Middle East & Africa Data Center Colocation Market – Industry Outlook & Forecast 2026-2031

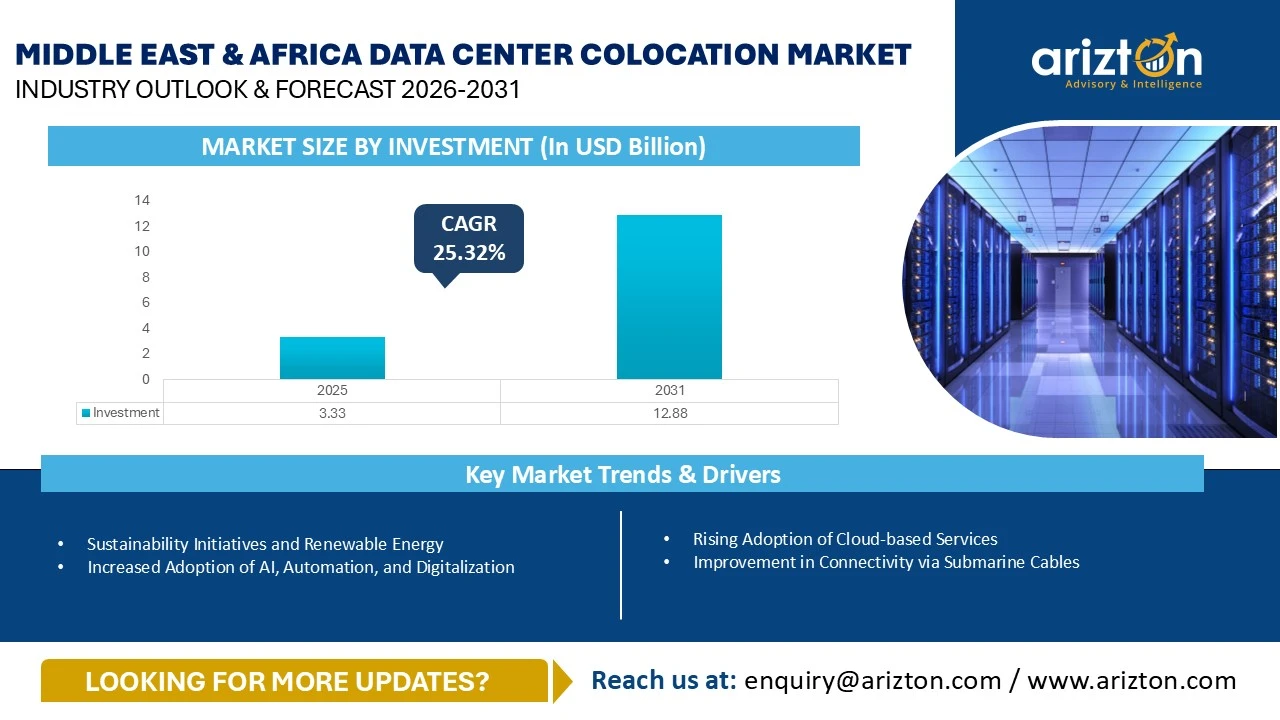

MIDDLE EAST & AFRICA DATA CENTER COLOCATION MARKET SIZE BY INVESTMENT WAS VALUED AT USD 3.33 BILLION IN 2025 AND IS EXPECTED TO REACH USD 12.88 BILLION BY 2031, GROWING AT A CAGR OF 25.32% DURING THE FORECAST PERIOD.

Middle East & Africa Data Center Colocation Market Growth Insights – Market Area to Reach 3.98 Million Sq. Ft. and Power Capacity to Exceed 1,014 MW by 2031, Driven by Cloud Adoption, AI Deployments, Smart City Initiatives, Digital Transformation, and Rising Demand for Scalable Colocation Infrastructure (2026–2031)

Published Date : July 2026

Last Updated : July 2026

format: PDF

edition : Fourth Edition

304 pages

region

countries

57 company

9 segments

Purchase Options

Middle East & Africa Data Center Colocation Market – Industry Outlook & Forecast 2026-2031

MIDDLE EAST & AFRICA DATA CENTER COLOCATION MARKET SIZE BY INVESTMENT WAS VALUED AT USD 3.33 BILLION IN 2025 AND IS EXPECTED TO REACH USD 12.88 BILLION BY 2031, GROWING AT A CAGR OF 25.32% DURING THE FORECAST PERIOD.

