Steam Turbine Aftermarket Market Research Report 2026-2031

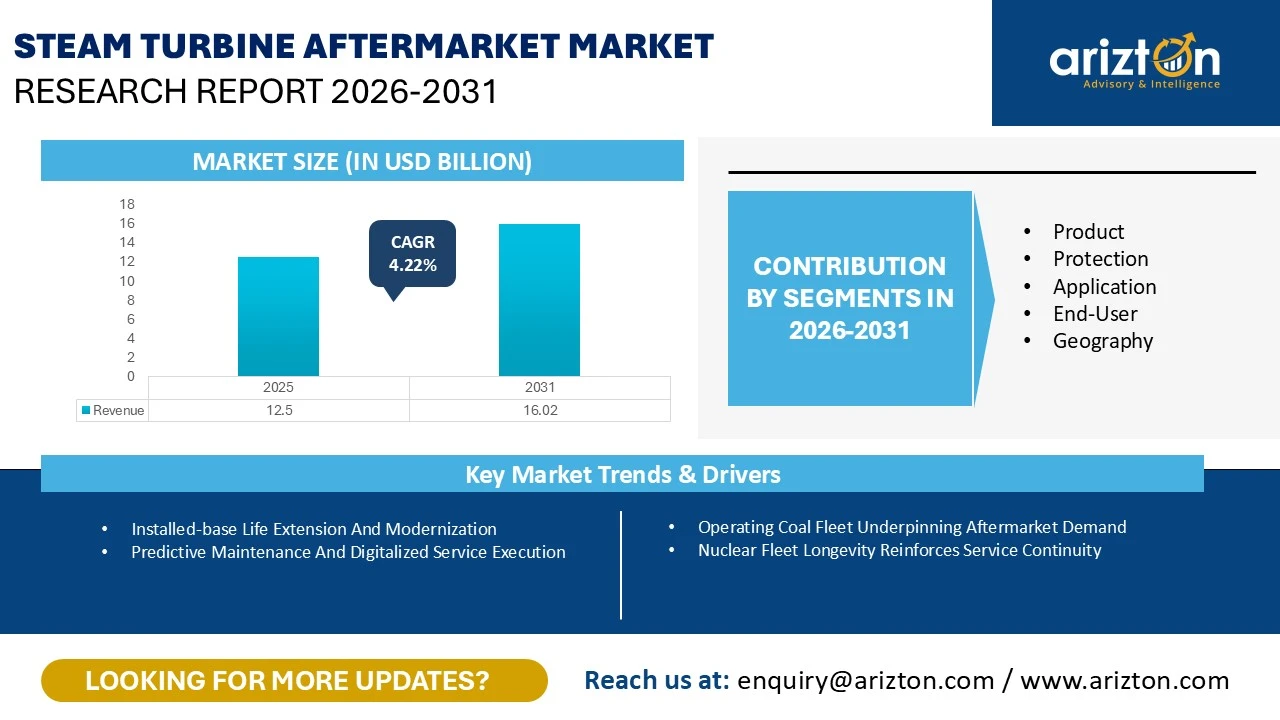

THE GLOBAL STEAM TURBINE AFTERMARKETS MARKET WAS VALUED AT USD 12.50 BILLION IN 2025 AND IS EXPECTED TO REACH USD 16.02 BILLION BY 2031, GROWING AT A CAGR OF 4.22% FROM 2025–2031.

Steam Turbine Aftermarket Growth Insights – Driven by Rising Demand for Inspection, Repair, Maintenance, Spare Parts, Upgrades, and Lifecycle Services Across Coal, Nuclear, Gas, Biomass, and Industrial Power Generation Facilities (2026–2031)

Published Date : July 2026

Last Updated : July 2026

format: PDF

197 pages

49 company

5 segments

5 region

24 countries

Purchase Options

Steam Turbine Aftermarket Market Research Report 2026-2031

THE GLOBAL STEAM TURBINE AFTERMARKETS MARKET WAS VALUED AT USD 12.50 BILLION IN 2025 AND IS EXPECTED TO REACH USD 16.02 BILLION BY 2031, GROWING AT A CAGR OF 4.22% FROM 2025–2031.

