U.S. Data Center Construction Market – Industry Outlook & Forecast 2026-2031

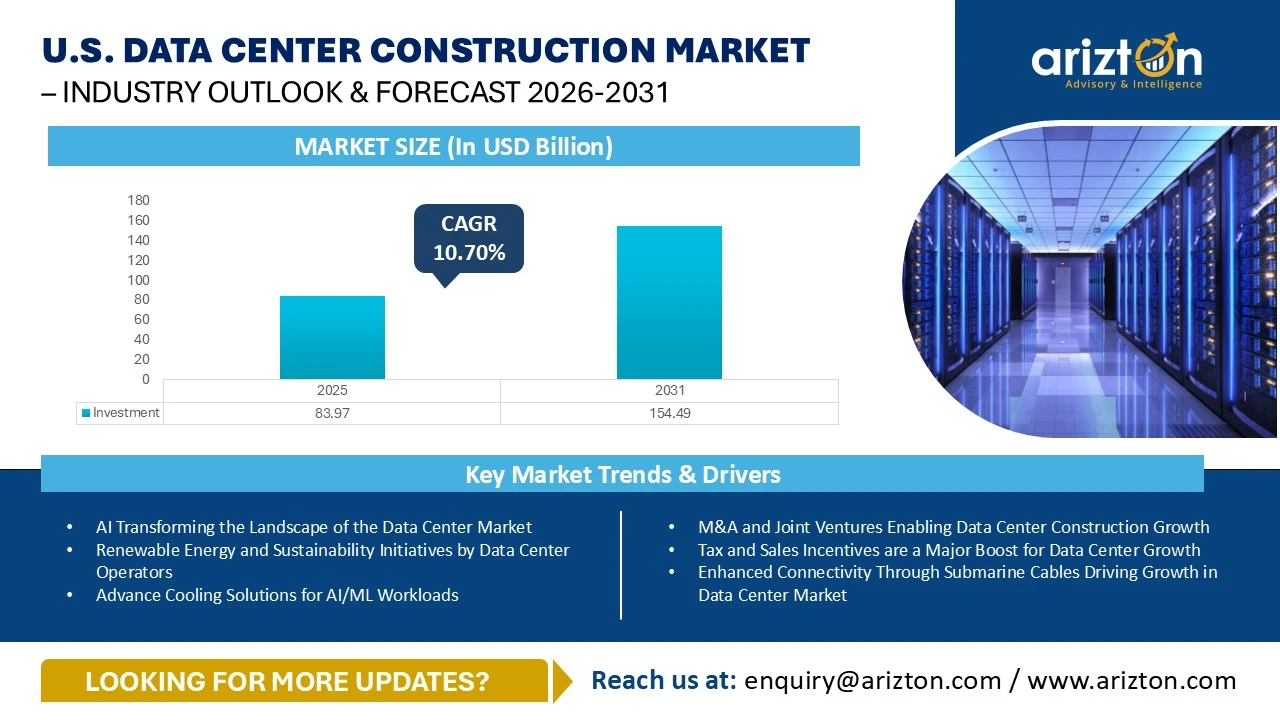

THE U.S. DATA CENTER CONSTRUCTION MARKET SIZE WAS VALUED AT USD 83.97 BILLION IN 2025 AND IS EXPECTED TO REACH USD 154.49 BILLION BY 2031, GROWING AT A CAGR OF 10.70%.

U.S. Data Center Construction Market Size, Share, Industry Analysis by Colocation Data Centers, Hyperscale Data Centers, and Enterprise Data Centers, Electrical Infrastructure, Mechanical Infrastructure, Cooling Systems, Tier Standards

Published Date : March 2026

Last Updated : March 2026

format: PDF

edition : Seventh Edition

260 pages

5 region

1 countries

179 company

9 segments

Purchase Options

U.S. Data Center Construction Market – Industry Outlook & Forecast 2026-2031

THE U.S. DATA CENTER CONSTRUCTION MARKET SIZE WAS VALUED AT USD 83.97 BILLION IN 2025 AND IS EXPECTED TO REACH USD 154.49 BILLION BY 2031, GROWING AT A CAGR OF 10.70%.

