Global Precision Agriculture Market Research Report 2026-2031

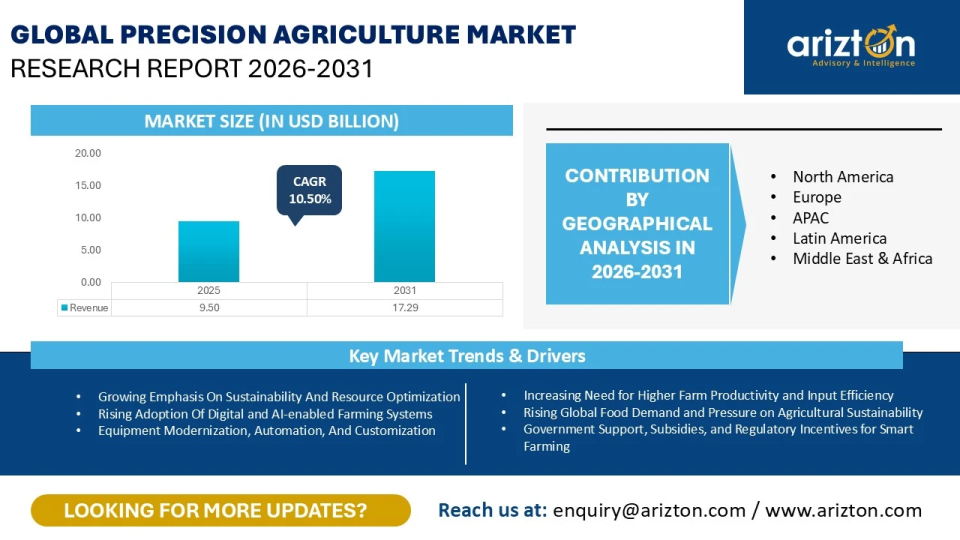

THE GLOBAL PRECISION AGRICULTURE MARKET WAS VALUED AT USD 9.50 BILLION IN 2025 AND IS EXPECTED TO REACH USD 17.29 BILLION BY 2031, GROWING AT A CAGR OF 10.50%.

The Precision Agriculture Market Size, Share, & Trends By Component, Hardware, Software, Technology, Application, Farm Size, & Geography - Industry Analysis Report, Regional Outlook, Growth, Competitive Market Share & Forecast 2031.

Published Date : March 2026

Last Updated : March 2026

format: PDF

edition : Second Edition

229 pages

5 region

24 countries

38 company

07 segments

Purchase Options

Global Precision Agriculture Market Research Report 2026-2031

THE GLOBAL PRECISION AGRICULTURE MARKET WAS VALUED AT USD 9.50 BILLION IN 2025 AND IS EXPECTED TO REACH USD 17.29 BILLION BY 2031, GROWING AT A CAGR OF 10.50%.

The Precision Agriculture Market Size, Share, & Trends Analysis Report By

- Component: Hardware and Software

- Hardware: Guidance & Steering Systems, Field Sensing & Monitoring Devices, Imaging & Remote-Sensing, Variable-Rate Application (VRT) Equipment, Precision Irrigation Equipment, Robotics & Autonomous Machinery, and Others

- Software: Farm Management Software (FMS), Mapping, GIS & Remote Sensing Software, VRT & Prescription Software, Telematics & Fleet Management Platforms, AI, Analytics & Forecasting Tools, and Others

- Technology: Guidance & Navigation Technologies, Field Sensing Technologies, Remote Sensing Technologies, Data & Analytics Technologies, Automation & Robotics Technologies, and Others

- Application: Precision Crop Farming, Precision Livestock Management, Smart Greenhouse Management, Precision Forestry, and Others

- Farm Size: Large Farms, Medium Farms, and Small Farms

- Geography: North America, Europe, APAC, Latin America, and Middle East & Africa

Industry Analysis Report, Regional Outlook, Growth Potential, Price Trends, Competitive Market Share & Forecast 2026–2031.