The Steam Turbine Aftermarkets Market Size, Share & Trends Analysis Report By

- Offering Type: Spare Parts & Consumables, Maintenance & Repair Services, Upgrades & Retrofits, Digital Solutions, and Others

- Fuel Type: Coal, Gas, Nuclear, and Others

- End-Use Industry: Power Generation, Oil & Gas, Industrial Manufacturing, District Heating & Cooling, Mining & Metal Processing, Marine, and Others

- Capacity: Large Turbines (>300 MW), Medium Turbines (151–300 MW), and Small Turbines (≤150 MW)

- Geography: North America, Europe, APAC, Latin America, and Middle East & Africa

Industry Analysis Report, Regional Outlook, Growth Potential, Price Trends, Competitive Market Share & Forecast 2026–2031.

This report includes market data points, ranging from trend

analyses to market estimates & forecasts that you can customize

STEAM TURBINE MARKET REPORT SCOPE

| REPORT ATTRIBUTE | DETAILS |

|---|---|

| MARKET SIZE (2031) | USD 16.02 Billion |

| MARKET SIZE (2025) | USD 12.50 Billion |

| CAGR (2025-2031) | 4.22% |

| HISTORIC YEAR | 2022- 2024 |

| BASE YEAR | 2025 |

| FORECAST YEAR | 2026-2031 |

| SEGMENTS BY | Offering Type, Capacity, Fuel Type, End-Use Industry, and Geography |

| GEOGRAPHIC ANALYSIS | North America, Europe, APAC, Latin America, & Middle East & Africa |

| KEY PLAYERS | General Electric (GE), Siemens A.G., Mitsubishi Heavy Industries (MHI), Shanghai Electric, Doosan Skoda Power, Toshiba America Energy Systems Corporation (TAES), Hyundai Heavy Industries Turbomachinery Co., Ltd. (HHI-TMC), Bharat Heavy Electricals Ltd. (BHEL), Everllence, and Ansaldo Energia |

STEAM TURBINE AFTERMARKETS MARKET SIZE & SHARE

The global Steam Turbine Aftermarket Market was valued at USD 12.50 billion in 2025 and is expected to reach USD 16.02 billion by 2031, growing at a CAGR of 4.22% during the forecast period. Demand remains anchored in conventional generation assets already in service, where steam turbine-driven coal, nuclear, gas, biomass, and industrial facilities continue to require inspection, repair, spares, upgrades, and lifecycle services. Within this ecosystem, the broader Steam Turbine Services Market thrives on optimizing existing infrastructure rather than building new capacity from scratch.

Nuclear power remains a major anchor for the Steam Turbine Aftermarket. Operating nuclear power plants rely on massive turbine-generator systems that require recurring inspection, overhaul, parts replacement, and life-extension support. According to the International Atomic Energy Agency (IAEA), 417 nuclear power reactors were in operation globally at the end of 2024, representing a combined net electrical capacity of 377 GW(e). This extensive operating base supports steady demand for OEM services, independent repairs, spare parts, outage support, and modernization work.

Modern aftermarket demand is increasingly organized around planned outage cycles rather than reactive, failure-led interventions. These windows allow operators to comprehensively address the Steam Turbine Maintenance Market, inspecting critical components like rotors, blades, seals, valves, bearings, controls, and generator-side systems within tightly defined maintenance schedules. IAEA outage data for 2024 underscores this trend, showing that inspection, maintenance, or repair combined with refueling accounted for 70.57% of planned full-outage energy loss.

Recent Developments in the Steam Turbine Aftermarket Market

- May 2025: EthosEnergy acquired Turbine Services, Ltd., a prominent aftermarket parts supplier. This acquisition strengthens EthosEnergy’s replacement-parts access and non-OEM support capability, crucial advantages as operators prioritize lifecycle support and faster turnarounds for installed fleets.

- April 2025: Siemens Energy highlighted its key role in recommissioning the Palisades Nuclear Power Plant in Michigan. The scope covers steam turbine and generator replacement, refurbishment, and field service support, illustrating how restart and life-extension programs drive deeper technical work across the Steam Turbine Repair Market.