The U.S. Data Center Construction Market Research Report Includes Size, Share, and Growth in Terms of

- Facility Type: Hyperscale Data Centers, Colocation Data Centers, and Enterprise Data Centers

- Infrastructure: Electrical Infrastructure, Mechanical Infrastructure, and General Construction

- Electrical Infrastructure: UPS Systems, Generators, Transfer Switches & Switchgears, PDUs, and Other Electrical Infrastructure

- Mechanical Infrastructure: Cooling Systems, Racks, and Other Mechanical Infrastructure

- Cooling System: CRAC & CRAH Units, Chillers Units, Cooling Towers, Condensers, and Dry Coolers, and Other Cooling Units

- Cooling Techniques: Air-based Cooling and Liquid-based Cooling

- General Construction: Core & Shell Development, Installation & Commissioning Services, Engineering & Building Design, Fire Detection & Suppression, Physical Security, and DCIM/BMS Solutions

- Tier Standards: Tier I & Tier II, Tier III, and Tier IV

- Regions: Southeastern U.S., Midwestern U.S., Southwestern U.S., Western U.S., and Northeastern U.S.

Industry Analysis Report, Regional Outlook, Growth Potential, Price Trends, Competitive Market Share & Forecast 2026–2031.

This report includes market data points, ranging from trend

analyses to market estimates & forecasts that you can customize

U.S. DATA CENTER CONSTRUCTION MARKET REPORT SCOPE

| REPORT ATTRIBUTE | DETAILS |

|---|---|

| MARKET SIZE BY INVESTMENT (2031) | USD 154.49 Billion |

| MARKET SIZE BY INVESTMENT (2025) | USD 83.97 Billion |

| CAGR BY INVESTMENT (2025-2031) | 10.70% |

| MARKET SIZE - AREA (2031) | 52.57 Million Sq. Ft. |

| POWER CAPACITY (2031) | 13,565 MW |

| HISTORIC YEAR | 2022-2024 |

| BASE YEAR | 2025 |

| FORECAST YEAR | 2026-2031 |

| MARKET SEGMENTS | Facility Type, Infrastructure, Electrical Infrastructure, Mechanical Infrastructure, Cooling Systems, Cooling Technique, General Construction, Tier Standards, and Geography |

| GEOGRAPHICAL ANALYSIS | Southeastern U.S., Midwestern U.S., Southwestern U.S., Western U.S., and Northeastern U.S. |

UNITED STATES DATA CENTER CONSTRUCTION MARKET SIZE

The U.S. data center construction market size by investment was valued at USD 83.97 billion in 2025 and is expected to reach USD 154.49 billion by 2031, growing at a CAGR of 10.70%. The rapid adoption of generative AI, enterprise cloud migration, and data-intensive digital applications is fundamentally reshaping infrastructure demand in the Data Center Construction Market in the U.S. and the broader U.S. Data Center Infrastructure Market. AI workloads, particularly large language models as well as GPU-based training and inference, require significantly higher compute density, storage capacity, and power intensity than traditional enterprise IT, accelerating demand for AI data center infrastructure, high-performance computing data centers, and hyperscale cloud infrastructure.

Enterprises are accelerating migration from on-premise systems to public and hybrid cloud platforms to improve scalability, resilience, and cost efficiency. This has driven large enterprises to expand data center footprints to support sustained high-performance workloads, meet the low-latency requirements of real-time applications, and comply with national data sovereignty and regulatory standards, thereby reinforcing long-term demand for U.S. data center development and edge computing infrastructure across the country.

The cost of data center construction in the U.S. can range from $9 million to $14 million per MW, depending on the location. These elevated costs are influenced by factors such as limited land availability, high labor rates, inflation, and access to power. Thus, operators are seeking markets that offer comparatively lower construction costs, abundant power and land, as well as favorable regulatory environments, making these locations attractive for cost-efficient development within the Data Center Building Market U.S. and the expanding U.S. Hyperscale Data Center Construction ecosystem.