This report includes market data points, ranging from trend

analyses to market estimates & forecasts that you can customize

PRECISION AGRICULTURE MARKET REPORT SCOPE

| REPORT ATTRIBUTE | DETAILS |

|---|---|

| MARKET SIZE (2031) | USD 17.29 Billion |

| MARKET SIZE (2025) | USD 9.50 Billion |

| CAGR (2025-2031) | 10.50% |

| HISTORIC YEAR | 2022-2024 |

| BASE YEAR | 2025 |

| FORECAST YEAR | 2026-2031 |

| SEGMENTS BY | Component, Hardware, Software, Technology, Application, Farm Size, and Geography |

| GEOGRAPHIC ANALYSIS | North America, Europe, APAC, Latin America, and Middle East & Africa |

| KEY PLAYERS | Deere & Company, AGCO Corporation, CNH Industrial, Trimble, Topcon, Bayer, CLAAS, and Kubota Corporation |

PRECISION AGRICULTURE MARKET SIZE & SHARE

The global precision agriculture market size was valued at USD 9.50 billion in 2025 and is expected to reach USD 17.29 billion by 2031, growing at a CAGR of 10.50% during the forecast period. Precision agriculture is evolving from a set of niche tools into a connected operating layer for farms. The market is coalescing around platforms that combine GNSS guidance, sensing, imaging, and farm management software into unified workflows, helping growers turn field data into actionable, season-long decisions rather than isolated input adjustments.

Precision agriculture solutions integrate GNSS guidance, IoT sensors, soil and crop monitoring, imaging systems, drones, analytics platforms, and variable rate technologies to enable site-specific decision-making. These tools help optimise fertiliser, pesticide, seed, and water use, lowering operating costs and improving yields, sustainability metrics, and resource efficiency.

Global environmental pressures are accelerating the shift toward climate-smart farming. Agriculture accounts for a dominant share of freshwater extraction and a significant portion of global greenhouse gas emissions. Governments are responding through initiatives such as the EU Common Agricultural Policy, the US Climate-Smart Commodities programme, India’s Digital Agriculture Mission, and China’s Smart Agriculture Five-Year Plan, all of which encourage wider adoption of digital field monitoring and automated input management.

Digitisation is now a core operating layer of modern farm operations. High-resolution imagery, weather intelligence, soil data, and equipment telematics now feed into integrated platforms supported by AI, edge analytics, and cloud connectivity. Adoption is advancing rapidly in North America and Europe, where farms already use precision-enabled machinery including GPS-guided tractors, automated sprayers, yield-monitoring harvesters, and smart irrigation systems. In Asia Pacific and Latin America, growth is driven by targeted subsidies, digital agronomy services, and the availability of affordable sensors and mobile-based farm management tools for small and mid-scale growers.

PRECISION AGRICULTURE MARKET TRENDS & DRIVERS

- Rising AI-enabled agronomy is gaining pace as farms combine decision support, remote sensing, and variable rate application to refine field-level choices. Earth observation programs such as the EU Copernicus Sentinel missions and NASA Landsat strengthen imagery availability for crop vigor and stress mapping, while platforms such as John Deere Operations Center, Climate FieldView, and Trimble agriculture tools connect equipment and agronomic data into a unified workflow. The result is stronger forecasting, lower input leakage, and more repeatable yield outcomes.

- Sustainability priorities are reinforcing digital adoption as growers pursue water-efficient irrigation, nutrient optimization, and climate-smart production. Frameworks such as FAO Climate Smart Agriculture and the EU Farm to Fork strategy are shaping expectations around input efficiency and environmental performance, while EU Common Agricultural Policy eco schemes encourage practices that can be monitored and validated. Precision monitoring supports targeted applications, improves soil stewardship, and helps track progress toward lower-impact operations.

- Rising input costs and yield variability are strengthening the case for technologies that improve application accuracy and operational efficiency. Guidance, section control, and variable rate seeding and fertilization help align inputs with soil and crop needs, reducing waste while protecting margin. In parallel, public and industry initiatives such as the USDA Partnerships for Climate Smart Commodities accelerate measurement and data readiness, supporting wider deployment of digital field management.