- February 2025: Sulzer expanded its Vadodara Service Centre in India to bolster regional turbomachinery support. The facility enhances Sulzer's capabilities in steam turbine repair, refurbishment, retrofits, reverse engineering, and parts support for aging regional steam assets.

STEAM TURBINE AFTERMARKETS MARKET TRENDS & DRIVERS

- Fleet Life Extension over Replacement: Demand is heavily anchored in extending the lifespans of installed fleets, particularly aging coal and nuclear assets where full replacement is cost-prohibitive. Global Energy Monitor’s Boom and Bust Coal 2025 report notes that OECD countries operate over 200 GW of coal capacity exceeding 40 years of age. This keeps activity high in the Steam Turbine Overhaul Market, as operators prioritize refurbishing rotors, blades, seals, casings, and control systems over purchasing entirely new units.

- Shift to Condition-Based Maintenance: The industry is pivoting away from rigid, periodic schedules toward condition-based maintenance powered by continuous monitoring, diagnostics, and asset analytics. Operators leverage these digital tools to identify early equipment risks, refine outage planning, prioritize service scopes, and mitigate unplanned downtime, reinforcing a broader shift toward availability-led service models.

- Surge in Global Electricity Demand: The IEA’s Electricity 2025 report projects global electricity demand to grow at close to 4% annually through 2027. This rapid growth pressures plant owners to maintain highly reliable thermal and nuclear assets, ensuring sustained spending on turbine maintenance, outage execution, and targeted modernization.

- Capital-Discipline and Efficiency Optimization: Investment is increasingly flowing into clean energy, grids, storage, and electrification rather than new fossil fuel capacity. The IEA’s World Energy Investment 2025 report forecasts global energy investment to reach $3.3 trillion in 2025, with $2.2 trillion allocated to clean technologies and $1.1 trillion to fossil fuels. This capital split forces thermal plant owners to be highly selective, favoring targeted turbine refurbishment and efficiency tweaks that extend useful life at a lower cost than full replacement.

INDUSTRY RESTRAINTS

Outage Economics: Shutdown windows are expensive, strictly limited, and tightly managed. The Electric Power Research Institute (EPRI) indicates that up to 70% of planned steam power plant outages involve turbine-generator work. This intense financial pressure often forces owners to defer non-critical repairs, narrow approved work scopes, and prioritize only the highest-value maintenance actions.

Labor Shortages and Component Lead Times: Service execution relies on highly specialized labor and timely parts access, both of which face structural bottlenecks. The IEA’s World Energy Employment 2025 report notes that in nuclear roles, 1.7 workers are approaching retirement for every young worker entering the workforce. Compounded by long lead times for large turbine components, this talent gap raises outage execution risks and limits scheduling flexibility for complex repair programs.

MARKET SEGMENTATION INSIGHTS

Insight by Offering Type

The global steam turbine aftermarket market, by offering type, is segmented into spare parts & consumables, maintenance & repair services, upgrades & retrofits, digital solutions, and others. Among these, the spare parts & consumables segment holds the largest market share. This segment forms the foundation of the aftermarket, as steam turbines require periodic replacement of critical components due to continuous wear, aging, and operational stress. Components such as turbine blades, seals, bearings, valves, and gaskets must be regularly replaced to ensure optimal performance and minimize the risk of unplanned failures.

Demand for spare parts and consumables remains highly resilient because maintenance activities are driven by scheduled outage cycles and asset reliability requirements rather than new equipment installations. Power utilities and industrial operators consistently allocate budgets for inventory management, planned maintenance, and lifecycle support, making this segment closely tied to the extensive installed base of steam turbines worldwide.

Insight by Fuel Type

Based on fuel type, the nuclear segment is projected to register the fastest growth during the forecast period. Nuclear power plants rely on large steam turbine-generator systems that operate under stringent safety, reliability, and regulatory requirements. These facilities typically have long operating lifespans and follow planned refueling and maintenance schedules, creating sustained demand for turbine inspections, rotor and blade refurbishment, component replacements, modernization projects, and comprehensive lifecycle support services.