Some of the top operators investing in the U.S. include Apple, Aligned Data Centers, AWS, CyrusOne, DataBank, Digital Realty, Equinix, Meta, NTT DATA, and Vantage Data Centers, among others, supporting large-scale investments in hyperscale cloud infrastructure, AI data center infrastructure, and advanced edge computing infrastructure.

U.S. DATA CENTER CONSTRUCTION MARKET KEY TRENDS

AI Transforming the Landscape of the Data Center Market

The AI industry is set to increase the size of hyperscale data centers significantly, driving rapid expansion across the U.S. Hyperscale Data Center Construction segment. Even though current AI investments haven’t fully offset the growth in hyperscale data centers, the capacity of these facilities, especially those supporting AI data center infrastructure and high-performance computing data centers, is expected to almost triple over the next five to six years. With the rising adoption of AI across several industries, new data centers are being designed to support high-density AI-based workloads and large-scale hyperscale cloud infrastructure deployments.

With the rise in the development of AI-optimized data center facilities, the adoption of GPUs in data centers is significantly increasing in the U.S. data center development market. AI-based data centers utilize GPUs as they can perform massively parallel computations, train and run AI models dramatically faster, use power more efficiently for each AI task, support real-time AI inference, and enable high-density, scalable facilities for high-performance computing data centers.

In October 2025, Lambda, the Superintelligence Cloud, is setting up a next-generation AI Factory in Kansas City, Missouri, converting a vacant facility (built in 2009) into a cutting-edge AI data center. The site will be powered by over 10,000 NVIDIA Blackwell Ultra GPUs, with plans to expand its capacity in later phases, strengthening the U.S. Data Center Construction Market and accelerating innovation in AI data center infrastructure.

Advance Cooling Solutions for AI/ML Workloads

There is a growing emphasis on sustainable and innovative technologies for data centers across the United States Data Center Construction Market Size landscape. As computing power demands and performance expectations rise, driven by advancements in Artificial Intelligence (AI), the Internet of Things (IoT), and Machine Learning (ML), the need for power usage will increase, resulting in higher temperatures within IT infrastructure. These cutting-edge cooling solutions, including liquid cooling data centers, are essential for ensuring performance, reliability, and reduced energy and water consumption, which are critical as AI and ML become the primary drivers of computing demand.

The market is observing an increasing number of partnerships among data center operators, cooling technology vendors, chip manufacturers, and energy innovators. These collaborations are becoming essential for developing sustainable AI data center infrastructure. They facilitate the adoption of liquid cooling data centers, hybrid thermal systems, and energy-efficient designs that support high-density computing while managing energy consumption and minimizing environmental impact. This is crucial for meeting the competitive demands and regulatory standards of modern data centers in the U.S. Data Center Infrastructure Market.

For instance, in November 2025, Switch and Schneider Electric signed an expanded USD 1.9 billion agreement, marking the largest data center cooling contract in North America. Under the supply capacity deal, Schneider Electric will provide prefabricated power modules and its Uniflair chiller systems for Switch’s facilities, with the chillers set to be used in the U.S. for the first time, advancing liquid cooling data centers and energy-efficient Data Center Building Market U.S. developments.

The electrical infrastructure is witnessing several innovations in the UPS systems, generators, transfer switches & switchgears and other electrical equipment across the U.S. data center construction market. Some of these innovations include HVO fuel for generator sets, which reduces emissions as a measure to curb environmental impact within hyperscale cloud infrastructure developments.

Additionally, several innovative UPS batteries, such as Nickel-Zinc (NiZn) and Sodium-Ion batteries, are gaining traction in the U.S. Data Center Infrastructure Market due to their high power density, safety, sustainability, and efficiency benefits.

