Global Industrial Laser Market Research Report 2026-2031

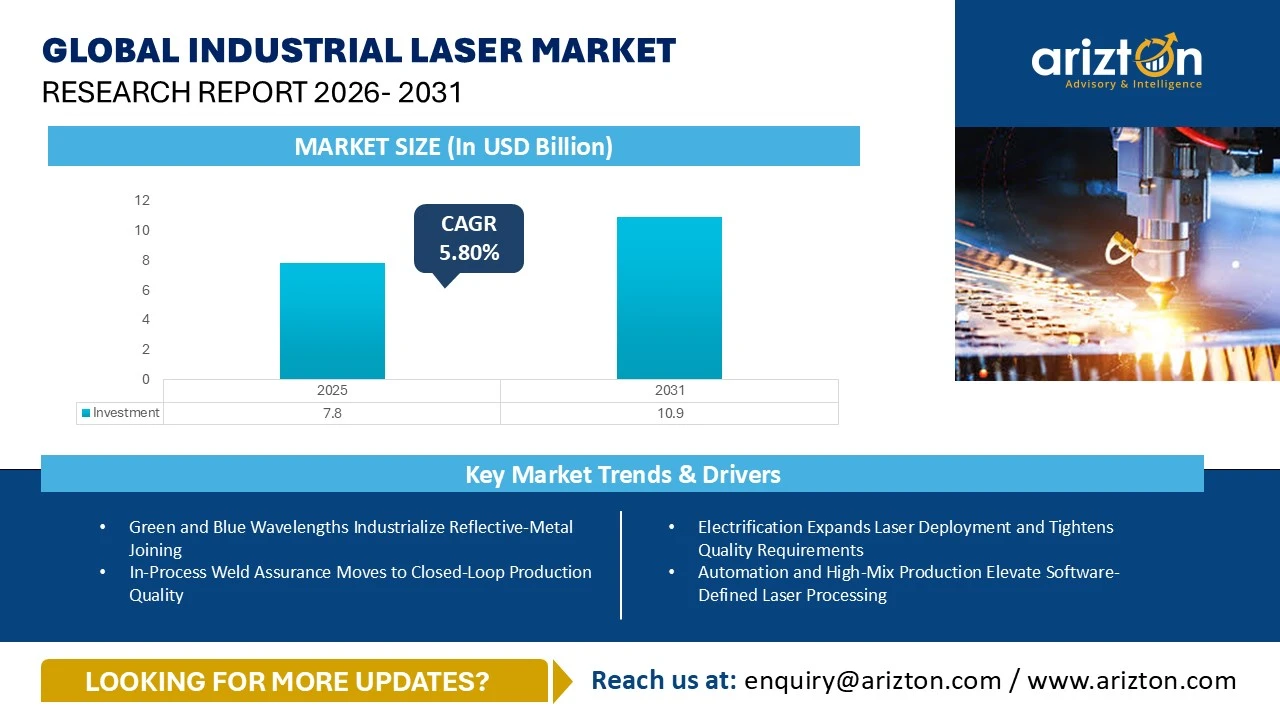

THE GLOBAL INDUSTRIAL LASER MARKET VALUED AT USD 7.8 BILLION IN 2025 AND IS PROJECTED TO REACH USD 10.9 BILLION BY 2031, GROWING AT A CAGR OF 5.80% FROM 2025 TO 2031.

Global Industrial Laser Market Research Report 2026-2031

THE GLOBAL INDUSTRIAL LASER MARKET VALUED AT USD 7.8 BILLION IN 2025 AND IS PROJECTED TO REACH USD 10.9 BILLION BY 2031, GROWING AT A CAGR OF 5.80% FROM 2025 TO 2031.

The Industrial Laser Market Size, Share & Trends Analysis Report By

- Type: Fiber, CO2, Solid State, and Others

- Power Output: Low Power, Medium Power, and High Power

- End-User: Semiconductor and Electronics, Metal Fabrication, Automotive, Energy and Heavy Industry, Non-Metal Processing and Consumer Goods, Aerospace and Defense, Healthcare and Medical Devices, and Others

- Application: Cutting, Welding and Brazing, Marking and Engraving, Drilling, and Others

- Geography: North America, Europe, APAC, Latin America, & Middle East & Africa

Industry Analysis Report, Regional Outlook, Growth Potential, Price Trends, Competitive Market Share & Forecast 2026–2031.