As countries continue investing in extending the operational life of existing nuclear power plants and developing new nuclear generation capacity, demand for specialized steam turbine aftermarket services is expected to accelerate throughout the forecast period.

Insight by End-Use Industry

Based on end use, the power generation segment dominates the global steam turbine aftermarket market. Growing global electricity demand, combined with the continued operation of coal-, gas-, and nuclear-based power plants, has strengthened the need for reliable steam turbine maintenance and modernization. Since steam turbines remain essential for baseload electricity generation, plant operators prioritize regular maintenance, performance optimization, and life-extension programs to maximize availability and improve operational efficiency.

The recurring nature of planned outages and asset management strategies ensures consistent demand for repair services, spare parts, and turbine upgrades across utility-scale power generation facilities, reinforcing the segment's leading market position.

Insight by Capacity

Based on capacity, the large steam turbines segment accounts for the largest share of the global steam turbine aftermarket market and is expected to witness the strongest growth over the forecast period. Large-capacity turbines are primarily deployed in utility-scale coal-fired, nuclear, and thermal power plants, where uninterrupted operation is critical to maintaining grid stability and power output. Because outages involving these units can significantly impact electricity generation, operators place a strong emphasis on preventive maintenance, major overhauls, and performance enhancement initiatives.

The aftermarket for large steam turbines is supported by long asset lifecycles and the high capital cost associated with equipment replacement. Rather than investing in new turbine installations, utilities increasingly focus on modernization, control system upgrades, rotor refurbishment, and life-extension programs to improve efficiency and extend asset reliability. This approach continues to drive sustained investment in planned outage services and comprehensive lifecycle maintenance solutions.

REGIONAL ANALYSIS

Asia Pacific (APAC)

Asia Pacific is the dominant and fastest-growing regional market, projected to grow at a CAGR of 4.86% from 2025 to 2031. The region features a powerful combination of massive coal-fired fleets, heavy industrial steam demand, and expanding nuclear infrastructure.

- China serves as the primary driver in APAC due to its massive coal-generation fleet and rapid nuclear expansion. According to World Nuclear Association data, China accounts for nearly half of the global nuclear reactors under construction, ensuring deep, long-term opportunities for turbine-generator inspections, retrofits, and lifecycle support.

North America

North America stands as a premier high-value market driven by aging nuclear assets, mature coal fleets, and combined-cycle gas plants. Operators here heavily prioritize long-term service agreements (LTSAs), obsolescence management, and performance recovery.

- Canada offers a highly focused, nuclear-led aftermarket pipeline. Canadian operators look to extend the operating lives of their baseload nuclear assets through targeted rotor, blade-path, and control upgrades without undertaking full asset replacement.

STEAM TURBINE AFTERMARKETS MARKET VENDOR LANDSCAPE

The competitive environment features a strategic mix of original equipment manufacturers (OEMs), independent service providers, regional repair workshops, and component specialists. Competition spans multiple asset types, including utility, nuclear, combined heat and power (CHP), and industrial steam facilities. The sheer scale of the installed base keeps the market decentralized; for context, the COGEN World Coalition reported that global CHP plants produced 4,492 TWh of electricity and 13,821 TWh of heat in 2023.

Market leadership hinges on a provider's ability to minimize outage risks and reliably restore turbine performance:

- GE Vernova anchors its strategy around parts, complex repairs, outage planning, and life extension, primarily serving North American nuclear fleets and global coal plants.

- Siemens Energy emphasizes deep modernization capabilities, having updated over 350 steam turbines globally.

- Doosan Škoda Power delivers a balance of OEM and non-OEM services, workshop repairs, and on-site machining.

Competition is rapidly evolving beyond mechanical fixes into digital differentiation. Mitsubishi Power’s TOMONI Hub provides connected monitoring and early warning systems, while Woodward delivers robust steam turbine controls in simplex, dual, and triple-modular-redundant configurations. Underscoring the importance of component readiness, GE Vernova actively supports over 17,000 control part numbers, proving that digital support and parts availability are the new frontiers of the aftermarket landscape.