Liquid cooling data centers are becoming a significant trend that major colocation operators are implementing in their data center facilities. It is emerging as a key differentiator for colocation providers as AI and compute-intensive workloads continue to grow across AI data center infrastructure and high-performance computing data centers. Companies like Equinix, Digital Realty, Aligned Data Centers, Microsoft, Meta, and CyrusOne are leading the way by offering scalable and energy-efficient solutions that can support the increasing demands of hyperscale cloud infrastructure.

U.S. DATA CENTER CONSTRUCTION MARKET REGIONAL ANALYSIS

In the U.S. Data Center Construction Market, the Southeastern U.S. is expected to be the largest market in 2031 in terms of power capacity, with a share of around 32%, followed by the Midwestern U.S., driven by investments in U.S. Hyperscale Data Center Construction and edge computing infrastructure.

In the Southeastern U.S., the market remains strong with a sizable pipeline of upcoming projects, driven by expansion in major hubs as well as the rise of new clusters in nearby areas. In the first nine months of 2025 alone, filings were submitted for 54 new data centers in Virginia, reinforcing the region’s dominance in the Data Center Construction Market in the U.S.

The Southwestern U.S. includes states such as Texas, Arizona, New Mexico, and Oklahoma. Among these four states, Texas and Arizona contribute to over 90% of data center investments, with strong activity in U.S. Data Center Development Market projects and hyperscale cloud infrastructure facilities.

Northeastern U.S. is a developing data center market. The demand for data centers in the New York–New Jersey market remains high. This has driven down vacancies to less than 6%. The expansion of this market can be attributed to the ongoing demand for data center space, thereby serving as a connectivity hub in the heart of New York City’s financial center, supporting edge computing infrastructure growth.

The U.S. data center construction market is projected to experience substantial growth in the Western U.S. Meta is building an $800 million data center in Cheyenne, Wyoming, on a site of about 960 acres in the High Plains Business Park. The planned facility spans 715,000 square feet and is optimized for AI data center infrastructure and high-performance computing data centers. Fortis Construction is the lead builder of the campus.

UNITED STATES DATA CENTER CONSTRUCTION MARKET – VENDOR INSIGHTS

The U.S. data center construction market includes major investors such as Apple, Applied Digital, AWS, CyrusOne, DataBank, Digital Realty, Equinix, Google, Meta, Microsoft, NTT DATA, Vantage Data Centers, STACK Infrastructure, and QTS. These companies are driving large-scale investments in hyperscale cloud infrastructure, AI data center infrastructure, and the Data Center Building Market U.S.

Other active investors include Aligned Data Centers, American Tower, CloudHQ, Cologix, Compass Datacenters, DC BLOX, EdgeConneX, EdgeCore Digital Infrastructure, Flexential, Iron Mountain, Novva Data Centers, Sabey Data Centers, Stream Data Centers, Switch, T5 Data Centers, TierPoint, Yondr, 365 Data Centers, and 5C Data Centers, supporting the expansion of the U.S. Data Center Infrastructure Market.

Emerging players such as Ada Infrastructure, CleanArc Data Centers, Edged Energy, Fleet Data Centers, Lambda, Prometheus Hyperscale, Quantum Loophole, RadiusDC, and Rowan Digital Infrastructure are increasing competition in the U.S. Hyperscale Data Center Construction landscape.

AWS plans to develop two data centers in Madison County, Mississippi, with an investment of $10 billion. The project is expected to create around 1,000 construction jobs and strengthen hyperscale cloud infrastructure, AI data center infrastructure, and edge computing infrastructure across the United States Data Center Construction Market.

SNAPSHOT

The U.S. data center construction market size by investment will reach USD 154.49 billion by 2031, growing at a CAGR of 10.70% from 2025 to 2031.

