Global Pro AV Market Research Report 2025–2030

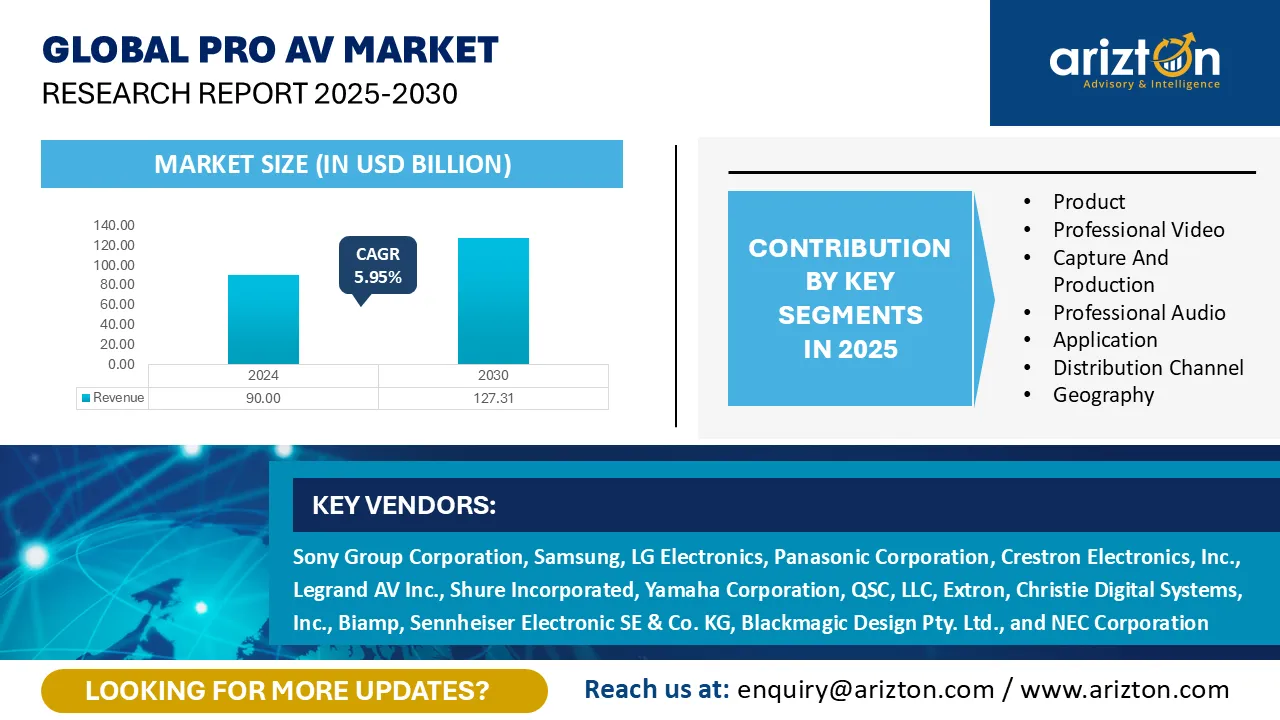

THE GLOBAL PRO AV MARKET SIZE IS EXPECTED TO REACH USD 127.31 BILLION BY 2030 FROM USD 90.00 BILLION IN 2024, GROWING AT A CAGR OF 5.95% DURING THE FORECAST PERIOD.

Pro AV Market Size & Share By Product, By Professional Video, By Capture And Production, By Professional Audio, By Application, By Distribution Channel, By Geography. This Industry Analysis Covers the Market Size (in USD Million) for All the Above Segment

Published Date : October 2025

Last Updated : October 2025

format: PDF

edition : Second Edition

230 pages

51 company

07 segments

5 region

24 countries

Purchase Options

Global Pro AV Market Research Report 2025–2030

THE GLOBAL PRO AV MARKET SIZE IS EXPECTED TO REACH USD 127.31 BILLION BY 2030 FROM USD 90.00 BILLION IN 2024, GROWING AT A CAGR OF 5.95% DURING THE FORECAST PERIOD.