The Middle East & Africa Data Center Colocation Market Report Includes

- Colocation Type: Retail Colocation and Wholesale Colocation

- Infrastructure: Electrical Infrastructure, Mechanical Infrastructure, and General Construction

- Electrical Infrastructure: UPS Systems, Generators, Transfer Switches & Switchgear, PDUs, and Other Electrical Infrastructure

- Mechanical Infrastructure: Cooling Systems, Racks, and Other Mechanical Infrastructure

- Cooling Systems: CRAC & CRAH Units, Chiller Units, Cooling Towers, Condensers & Dry Coolers, Economizers & Evaporative Coolers, and Other Cooling Units

- Cooling Techniques: Air-based Cooling and Liquid-based Cooling

- General Construction: Core & Shell Development, Installation & Commissioning Services, Engineering & Building Design, Fire Detection & Suppression, Physical Security, and DCIM/BMS Solutions

- Tier Standard: Tier I & II, Tier III, and Tier IV

- Geography: Middle East (UAE, Saudi Arabia, Israel, Oman, Qatar, Kuwait, Bahrain, and Other Middle Eastern Countries) and Africa (South Africa, Kenya, Nigeria, Egypt, and Other African Countries)

Industry Analysis Report, Regional Outlook, Growth Potential, Price Trends, Competitive Market Share & Forecast 2026–2031

This report includes market data points, ranging from trend

analyses to market estimates & forecasts that you can customize

MIDDLE EAST & AFRICA DATA CENTER COLOCATION MARKET REPORT SCOPE

| REPORT ATTRIBUTE | DETAILS |

|---|---|

| MARKET SIZE BY INVESTMENT 2031 | USD 12.88 Billion |

| MARKET SIZE BY INVESTMENT 2025 | USD 3.33 Billion |

| CAGR - INVESTMENT (2025-2031) | 25.32% |

| MARKET SIZE - COLOCATION REVENUE 2031 | USD 8.63 Billion |

| MARKET SIZE AREA (2031) | 3.98 million sq. feet |

| POWER CAPACITY (2031) | 1,014 MW |

| BASE YEAR | 2025 |

| FORECAST YEAR | 2026-2031 |

| MARKET SEGMENTS | Colocation Service, Infrastructure, Electrical Infrastructure, Mechanical Infrastructure, Cooling Systems, Cooling Techniques, General Construction, Tier Standards, and Geography |

| GEOGRAPHICAL ANALYSIS | Middle East (UAE, Saudi Arabia, Israel, Oman, Qatar, Kuwait, Bahrain, and Other Middle Eastern Countries) and Africa (South Africa, Kenya, Nigeria, Egypt, and Other African Countries) |

MIDDLE EAST & AFRICA DATA CENTER COLOCATION MARKET SIZE

The Middle East & Africa data center colocation market size by investment was valued at USD 3.33 billion in 2025 and is expected to reach USD 12.88 billion by 2031, growing at a CAGR of 25.32% during the forecast period. The demand for colocation data centers in the Middle East & Africa (MEA) is increasing as enterprises and governments accelerate digital transformation through cloud adoption, AI deployments, and smart city initiatives. Colocation provides a cost-effective and scalable alternative to developing private data center facilities. This growth is further supported by economic diversification strategies, rising internet traffic, and favorable government policies.

The Middle East region is expected to account for a significant share of regional data center investments, led by large-scale developments in Saudi Arabia and the UAE. Growth is being fueled by government-backed digital transformation initiatives, continued investments in smart city projects, and increasing demand for digital infrastructure.

Geopolitical conflicts and regional instability may lead to delays in data center construction due to supply chain disruptions, material shortages, and labor constraints. At the same time, the need for resilient and localized digital infrastructure is expected to drive higher investments in data centers across relatively stable markets in the region.

The cost of data center construction in the Middle East and Africa region can range from $6 million to $12 million per MW, depending on the location. These elevated costs are influenced by factors such as limited land availability, high labor rates, inflation, and access to power.