The following factors are likely to contribute to the growth of the U.S. data center construction market during the forecast period:

- M&A and Joint Ventures Enabling Data Center Construction Growth

- Tax and Sales Incentives are a Major Boost for Data Center Growth

- Enhanced Connectivity Through Submarine Cables Driving Growth in Data Center Market

- Acceleration of Cloud Infrastructure Uptake

Base Year: 2025

Forecast Year: 2026-2031

The study considers the present scenario of the U.S. data center construction market and its market dynamics for 2026−2031. It covers a detailed overview of several market growth enablers, restraints, and trends. The report offers both the demand and supply aspects of the market. It profiles and examines leading companies and other prominent ones operating in the market.

The report includes the investment in the following areas:

- Facility Type

- Hyperscale Data Centers

- Colocation Data Centers

- Enterprise Data Centers

- Infrastructure

- Electrical Infrastructure

- Mechanical Infrastructure

- General Construction

- Electrical Infrastructure

- UPS Systems

- Generators

- Transfer Switches & Switchgears

- PDUs

- Other Electrical Infrastructure

- Mechanical Infrastructure

- Cooling Systems

- Racks

- Other Mechanical Infrastructure

- Cooling System

- CRAC & CRAH Units

- Chillers Units

- Cooling Towers, Condensers, and Dry Coolers

- Other Cooling Units

- Cooling Techniques

- Air-based Cooling Technique

- Liquid-based Cooling Technique

- General Construction

- Core & Shell Development

- Installation & Commissioning Services

- Engineering & Building Design

- Fire Detection & Suppression

- Physical Security

- DCIM/BMS Solutions

- Tier Standards

- Tier I & Tier II

- Tier III

- Tier IV

- Geography

- Southeastern U.S.

- Midwestern U.S.

- Southwestern U.S.

- Western U.S.

- Northeastern U.S.

Key Data Center Support Infrastructure Providers

- ABB

- Caterpillar

- Cummins

- Delta Electronics

- Eaton

- Legrand

- Rolls-Royce

- Schneider Electric

- STULZ

- Vertiv

Other Data Center Support Infrastructure Providers

- Airedale

- Alfa Laval

- Asetek

- Bloom Energy

- Carrier

- Condair

- Cormant

- Cyber Power Systems

- Enlogic

- FNT Software

- Generac Power Systems

- Green Revolution Cooling (GRC)

- HIMOINSA (Yanmar)

- HITEC Power Protection

- Johnson Controls

- KOHLER (Rehlko)

- KyotoCooling

- Mitsubishi Electric

- Natron Energy

- NetZoom

- Nlyte Software

- Rittal

- Siemens

- Trane

- ZincFive

Key Data Center Construction Contractors

- AECOM

- Ames Construction

- Arup

- Barge Design Solutions

- Burns & McDonnell

- Corgan

- DPR Construction

- Fortis Construction

- Haydon

- Holder Construction

- Jacobs

- KDC

- Kiewit Corporation

- Lewis Michael Consultants

- Morgan Construction

- Morgan Corp

- Page

- Rogers-O’Brien Construction

- Rosendin Electric

- Syska Hennessy Group

- Turner Construction

Other Data Center Construction Contractors

- AlfaTech

- Aplena

- Black & Veatch

- BlueScope Construction

- Brasfield & Gorrie

- CallisonRTKL

- Clark Construction Group

- Clayco

- Climatec

- Clune Construction

- EMCOR Group

- EYP MCF

- Fitzpatrick Architects

- Fluor Corporation

- Gensler

- Gilbane Building Company

- Gray

- HDR

- Hensel Phelps

- HITT Contracting

- Hoffman Construction

- JE Dunn Construction

- JHET Architects,

- JTM Construction Group

- kW Engineering

- Linesight

- M+W Group (Exyte)

- McCarthy Building Companies

- Morrison Hershfield

- Mortenson

- Pepper Construction

- Rosendin

- Ryan Companies

- Salute Mission Critical

- Sheehan Nagle Hartray Architects

- Skanska

- Southland Industries

- STO Building Group

- Sturgeon Electric Company

- Suffolk Construction

- Sundt Construction

- The Mulhern Group

- The Walsh Group

- The Weitz Company

- The Whiting-Turner Contracting Co.