- Food system resilience goals are increasing attention on scalable approaches that raise output while conserving resources. Precision agriculture supports this shift through soil health sensing, irrigation scheduling, and responsible nutrient management that aligns with supply chain requirements for traceability and lower footprint practices. As government programs, processors, and vendors expand climate and sustainability targets, demand is rising for tools that convert field data into practical actions and documented outcomes.

INDUSTRY RESTRAINTS

Upfront investment remains a material hurdle as precision agriculture increasingly depends on higher-cost hardware such as GNSS guidance, variable rate application systems, camera-based machine vision systems for precision targeting, drones, and autonomous-capable tractors. For small and mid-sized farms, payback timelines can appear uncertain when yields fluctuate and input prices move quickly, while recurring software and data subscriptions add ongoing cost. Although initiatives such as the EU Common Agricultural Policy rural development measures, and the USDA NRCS Environmental Quality Incentives Program can support modernization, access and relevance differ by region and farming practice, so affordability remains uneven.

PRECISION AGRICULTURE MARKET SEGMENTATION INSIGHTS

INSIGHT BY COMPONENT

The global precision agriculture market by component is segmented into hardware and software. The hardware segment accounted for the largest market share of around 74%. Hardware components represent the physical infrastructure deployed on farms to capture field, crop, livestock, and environmental data and to execute precision actions such as variable-rate input application, automated steering, sensing, and controlled irrigation. These systems directly interact with land, crops, animals, and machinery.

Adoption at the component level is strongest in large and highly mechanized farming systems, where execution accuracy has a direct impact on costs and yields. In 2024, USDA research shows that yield monitors, yield maps, and soil maps are used on 68% of large crop-producing farms, indicating that core precision hardware is no longer experimental but embedded in commercial-scale operations, thus helping segmental growth.

INSIGHT BY HARDWARE

Based on the hardware, the guidance and steering systems dominates and holds the largest global precision agriculture market share in 2025. Guidance and steering systems form the execution backbone of precision agriculture because they convert positioning intelligence into repeatable machine movement. They are typically the first precision capability scaled across fleets due to immediate operational benefits in planting, spraying, and harvesting.

Furthermore, the growth is reflected by a high repeatability value across field passes through execution consistency and operational discipline, packaged in practical field-ready stacks such as John Deere AutoTrac from John Deere. Accuracy and mixed implement compatibility are strengthened through correction services such as CenterPoint RTX from Trimble and interoperability expectations anchored in International Organization for Standardization 11783.

INSIGHT BY SOFTWARE

Based on the software, the farm management software at a CAGR of 10.37% is supported by the need for a single operational record that connects fields, jobs, and outcomes across the crop year, especially as farms manage more variability and tighter documentation expectations. John Deere Operations Center is explicitly positioned as an online farm management system designed to provide access to farm information across devices, reinforcing sustained budget priority for this subsegment as the farm’s central system of record and day-to-day workflow hub.

Mapping, GIS and remote sensing software hold a significant global precision agriculture market share in 2025, reflecting its role as the visual interface that converts field variability into decisions, with scouting, zoning, and prescriptions frequently initiated in a map layer before moving into execution. Esri ArcGIS positions agriculture use cases around integrating earth observations, imagery, field data, and real-time streams in one system, and agriculture-focused models, such as field delineation workflows, illustrate how mapping environments continue absorbing more of the imagery into the decision pipeline as remote sensing volumes rise.

INSIGHT BY TECHNOLOGY

By technology, the remote sensing technologies segment shows significant growth, with the fastest-growing CAGR during the forecast period. Remote sensing technologies provide field-scale measurement by translating spectral, thermal, and structural crop responses into actionable signals. Spectral observations support vegetation vigor and stress assessment, thermal sensing informs water and evapotranspiration conditions, and structural analysis highlights canopy gaps and biomass distribution. These capabilities are increasingly delivered through multispectral and thermal payloads deployed via satellites and drones for routine crop monitoring.

