADOPTION

35.8. MARKET BY INFRASTRUCTURE

36. NORWAY

36.1. INVESTMENT

36.2. MARKET BY INVESTMENT

36.3. AREA

36.4. MARKET BY AREA

36.5. POWER CAPACITY

36.6. MARKET BY POWER CAPACITY

36.7. KEY SUPPORT INFRASTRUCTURE ADOPTION

36.8. MARKET BY INFRASTRUCTURE

37. FINLAND & ICELAND

37.1. INVESTMENT

37.2. MARKET BY INVESTMENT

37.3. AREA

37.4. MARKET BY AREA

37.5. POWER CAPACITY

37.6. MARKET BY POWER CAPACITY

37.7. KEY SUPPORT INFRASTRUCTURE ADOPTION

37.8. MARKET BY INFRASTRUCTURE

38. CENTRAL & EASTERN EUROPEAN COUNTRIES

38.1. MARKET SNAPSHOT & KEY HIGHLIGHTS

38.2. DATA CENTER MARKET BY INVESTMENT

38.3. DATA CENTER MARKET BY INFRASTRUCTURE

38.4. DATA CENTER MARKET BY AREA

38.5. DATA CENTER MARKET BY POWER CAPACITY

38.6. DATA CENTER MARKET BY SUPPORT INFRASTRUCTURE

387. DATA CENTER MARKET BY IT INFRASTRUCTURE

38.8. LIST OF UPCOMING DATA CENTER PROJECTS IN CENTRAL & EASTERN EUROPEAN COUNTRIES

39. POLAND

39.1. INVESTMENT

39.2. MARKET BY INVESTMENT

39.3. AREA

39.4. MARKET BY AREA

39.5. POWER CAPACITY

39.6. MARKET BY POWER CAPACITY

39.7. KEY SUPPORT INFRASTRUCTURE ADOPTION

39.8. MARKET BY INFRASTRUCTURE

40. AUSTRIA

40.1. INVESTMENT

40.2. MARKET BY INVESTMENT

40.3. AREA

40.4. MARKET BY AREA

40.5. POWER CAPACITY

40.6. MARKET BY POWER CAPACITY

40.7. KEY SUPPORT INFRASTRUCTURE ADOPTION

40.8. MARKET BY INFRASTRUCTURE

41. OTHER CENTRAL & EASTERN EUROPEAN COUNTRIES

41.1. INVESTMENT

41.2. MARKET BY INVESTMENT

41.3. AREA

41.4. MARKET BY AREA

41.5. POWER CAPACITY

41.6. MARKET BY POWER CAPACITY

41.7. KEY SUPPORT INFRASTRUCTURE ADOPTION

41.8. MARKET BY INFRASTRUCTURE

42. MIDDLE EAST & AFRICA

42.1. MARKET SNAPSHOT & KEY HIGHLIGHTS

42.2. DATA CENTER MARKET BY INVESTMENT

42.3. DATA CENTER MARKET BY INFRASTRUCTURE

42.4. DATA CENTER MARKET BY AREA

42.5. DATA CENTER MARKET BY POWER CAPACITY

42.6. DATA CENTER MARKET BY SUPPORT INFRASTRUCTURE

42.7. DATA CENTER MARKET BY IT INFRASTRUCTURE

42.8. LIST OF UPCOMING DATA CENTER PROJECTS IN THE MIDDLE EAST

42.9. LIST OF UPCOMING DATA CENTER PROJECTS IN AFRICA

43. UAE

43.1. INVESTMENT

43.2. MARKET BY INVESTMENT

43.3. AREA

43.4. MARKET BY AREA

43.5. POWER CAPACITY

43.6. MARKET BY POWER CAPACITY

43.7. KEY SUPPORT INFRASTRUCTURE ADOPTION

43.8. MARKET BY INFRASTRUCTURE

44. SAUDI ARABIA

44.1. INVESTMENT

44.2. MARKET BY INVESTMENT

44.3. AREA

44.4. MARKET BY AREA

44.5. POWER CAPACITY

44.6. MARKET BY POWER CAPACITY

44.7. KEY SUPPORT INFRASTRUCTURE ADOPTION

44.8. MARKET BY INFRASTRUCTURE

45. ISRAEL

45.1. INVESTMENT

45.2. MARKET BY INVESTMENT

45.3. AREA

45.4. MARKET BY AREA

45.5. POWER CAPACITY

45.6. MARKET BY POWER CAPACITY

45.7. KEY SUPPORT INFRASTRUCTURE ADOPTION

45.8. MARKET BY INFRASTRUCTURE

46. OTHER MIDDLE EAST COUNTRIES

46.1. INVESTMENT

46.2. MARKET BY INVESTMENT

46.3. AREA

46.4. MARKET BY AREA

46.5. POWER CAPACITY

46.6. MARKET BY POWER CAPACITY

46.7. KEY SUPPORT INFRASTRUCTURE ADOPTION

46.8. MARKET BY INFRASTRUCTURE

47. SOUTH AFRICA

47.1. INVESTMENT