- TRINITY Group Construction

- Walbridge

- WSP

Key Data Center Investors

- Apple

- Applied Digital

- AWS

- CyrusOne

- DataBank

- Digital Realty

- Equinix

- Meta

- Microsoft

- NTT DATA

- Vantage Data Centers

Other Data Center Investors

- AAIM Data Centers

- Aligned Data Centers

- American Tower

- Aubix

- Centersquare

- CloudHQ

- Cologix

- Compass Datacenters

- COPT Data Center Solutions

- Core Scientific

- Centra

- Crusoe

- DartPoints

- DC BLOX

- DigiPowerX (DigiHost)

- EdgeConneX

- EdgeCore Digital Infrastructure

- Element Critical

- FifteenFortySeven Critical Systems Realty (1547)

- Flexential

- H5 Data Centers

- HostDime

- Hut 8

- Iron Mountain

- Netrality Data Centers

- Novva Data Centers

- PhoenixNAP

- PowerHouse Data Centers

- Prime Data Centers

- QTS Realty Trust

- Sabey Data Centers

- Skybox Datacenters

- STACK Infrastructure

- Stream Data Centers

- Switch

- T5 Data Centers

- TierPoint

- WhiteFiber

- Yondr

- 365 Data Centers

- 5C Data Centers

New Entrants

- Ada Infrastructure

- Ardent Data Centers

- Beale infrastructure

- Big Sky Digital Infrastructure

- CleanArc Data Centers

- CloudBurst Data Centers,

- Colovore

- Crane Data Centers

- Edged Energy

- Fleet Data centers

- Lambda

- LightHouse Data Centers

- Metroblocks

- NE Edge

- Penzance

- Prometheus Hyperscale

- Quantum Loophole

- RadiusDC

- Related digital

- Rowan Digital Infrastructure

- Sailfish Investors

- Tract

U.S. DATA CENTER CONSTRUCTION MARKET FAQs

How big is the U.S. data center construction market?

What is the estimated market size in terms of area in the U.S. data center construction market by 2031?

What is the growth rate of the U.S. data center construction market?

What are the key trends in the U.S. data center construction market?

How many MW of power capacity is expected to reach the U.S. data center construction market by 2031?

For more details, please reach us at [email protected]