The Global Pro AV Market Size, Share, & Trends Analysis Report By

- Product: Professional Video and Professional Audio

- Professional Video: Video Displays, Capture and Production, Video Projection, and Others

- Capture And Production: Broadcast & Video Production, Enterprise – Fortune 500, Government Bodies, Higher Education, Healthcare, Sports, Worship & Non-Profit, K–12 Education, Museums, Themed Entertainment, and Others

- Professional Audio: Microphones, Pro Speakers, Sound Mixers, Signal Processors, Power Amplifiers, and Others

- Application: Corporates, Media & Entertainment, Venues & Events, Educational Institutions, Government & Military, Retail, Transportation, Hospitality, and Others

- Distribution Channel: Offline and Online

- Geography: North America, Europe, APAC, Latin America, and Middle East & Africa

Industry Analysis Report, Regional Outlook, Growth Potential, Price Trends, Competitive Market Share & Forecast 2025–2030.

This report includes market data points, ranging from trend

analyses to market estimates & forecasts that you can customize

PRO AV MARKET REPORT SCOPE

| REPORT ATTRIBUTE | DETAILS |

|---|---|

| Market Size (2030) | USD 127.31 Billion |

| Market Size (2024) | USD 90.00 Billion |

| CAGR (2024-2030) | 5.95% |

| HISTORIC YEAR | 2021-2023 |

| BASE YEAR | 2024 |

| FORECAST YEAR | 2025-2030 |

| SEGMENTS BY | Product, Professional Video, Capture And Production, Professional Audio, Application, Distribution Channel, and Geography |

| LARGEST REGION (2024) | APAC |

| GEOGRAPHIC ANALYSIS | North America, Europe, APAC, Latin America, and Middle East & Africa |

| KEY PLAYERS | Sony Group Corporation, Samsung, LG Electronics, Panasonic Corporation, Crestron Electronics, Inc., Legrand AV Inc., Shure Incorporated, Yamaha Corporation, QSC, LLC, Extron, Christie Digital Systems, Inc., Biamp, Sennheiser Electronic SE & Co. KG, Blackmagic Design Pty. Ltd., and NEC Corporation |

PRO AV MARKET SIZE & OVERVIEW

The global pro AV market was valued at USD 90.00 billion in 2024 and is expected to reach USD 127.31 billion by 2030, growing at a CAGR of 5.95% during the forecast period. The market growth is driven by flexible work environments, rising demand for immersive experiences, and increased engagement with video and audio content across end-users. In this landscape, the professional video segment is set for substantial growth and is predicted to surpass USD 90 billion by 2030. This growth is driven by greater adoption in broadcasting, enterprise communication, and live event streaming, as organizations increasingly prioritize high-quality video solutions to enhance audience engagement, ensure seamless remote collaboration, and meet the rising demand for real-time content delivery. Also, video solutions 4K/8K displays, PTZ cameras, and AV-over-IP encoders are all high-performance video tools that are in high demand within corporate, education, healthcare, and government environments. This demand stems from the need for high-resolution content and low-latency transmission.

As AV systems become more advanced, costs can be two to four times higher than standard systems. These systems often need specialized integration, acoustic calibration, and ongoing support. To reduce complexity, integrators are increasingly using simulation tools, modular platforms, and centralized device management systems. Furthermore, there is also a clear shift toward integrated AV ecosystems that provide unified control, real-time analytics, edge processing, and remote device management. Auto-framing, beamforming microphones, and AI-powered voice tracking functionality are making systems smarter and creating greater user experiences.

Upholding a high continuity of operations, low latency, and signal integrity is increasingly becoming important, particularly in critical environments such as command centers and live operational fields (e.g., broadcast, defense, or emergency response). In such settings, continuous monitoring and proactive system checks play a crucial role in the success and continuity of operations with minimum latency.

Regionally, North America is among the leaders in the global pro AV market, backed by strong institutional and enterprise spending in the United States. At the same time, the fastest-growing market is anticipated to be APAC because of the growing use of digital content in China, India, and Southeast Asia. Also, leading manufacturers in the pro AV market, such as Crestron, Samsung, and Sony, are actively expanding their product offerings and vertical integrations. For instance, Barco is improving its immersive display solutions, while audio companies like QSC and Shure are investing in AV-over-IP interoperability to enhance ecosystem compatibility.

