Latin America Data Center Colocation Market – Industry Outlook & Forecast 2026-2031

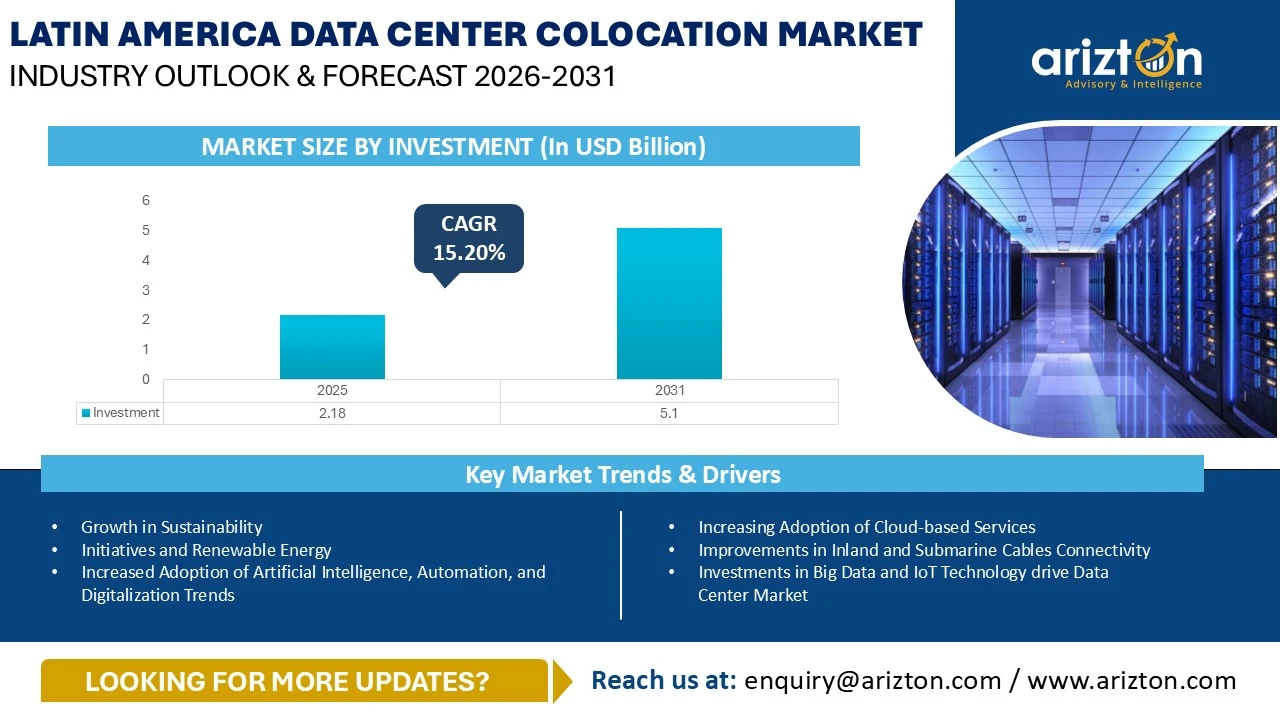

LATIN AMERICA DATA CENTER COLOCATION MARKET SIZE BY INVESTMENT WAS VALUED AT USD 2.18 BILLION IN 2025 AND IS EXPECTED TO REACH USD 5.10 BILLION BY 2031, GROWING AT A CAGR OF 15.20% DURING THE FORECAST PERIOD.

193 pages

47 company

9 segments

1 region

6 countries

Purchase Options

Latin America Data Center Colocation Market – Industry Outlook & Forecast 2026-2031

LATIN AMERICA DATA CENTER COLOCATION MARKET SIZE BY INVESTMENT WAS VALUED AT USD 2.18 BILLION IN 2025 AND IS EXPECTED TO REACH USD 5.10 BILLION BY 2031, GROWING AT A CAGR OF 15.20% DURING THE FORECAST PERIOD.