Platform choice reflects trade-offs between coverage, resolution, and timing. Satellite systems enable consistent, large-area monitoring across seasons, while drones deliver greater spatial detail for targeted field decisions. Copernicus Sentinel-2 specifications highlight 13 spectral bands with 10–60-meter resolution and a five-day revisit cycle, supporting repeatable crop health tracking at field and regional scale without custom deployment.

INSIGHT BY APPLICATION

The precision crop farming segment accounted for the largest global precision agriculture market share. Precision crop farming reflects the concentration of high-frequency operational decisions in planting, spraying, and nutrient placement that create continuous opportunities for optimization at the field scale, reinforced by targeted application platforms such as John Deere See and Spray and input placement upgrades such as ExactShot.

Execution in precision crop farming depends on a coordinated dependency chain rather than advanced analytics alone. Accurate field boundary mapping, guidance-grade positioning systems, controllable implements, integrated prescription workflows, and traceable operational records must work in unison to translate digital decisions into measurable field outcomes. As a result, interoperability and data continuity are becoming critical growth enablers across precision crop farming segments, particularly in mixed fleets and multi-operator environments, where standardized processes across equipment and teams determine the scalability of precision practices beyond isolated fields.

INSIGHT BY FARM SIZE

The global precision agriculture market by farm size is segregated into large farms, medium farms, and small farms. The large farm segment accounted for the largest market share in 2025. The large farms reflect faster scale-up across equipment fleets and multi-field operations, with higher utilization across machine hours and more standardized execution across planting, application, and harvest. USDA Economic Research Service analysis using ARMS data shows precision agriculture adoption rises sharply with farm size, reinforcing the concentration of spending and deployments in the large farm cohort.

Larger farms typically deploy precision technologies across multiple operations to support scale efficiency, workflow coordination, and execution consistency, while medium and small farms adopt precision solutions selectively to improve operational accuracy and resource utilization.

Technology preferences on large farms emphasize deep OEM integration and fleet-level reliability because uptime and predictability outweigh experimentation. Positioning architectures are selected for stability across variable field conditions and seamless in-cab control. In Europe and North America, guidance-grade GNSS has become embedded within new machinery ecosystems, reinforcing navigation accuracy as a baseline expectation rather than a premium enhancement.

PRECISION AGRICULTURE MARKET GEOGRAPHICAL ANALYSIS

In 2025, North America accounts for over 35% share of the global precision agriculture market, supported by large scale row crop operations and strong equipment penetration that strengthen the unit economics of automation, telemetry, and variable rate execution. Connectivity policy adds further momentum, with Federal Communications Commission programs such as the Rural Digital Opportunity Fund expanding rural broadband buildout, and the FCC Precision Agriculture Task Force emphasizing broadband availability across agricultural lands as an adoption enabler.

Within North America, the US holds the major market share, aligned with incentive structures that reward measurable outcomes, traceability, and practice adoption, which lifts demand for monitoring and verification capabilities across precision agriculture deployments. U.S. Department of Agriculture programs such as Partnerships for Climate-Smart Commodities reinforced the role of MRV in program design, and the April 2025 restructuring into Advancing Markets for Producers sharpened the focus on producer benefit and implementable delivery at scale. Canada is positioned for the highest regional growth over 2025–2031, supported by continued modernization and enabling connectivity that improves deployment readiness for connected tools.

APAC leads growth, with the highest CAGR of 11.25% during the forecast period, as governments advance from pilots to scaled deployment and invest in data and infrastructure foundations that support consistent implementation. In Japan, the Ministry of Agriculture, Forestry and Fisheries reports smart agriculture demonstrations across 217 districts, creating a clear pathway from field validation to broader adoption. In South Korea, the Smart Farm Innovation Valley cluster model formalizes training, incubation, and commercialization linkages that accelerate the rollout of smart farm systems. In Australia, the Digital Foundations for Agriculture Strategy sets a national direction around digital uptake, data governance, and connectivity as core enablers for industry-wide scaling.