IMPACT OF US & CHINA TRADE WAR

The US-China trade war escalated in January 2025, which resulted in higher tariffs on Pro AV imports, including displays, projectors, audio processors, and networking components. This raised procurement costs for integrators and end-users relying on Chinese and Taiwanese suppliers. Many manufacturers started shifting sourcing to Southeast Asia and Latin America, but these adjustments created moderate shipment delays that disrupted delivery schedules for large venue installations and enterprise AV projects across key US markets.

In addition, US-India trade tensions intensified after tariffs on Indian exports were raised to 50% in August 2025, directly impacting specialized cabling, accessory components, and metal enclosures such as racks, chassis, and protective casings used in AV systems. Companies are either absorbing these extra costs or moving their sourcing to other regions, which complicates inventory planning and affects project timelines. Overall, the pro AV market is dealing with ongoing cost pressures and supply chain changes in 2025. These factors are influencing pricing strategies, procurement cycles, and the availability of professional-grade equipment.

PRO AV MARKET TRENDS & DRIVERS

- Smart and connected learning environments are accelerating the adoption of interactive displays, lecture capture, and AV-over-IP systems in schools and universities. These solutions improve hybrid teaching, expand digital classrooms, and support education sectors that are investing heavily in modernization. Such factors are projected to impact the pro AV market positively.

- Next-generation digital signage and experiential AV are changing retail, airports, and entertainment venues with immersive projection, LED walls, and interactive displays. They drive customer engagement, efficient advertising, and seamless wayfinding across high-traffic commercial environments.

- AI and automation-powered AV systems simplify meeting-room experiences with automatic camera tracking, voice recognition, and touchless controls. These capabilities help businesses reduce setup time, minimize IT intervention, and enable smoother collaboration between remote and in-office teams.

- Cloud-driven Pro AV platforms enable centralized monitoring, remote troubleshooting, and scalable content delivery across distributed sites. Institutions and corporations adopt them for cost savings, higher functioning time, and flexible integration with IT-led infrastructures.

- Rising demand for event-driven AV is boosting rental services, staging solutions, and live production technologies for concerts, sports, and exhibitions. Large-scale events need immersive displays, real-time broadcasting, and reliable sound reinforcement.

- Adoption of AV-as-a-Service and subscription-based models is growing among enterprises seeking flexible procurement in the pro AV market. This change reduces upfront costs, offers predictable operating expenses, and ensures ongoing access to the latest AV technologies.

INDUSTRY RESTRAINTS

High capital and operational costs limit the growth of the pro AV market, especially for small businesses and schools with tight budgets. The expenses for installation, integration, and frequent upgrades discourage long-term investment, even as demand for modern AV solutions grows. Moreover, a lack of skilled AV professionals and certified integrators slows down deployment and impacts system reliability. Many areas experience training gaps, resulting in delays for large installations and higher costs for specialized labor.

Interoperability issues and vendor lock-in complicate multi-vendor system integration across enterprises, educational institutions, and event venues. Vendor-specific platforms often limit flexibility, increasing dependence on single suppliers and driving up long-term maintenance costs. Furthermore, cybersecurity risks in networked and cloud-based AV systems are increasing as companies move to AV-over-IP and remote management platforms. Vulnerabilities in conferencing, streaming, and data-sharing channels expose organizations to potential breaches and compliance challenges.

SEGMENTATION INSIGHTS

INSIGHTS BY PRODUCT

The global pro AV market by product segment covers professional video and professional audio systems, which form the two main pillars of Pro AV technology adoption across end-users. Professional video segments make up the dominant segmental share, due to strong reliance on video solutions for communication, broadcasting, and events. The demand for LED walls, UHD displays, and IP-based workflows supports this leadership, while integration with AV-over-IP improves scalability and encourages long-term use in corporate and entertainment settings.