This report includes market data points, ranging from trend

analyses to market estimates & forecasts that you can customize

INDUSTRIAL LASER MARKET REPORT SCOPE

| REPORT ATTRIBUTE | DETAILS |

|---|---|

| MARKET SIZE (2031) | USD 10.9 Billion |

| MARKET SIZE (2025) | USD 7.8 Billion |

| CAGR (2025-2031) | 5.80% |

| HISTORIC YEAR | 2022-2024 |

| BASE YEAR | 2025 |

| FORECAST YEAR | 2026-2031 |

| SEGMENTS BY | Type, Power Output, End-User, Application, and Geography |

| GEOGRAPHIC ANALYSIS | North America, Europe, APAC, Latin America, & Middle East & Africa |

| KEY PLAYERS | TRUMPF, Han’s Laser, Coherent, IPG Photonics, AMADA, and Bystronic |

INDUSTRIAL LASER MARKET SIZE ANALYSIS

The global industrial laser market was valued at USD 7.8 billion in 2025 and is projected to reach USD 10.9 billion by 2031, growing at a CAGR of 5.80% during the forecast period.

The market is evolving as manufacturers increasingly adopt advanced industrial laser systems, industrial laser technology, and high-performance laser processing systems to enhance precision, throughput, and automation across industries such as metal fabrication, electronics, and e-mobility.

The growth of the industrial lasers market is supported by the expanding use of laser cutting machines, laser welding systems, and other industrial laser equipment in production environments where clean processing, high precision, and automation compatibility are critical. Technologies such as laser beam machining are gaining importance for delivering consistent output and improved production efficiency.

Demand is also rising in semiconductor manufacturing, where fab expansions are driving the adoption of advanced industrial laser systems for precision processing and traceability. SEMI reported that 18 new semiconductor fabs were expected to begin construction in 2025, with several advanced facilities scheduled for operation between 2026 and 2027. These developments support increased deployment of laser processing systems in packaging, marking, and microfabrication.

Industrial lasers include production-grade sources and integrated industrial laser equipment used for cutting, welding, drilling, marking, cleaning, and micromachining across metals, polymers, ceramics, and semiconductor materials. The technology landscape spans fiber laser technology, CO2 laser systems, solid-state laser systems, and ultrafast lasers industrial use, each addressing specific industrial requirements. Their adoption continues to grow in applications requiring controlled heat input, precision, and automation compatibility.

Keyence highlights advanced laser marking solutions that enable permanent, machine-readable markings, supporting traceability and quality control across modern industrial laser systems.

Industrial Laser Market Size Summary

- Market to grow from $7.8B (2025) to $10.9B (2031) at 5.8% CAGR

- Adoption rising for precision, automation, and high-efficiency manufacturing

- Strong demand from metal, electronics, e-mobility, and semiconductors

- Growth driven by laser cutting, welding, and machining applications

- Fiber, CO₂, solid-state, and ultrafast lasers are leading the technology adoption

KEY TAKEAWAYS

- Power Output: Medium power lasers accounted for the largest industrial lasers market share in 2025.

- Type: CO2 laser systems accounted for the second-largest share of around 21%.

- End-User: Semiconductor and electronics show significant growth, supported by increasing adoption of industrial laser technology.

- Application: Laser cutting machines dominate and hold the largest market share.

- Geography: APAC accounted for the largest industrial lasers market share of around 53%.

INDUSTRIAL LASER MARKET PRODUCT DEVELOPMENTS

Recent innovations continue to strengthen the industrial lasers market:

- In June 2025, HGTECH introduced advanced semiconductor-focused laser processing systems, including SiC wafer laser annealing equipment.

- In September 2025, Yamazaki Mazak launched high-power fiber-based laser cutting machines to improve thick plate processing efficiency.

- In June 2025, Bodor Laser introduced cost-effective sheet metal industrial laser equipment, expanding accessibility for mid-tier manufacturers.

- In October 2025, Penta Laser expanded its European footprint, strengthening the adoption of industrial laser systems in high-power cutting.

- In March 2025, BLM GROUP introduced CAM software to enhance the productivity of 3D laser processing systems.

- In June 2025, Prima Power launched multi-head 3D laser cutting machines for high-volume automotive production.