The Latin America Data Center Colocation Market Report Includes

- Colocation Type: Retail Colocation and Wholesale Colocation

- Infrastructure: Electrical Infrastructure, Mechanical Infrastructure, and General Construction

- Electrical Infrastructure: UPS Systems, Generators, Transfer Switches & Switchgear, PDUs, and Other Electrical Infrastructure

- Mechanical Infrastructure: Cooling Systems, Racks, and Other Mechanical Infrastructure

- Cooling Systems: CRAC & CRAH Units, Chiller Units, Cooling Towers, Condensers & Dry Coolers, Economizers & Evaporative Coolers, and Other Cooling Units

- Cooling Techniques: Air-based Cooling and Liquid-based Cooling

- General Construction: Core & Shell Development, Installation & Commissioning Services, Engineering & Building Design, Fire Detection & Suppression, Physical Security, and DCIM/BMS Solutions

- Tier Standard: Tier I & II, Tier III, and Tier IV

- Geography: Brazil, Mexico, Chile, Colombia, Argentina, and Rest of Latin America

Get Insights on 260 Existing Data Center Facilities and 78 Upcoming Facilities across Latin America

This report includes market data points, ranging from trend

analyses to market estimates & forecasts that you can customize

LATIN AMERICA DATA CENTER COLOCATION MARKET REPORT SCOPE

| REPORT ATTRIBUTE | DETAILS |

|---|---|

| MARKET SIZE BY INVESTMENT 2031 | USD 5.10 Billion |

| MARKET SIZE BY INVESTMENT 2025 | USD 2.18 Billion |

| CAGR - INVESTMENT (2025-2031) | 15.20% |

| MARKET SIZE - COLOCATION REVENUE 2031 | USD 4.51 Billion |

| MARKET SIZE AREA (2031) | 1.54 million sq. feet |

| POWER CAPACITY (2031) | 389 MW (2030) |

| BASE YEAR | 2025 |

| FORECAST YEAR | 2026-2031 |

| MARKET SEGMENTS | Colocation Service, Infrastructure, Electrical Infrastructure, Mechanical Infrastructure, Cooling Systems, Cooling Techniques, General Construction, Tier Standards, and Geography |

| GEOGRAPHICAL ANALYSIS | Brazil, Mexico, Chile, Colombia, Argentina, and Rest of Latin America |

LATIN AMERICA DATA CENTER COLOCATION MARKET SIZE

The Latin America data center colocation market size by investment was valued at USD 2.18 billion in 2025 and is expected to reach USD 5.10 billion by 2031, growing at a CAGR of 15.20% during the forecast period. The Latin American data center colocation market continues to experience rapid global growth, driven by increasing cloud adoption, the expansion of edge computing, and the growing deployment of technologies such as AI, big data, and the IoT.

The region is estimated to witness a cumulative investment of around $23.15 billion from 2026-2031; where Brazil will contribute around $11.53 billion, representing around 49.8% of the overall share.

Investment in the Latin America data centers colocation market more than doubled as compared with 2025, fueled by strong construction activity from both colocation and hyperscale operators. It is estimated that the demand for data centers will continue to grow as Artificial Intelligence (AI) becomes more prevalent

The cost of data center construction in the Latin America region can range from $7 million to $10 million per MW, depending on the location. These elevated costs are influenced by factors such as limited land availability, high labor rates, inflation, and access to power.

LATIN AMERICA DATA CENTER COLOCATION MARKET OPPORTUNITIES & TRENDS

AI Transforming the Landscape of the Data Center Market

- Brazil continues to experience a broad-based digital transformation, supported by a steadily expanding internet user population and coordinated efforts from both public and private sectors. By 2025, internet penetration in Brazil had surpassed 86.5%, translating to more than 184 million users nationwide.

- Colombia continues to enter a new phase of digital maturity, and AI is at the forefront of this transformation. Claro Colombia continues to invest over $200 million to expand its fiber optic network. The purpose of this investment is to prepare its infrastructure for the adoption of advanced technologies such as AI.

- Chile is increasingly positioning itself as a regional center for digital innovation and emerging technologies, driven by a strong tech ecosystem and forward-thinking government policies. Government initiatives such as the Digital Transformation Strategy 2035 emphasize improving digital skills, strengthening cybersecurity frameworks, and enhancing technology-enabled public services. Active measures to attract global tech partnerships are further elevating the position of Chile as a regional innovation powerhouse.

- Mexico is undergoing digital transformation owing to the expanding internet user base, driven by a combination of public and private sector efforts. At the end of 2025, Mexico had 99 million active social media user identities. Facebook and YouTube accounted for the greatest number of users in Mexico. The country accounted for an internet penetration rate of 83.5%.