INSIGHTS BY PROFESSIONAL VIDEO

The professional video category is segmented into video displays, capture and production, video projection, and others, which include video conferencing systems, digital signage players, AV-over-IP encoders and decoders, matrix switchers, media servers, and multi-viewers. The video display market is expected to grow at a rate of 6.76% during the forecast period and holds the largest segmental share, fueled by the increasing use of LED walls and flat panels in boardrooms, control centers, and venues. Lower costs for LEDs are encouraging more installations in retail and transport hubs. Furthermore, the capture and production segment accounted for over40% of professional video revenue in 2024. Broadcast cameras, studio switchers, and editing systems lead as OTT platforms, esports, and businesses increase their content production.

INSIGHTS BY CAPTURE AND PRODUCTION

The capture and production segment is further divided into application-based subsegments, including broadcast & video production, enterprise–Fortune 500, government bodies, higher education, healthcare, sports, worship & non-profit, K–12 education, museums, themed entertainment, and others such as retail, hospitality, tourism, and small business events. Broadcast & video production is forecast to record the highest CAGR of 7.54% during the forecast period. Investments in 4K/8K cameras, IP-based workflows, and cloud editing tools sustain this demand. Sports broadcasting and OTT services drive constant upgrades, making this the most rapidly expanding capture and production application across global Pro AV.

Furthermore, the themed entertainment held the lowest share in 2024; this adoption is limited by high system costs and project-based spending in theme parks and attractions. Although niche, immersive AV projects in Asia-Pacific and the Middle East maintain relevance.

INSIGHTS BY PROFESSIONAL AUDIO

The professional audio segment includes microphones, pro speakers, sound mixers, signal processors, power amplifiers, and others, such as studio interfaces, podcast consoles, DI boxes, IEM systems, and monitor controllers. Microphones held the largest share at over 34% in 2024, supported by widespread deployment in conferencing, hybrid classrooms, and live venues. Network-ready and compact wireless microphones remain essential for corporate and broadcast environments.

Sound mixers are expected to have the highest growth rate of 5.91%. Digital and software-based mixers are becoming more popular in studios, education, and live events. These mixers focus on integration with networked audio and compact, remotely operated setups. These qualities make mixers the most flexible and growing part of professional audio systems.

INSIGHTS BY APPLICATION

The global pro AV market by application includes corporates, media & entertainment, venues & events, educational institutions, government & military, retail, transportation, hospitality, and others, such as healthcare, energy and utility sectors, houses of worship, museums, and other public or non-commercial venues. The corporates segment holds the most significant segmental share in 2024. Corporate AV helps communication, teamwork, and content sharing across offices with integrated systems like conference rooms, training centers, digital signs, and audio support. Moreover, common setups include UC platforms, networked conferencing bars, ceiling microphones, DSPs, control panels, and wireless sharing tools that create a consistent experience in different meeting spaces.

Furthermore, the venues & events segment holds a significant share of the global pro AV market in 2024 and is forecasted as the fastest-growing application. Recovery of concerts, exhibitions, and conventions fuels large-scale investment in immersive video walls, high-power projection, and audio reinforcement, strengthening the role of venues and events. Also, transportation applications are projected to expand at the second-fastest CAGR of 6.81%. Airports, metros, and intercity hubs are deploying digital signage, information systems, and AV-linked monitoring to improve passenger flow and engagement. Smart mobility initiatives sustain adoption, making transport one of the strongest emerging verticals within Pro AV infrastructure.

INSIGHTS BY DISTRIBUTION CHANNEL

The global pro AV market by distribution segmentation distinguishes between offline and online channels, reflecting the way integrators, enterprises, and end-users source professional AV equipment. Online channels, though smaller in 2024, are forecasted to grow at a CAGR of 7.17%. SMEs and independent consumers increasingly procure standardized AV systems through e-commerce, while integrators rely on digital platforms for components. Improved support and bundled delivery accelerate adoption, making online sourcing a key future growth vector.