INDUSTRIAL LASER DEMAND & INVESTMENT OPPORTUNITY

The industrial laser investment thesis is compelling across both established and high-growth manufacturing economies. Several structural forces are converging to widen the addressable market.

- Semiconductor fab expansion: SEMI data confirms 18 new fabs expected to break ground in 2025, directly expanding laser processing and traceability marking demand in advanced chip manufacturing.

- Electrification and EV production growth: The IEA reports global EV battery demand exceeded 750 GWh in 2023, with US manufacturing capacity reaching over 200 GWh in 2024 and nearly 700 GWh under construction — all requiring laser-based welding, electrode cutting, and copper processing.

- Automation and flexible manufacturing investment: As factories manage broader product variation and higher automation levels, lasers are becoming core flexible production tools for high-mix, low-volume and high-throughput environments alike.

- India's semiconductor programme execution: Approved projects, including Tata Electronics' Dholera facility and a semiconductor plant in Assam, supported by the India Semiconductor Mission, are expected to drive demand for precision laser processing equipment as they move toward operationalisation.

INDUSTRIAL LASER MARKET TRENDS & DRIVERS

The adoption of laser welding systems integrated with real-time quality monitoring is increasing, enabling defect prevention and improved production consistency. Companies such as FANUC highlight the use of robotic industrial laser systems that support adaptive welding and process control.

Advancements in industrial laser technology, particularly visible-wavelength lasers, are improving copper processing efficiency. Laserline GmbH emphasizes the role of blue diode lasers in applications such as battery components and electrical contacts, where precision and stability are critical.

The rise of electrification and EV manufacturing is further accelerating demand for laser processing systems, especially for battery welding, electrode cutting, and precision joining. According to the International Energy Agency, global EV battery demand exceeded 750 GWh in 2023, supporting increased adoption of industrial laser equipment.

Additionally, flexible manufacturing environments are driving demand for adaptable industrial laser systems. IPG Photonics promotes automated solutions that enhance productivity in high-mix production environments.

INDUSTRY RESTRAINTS

The industrial lasers market remains sensitive to fluctuations in industrial investment cycles, which can impact demand for industrial laser equipment. TRUMPF reported a decline in order intake amid weaker demand conditions, reflecting cyclical trends in manufacturing.

Increasing price competition in standard laser cutting machines, particularly those based on fiber laser technology, is making differentiation more challenging for vendors.

INDUSTRIAL LASER MARKET SEGMENTATION INSIGHTS

INSIGHT BY POWER OUTPUT

Based on the power output, the medium power accounted for the largest global industrial laser market share in 2025. Medium power from 1 to 6 kW anchors mainstream industrial deployment because it covers a span of cutting and welding needs within general manufacturing. Customers view this band as the practical core for high mix production, where speed and output quality both matter. Offerings include flatbed sheet cutters, tube cutting platforms, and robotic welding cells built around standardized machine architectures.

Typical workflows include 2D sheet cutting for parts, tube profiling, and laser welding for assemblies across automotive, appliance, industrial equipment, and contract manufacturing. Customers value versatility across materials and programs, shifting between jobs through software rather than tooling. In joining, many applications sit around 2 to 3 kW, supporting deep seams with controlled distortion and takt alignment in production cells.

Medium power laser systems serve as the production backbone for general manufacturers, enabling high-mix throughput across cutting and welding without tooling investment or line reconfiguration.

INSIGHT BY TYPE

The global industrial lasers market by type is segmented into fiber, CO2, solid state, and others. The CO₂ lasers accounted for the second largest market share of around 21%, as they remain well-suited for processing non-metal materials across industries such as packaging, consumer products, and light manufacturing. CO₂ lasers offer strong material interaction with substrates including plastics, paper, textiles, leather, and glass, enabling efficient cutting, engraving, and marking applications.

Companies such as Trotec Laser GmbH highlight the widespread use of CO₂ lasers in processing these materials, reinforcing their continued relevance in workflows where non-metal fabrication and surface processing are critical.

Solid State shows significant growth from 2025 to 2031, driven by the expansion of precision processing applications across electronics, semiconductor manufacturing, and medical device production. These applications require high accuracy, minimal heat-affected zones, and strong process control, supporting continued adoption of solid-state laser technologies.