- The Argentina AI market is growing rapidly, driven by enterprise analytics, government AI initiatives, and a thriving tech/startup scene that needs local compute for training and inference. In May 2025, the government of Argentina promoted the country to become a global AI hub, aiming to be the "world’s fourth AI center" by offering minimal regulation, abundant land, and low energy costs to global tech firms.

Renewable Energy and Sustainability Initiatives by Data Center Operators

- The Latin America data center colocation market is increasingly integrating sustainability and renewable energy practices into infrastructure development, supported by strong government policies and corporate commitments to reduce carbon emissions. Countries across the region are setting ambitious renewable energy and carbon-neutrality targets while encouraging energy-efficient digital infrastructure and green power adoption for hyperscale and colocation facilities.

- The Argentine government has outlined a clear roadmap to expand the use of renewable energy as part of its national energy transition strategy. It has set ambitious targets to ensure that 20% of the total electricity consumption of the country comes from renewable sources by 2025, and to further increase this share to 35% by 2030. The Argentine government has also established the National Energy Efficiency Plan, which aims to reduce energy consumption and promote energy efficiency.

- The Brazilian data center market increasingly prioritizes sustainability, with many operators investing in energy-efficient infrastructure and renewable energy sources. Data centers continue to adopt green practices such as using solar and wind energy, implementing advanced cooling technologies, and optimizing PUE.

- Mexico has committed to achieving net-zero emissions by 2050. Several data center operators have been actively working toward the sustainability of data center facilities by powering them with renewable energy, adopting efficient electrical and mechanical infrastructure, and using several power monitoring systems.

- Chile has set an ambitious vision to prevent climate change and promote sustainability. The goals of the country include achieving peak greenhouse gas emissions by 2030, reaching carbon neutrality by 2050, and attaining net-zero greenhouse gas emissions by 2065. This vision aligns with global efforts to mitigate climate change and underscores Chile’s commitment to a sustainable future.

- Colombia has a diverse array of renewable energy sources, including wind, hydropower, biomass, geothermal, and solar energy. The country aims to produce 70% of energy through renewable sources by 2030. The renewable energy expansion goals of the country include a target of 6 GW of solar and wind energy by 2026. It aims to achieve carbon neutrality by 2050. In November 2025, Colombia made over 5,000 MW of space available on its electricity grid by clearing stalled or inactive connection requests. This allows new solar and wind projects to connect and start delivering power.

LATIN AMERICA DATA CENTER COLOCATION MARKET SEGMENTATION INSIGHTS

- The electrical infrastructure is witnessing several innovations in the UPS systems, generators, transfer switches & switchgears and other electrical equipment. Most data centers adopt N+1 diesel generators, providing backup fuel for up to 24 hours or more. For instance, Equinix’s MX2 data center is backed by the dual 1,939 kW diesel generators for main electrical bus support.

- Additionally, several innovative UPS batteries such as Nickel-Zinc (NiZn) and Sodium-Ion batteries are gaining traction in the market due to their high-power density, safety, sustainability, and other factors.

- AI workloads are changing cooling standards in US data centers, as traditional air cooling is insufficient to manage the heat output from GPU-dense clusters. The market is observing an increasing number of partnerships among data center operators, cooling technology vendors, chip manufacturers, and energy innovators, for instance, KIO Data Centers’ MEX 6 data center is equipped with 2N redundant chillers. It uses frozen water-cooling type solutions and N+2 redundant humidity controllers.

LATIN AMERICA DATA CENTER COLOCATION MARKET GEOGRAPHICAL ANALYSIS

- The Latin America data center market is currently experiencing significant growth, driven largely by the increasing adoption of technologies, particularly Artificial Intelligence (AI).

- Brazil holds a significant market share in the data center growth of Latin America. Digital transformation policies, coupled with the widespread adoption of IoT and big data, support major investments in data center infrastructure.

- Local and established providers play a significant role in offering tailored services for Brazilian businesses. In February 2026, Legrand acquired Green4T, a São Paulo-based data center infrastructure services provider with approx. 750 employees and about $53 million in annual revenue, further expanding its Latin American data center portfolio.

- The Mexico data center market is driven by factors such as the growing adoption of digital platforms, advanced technologies, including AI, IoT, and big data, and other factors. In November 2025, Telmex announced its plans to build a new data center in Northeastern Mexico, which is expected to become operational in 2026.