MIDDLE EAST & AFRICA DATA CENTER COLOCATION MARKET TRENDS

Increased Adoption of AI, Automation and Digitalization

- The Middle East and Africa region is accelerating its shift toward AI, automation, and digitization, supported by advances in cloud computing, data centers, and supercomputing capabilities for climate research. The region is leveraging AI to enhance productivity across sectors, while prioritizing renewable energy and sustainable digital solutions.

- AI is set to significantly transform the economy of the UAE, potentially accounting for up to 14% of its GDP by 2030, which is approximately $100 billion (AED 367 billion). The UAE positions itself as a global leader in the AI sector. As the industry gears up for substantial growth, projections suggest that the UAE AI market can reach $50 billion by 2031.

- The South African government continues to invest in AI. For instance, in July 2025, South Africa’s Minister of Science, Technology, and Innovation announced an investment by the country of approximately $28.4 million in AI, blockchain, and other emerging technologies to strengthen foundational digital capabilities in the public sector. In addition, the fund supports the Foundational Digital Capabilities Research (FDCR) platform and the Centre for Artificial Intelligence Research (CAIR) across nine universities located in Cape Town, Pretoria, Stellenbosch, and Sol Plaatje University.

Sustainability Initiatives and Renewable Energy

- Data centers in the Middle East and Africa region are energy-intensive facilities, and sustainability has become an important focus as the region expands its digital infrastructure. Operators are increasingly exploring renewable energy sources such as solar, wind, and hydro power to reduce emissions and operational costs. Several Middle East and African countries have strong renewable potential, which creates opportunities for building greener and more energy-efficient data centers across the continent.

- In September 2025, Kenya launched a new clean energy policy aimed at achieving universal access to green power by 2030 and reaching net-zero carbon emissions by 2050.

- The Egyptian government is making substantial efforts to shift toward sustainability by implementing several sustainability measures to minimize the environmental impact and carbon emissions of the nation. The Egyptian government is committed to generating approximately 12 GW of renewable energy in 2026.

- Data center companies in Turkey are procuring renewable energy to power their facility operations. For instance, Telehouse is committed to powering its entire data center operations with 100% renewable energy.

- In August 2025, Oman Data Park (ODP) announced that it had signed a partnership deal with Solar Wadi to provide solar energy in its data center. The initial phase is likely to generate around 1.4 MW.

MIDDLE EAST & AFRICA DATA CENTER COLOCATION MARKET SEGMENTATION INSIGHTS

- The need for generators in data centers is still high, despite generators being the major contributors to carbon emissions. Africa Data Centres’ Lagos facility maintains 48 hours of diesel backup at full load, supported through agreements with trusted fuel vendors to ensure uninterrupted availability.

- Additionally, several innovative UPS batteries, such as Nickel-Zinc (NiZn) and Sodium-Ion batteries, are gaining traction in the market due to their high-power density, safety, sustainability, and other factors.

- The 42U rack unit is the most used in data centers. Rack units of 45U, 47U, and 48U are mainly installed in large data center environments. A single data center can comprise racks of different sizes. The Riyadh data center facility in Saudi Arabia, operated by NourNet, has been installed with approximately 450 rack cabinets.

- The MEA market is still dominated by conventional air-based systems but is evolving toward hybrid architectures due to climate and density challenges. Overall, MEA is evolving toward a hybrid-to-liquid cooling future, where liquid technologies will play a critical and expanding role in enabling next-generation data center infrastructure.

MIDDLE EAST & AFRICA DATA CENTER COLOCATION MARKET REGIONAL ANALYSIS

- The UAE continues to rank among the most advanced data center markets in the Middle East, supported by accelerating digitalization, proactive government initiatives, high internet and social media penetration, extensive inland and submarine connectivity, as well as a well-defined regulatory framework.

- Saudi Arabia’s data center market is one of the fastest-growing in the Middle East, driven by large-scale digital transformation, hyperscale cloud investments, and strong government support under Vision 2030. The market is in a high-growth, investment-heavy phase, rapidly evolving into a hyperscale, AI-driven digital infrastructure hub supported by strong government policy, global cloud players, and rising data demand.