INSIGHT BY END-USER

Based on the end-user, the semiconductor and electronics show significant growth, with the fastest-growing CAGR of 7.14% during the forecast period. The segment growth is driven by the widespread adoption of laser processing in applications such as wafer dicing, scribing, trimming, package marking, and PCB microvia formation. These processes require high precision, clean edge quality, and minimal thermal impact, making lasers a preferred solution in advanced electronics manufacturing.

Additionally, companies such as LPKF Laser & Electronics highlight that laser drilling enables the production of microvias below 200 µm in advanced PCB substrates, reinforcing the critical role of laser technologies in supporting miniaturization and high-density electronic designs.

Semiconductor fab expansion and EV production scale-up are jointly reinforcing laser demand across two of the market's highest-growth end-use segments simultaneously.

INSIGHT BY APPLICATION

The cutting segment dominates and holds the largest global industrial laser market share. Laser cutting in industrial settings spans 2D sheet cutting, tube cutting, and 3D contour cutting across metals and selected non-metals. It serves as a high-throughput shaping step that delivers parts with precise geometry and consistent edge quality. Systems are deployed in fabrication workflows and production lines where dimensional accuracy and stable cycle performance support scheduling discipline and capacity planning.

Metal fabrication customers adopt this subsegment because software-based programs handle diverse part mixes without tooling changes and enable faster changeovers. Production plants scale laser cutting when consistent cut quality supports downstream forming and assembly performance. Demand rises as facilities digitize fabrication and add automation, with adoption extending into electric vehicle chassis and renewable energy structures that require contour cutting at higher volumes.

INDUSTRIAL LASER MARKET GEOGRAPHICAL ANALYSIS

The APAC region accounted for the largest industrial lasers market share of around 53%. APAC remains the largest production base for industrial lasers, supported by large-scale manufacturing activity that sustains demand for cutting, welding, and marking across automated production stations. OICA reported 54.9 million motor vehicles produced in Asia Oceania in 2024. Competition, therefore, centres on throughput, stable output, and service coverage, while buyers prioritize automation ready platforms that integrate with robotics and traceability requirements in major manufacturing clusters.

India is projected to register the highest CAGR during 2025–2031, driven by the transition of electronics and semiconductor manufacturing from policy intent to on-ground project execution. The country is witnessing increasing investments in domestic fabrication and assembly capabilities, supporting demand for advanced manufacturing technologies. Under the national semiconductor program, approved projects include facilities by Tata Electronics in Dholera, Gujarat, with a planned capacity of around 50,000 wafer starts per month. Additionally, a semiconductor facility in Assam is expected to scale production significantly, further strengthening the domestic ecosystem.

This broader initiative is supported by substantial government incentives under the India Semiconductor Mission, aimed at expanding local manufacturing capacity. As these projects move toward operationalization, they are expected to drive demand for precision manufacturing equipment, including laser-based processing systems used in electronics and semiconductor production.

Europe accounted for the second largest market share in 2025, supported by its broad precision-manufacturing base and steady demand from automotive, machinery, electronics, and other regulated industrial sectors. ACEA reports that EU car production reached 11.4 million units in 2024, underscoring the region’s continued importance in advanced manufacturing. This large industrial base continues to support laser adoption in cutting, welding, marking, and precision fabrication, where process consistency and automation are important production requirements.

India and Southeast Asia represent the highest forward-looking growth opportunities, as semiconductor fab investment and electronics manufacturing localisation convert government policy commitments into active procurement of advanced laser processing equipment.

INDUSTRIAL LASER MARKET VENDOR LANDSCAPE

The global industrial laser market is characterised by a relatively concentrated group of laser source manufacturers and laser-enabled machine tool OEMs, supported by a broader ecosystem of automation, optics, and motion-control providers. This ecosystem enables the expansion of laser applications across cutting, welding, marking, microprocessing, and additive manufacturing at the system integration level.

In high-power cutting, competitive differentiation is increasingly shaped by thick-material throughput, process stability, and automation readiness, as end users demand higher productivity and consistent output in heavy-duty fabrication. In welding and joining, competitive advantage depends on beam-delivery flexibility, reflective-metal capability, and repeatable process quality. Software and service ecosystems are also becoming stronger competitive levers, with leading OEMs expanding digital production-control, automation, and monitoring capabilities to improve machine utilisation and connected factory performance.