47.2. MARKET BY INVESTMENT

47.3. AREA

47.4. MARKET BY AREA

47.5. POWER CAPACITY

47.6. MARKET BY POWER CAPACITY

47.7. KEY SUPPORT INFRASTRUCTURE ADOPTION

47.8. MARKET BY INFRASTRUCTURE

48. KENYA

48.1. INVESTMENT

48.2. MARKET BY INVESTMENT

48.3. AREA

48.4. MARKET BY AREA

48.5. POWER CAPACITY

48.6. MARKET BY POWER CAPACITY

48.7. KEY SUPPORT INFRASTRUCTURE ADOPTION

48.8. MARKET BY INFRASTRUCTURE

49. OTHER AFRICAN COUNTRIES

49.1. INVESTMENT

49.2. MARKET BY INVESTMENT

49.3. AREA

49.4. MARKET BY AREA

49.5. POWER CAPACITY

49.6. MARKET BY POWER CAPACITY

49.7. KEY SUPPORT INFRASTRUCTURE ADOPTION

49.8. MARKET BY INFRASTRUCTURE

50. APAC

50.1. MARKET SNAPSHOT & KEY HIGHLIGHTS

50.2. DATA CENTER MARKET BY INVESTMENT

50.3. DATA CENTER MARKET BY INFRASTRUCTURE

50.4. DATA CENTER MARKET BY AREA

50.5. DATA CENTER MARKET BY POWER CAPACITY

50.6. DATA CENTER MARKET BY SUPPORT INFRASTRUCTURE

50.7. DATA CENTER MARKET BY IT INFRASTRUCTURE

50.8. LIST OF UPCOMING DATA CENTER PROJECTS IN APAC

51. CHINA

51.1. INVESTMENT

51.2. MARKET BY INVESTMENT

51.3. AREA

51.4. MARKET BY AREA

51.5. POWER CAPACITY

51.6. MARKET BY POWER CAPACITY

51.7. KEY SUPPORT INFRASTRUCTURE ADOPTION

51.8. MARKET BY INFRASTRUCTURE

51.9. LIST OF UPCOMING DATA CENTER PROJECTS IN CHINA

52. HONG KONG

52.1. INVESTMENT

52.2. MARKET BY INVESTMENT

52.3. AREA

52.4. MARKET BY AREA

52.5. POWER CAPACITY

52.6. MARKET BY POWER CAPACITY

52.7. KEY SUPPORT INFRASTRUCTURE ADOPTION

52.8. MARKET BY INFRASTRUCTURE

53. AUSTRALIA

53.1. INVESTMENT

53.2. MARKET BY INVESTMENT

53.3. AREA

53.4. MARKET BY AREA

53.5. POWER CAPACITY

53.6. MARKET BY POWER CAPACITY

53.7. KEY SUPPORT INFRASTRUCTURE ADOPTION

53.8. MARKET BY INFRASTRUCTURE

54. NEWZEALND

54.1. INVESTMENT

54.2. MARKET BY INVESTMENT

54.3. AREA

54.4. MARKET BY AREA

54.5. POWER CAPACITY

54.6. MARKET BY POWER CAPACITY

54.7. KEY SUPPORT INFRASTRUCTURE ADOPTION

54.8. MARKET BY INFRASTRUCTURE

55. INDIA

55.1. INVESTMENT

55.2. MARKET BY INVESTMENT

55.3. AREA

55.4. MARKET BY AREA

55.5. POWER CAPACITY

55.6. MARKET BY POWER CAPACITY

55.7. KEY SUPPORT INFRASTRUCTURE ADOPTION

55.8. MARKET BY INFRASTRUCTURE

56. JAPAN

56.1. INVESTMENT

56.2. MARKET BY INVESTMENT

56.3. AREA

56.4. MARKET BY AREA

56.5. POWER CAPACITY

56.6. MARKET BY POWER CAPACITY

56.7. KEY SUPPORT INFRASTRUCTURE ADOPTION

56.8. MARKET BY INFRASTRUCTURE

57. SOUTH KOREA

57.1. INVESTMENT

57.2. MARKET BY INVESTMENT

57.3. AREA

57.4. MARKET BY AREA

57.5. POWER CAPACITY

57.6. MARKET BY POWER CAPACITY

57.7. KEY SUPPORT INFRASTRUCTURE ADOPTION

57.8. MARKET BY INFRASTRUCTURE

58. TAIWAN

58.1. INVESTMENT

58.2. MARKET BY INVESTMENT

58.3. AREA

58.4. MARKET BY AREA

58.5. POWER CAPACITY

58.6. MARKET BY POWER CAPACITY

58.7. KEY SUPPORT INFRASTRUCTURE ADOPTION

58.8. MARKET BY INFRASTRUCTURE

59. SINGAPORE

59.1. INVESTMENT

59.2. MARKET BY INVESTMENT

59.3. AREA

59.4. MARKET BY AREA

59.5. POWER CAPACITY

59.6. MARKET BY POWER CAPACITY

59.7. KEY SUPPORT INFRASTRUCTURE ADOPTION