1. ABOUT ARIZTON

2. ABOUT OUR DATA CENTER CAPABILITIES

3. WHAT’S INCLUDED

4. SEGMENTS INCLUDED

5. RESEARCH METHODOLOGY

6. MARKET AT GLANCE

7. PREMIUM INSIGHTS

8. INTRODUCTION

9. INVESTMENT OPPORTUNITIES

9.1. INVESTMENT: MARKET SIZE & FORECAST

9.2. AREA: MARKET SIZE & FORECAST

9.3. POWER CAPACITY: MARKET SIZE & FORECAST

9.4. SUPPORT INFRASTRUCTURE: MARKET SIZE & FORECAST

10. MARKET DYNAMICS

10.1. MARKET OPPORTUNITIES & TRENDS

10.2. MARKET GROWTH ENABLERS

10.3. MARKET RESTRAINTS

10.4. SITE SELECTION CRITERIA

11. FACILITY TYPE SEGMENTATION

11.1. HYPERSCALE DATA CENTERS

11.2. COLOCATION DATA CENTERS

11.3. ENTERPRISE DATA CENTERS

12. INFRASTRUCTURE SEGMENTATION

12.1. ELECTRICAL INFRASTRUCTURE

12.2. MECHANICAL INFRASTRUCTURE

12.3. COOLING SYSTEMS

12.4. COOLING TECHNIQUES

12.5. GENERAL CONSTRUCTION

13. TIER STANDARDS SEGMENTATION

14. GEOGRAPHY SEGMENTATION

15. SOUTH-EASTERN US

15.1. INVESTMENTS

15.2. AREA

15.3. POWER CAPACITY

15.4. KEY SUPPORT INFRASTRUCTURE ADOPTION

15.5. INDUSTRIAL ELECTRICITY PRICING

15.6. LIST OF UPCOMING DATA CENTER PROJECTS

16. MID-WESTERN US

16.1. INVESTMENTS

16.2. AREA

16.3. POWER CAPACITY

16.4. KEY SUPPORT INFRASTRUCTURE ADOPTION

16.5. INDUSTRIAL ELECTRICITY PRICING IN MID-WESTERN US

16.6. LIST OF UPCOMING DAT ACENTER PROJECTS

17. SOUTH-WESTERN US

17.1. INVESTMENTS

17.2. AREA

17.3. POWER CAPACITY

17.4. KEY SUPPORT INFRASTRUCTURE ADOPTION

17.5. INDUSTRIAL ELECTRICITY PRICING IN SOUTH-WESTERN US

17.6. LIST OF UPCOMING DAT ACENTER PROJECTS

18. WESTERN US

18.1. INVESTMENTS

18.2. AREA

18.3. POWER CAPACITY

18.4. KEY SUPPORT INFRASTRUCTURE ADOPTION

18.5. INDUSTRIAL ELECTRICITY PRICING IN WESTERN US

18.6. LIST OF UPCOMING DAT ACENTER PROJECTS

19. NORTH-EASTERN US

19.1. INVESTMENTS

19.2. AREA

19.3. POWER CAPACITY

19.4. KEY SUPPORT INFRASTRUCTURE ADOPTION

19.5. INDUSTRIAL ELECTRICITY PRICING IN NORTH-EASTERN US

19.6. LIST OF UPCOMING DAT ACENTER PROJECTS

20. COMPETITIVE LANDSCAPE

20.1. SUPPORT INFRASTRUCTURE PROVIDERS

20.2. CONSTRUCTION CONTRACTORS & SUBCONTRACTORS

20.3. DATA CENTER INVESTORS

21. MARKET PARTICIPANTS

21.1. KEY DATA CENTER SUPPORT INFRASTRUCTURE PROVIDERS

21.2. OTHER DATA CENTER SUPPORT INFRASTRUCTURE PROVIDERS

21.3. KEY DATA CENTER CONTRACTORS

21.4. OTHER DATA CENTER CONTRCTORS

21.5. KEY DATA CENTER INVESTORS

21.6. OTHER DATA CENTER INVESTORS

21.7. NEW ENTRANTS

22. QUANTITATIVE SUMMARY

23. APPENDIX

23.1. ABBREVIATIONS

23.2. DEFINITIONS

23.3. SEGMENTAL COVERAGE

Select a license type that suits your business needs

Single User Licence

- Report accessible by one user only

- Free 10% or 3 days of customization

- Free post-sale service assistance

- Continuous support through email

5 User Licence

- Report accessible by 5 users within the organization

- Free 15% or 4.5 days of customization

- Continuous support through email and telephone

- Free analyst hour

- Free Upgrade: If an updated report published within 180 days of purchase, you will get the revised report free of charge

Corporate Licence

- Free Datasheet worth $1500

- Report accessible by the entire organization

- Free 20% or 6 days of customization

- Free post-sale service assistance

- Continuous support through email and telephone

- Direct access to lead analysts

- Free analyst hour

- Free Upgrade: If an updated report published within 180 days of purchase, you will get the revised report free of charge

Datasheet Licence

- Report accessible by 1 user only

- Free 15% or 32 hours of customization

- Free post-sale service assistance

- Direct access to lead analysts

Frequently Asked Questions

How big is the U.S. data center construction market?

What is the estimated market size in terms of area in the U.S. data center construction market by 2031?

What is the growth rate of the U.S. data center construction market?

What are the key trends in the U.S. data center construction market?

How many MW of power capacity is expected to reach the U.S. data center construction market by 2031?

Other RELATED Reports

U.S. Data Center Colocation Market - Industry Outlook & Forecast 2025-2030

Published : August 2025