- TRUMPF GmbH + Co. KG (Germany): A global leader in industrial laser sources and sheet metal processing systems. TRUMPF reported group order intake of $5.08 billion in fiscal 2023/24 and continues to expand digital production-control and automation capabilities to strengthen connected factory positioning across cutting and welding applications.

- IPG Photonics (USA): A dominant supplier of high-power fibre laser sources. IPG positions its LightWELD Cobot System around automation of repetitive welds and high-mix, low-volume fabrication, while emphasising energy-efficient fibre laser architectures to lower power consumption in high-power industrial operations.

- Coherent Corp. (USA): A major supplier of lasers and photonics technologies across industrial, semiconductor, and communications markets. Coherent strengthens its welding and joining position through flexible fibre-laser architectures, while acknowledging that many industrial end markets remain cyclical in nature.

- Laserline GmbH (Germany): Focused on diode and blue-laser solutions for copper-intensive applications in automotive and e-mobility manufacturing. Laserline highlights that blue diode lasers are especially effective for electrical contacts, battery components, and thin sheets or foils, where infrared wavelength absorption inconsistencies can cause weld defects.

- Yamazaki Mazak (Japan): A leading machine tool OEM with a strong laser cutting portfolio. Mazak announced the OPTIPLEX 3015 HP / 4220 HP high-power 2D fibre laser processing machines in September 2025 to reinforce competitiveness in high-power thick plate cutting.

- Bystronic AG (Switzerland): A prominent supplier of laser cutting and bending systems. Bystronic is expanding digital production-control and monitoring capabilities alongside its core cutting hardware to strengthen automation and workflow coordination for fabrication customers.

SNAPSHOT

The global industrial laser market size is expected to grow at a CAGR of approximately 5.80% from 2025 to 2031.

The following factors are likely to contribute to the growth of the global industrial laser market during the forecast period:

- Electrification Expands Laser Deployment and Tightens Quality Requirements

- Automation and High-Mix Production Elevate Software-Defined Laser Processing

- Miniaturization Expands Low-Thermal Precision Processing Needs

- Traceability and Governance Increase Demand for Marking and Process Data

Base Year: 2025

Forecast Year: 2026-2031

The report examines the current state of the global industrial laser market and its market dynamics through 2026−2031. It covers a detailed overview of several market growth enablers, restraints, and trends. The study covers both the demand and supply sides of the market. It also profiles and analyses leading companies and several other prominent companies operating in the market.

Key Company Profiles

- TRUMPF

- Business Overview

- Product Offerings

- Key Developments

- Key Strategies

- Key Strengths

- Key Opportunities

- Han’s Laser

- Coherent

- IPG Photonics

- AMADA

- Bystronic

Other Prominent Company Profiles

- HGTECH

- Business Overview

- Product Offerings

- Yamazaki Mazak (Mazak Optonics)

- Bodor Laser

- HSG Laser

- Prima Power

- Mitsubishi Electric

- Penta Laser

- KEYENCE

- FANUC

- Salvagnini

- Laserline

- BLM GROUP

- GWEIKE

- Videojet

- Trotec Laser

- Raycus

- LVD

- Golden Laser

- Epilog Laser

- Universal Laser Systems

- Domino Printing Sciences

- Nukon

- Maxphotonics

- Kimla

Segmentation by Power Output:

- Low Power

- Medium Power

- High Power

Segmentation by Type

- Fiber

- CO2

- Solid State

- Others

Segmentation by End-User

- Semiconductor and Electronics

- Metal Fabrication

- Automotive

- Energy and Heavy Industry

- Non-Metal Processing and Consumer Goods

- Aerospace and Defense

- Healthcare and Medical Devices

- Others

Segmentation by Application

- Cutting

- Welding and Brazing

- Marking and Engraving

- Drilling

- Others

Segmentation by Geography

- APAC

- China

- Japan

- South Korea

- India

- Thailand

- Malaysia

- Indonesia

- Australia

- Europe

- Germany

- France

- Italy

- UK

- Spain

- Russia

- Poland

- Netherlands

- North America

- U.S.

- Canada

- Latin America

- Brazil

- Mexico

- Argentina

- Middle East & Africa

- Saudi Arabia

- UAE

- South Africa

INDUSTRIAL LASER MARKET FAQs

How big is the global industrial laser market?

What is the growth rate of the global industrial laser market?

Which region dominates the global industrial laser market?

What are the key trends in the global industrial laser market?