PRO AV MARKET GEOGRAPHICAL ANALYSIS

APAC dominated the global pro AV market, accounting for a share of over 37% in 2024. Growing demand for immersive digital experiences in education, retail, and corporate sectors across India, China, and Southeast Asia drives the integration of interactive displays, video walls, and hybrid conferencing systems. Also, expanding infrastructure in transportation, hospitality, and government facilities increases the use of large-scale public address systems, control room AV, and digital signage solutions. Furthermore, the rapid growth of smart cities and 5G networks helps with the deployment of networked AV systems, remote monitoring tools, and cloud-connected AV control platforms in urban and industrial areas.

North America holds a significant share of the global pro AV market. Rapid growth of hybrid workspaces and smart learning environments in the U.S. and Canada increases the need for unified communication systems, interactive flat panels, and high-quality conferencing AV solutions. Also, growing investments in AI-driven automation and cloud-managed AV platforms speed up the integration of intelligent AV systems in corporate, education, and public sector settings.

In 2024, Europe recorded the second-highest growth in the global pro AV market with a CAGR of 6.35%. Germany contributed 22.76% of regional revenue, supported by its strong trade-show ecosystem, corporate base, and integrator networks. Europe’s pro AV market growth is further reinforced by corporate and education upgrade cycles, demand from exhibitions such as Messe Frankfurt and IFA Berlin, and broadcaster investments in studio and OB-truck modernization, ensuring consistent adoption across its major submarkets.

In the Middle East and Africa, expansion is driven by luxury hospitality, stadium upgrades, and smart city projects in Saudi Arabia, the UAE, and Turkey. Within the region, South Africa's pro AV market leads with a 6.53% CAGR, supported by convention centres, broadcasting, and event rentals. Also, regional adoption in MEA is strengthened by infrastructure upgrades and telecom improvements that enable cloud conferencing and managed AV services. Combined with Saudi, UAE, and Turkish projects, South Africa’s diverse demand profile reinforces strong market momentum.

In 2024, Latin America accounted for a lower market share of the global pro AV market, with growth centred in Brazil and Mexico. Convention centres, live events, and sports venue upgrades fuel activity, though overall share remains limited by import costs.

VENDOR LANDSCAPE

The global pro AV market is highly fragmented, with strong competition from leaders like LG Electronics, Crestron Electronics, Samsung, and Sony. These companies dominate with varied product lines, well-known brands, and wide distribution networks. Furthermore, technological innovation and specific industry needs drive competition. Video walls for control centers, AV-over-IP for corporate boardrooms, and immersive sound systems for entertainment venues push vendors to keep up with changing standards like HDMI 2.1 and IPMX.

Established manufacturers in the pro AV market like Barco, Harman (part of Samsung), and Panasonic integrate IoT, cloud-based control systems, and AI-based automation that enable them to propose distinct solutions to high-end commercial applications.

Regional companies in emerging markets like India and Southeast Asia provide affordable AV integration services, quick installations, and local customization. However, they often struggle against international brands that have better financial and technical resources. Furthermore, the rise of live events, hybrid workplaces, and smart classrooms is speeding up global adoption, especially in APAC and Latin America, and boosting the pro AV market growth. There, increased investment in infrastructure and urbanization is creating new demand for enhanced AV setups.

Recent Developments in the Global Pro AV Market

- In June 2025, QSC launched the Core 24f processor Server Core X10 X20r and VSA-100 VisionSuite AI Accelerator, enhancing processing power and AI automation for Pro AV systems. These products improve signal management analytics integration and overall efficiency in enterprise and large venue environments.

- In April 2025, Blackmagic Design introduced the DeckLink IP 100G capture card supporting eight Ultra HD channels over 100G Ethernet. At NAB 2025, they also unveiled the PYXIS 12K camera, Videohub Mini routers, streaming encoders, decoders, and 2110 IP converters, providing advanced routing and efficient IP-based workflows.

- In June 2025, Sony enhanced its Spatial Reality Display with Twinmotion support, offering immersive real-time 3D visualization for designers, architects, and content creators. In January 2025, the company also partnered with Exertis AV to expand distribution of professional displays and signage in the UK and Ireland, accelerating adoption in commercial markets.