PRECISION AGRICULTURE MARKET COMPETITIVE LANDSCAPE

The global precision agriculture market remains structurally fragmented, shaped by a mix of multinational OEMs, specialized technology providers, regional system integrators, and a growing layer of software-first agritech firms. While large equipment manufacturers anchor the competitive landscape, a long tail of niche vendors supplying sensors, connectivity modules, analytics platforms, and application-specific solutions sustains high competitive intensity across regions.

Competition is increasingly defined by ecosystem depth rather than standalone products. Leading players such as John Deere, AGCO, CNH Industrial, Trimble, and Topcon are expanding through integrated hardware-software stacks, OEM partnerships, and open digital platforms that lock in data flows across the farm lifecycle. This contrasts with smaller vendors that compete on single-function solutions such as guidance, variable-rate control, sensing, or farm management software.

Regional dynamics strongly influence competitive positioning. North America and Europe are characterized by higher consolidation and OEM-led ecosystems, supported by strong dealer networks, interoperability standards, and regulatory alignment around sustainability and traceability. In contrast, Asia-Pacific and Latin America exhibit more fragmented structures, where local integrators, distributors, and service-led models play a critical role in adapting precision solutions to diverse farm sizes, crops, and connectivity conditions.

Barriers to scale are increasingly non-manufacturing in nature. Access to agronomic datasets, digital talent, cybersecurity compliance, and trusted distribution networks now matters as much as engineering capability. As a result, partnerships with input suppliers, cooperatives, insurers, and financial institutions are emerging as a key competitive lever, particularly in emerging markets.

Recent Developments in the Precision Agriculture Market

- In May 2025, John Deere acquired Sentera, a drone-imagery and agronomic analytics provider, to deepen integration of aerial scouting data into the John Deere Operations Center. The move strengthens Deere’s ability to convert high-resolution field imagery into in-season prescriptions and decision workflows, complementing precision offerings such as targeted spraying and digital agronomy toolchains.

- In January 2025, Lindsay Corporation completed the acquisition of a 49.9 % minority stake in Pessl Instruments, expanding its precision irrigation and on-farm sensing portfolio. The integration of FieldNET / FieldNET Advisor with METOS weather stations, soil probes, and FieldClimate tools reinforces Lindsay’s strategy to couple connected irrigation control with agronomic intelligence and AI-led product development.

- In March 2025, Orbia Netafim partnered with Virridy to launch a carbon credit program in Turkey, starting with over 1,000 hectares and targeting at least 3.5 tons of CO₂e per hectare per year reduction. By pairing precision irrigation with digital monitoring, reporting, and verification, the initiative positions carbon finance as a scalable lever for the adoption of water-efficient precision practices in irrigated regions.

- In February 2025, Orbia Netafim unveiled its patented Hybrid Dripline, positioned as the first integral dripline with a built-in outlet that combines the benefits of integral and on-line dripper systems. The product targets labour and reliability constraints in orchards, vineyards, and protected crops by reducing manual installation steps while improving clog resistance and consistent distribution under variable water-quality conditions.

- In January 2025, Valley Irrigation (Valmont) announced a strategic consolidation of multiple technology platforms into the AgSense 365 app to streamline digital irrigation management. The consolidation is designed to reduce platform fragmentation for growers and accelerate the adoption of unified, app-centric irrigation operations and scheduling workflows across Valley’s installed base.

SNAPSHOT

The global precision agriculture market size is expected to grow at a CAGR of approximately 9.02% from 2025 to 2031.

The following factors are likely to contribute to the growth of the global precision agriculture market during the forecast period:

- Increasing Need for Higher Farm Productivity and Input Efficiency

- Rising Global Food Demand and Pressure on Agricultural Sustainability

- Government Support, Subsidies, and Regulatory Incentives for Smart Farming

- Expansion of Connectivity Infrastructure and Digital Agriculture Ecosystems

Base Year: 2025

Forecast Year: 2026-2031

The report examines the current state of the global precision agriculture market and its market dynamics through 2026−2031. It covers a detailed overview of several market growth enablers, restraints, and trends. The study covers both the demand and supply sides of the market. It also profiles and analyses leading companies and several other prominent companies operating in the market.