- In August 2025, Ooredoo inaugurated a new data center and cable landing station in Salalah, Oman, initially offering space for 125 racks with plans to expand to 500 racks. The facility will host the 2Africa subsea cable, strengthen international connectivity, and support the digital infrastructure growth in Oman.

- As of November 2025, South Africa hosts around 11 operational submarine cables. In July 2025, NVIDIA announced the signing of a partnership deal with Cassava Technologies to build AI-ready data centers across African countries such as Egypt, Nigeria, Kenya, and Morocco, for a total investment of around $700 million.

- Nairobi is the top data center destination in Kenya. It continues to be the leading hub for data center expansion in Kenya, marked by a concentrated growth in advanced facilities and dedicated cloud regions. There are eight existing and seven upcoming data centers in Nairobi as of December 2025.

- The number of third-party data center facilities in Nigeria is steadily growing. As an established market within West Africa, Nigeria currently hosts around 20 colocation data centers, with the majority concentrated in Lagos, the country’s primary digital hub.

- Egypt is expected to witness the entry of foreign data center companies as the demand for data center services is increasing gradually in the country. The foreign data center companies are collaborating with the local Egyptian companies to develop data centers in the country.

MIDDLE EAST & AFRICA DATA CENTER COLOCATION MARKET VENDOR LANDSCAPE

- The Middle East and Africa data center market has the presence of key investors such as Africa Data Centres, Bynet Data Communications, Compass Datacenters, DAMAC Digital, Digital Realty, EdgeConneX, Equinix, Gulf Data Hub, Khazna Data Centers, MedOne, MEEZA, Mobily, Nxtra by Airtel, Oman Data Park, Ooredoo, Open Access Data Centres, Orange Business, Quantum Switch, Rack Centre, Raxio Group, Sahayeb Data Centers, Saudi Telecom Company (center3), Serverfarm, Turkcell, Vantage Data Centers and others.

- In 2025, Sahayeb Data Centers was involved in the development of two data center facilities across Riyadh and Dammam, accounting for a combined IT power capacity of around 60 MW as well as covering a total area of around 600 thousand square feet.

- In March 2025, Open Access Data Centres announced its plan to invest around $240 million for the development of a new data center facility in Lagos. The data center will support 24 MW on completion and will be built in two stages. The first phase, with 12 MW, is likely to become operational by 2026.

- New entrants in the region include Agility Logistics Parks, Anan, Cloudoon, DataVolt, Desert Dragon Data Centers, Ezditek, Humain, Kasi Cloud, Mega DC, MultiDC, NED, NEOIX, Pure Data Centres, Qareeb Data Centres, Techtonic and Volt.

- In February 2025, DataVolt announced its plans for the development of a new AI-ready data center facility in Riyadh, Saudi Arabia; the company has planned to develop a Neom data center, with an IT power capacity of around 1.5 GW, in Neom, Saudi Arabia.

SNAPSHOT

The Middle East & Africa data center colocation market by investment is projected to reach USD 12.88 billion by 2031, growing at a CAGR of 25.32% from 2025 to 2031.

The following factors are likely to contribute to the growth of the Middle East & Africa data center colocation market during the forecast period:

- Rising Adoption of Cloud-based Services

- Improvement in Connectivity via Submarine Cables

Base Year: 2025

Forecast Year: 2026-2031

The report considers the present scenario of the Middle East & Africa data center colocation market and its market dynamics for 2026−2031. It covers a detailed overview of several market growth enablers, restraints, and trends. The study includes the demand and supply aspects of the Middle East & Africa data center colocation industry.