SNAPSHOT

The global pro AV market size is expected to grow at a CAGR of approximately 5.95% from 2024 to 2030.

The following factors are likely to contribute to the growth of the global pro AV market during the forecast period:

- Rise of the Event-Driven AV Demand

- Institutional & Enterprise AV Integration

- Shift to Cloud-Native & Remote AV Management

- Adoption of AV-as-a-Service (AVaaS) & Subscription Models

Base Year: 2024

Forecast Year: 2025-2030

The report considers the present scenario of the global pro AV market and its market dynamics for 2025−2030. It covers a detailed overview of several market growth enablers, restraints, and trends. The study covers both the demand and supply sides of the market. It also profiles and analyzes leading companies and several other prominent companies operating in the market.

Key Company Profiles

- Sony Group Corporation

- Business Overview

- Product Offerings

- Key Developments

- Key Strategies

- Key Strengths

- Key Opportunities

- Samsung

- LG Electronics

- Panasonic Corporation

- Crestron Electronics, Inc.

- Legrand AV Inc.

- Shure Incorporated

- Yamaha Corporation

- QSC, LLC

- Extron

- Christie Digital Systems, Inc.

- Biamp

- Sennheiser Electronic SE & Co. KG

- Blackmagic Design Pty. Ltd.

- NEC Corporation

Other Prominent Company Profiles

- Bose Corporation

- Business Overview

- Product Offerings

- Poly Inc. (Part of HP Development Company)

- Logitech

- Hitachi, Ltd.

- Koninklijke Philips N.V.

- BenQ Corporation

- Sharp Corporation

- TCL Technology Group

- Toshiba Corporation

- Audio-Technica

- d&b audiotechnik GmbH & Co. KG.

- L-Acoustics

- Hisense Group

- InFocus Corporation

- Optoma Corporation

- TOA Corporation

- Boxlight Corporation

- Peerless‑AV

- AtlasIED

- ClearOne

- Kramer Electronics

- RTI (Remote Technologies Inc.)

- Altinex

- Hall Technologies

- RGB Spectrum

- Aurora Multimedia

- Lightware Visual Engineering

- Audinate

- Matrox

- Bang & Olufsen

- Leyard

- Semtech Corporation

- ViewSonic Corporation

- AVI‑SPL

- TD SYNNEX

- Barco Electronic Systems Pvt Ltd

Segmentation by Product

- Professional Video

- Professional Audio

Segmentation by Professional Video

- Video Displays

- Capture and Production

- Video Projection

- Others

Segmentation by Capture And Production

- Broadcast & Video Production

- Enterprise – Fortune 500

- Government Bodies

- Higher Education

- Healthcare

- Sports

- Worship & Non-Profit

- K–12 Education

- Museums

- Themed Entertainment

- Others

Segmentation by Professional Audio

- Microphones

- Pro Speakers

- Sound Mixers

- Signal Processors

- Power Amplifiers

- Others

Segmentation by Application

- Corporates

- Media & Entertainment

- Venues & Events

- Educational Institutions

- Government & Military

- Retail

- Transportation

- Hospitality

- Others

Segmentation by Distribution Channel

- Offline

- Online

Segmentation by Geography

- APAC

- China

- India

- Japan

- South Korea

- Australia

- Indonesia

- Vietnam

- Malaysia

- North America

- U.S.

- Canada

- Europe

- Germany

- Russia

- UK

- France

- Italy

- Spain

- Poland

- Latin America

- Brazil

- Mexico

- Argentina

- Middle East & Africa

- Saudi Arabia

- UAE

- South Africa

- Turkey

PRO AV MARKET FAQs

What is the growth rate of the global pro AV market?

What are the significant trends in the pro AV industry?

Which region dominates the global pro AV market share?

How big is the global pro AV market?

Who are the key players in the global pro AV market?

