U.S. Data Center Colocation Market - Industry Outlook & Forecast 2026-2031

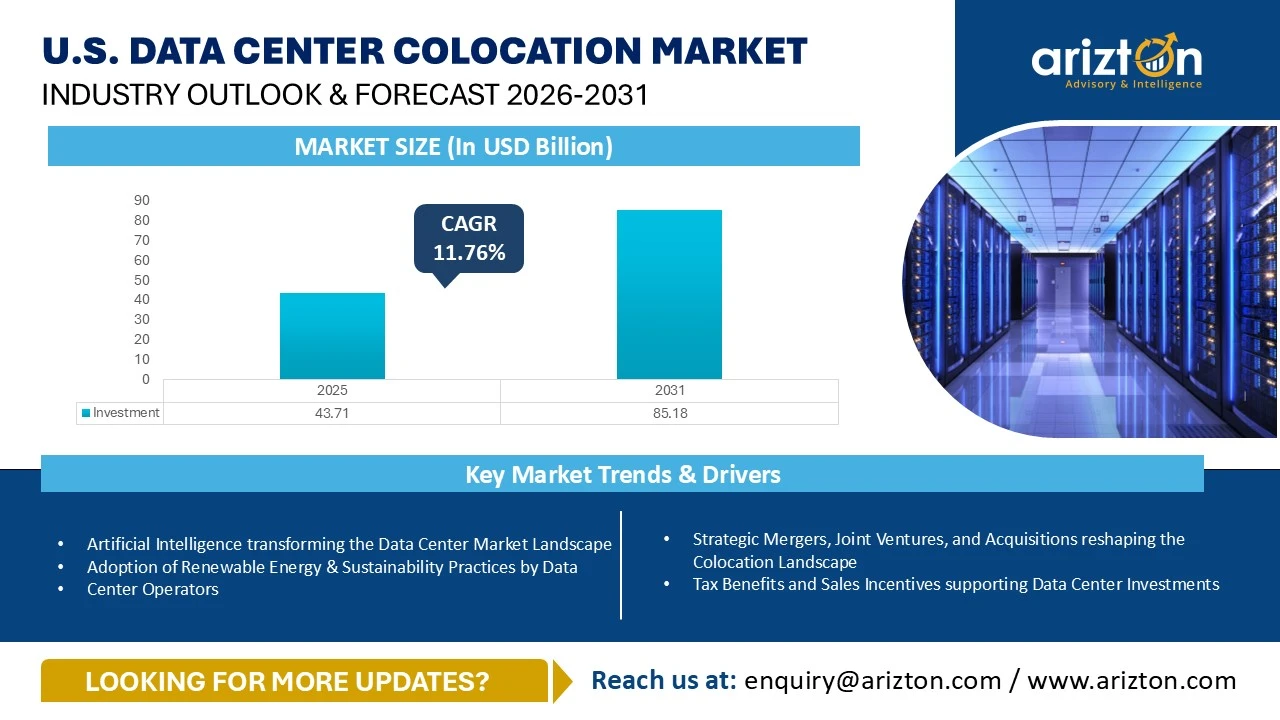

U.S. DATA CENTER COLOCATION MARKET SIZE BY INVESTMENT WAS VALUED AT USD 43.71 BILLION IN 2025 AND IS EXPECTED TO REACH USD 85.18 BILLION BY 2031, GROWING AT A CAGR OF 11.76% DURING THE FORECAST PERIOD.

U.S. Data Center Colocation Market Growth Insights – Market Area to Reach 30.02 Million Sq. Ft. and Power Capacity to Surpass 7,542 MW by 2031, Driven by Generative AI Adoption, Enterprise Cloud Migration, Data-Intensive Workloads, and Expanding Colocation Infrastructure Across the Uited States (2026–2031)

To Be Published : July 2026

Last Updated : July 2026

format: PDF

edition : Fourth Edition

194 pages

region

countries

66 company

9 segments

Purchase Options

U.S. Data Center Colocation Market - Industry Outlook & Forecast 2026-2031

U.S. DATA CENTER COLOCATION MARKET SIZE BY INVESTMENT WAS VALUED AT USD 43.71 BILLION IN 2025 AND IS EXPECTED TO REACH USD 85.18 BILLION BY 2031, GROWING AT A CAGR OF 11.76% DURING THE FORECAST PERIOD.