SNAPSHOT

The global steam turbine aftermarkets market size is expected to grow at a CAGR of approximately 4.22% from 2025 to 2031.

The following factors are likely to contribute to the growth of the global steam turbine aftermarkets market during the forecast period:

- Operating coal fleet underpinning aftermarket demand

- Nuclear fleet longevity reinforces service continuity

- Electricity demand growth sustains asset relevance

- Service ecosystem maturity supporting recurring demand

Base Year: 2025

Forecast Year: 2026-2031

The report examines the current state of the global steam turbine aftermarkets market and its market dynamics through 2026−2031. It covers a detailed overview of several market growth enablers, restraints, and trends. The study covers both the demand and supply sides of the market. It also profiles and analyses leading companies and several other prominent companies operating in the market.

Key Company Profile

- General Electric (GE)

- Business Overview

- Product Offerings

- Key Developments

- Key Strategies

- Key Opportunities

- Key Strengths

- Siemens A.G.

- Mitsubishi Heavy Industries (MHI)

- Shanghai Electric

- Doosan Skoda Power

- Toshiba America Energy Systems Corporation (TAES)

- Hyundai Heavy Industries Turbomachinery Co., Ltd. (HHI-TMC)

- Bharat Heavy Electricals Ltd. (BHEL)

- Everllence

- Ansaldo Energia

Other Company Profiles

- Dongfang Electric Corporation

- Business Overview

- Product Offerings

- JSC Atomenergomash (AEM)

- Kawasaki Heavy Industries

- WEG

- Triveni Turbine

- Nanjing Turbine & Electric Machinery

- Hangzhou Turbine

- Fuji Electric Co., Ltd.

- Power Machines

- MAPNA Group

- Shandong Qingneng Steam Turbine

- Ural Turbine Works

- Turbimaq

- Ukrainian Energy Machines

- Baker Hughes

- Ebara Elliott Energy

- Chola Turbo Machinery

- M+M Turbinen-Technik

- TurboTech Precision Engineering

- EthosEnergy

- Arani Power Systems

- Turtle Turbines

- NG Metalurgica S.A.

- Fincantieri

- Harbin Turbine Company Limited

- NCON Turbo Tech

- Trillium Flow Technologies

- Chart Industries

- De Pretto Industrie S.R.L.

- Mechanical Dynamics & Analysis (MD&A)

- Sulzer Ltd

- Bilfinger

- Allied Power Group

- Goltens

- Power Services Group

- Reliable Turbine Services

- Shin Nippon Machinery Co. Ltd.

Segmentation by Offering Type

- Spare Parts & Consumables

- Maintenance & Repair Services

- Upgrades & Retrofits

- Digital Solutions

- Others

Segmentation by Capacity

- Large Turbines (>300 MW)

- Medium Turbines (151–300 MW)

- Small Turbines (≤150 MW)

Segmentation by Fuel Type

- Coal

- Gas

- Nuclear

- Others

Segmentation by End-Use Industry

- Power Generation

- Oil & Gas

- Industrial Manufacturing

- District Heating & Cooling

- Mining & Metal Processing

- Marine

- Others

Segmentation by Geography

- North America

- US

- Canada

- APAC

- China

- India

- Japan

- South Korea

- Indonesia

- Australia

- Taiwan

- Europe

- Germany

- France

- Russia

- UK

- Italy

- Poland

- Spain

- Netherlands

- Latin America

- Brazil

- Mexico

- Argentina

- Middle East & Africa

- Saudi Arabia

- UAE

- Egypt

- South Africa

STEAM TURBINE MARKET FAQs

What is the growth rate of the global steam turbine aftermarkets market?

How big is the global steam turbine aftermarket market?

Which region dominates the global steam turbine aftermarket market?

What are the key trends in the global steam turbine aftermarkets market?

Who are the major players in the global steam turbine aftermarkets market?