Key Data Center Investors

- 21st Century Technologies

- Africa Data Centres

- Bezeq International

- Bynet Data Communications

- Compass Datacenters

- DAMAC Digital

- Digital Parks Africa

- Digital Realty

- du

- e& Egypt

- ECC Solutions

- EdgeConneX

- Equinix

- Global Technical Realty

- GPX Global Systems

- Gulf Data Hub

- iXAfrica Data Centres

- Khazna Data Centers

- MedOne

- MEEZA

- Mobily

- Moro Hub

- MTN

- Nxtra by Airtel

- Oman Data Park

- Ooredoo

- Open Access Data Centres

- Orange Business

- Paratus Namibia

- Quantum Switch

- Rack Centre

- Raxio Group

- Raya Data Center

- Safaricom

- Sahayeb Data Centers

- Saudi Telecom Company (center3)

- Serverfarm

- Telecom Egypt

- Telkom Kenya

- Turkcell

- Vantage Data Centers

New Entrants

- Agility Logistics Parks

- Anan

- Cloudoon

- DataVolt

- Desert Dragon Data Centers

- ezditek

- HUMAIN

- Kasi Cloud

- Mega DC

- MultiDC

- NED

- NEOIX

- Pure Data Centres

- Qareeb Data Centres

- Techtonic

- Volt

Segmentation by Colocation Type

- Retail Colocation

- Wholesale Colocation

Segmentation by Infrastructure

- Electrical Infrastructure

- Mechanical Infrastructure

- General Construction

Segmentation by Electrical Infrastructure

- UPS Systems

- Generators

- Transfer Switches & Switchgear

- PDUs

- Other Electrical Infrastructure

Segmentation by Mechanical Infrastructure

- Cooling Systems

- Racks

- Other Mechanical Infrastructure

Segmentation by Cooling Systems

- CRAC & CRAH Units

- Chiller Units

- Cooling Towers, Condensers & Dry Coolers

- Economizers & Evaporative Coolers

- Other Cooling Units

Segmentation by Cooling Techniques

- Air-based Cooling

- Liquid-based Cooling

Segmentation by General Construction

- Core & Shell Development

- Installation & Commissioning Services

- Engineering & Building Design

- Fire Detection & Suppression

- Physical Security

- DCIM/BMS Solutions

Segmentation by Tier Standard

- Tier I & II

- Tier III

- Tier IV

Segmentation by Geography

- Middle East

- UAE

- Saudi Arabia

- Israel

- Oman

- Qatar

- Kuwait

- Bahrain

- Other Middle Eastern Countries

- Africa

- South Africa

- Kenya

- Nigeria

- Egypt

- Other African Countries

MIDDLE EAST & AFRICA DATA CENTER COLOCATION MARKET FAQs

How big is the Middle East and Africa data center colocation market?

What is the growth rate of the Middle East and Africa data center colocation market?

What are the key trends in the Middle East and Africa data center colocation market?

What is the estimated market size in terms of area in the Middle East and Africa data center colocation market by 2031?

Q: How much MW of power capacity is expected to reach the Middle East data center market by 2031?

How much MW of power capacity is expected to reach the Middle East data center market by 2031?

For more details, please reach us at [email protected]

For more details, please reach us at [email protected]

Select a license type that suits your business needs

Single User Licence

- Report accessible by one user only

- Free 10% or 3 days of customization

- Free post-sale service assistance

- Continuous support through email

5 User Licence

- Report accessible by 5 users within the organization

- Free 15% or 4.5 days of customization

- Continuous support through email and telephone

- Free analyst hour

- Free Upgrade: If an updated report published within 180 days of purchase, you will get the revised report free of charge

Corporate Licence

- Free Datasheet worth $1500

- Report accessible by the entire organization

- Free 20% or 6 days of customization

- Free post-sale service assistance

- Continuous support through email and telephone

- Direct access to lead analysts

- Free analyst hour

- Free Upgrade: If an updated report published within 180 days of purchase, you will get the revised report free of charge

Datasheet Licence

- Report accessible by 1 user only

- Free 15% or 32 hours of customization

- Free post-sale service assistance

- Direct access to lead analysts

Frequently Asked Questions

How big is the Middle East and Africa data center colocation market?

What is the growth rate of the Middle East and Africa data center colocation market?

What are the key trends in the Middle East and Africa data center colocation market?

What is the estimated market size in terms of area in the Middle East and Africa data center colocation market by 2031?

Q: How much MW of power capacity is expected to reach the Middle East data center market by 2031?

How much MW of power capacity is expected to reach the Middle East data center market by 2031?

Other RELATED Reports

Middle East and Africa Data Center Construction Market – Industry Outlook & Forecast 2026-2031

Published : June 2026