The U.S. Data Center Colocation Market Report Includes

- Colocation Type: Retail Colocation and Wholesale Colocation

- Infrastructure: Electrical Infrastructure, Mechanical Infrastructure, and General Construction

- Electrical Infrastructure: UPS Systems, Generators, Transfer Switches & Switchgear, PDUs, and Other Electrical Infrastructure

- Mechanical Infrastructure: Cooling Systems, Racks, and Other Mechanical Infrastructure

- Cooling Systems: CRAC & CRAH Units, Chiller Units, Cooling Towers, Condensers & Dry Coolers, Economizers & Evaporative Coolers, and Other Cooling Units

- Cooling Techniques: Air-based Cooling and Liquid-based Cooling

- General Construction: Core & Shell Development, Installation & Commissioning Services, Engineering & Building Design, Fire Detection & Suppression, Physical Security, and DCIM/BMS Solutions

- Tier Standard: Tier I & II, Tier III, and Tier IV

- Geography: Southeastern U.S., Southwestern U.S., Western U.S., Midwestern U.S., and Northeastern U.S.

Industry Analysis Report, Regional Outlook, Growth Potential, Price Trends, Competitive Market Share & Forecast 2026–2031

This report includes market data points, ranging from trend

analyses to market estimates & forecasts that you can customize

U.S. DATA CENTER COLOCATION MARKET REPORT SCOPE

| REPORT ATTRIBUTE | DETAILS |

|---|---|

| MARKET SIZE BY INVESTMENT 2031 | USD 85.18 Billion |

| MARKET SIZE BY INVESTMENT 2025 | USD 43.71 Billion |

| CAGR - INVESTMENT (2025-2031) | 11.76% |

| MARKET SIZE - COLOCATION REVENUE 2031 | USD 46.90 Billion |

| MARKET SIZE AREA (2031) | 30.02 million sq. feet |

| POWER CAPACITY (2031) | 7,542 MW |

| BASE YEAR | 2021 |

| FORECAST YEAR | 2026-2031 |

| MARKET SEGMENTS | Colocation Service, Infrastructure, Electrical Infrastructure, Mechanical Infrastructure, Cooling Systems, Cooling Techniques, General Construction, Tier Standards, and Geography |

| GEOGRAPHICAL ANALYSIS | Southeastern U.S., Southwestern U.S., Western U.S., Midwestern U.S., and Northeastern U.S. |

U.S. DATA CENTER COLOCATION MARKET SIZE

The U.S. data center colocation market size by investment was valued at USD 43.71 billion in 2025 and is expected to reach USD 85.18 billion by 2031, growing at a CAGR of 11.76% during the forecast period. The rapid adoption of generative AI, enterprise cloud migration, and data-intensive digital applications is fundamentally reshaping infrastructure demand in the U.S. market.

The U.S. data center colocation market is estimated to witness a cumulative investment of around $461.62 billion during 2026–2031; the South-Eastern US region will contribute around $127.84 billion, representing around 28% of the overall share. The market provides exciting opportunities to investors looking to enter and invest in the market.

The cost of constructing a data center in the US can range from $9 million to $14 million per megawatt (MW), depending on the location. These high costs are influenced by several factors, including limited land availability, elevated labor rates, inflation, and access to power.

Northern Virginia is recognized as the data center capital of the world, often referred to as an alley of data centers. It continues to be the largest data center market, boasting over 4 gigawatts (GW) of core and shell colocation capacity. This market is increasingly becoming a prime location for large contiguous capacities and hyperscale campuses, with growing competition and intensifying pricing pressures.

U.S. DATA CENTER COLOCATION MARKET KEY TRENDS

Artificial Intelligence transforming the Data Center Market Landscape

- The artificial intelligence (AI) industry is set to significantly increase the size of hyperscale data centers. Although current AI investments have not fully compensated for the growth in hyperscale data centers, the capacity of these data centers, especially for AI workloads, is expected to almost triple in the next five to six years. With the rising adoption of AI across several industries, new data centers are being designed to support high-density AI-based workloads.