- As of December 2025, Chile hosted 39 operational data center facilities, spanning a total of 1,152.2 thousand square feet of white floor space, along with 9 upcoming facilities covering around 1,984.4 thousand square feet.

- Colombia is the fourth-largest economy in Latin America, playing an important role in the expansion of data centers across the region. In August 2025, Colombia launched ACOLDC, the Colombian Association of Data Centers and Data Technology, a non-profit organization that brings together key companies in the data center industry of Colombia.

- Power costs in Latin America vary widely by country, shaping data center location decisions. Chile has some of the highest electricity rates in the region, driving up operational costs; on the other hand, countries, including Argentina and Brazil, offer lower power prices, making them more appealing for cost-effective data center growth.

LATIN AMERICA DATA CENTER COLOCATION MARKET VENDOR LANDSCAPE

- The Latin America data center market has the presence of key investors such as Ascenty, Cirion Technologies, Claro, EdgeConneX, Elea Data Centers, Equinix, GTD, HostDime, IPXON Networks, KIO Data Centers, NextStream (Actis), ODATA (Aligned Data Centers), Quantico Data Center, Scala Data Centers, Takoda Data Centers, Tecto Data Centers, and others.

- In April 2026, I Squared Capital, a global infrastructure investor, announced its acquisition of a majority stake in Elea Data Centers, which is one of Brazil’s largest carrier-neutral data center platforms.

- In August 2025, ODATA (Aligned Data Centers) announced the launch of the first phase of its QR04 data center facility in Queretaro, Mexico, which will initially have an IT power capacity of 12 MW. Once fully constructed, the data center is expected to support a total capacity of 24 MW.

- New entrants in the region include 247 Data Centers, Ada Infrastructure, Atlantic Data Centers, Ava Telecom, CloudHQ, Fermaca Networks, Layer 9 Data Centers, MDC Data Centers, OpenAI & Sur Energy, Surfix Data Center, and Terranova.

- In October 2025, the Argentinian government introduced the Stargate Argentina initiative to support a large-scale facility, which would host OpenAI’s future AI workloads. OpenAI and Sur Energy signed a Letter of Intent for a project targeting up to 500 MW of capacity with an estimated $25 billion investment, with the initial 100 MW phase expected to become operational in 2027.

SNAPSHOT

The Latin America data center colocation market by investment is projected to reach USD 5.10 billion by 2031, growing at a CAGR of 15.20% from 2025 to 2031.

The following factors are likely to contribute to the growth of the Latin America data center colocation market during the forecast period:

- Rising Adoption of Cloud-based Services

- Government Support & Digital Economy Push

- Improvement in Connectivity via Submarine Cables

Base Year: 2025

Forecast Year: 2026-2031

The report considers the present scenario of the Latin America data center colocation market and its market dynamics for 2026−2031. It covers a detailed overview of several market growth enablers, restraints, and trends. The study includes the demand and supply aspects of the Latin America data center colocation industry.

Key Data Center Investors

- Ascenty

- Cirion Technologies

- Elea Data Centers

- Equinix

- KIO Data Centers

- NextStream (Actis)

- ODATA (Aligned Data Centers)

- Scala Data Centers

Other Data Center Investors

- Angola Cables

- Claro

- DHAmericas

- Edge Uno

- EdgeConneX

- EMPATEL SAPEM

- Etix Everywhere

- EVEO

- G2K

- GlobeNet International Corp.