Key Company Profile

- Deere & Company

- Business Overview

- Product Offerings

- Key Developments

- Key Strategies

- Key Strengths

- Key Opportunities

- AGCO Corporation

- CNH Industrial

- Trimble

- Topcon

- Bayer

- CLAAS

- Kubota Corporation

Other Prominent Company Profile

- DJI Agriculture

- Business Overview

- Product Offerings

- AG Leader Technology

- Netafim

- Valley Irrigation

- Lindsay Corporation

- Hexagon

- Jain Irrigation Systems Ltd.

- Rivulis

- Corteva Agriscience

- Xarvio

- Sentera

- Monarch

- DICKEY-john

- Carbon Robotics

- FarmWise

- AgXeed

- AGRIVI

- CropX

- Arable

- METOS

- Proagrica

- DeLaval

- AquaSpy

- Davis Instruments

- YANMAR Holdings

- TeeJet Technologies

- Yara

- Valmont

- Raven

- Precision Planting

Segmentation by Component

- Hardware

- Software

Segmentation by Hardware

- Guidance & Steering Systems

- Field Sensing & Monitoring Devices

- Imaging & Remote-Sensing

- Variable-Rate Application (VRT) Equipment

- Precision Irrigation Equipment

- Robotics & Autonomous Machinery

- Others

Segmentation by Software

- Farm Management Software (FMS)

- Mapping, GIS & Remote Sensing Software

- VRT & Prescription Software

- Telematics & Fleet Management Platforms

- AI, Analytics & Forecasting Tools

- Others

Segmentation by Technology

- Guidance & Navigation Technologies

- Field Sensing Technologies

- Remote Sensing Technologies

- Data & Analytics Technologies

- Automation & Robotics Technologies

- Others

Segmentation by Application

- Precision Crop Farming

- Precision Livestock Management

- Smart Greenhouse Management

- Precision Forestry

- Others

Segmentation by Farm Size

- Large Farms

- Medium Farms

- Small Farms

Segmentation by Geography

- APAC

- China

- India

- Japan

- South Korea

- Australia

- Indonesia

- Thailand

- North America

- U.S.

- Canada

- Europe

- France

- Germany

- Spain

- UK

- Italy

- Netherlands

- Sweden

- Switzerland

- Belgium

- Latin America

- Brazil

- Mexico

- Argentina

- Middle East & Africa

- UAE

- South Africa

- Saudi Arabia

PRECISION AGRICULTURE MARKET FAQs

What is the growth rate of the global precision agriculture market?

How big is the global precision agriculture market?

Which region dominates the global precision agriculture market?

What are the key trends in the global precision agriculture market?

Who are the major players in the global precision agriculture market?

For more details, please reach us at [email protected]