- With the rise in the development of AI-optimized data center facilities, the adoption of GPUs in data centers is significantly increasing in the market. AI-based data centers utilize GPUs as they can perform massively parallel computations, train and run AI models dramatically faster, use power more efficiently for each AI task, support real-time AI inference, and enable high-density, scalable facilities.

- In May 2025, NTT DATA announced a major expansion, delivering over 370MW of new capacity, launching 10 new data centers, and enabling more than 200MW of AI workloads. Once online, the company will position itself as the world’s third-largest data center provider. As AI transforms infrastructure requirements, the company continues to lead in innovation by deploying advanced liquid cooling systems and designing facilities specifically for high-density AI workloads.

- In January 2025, the Trump administration unveiled Stargate, a new AI infrastructure initiative, spearheaded by the private sector (in collaboration with OpenAI). With a planned investment of $500 billion over the next four years, the project represents a major financial commitment aimed at advancing AI innovation and reinforcing the U.S. leadership in the field.

Adoption of Renewable Energy & Sustainability Practices by Data Center Operators

- With the rapid growth in AI and cloud workloads, energy demand is increasing significantly. Hence, sustainability has become essential for managing carbon emissions, operating costs, and ensuring long-term grid stability. Data centers must prioritize sustainability, especially as local governments and residents are increasingly opposing projects that consume excessive energy, strain water resources, and contribute to higher emissions or noise levels.

- In August 2025, Soluna surpassed 1GW of clean computing capacity with the launch of its latest wind and solar-powered data centers in Texas. The two new facilities—Project Fei and Project Gladys—expanded the company’s renewable-powered footprint and pushed its total sustainable data center capacity beyond the 1GW milestone.

- In July 2025, Digital Realty achieved 75% renewable energy usage for its global electricity needs—a 9% increase from the previous year—and secured 1.5GW of renewable energy capacity through contracts. It matched 185 data centers with 100% renewable energy, implemented efficiency projects that save 42,400MWh annually, and earned the ENERGY STAR certification for 69% of its U.S. managed portfolio.

- Several data center operators have committed to becoming carbon neutral. For example, Equinix and CyrusOne have announced plans to achieve carbon neutrality by 2030, indicating that their data center facilities will be powered by carbon-free, renewable energy. These commitments reflect the industry's response to increasing energy consumption, investor demand for strong environmental, social, and governance (ESG) performance, as well as the regulatory pressure to decarbonize before 2030.

U.S. DATA CENTER COLOCATION MARKET SEGMENTATION INSIGHTS

- The electrical infrastructure is witnessing several innovations in UPS systems, generators, transfer switches & switchgear, and other electrical equipment. Most data centers adopt N+1 diesel generators, providing backup fuel for up to 24 hours or more. For instance, the NEO-01 facility of Aligned Data Centers in Ohio is equipped with 2N power redundancy and diverse utility feeds.

- Additionally, several innovative UPS batteries such as Nickel-Zinc (NiZn) and Sodium-Ion batteries are gaining traction in the market due to their high-power density, safety, sustainability, and other factors. The CH1 facility of NTT DATA in Chicago, Illinois, is equipped with four primary 34.5kV utility feeds, N+1 redundancy for UPS systems, and eight 1 MW UPS modules for every 6MW capacity.

- AI workloads are changing cooling standards in U.S. data centers, as traditional air cooling is insufficient to manage the heat output from GPU-dense clusters. The market is observing an increasing number of partnerships among data center operators, cooling technology vendors, chip manufacturers, and energy innovators.

- In March 2025, Crypto and IREN, an AI data center company, announced plans to develop a 75 MW AI data center in Texas. As per the agreement, the companies are planning to deploy a new 75 MW liquid-cooling data center for AI/HPC at its Childress site in Texas. It will be designed to support 200 kW per rack via direct-to-chip cooling for NVIDIA’s Blackwell GPUs.