For more details, please reach us at [email protected]

- Chapter 1- Scope & Coverage

- Market Definition

- Inclusion

- Exclusions

- Market Estimation Caveats

- Market Derivation

- Market Segmentation by Offering Type

- Market Segmentation by Capacity

- Market Segmentation by Fuel Type

- Market Segmentation by End Use Industry

- Chapter 2- Premium Insights

- Chapter 3- Market Dynamics

- Introduction

- Steam turbine lifecycle and aftermarket intensity model

- Steam turbine upgrade and modernization opportunity matrix

- Steam turbine aftermarket spend structure

- Service provider type landscape in the steam turbine aftermarkets

- Market Opportunities & Trends

- Installed-base life extension and modernization

- Predictive maintenance and digitalized service execution

- Flexibility upgrades for cycling and variable load operation

- Decarbonization-led efficiency retrofits and selective electrification

- Market Growth Enablers

- Operating coal fleet underpinning aftermarket demand

- Nuclear fleet longevity reinforces service continuity

- Electricity demand growth sustaining asset relevance

- Service ecosystem maturity supporting recurring demand

- Market Restraints

- Coal transition pressures reducing service visibility

- Investment prioritization limiting upgrade spend

- Outage economics restricting service scope

- Execution constraints delaying aftermarket delivery

- Market Landscape

- Five Forces Analysis

- Chapter 4- Market Segmentation

- Offering Type (Market Size & Forecast: 2022-2031)

- Spare Parts & Consumables

- Maintenance & Repair Services

- Upgrades & Retrofits

- Digital Solutions

- Others

- Capacity (Market Size & Forecast: 2022-2031)

- Large Turbines (>300 MW)

- Medium Turbines (151–300 MW)

- Small Turbines (≤150 MW)

- Fuel Type (Market Size & Forecast: 2022-2031)

- Coal

- Gas

- Nuclear

- Others

- End-Use Industry (Market Size & Forecast: 2022-2031)

- Power Generation

- Oil & Gas

- Industrial Manufacturing

- District Heating & Cooling

- Mining & Metal Processing

- Marine

- Others

- Chapter 5- Geography Segmentation

- Geography Segmentation (Market Size & Forecast: 2022-2031)

- Geographic Overview – Market Maturity Index

- APAC

- China

- India

- Japan

- South Korea

- Indonesia

- Australia

- Taiwan

- North America

- US

- Canada

- Europe

- Germany

- France

- Russia

- UK

- Italy

- Poland

- Spain

- Netherlands

- Latin America

- Brazil

- Mexico

- Argentina

- MEA

- Saudi Arabia

- UAE

- Egypt

- South Africa

- Chapter 6- Competitive Landscape

- Competitive Landscape

- Competition Overview

- Key Developments

- Key Company Profiles

- Other Prominent Company Profiles

- Report Summary

- Key Takeaways

- Strategic Recommendations

Select a license type that suits your business needs

Single User Licence

- Report accessible by one user only

- Free 10% or 3 days of customization

- Free post-sale service assistance

- Continuous support through email

5 User Licence

- Report accessible by 5 users within the organization

- Free 15% or 4.5 days of customization

- Continuous support through email and telephone

- Free analyst hour

- Free Upgrade: If an updated report published within 180 days of purchase, you will get the revised report free of charge

Corporate Licence

- Free Datasheet worth $1500

- Report accessible by the entire organization

- Free 20% or 6 days of customization

- Free post-sale service assistance

- Continuous support through email and telephone

- Direct access to lead analysts

- Free analyst hour

- Free Upgrade: If an updated report published within 180 days of purchase, you will get the revised report free of charge

Datasheet Licence

- Report accessible by 1 user only

- Free 15% or 32 hours of customization

- Free post-sale service assistance

- Direct access to lead analysts

Frequently Asked Questions

What is the growth rate of the global steam turbine aftermarkets market?

How big is the global steam turbine aftermarket market?

Which region dominates the global steam turbine aftermarket market?

What are the key trends in the global steam turbine aftermarkets market?

Who are the major players in the global steam turbine aftermarkets market?

Other RELATED Reports

Global Industrial Nailers and Staplers Market - Focused Insights 2024-2029

Published : September 2024