- Chapter 1- Scope & Coverage

- Market Definition

- Inclusion

- Exclusions

- Market Estimation Caveats

- Market Derivation

- Market Segmentation by Component

- Market Segmentation by Hardware

- Market Segmentation by Software

- Market Segmentation by Technology

- Market Segmentation by Application

- Market Segmentation by Farm Size

- Chapter 2- Premium Insights

- Chapter 3- Market Dynamics

- Introduction

- Precision Agriculture Categorization

- Technologies used in Field and Specialty Crops

- Digital Twins in Precision Agriculture

- Value Chain Analysis

- Technology Architecture & Integration

- AI Agronomy Copilots Simplifying Data-Driven Farming Decisions

- Deep-tech Innovation Shaping Precision Agriculture

- Government Regulations Promoting Precision Agriculture

- Platform Consolidation in Precision Agriculture

- Market Opportunities & Trends

- Rising Adoption of Digital and AI-Enabled Farming Systems

- Growing Emphasis on Sustainability and Resource Optimization

- Equipment Modernization, Automation, and Customization

- Advancements in Robotics, Drones, and Autonomous Farm Machinery

- Expansion of IoT-Integrated Monitoring and Predictive Analytics Platforms

- Market Growth Enablers

- Increasing Need for Higher Farm Productivity and Input Efficiency

- Rising Global Food Demand and Pressure on Agricultural Sustainability

- Government Support, Subsidies, and Regulatory Incentives for Smart Farming

- Expansion of Connectivity Infrastructure and Digital Agriculture Ecosystems

- Market Restraints

- High Upfront Costs and Limited Affordability for Small and Medium Farms

- Connectivity, Infrastructure, and Data Accessibility Challenges

- Operational Complexity, Skills Gaps, and Low Technology Readiness

- Fragmented Ecosystem and Poor Interoperability

- Market Landscape

- Five Forces Analysis

- Chapter 4- Market Segmentation

- Component (Market Size & Forecast: 2022-2031)

- Hardware

- Software

- Hardware (Market Size & Forecast: 2022-2031)

- Guidance & Steering Systems

- Field Sensing & Monitoring Devices

- Imaging & Remote-Sensing

- Variable-Rate Application (VRT) Equipment

- Precision Irrigation Equipment

- Robotics & Autonomous Machinery

- Others

- Software (Market Size & Forecast: 2022-2031)

- Farm Management Software (FMS)

- Mapping, GIS & Remote Sensing Software

- VRT & Prescription Software

- Telematics & Fleet Management Platforms

- AI, Analytics & Forecasting Tools

- Others

- Technology (Market Size & Forecast: 2022-2031)

- Guidance & Navigation Technologies

- Field Sensing Technologies

- Remote Sensing Technologies

- Data & Analytics Technologies

- Automation & Robotics Technologies

- Others

- Application (Market Size & Forecast: 2022-2031)

- Precision Crop Farming

- Precision Livestock Management

- Smart Greenhouse Management

- Precision Forestry

- Others

- Farm Size (Market Size & Forecast: 2022-2031)

- Large Farms

- Medium Farms

- Small Farms

- Chapter 5- Geography Segmentation

- Geography Segmentation (Market Size & Forecast: 2022-2031)

- Geographic Overview – Market Maturity Index

- APAC

- China

- India

- Japan

- South Korea

- Australia

- Indonesia

- Thailand

- North America

- US

- Canada

- Europe

- France

- Germany

- Spain

- UK

- Italy

- Netherlands

- Sweden

- Switzerland

- Belgium

- Latin America

- Brazil

- Mexico

- Argentina

- MEA

- UAE

- South Africa

- Saudi Arabia

- Chapter 6- Competitive Landscape

- Competitive Landscape

- Competition Overview

- Key Developments

- Key Company Profiles

- Other Prominent Company Profiles

- Report Summary

- Key Takeaways

- Strategic Recommendations

Select a license type that suits your business needs

Single User Licence

- Report accessible by one user only

- Free 10% or 3 days of customization

- Free post-sale service assistance

- Continuous support through email

5 User Licence

- Report accessible by 5 users within the organization

- Free 15% or 4.5 days of customization

- Continuous support through email and telephone

- Free analyst hour

- Free Upgrade: If an updated report published within 180 days of purchase, you will get the revised report free of charge

Corporate Licence

- Free Datasheet worth $1500

- Report accessible by the entire organization

- Free 20% or 6 days of customization

- Free post-sale service assistance

- Continuous support through email and telephone

- Direct access to lead analysts

- Free analyst hour

- Free Upgrade: If an updated report published within 180 days of purchase, you will get the revised report free of charge

Datasheet Licence

- Report accessible by 1 user only

- Free 15% or 32 hours of customization

- Free post-sale service assistance

- Direct access to lead analysts

Frequently Asked Questions

What is the growth rate of the global precision agriculture market?

How big is the global precision agriculture market?

Which region dominates the global precision agriculture market?

What are the key trends in the global precision agriculture market?

Who are the major players in the global precision agriculture market?