- Gtd

- HostDime

- IPXON Networks

- Iplan

- InterNexa

- Mexico Telecom Partners

- NetGlobalis

- OneX Data Center

- PowerHost

- Quantico Data Center

- SONDA

- Takoda Data Centers

- Telecentro Empresas

- Telecom Argentina

- Tecto Data Centers

New Entrants

- 247 Data Centers

- Ada Infrastructure

- Atlantic Data Centers

- Ava Telecom

- CloudHQ

- Fermaca Networks

- Layer 9 Data Centers

- MDC Data Centers

- OpenAI and Sur Energy

- Surfix Data Center

- Terranova

- TECfusions

Segmentation by Colocation Type

- Retail Colocation

- Wholesale Colocation

Segmentation by Infrastructure

- Electrical Infrastructure

- Mechanical Infrastructure

- General Construction

Segmentation by Electrical Infrastructure

- UPS Systems

- Generators

- Transfer Switches & Switchgear

- PDUs

- Other Electrical Infrastructure

Segmentation by Mechanical Infrastructure

- Cooling Systems

- Racks

- Other Mechanical Infrastructure

Segmentation by Cooling Systems

- CRAC & CRAH Units

- Chiller Units

- Cooling Towers, Condensers & Dry Coolers

- Economizers & Evaporative Coolers

- Other Cooling Units

Segmentation by Cooling Techniques

- Air-based Cooling

- Liquid-based Cooling

Segmentation by General Construction

- Core & Shell Development

- Installation & Commissioning Services

- Engineering & Building Design

- Fire Detection & Suppression

- Physical Security

- DCIM/BMS Solutions

Segmentation by Tier Standard

- Tier I & II

- Tier III

- Tier IV

Segmentation by Geography

- Latin America

- Brazil

- Mexico

- Chile

- Colombia

- Argentina

- Rest of Latin America

LATIN AMERICA DATA CENTER COLOCATION MARKET FAQs

How big is the Latin America data center colocation market?

What is the growth rate of the Latin America data center colocation market?

What are the key trends in the Latin America data center colocation market?

What is the estimated market size in terms of area in the Latin America data center colocation market by 2031?

How much MW of power capacity is expected to reach the Latin America data center colocation market by 2031?

What is the estimated market size in terms of area in the Latin America data center colocation market by 2031?

How big is the Latin America data center colocation market?

How much MW of power capacity is expected to reach the Latin America data center colocation market by 2031?

What are the key trends in the Latin America data center colocation market?

What is the growth rate of the Latin America data center colocation market?

What is the growth rate of the Latin America data center colocation market?

How big is the Latin America data center colocation market?

What is the estimated market size in terms of area in the Latin America data center colocation market by 2031?

What are the key trends in the Latin America data center colocation market?

How much MW of power capacity is expected to reach the Latin America data center colocation market by 2031?

What are the key trends in the Latin America data center colocation market?

What is the estimated market size in terms of area in the Latin America data center colocation market by 2031?

How much MW of power capacity is expected to reach the Latin America data center colocation market by 2031?

How big is the Latin America data center colocation market?

What is the growth rate of the Latin America data center colocation market?

For more details, please reach us at [email protected]

For more details, please reach us at [email protected]

Select a license type that suits your business needs

Single User Licence

- Report accessible by one user only

- Free 10% or 3 days of customization

- Free post-sale service assistance

- Continuous support through email

5 User Licence

- Report accessible by 5 users within the organization

- Free 15% or 4.5 days of customization

- Continuous support through email and telephone

- Free analyst hour

- Free Upgrade: If an updated report published within 180 days of purchase, you will get the revised report free of charge

Corporate Licence

- Free Datasheet worth $1500

- Report accessible by the entire organization

- Free 20% or 6 days of customization

- Free post-sale service assistance

- Continuous support through email and telephone

- Direct access to lead analysts

- Free analyst hour

- Free Upgrade: If an updated report published within 180 days of purchase, you will get the revised report free of charge

Datasheet Licence

- Report accessible by 1 user only

- Free 15% or 32 hours of customization

- Free post-sale service assistance

- Direct access to lead analysts

Frequently Asked Questions

How big is the Latin America data center colocation market?

What is the growth rate of the Latin America data center colocation market?

What are the key trends in the Latin America data center colocation market?

What is the estimated market size in terms of area in the Latin America data center colocation market by 2031?

How much MW of power capacity is expected to reach the Latin America data center colocation market by 2031?

What is the estimated market size in terms of area in the Latin America data center colocation market by 2031?

How big is the Latin America data center colocation market?

How much MW of power capacity is expected to reach the Latin America data center colocation market by 2031?

What are the key trends in the Latin America data center colocation market?

What is the growth rate of the Latin America data center colocation market?

What is the growth rate of the Latin America data center colocation market?

How big is the Latin America data center colocation market?

What is the estimated market size in terms of area in the Latin America data center colocation market by 2031?

What are the key trends in the Latin America data center colocation market?

How much MW of power capacity is expected to reach the Latin America data center colocation market by 2031?

What are the key trends in the Latin America data center colocation market?

What is the estimated market size in terms of area in the Latin America data center colocation market by 2031?

How much MW of power capacity is expected to reach the Latin America data center colocation market by 2031?

How big is the Latin America data center colocation market?

What is the growth rate of the Latin America data center colocation market?