Who are the major players in the global industrial laser market?

For more details, please reach us at [email protected]

Chapter 1- Scope & Coverage

- Market Definition

- Inclusion

- Exclusions

- Market Estimation Caveats

- Market Derivation

- Market Segmentation by Type

- Market Segmentation by Power Output

- Market Segmentation by End-User

- Market Segmentation by Application

Chapter 2- Premium Insights

Chapter 3- Market Dynamics

- Introduction

- Working of Industrial Lasers

- Value Chain Analysis

- Industrial Laser Type and Use Case

- Future Advancements in Industrial Laser Technologies

- Applications of Industrial Lasers

- Comparative Analysis of Scientific and Industrial Lasers

- Safety and Compliance Framework

- Market Opportunities & Trends

- In-Process Weld Assurance Moves to Closed-Loop Production Quality

- Green and Blue Wavelengths Industrialize Reflective-Metal Joining

- Ultrafast Lasers Scale to Production-Grade Throughput

- Laser Cleaning Becomes an Inline Surface-Conditioning Gate

- Market Growth Enablers

- Electrification Expands Laser Deployment and Tightens Quality Requirements

- Automation and High-Mix Production Elevate Software-Defined Laser Processing

- Miniaturization Expands Low-Thermal Precision Processing Needs

- Traceability and Governance Increase Demand for Marking and Process Data

- Market Restraints

- Capital Cycle Sensitivity and Project Timing Variability Reduce Visibility

- Pricing Pressure in Mature Cutting Segments Limits Value Capture

- Export Controls and Dual-Use Compliance Add Lead-Time Variability

- Market Landscape

- Five Forces Analysis

Chapter 4- Market Segmentation

- Type (Market Size & Forecast: 2022-2031)

- Fiber

- CO2

- Solid State

- Others

- Power Output (Market Size & Forecast: 2022-2031)

- Low Power

- Medium Power

- High Power

- End-User (Market Size & Forecast: 2022-2031)

- Semiconductor and Electronics

- Metal Fabrication

- Automotive

- Energy and heavy industry

- Non-metal processing and consumer goods

- Aerospace and defense

- Healthcare and medical devices

- Others

- Application (Market Size & Forecast: 2022-2031)

- Cutting

- Welding and brazing

- Marking and engraving

- Drilling

- Others

Chapter 5- Geography Segmentation

- Geography Segmentation (Market Size & Forecast: 2022-2031)

- Geographic Overview – Market Maturity Index

- APAC

- China

- Japan

- South Korea

- India

- Thailand

- Malaysia

- Indonesia

- Australia

- North America

- US

- Canada

- Europe

- Germany

- France

- Italy

- UK

- Spain

- Russia

- Poland

- Netherlands

- Latin America

- Brazil

- Mexico

- Argentina

- MEA

- Saudi Arabia

- UAE

- South Africa

Chapter 6- Competitive Landscape

- Competitive Landscape

- Competition Overview

- Key Developments

- Key Company Profiles

- Other Prominent Company Profiles

- Report Summary

- Key Takeaways

- Strategic Recommendations

Select a license type that suits your business needs

Single User Licence

- Report accessible by one user only

- Free 10% or 3 days of customization

- Free post-sale service assistance

- Continuous support through email

5 User Licence

- Report accessible by 5 users within the organization

- Free 15% or 4.5 days of customization

- Continuous support through email and telephone

- Free analyst hour

- Free Upgrade: If an updated report published within 180 days of purchase, you will get the revised report free of charge

Corporate Licence

- Free Datasheet worth $1500

- Report accessible by the entire organization

- Free 20% or 6 days of customization

- Free post-sale service assistance

- Continuous support through email and telephone

- Direct access to lead analysts

- Free analyst hour

- Free Upgrade: If an updated report published within 180 days of purchase, you will get the revised report free of charge

Datasheet Licence

- Report accessible by 1 user only

- Free 15% or 32 hours of customization

- Free post-sale service assistance

- Direct access to lead analysts

Frequently Asked Questions

How big is the global industrial laser market?

What is the growth rate of the global industrial laser market?

Which region dominates the global industrial laser market?

What are the key trends in the global industrial laser market?

Who are the major players in the global industrial laser market?

Other RELATED Reports

Global Industrial Nailers and Staplers Market - Focused Insights 2024-2029

Published : September 2024