For more details, please reach us at [email protected]

- Chapter 1- Scope & Coverage

- Market Definition

- Inclusion

- Exclusions

- Market Estimation Caveats

- Market Derivation

- Market Segmentation by Product

- Market Segmentation by Professional Video

- Market Segmentation by Capture and Production

- Market Segmentation by Professional Audio

- Market Segmentation by Application

- Market Segmentation by Distribution Channel

- Chapter 2- Premium Insights

- Chapter 3- Market Dynamics

- Introduction

- Applications of Professional Video Devices

- Applications of Professional Audio Devices

- End-User Segments Leveraging Pro AV

- Impact of The Ongoing Tariff War

- Market Opportunities & Trends

- Smart & connected learning environments

- Next-gen digital signage & experience av

- AI & automation-enhanced AV systems

- Cloud-driven pro AV systems & remote management

- Market Growth Enablers

- Rise of Event-Driven AV Demand

- Institutional & Enterprise AV Integration

- Shift to Cloud-Native & Remote AV Management

- Adoption of AV-as-a-Service (AVaaS) & Subscription Models

- Market Restraints

- High capital and operational costs

- Shortage of skilled AV professionals and integrators

- Interoperability issues and vendor lock-in

- Cybersecurity risks in networked and cloud AV systems

- Market Landscape

- Five Forces Analysis

- Chapter 4- Market Segmentation

- Product (Market Size & Forecast: 2021-2030)

- Professional Video

- Professional Audio

- Professional Video (Market Size & Forecast: 2021-2030)

- Video Displays

- Capture And Production

- Video Projection

- Others

- Capture And Production (Market Size & Forecast: 2021-2030)

- Broadcast & Video Production

- Enterprise – Fortune 500

- Government Bodies

- Higher Education

- Healthcare

- Sports

- Worship & Non-Profit

- K–12 Education

- Museums

- Themed Entertainment

- Others

- Professional Audio (Market Size & Forecast: 2021-2030)

- Microphones

- Pro Speakers

- Sound Mixers

- Signal Processors

- Power Amplifiers

- Others

- Application (Market Size & Forecast: 2021-2030)

- Corporates

- Media & Entertainment

- Venues & Events

- Educational Institutions

- Government & Military

- Retail

- Transportation

- Hospitality

- Others

- Distribution Channel (Market Size & Forecast: 2021-2030)

- Offline

- Online

- Chapter 5- Geography Segmentation

- Geography Segmentation (Market Size & Forecast: 2021-2030)

- Geographic Overview – Market Maturity Index

- APAC

- China

- India

- Japan

- South Korea

- Australia

- Indonesia

- Vietnam

- Malaysia

- Europe

- Germany

- Russia

- UK

- France

- Italy

- Spain

- Poland

- North America

- US

- Canada

- Middle East & Africa

- Saudi Arabia

- UAE

- South Africa

- Turkey

- Latin America

- Brazil

- Mexico

- Argentina

- Chapter 6- Competitive Landscape

- Competitive Landscape

- Competition Overview

- Key Developments

- Key Company Profiles

- Report Summary

- Key Takeaways

- Strategic Recommendations

Select a license type that suits your business needs

Single User Licence

- Report accessible by one user only

- Free 10% or 3 days of customization

- Free post-sale service assistance

- Continuous support through email

5 User Licence

- Report accessible by 5 users within the organization

- Free 15% or 4.5 days of customization

- Continuous support through email and telephone

- Free analyst hour

- Free Upgrade: If an updated report published within 180 days of purchase, you will get the revised report free of charge

Corporate Licence

- Free Datasheet worth $1500

- Report accessible by the entire organization

- Free 20% or 6 days of customization

- Free post-sale service assistance

- Continuous support through email and telephone

- Direct access to lead analysts

- Free analyst hour

- Free Upgrade: If an updated report published within 180 days of purchase, you will get the revised report free of charge

Datasheet Licence

- Report accessible by 1 user only

- Free 15% or 32 hours of customization

- Free post-sale service assistance

- Direct access to lead analysts

Frequently Asked Questions

What is the growth rate of the global pro AV market?

What are the significant trends in the pro AV industry?

Which region dominates the global pro AV market share?

How big is the global pro AV market?

Who are the key players in the global pro AV market?