59.8. MARKET BY INFRASTRUCTURE

60. INDONESIA

60.1. INVESTMENT

60.2. MARKET BY INVESTMENT

60.3. AREA

60.4. MARKET BY AREA

60.5. POWER CAPACITY

60.6. MARKET BY POWER CAPACITY

60.7. KEY SUPPORT INFRASTRUCTURE ADOPTION

60.8. MARKET BY INFRASTRUCTURE

69. MALAYSIA

69.1. INVESTMENT

69.2. MARKET BY INVESTMENT

69.3. AREA

69.4. MARKET BY AREA

69.5. POWER CAPACITY

69.6. MARKET BY POWER CAPACITY

69.7. KEY SUPPORT INFRASTRUCTURE ADOPTION

69.8. MARKET BY INFRASTRUCTURE

70. THAILAND

71.1. INVESTMENT

71.2. MARKET BY INVESTMENT

71.3. AREA

71.4. MARKET BY AREA

71.5. POWER CAPACITY

71.6. MARKET BY POWER CAPACITY

71.7. KEY SUPPORT INFRASTRUCTURE ADOPTION

71.8. MARKET BY INFRASTRUCTURE

72. PHILIPPINES

72.1. INVESTMENT

72.2. MARKET BY INVESTMENT

72.3. AREA

72.4. MARKET BY AREA

72.5. POWER CAPACITY

72.6. MARKET BY POWER CAPACITY

72.7. KEY SUPPORT INFRASTRUCTURE ADOPTION

72.8. MARKET BY INFRASTRUCTURE

73. VIETNAM

73.1. INVESTMENT

73.2. MARKET BY INVESTMENT

73.3. AREA

73.4. MARKET BY AREA

73.5. POWER CAPACITY

73.6. MARKET BY POWER CAPACITY

73.7. KEY SUPPORT INFRASTRUCTURE ADOPTION

73.8. MARKET BY INFRASTRUCTURE

74. MARKET PARTICIPANTS

74.1. IT INFRASTRUCTURE PROVIDER

74.2. DATA CENTER SUPPORT INFRASTRUCTURE PROVIDERS

75.4. DATA CENTER CONTRACTORS

74.6. DATA CENTER INVESTORS

74.7. NEW ENTRANTS

75. QUANTITATIVE SUMMARY

76. APPENDIX

76.1. ABBREVIATIONS

76.2. DEFINITIONS

76.3. SEGMENTAL COVERAGE

Select a license type that suits your business needs

Single User Licence

- Report accessible by one user only

- Free 10% or 3 days of customization

- Free post-sale service assistance

- Continuous support through email

5 User Licence

- Report accessible by 5 users within the organization

- Free 15% or 4.5 days of customization

- Continuous support through email and telephone

- Free analyst hour

- Free Upgrade: If an updated report published within 180 days of purchase, you will get the revised report free of charge

Corporate Licence

- Free Datasheet worth $1500

- Report accessible by the entire organization

- Free 20% or 6 days of customization

- Free post-sale service assistance

- Continuous support through email and telephone

- Direct access to lead analysts

- Free analyst hour

- Free Upgrade: If an updated report published within 180 days of purchase, you will get the revised report free of charge

Datasheet Licence

- Report accessible by 1 user only

- Free 15% or 32 hours of customization

- Free post-sale service assistance

- Direct access to lead analysts

Frequently Asked Questions

How big is the global hyperscale data center market in terms of investments?

Which region holds the most significant global hyperscale data center market share?

What is the estimated market size in terms of area in the global hyperscale data center market by 2030?

How many MW of power capacity is expected to reach the global hyperscale data center market by 2030?

What is the growth rate of the global hyperscale data center market?