U.S. DATA CENTER COLOCATION MARKET GEOGRAPHICAL ANALYSIS

- In the U.S. data center colocation market, the South-Eastern U.S., including states such as Virginia, Georgia, and North Carolina, continues to lead in data center investments, contributing over $15.04 billion in 2025.

- This is followed by the Southwestern U.S., with investments exceeding $14.95 billion in the same year, while the Midwestern U.S. region accounted for approximately $6.07 billion.

- In the South-Eastern U.S., the market remains strong with a sizable pipeline of upcoming projects, driven by expansion in major hubs as well as the rise of new clusters in nearby areas. The region is expected to add a power capacity of around 13,628MW during 2026–2031.

- The South-Western U.S. includes states such as Texas, Arizona, New Mexico, and Oklahoma. Among these four states, Texas and Arizona contribute to over 90% of the data center investments.

- North-Eastern U.S. is a developing data center market. The demand for data centers in the New York-New Jersey market remains high. This has driven down vacancies to less than 6%. The expansion of the New York-New Jersey data center market can be attributed to the ongoing demand for data center space, thereby serving as a connectivity hub in the heart of New York City’s financial center.

- In November 2025, the data center development initiatives were officially banned in Lordstown, Ohio, following a vote by the Lordstown Village Council to approve an ordinance prohibiting all such proposals. The decision was prompted by a planned project from Bristolville 25 Developer LLC on a 133-acre site near Tod Avenue. This regulatory change can reduce investment in the mid-western region, potentially prompting operators to explore alternative locations for future developments.

U.S. DATA CENTER COLOCATION MARKET VENDOR LANDSCAPE

- The U.S. data center colocation market has the presence of key investors such as Applied Digital, CyrusOne, DataBank, Digital Realty, Equinix, NTT DATA, QTS Realty Trust, and Vantage Data Centers.

- The market has a presence of several other investors, such as AAIM Data Centers, Aligned Data Centers, American Tower, CloudHQ, Cologix, Compass Datacenters, COPT Data Center Solutions, Core Scientific, Crusoe, DC BLOX, DigiPowerX (DigiHost), EdgeConneX, Edged, EdgeCore Digital Infrastructure, Element Critical, FifteenFortySeven Critical Systems Realty (1547), Flexential, H5 Data Centers, HostDime, Hut 8, Iron Mountain, Netrality Data Centers, Novva Data Centers, PowerHouse Data Centers, Prime Data Centers, RadiusDC, Sabey Data Centers, Skybox Datacenters, STACK Infrastructure, Stream Data Centers, Switch, T5 Data Centers, TierPoint, WhiteFiber, Yondr, 365 Data Centers, 5C Data Centers and others.

- New entrants include Ada Infrastructure, Ardent Data Centers, Beale Infrastructure, Big Sky Digital Infrastructure, CleanArc Data Centers, CloudBurst Data Centers, Colovore, Crane Data Centers, Fleet Data Centers, Lambda, LightHouse Data Centers, Metroblocks, NE Edge, Penzance, Prometheus Hyperscale, Related Digital, Rowan Digital Infrastructure, and Tract.

- In August 2025, Vantage Data Centers announced its largest investment to date (exceeding $25 billion) to develop the Frontier campus in Shackelford County, Texas. The 1,200-acre, 1.4 GW campus will comprise 10 data centers, totaling approximately 3.7 million square feet, designed to support ultra-high-density racks of 250 kW and above, reflecting a shift toward AI- and HPC-driven infrastructure.

SNAPSHOT

The U.S. data center colocation market by investment is projected to reach USD 85.18 billion by 2031, growing at a CAGR of 11.76% from 2025 to 2031.

The following factors are likely to contribute to the growth of the U.S. data center colocation market during the forecast period:

- Rising Adoption of Cloud-based Services

- Government Support & Digital Economy Push

- Improvement in Connectivity via Submarine Cables

Base Year: 2025

Forecast Year: 2026-2031

The report considers the present scenario of the U.S. data center colocation market and its market dynamics for 2026−2031. It covers a detailed overview of several market growth enablers, restraints, and trends. The study includes the demand and supply aspects of the U.S. data center colocation industry.

- Strategic Mergers, Joint Ventures, and Acquisitions reshaping the Colocation Landscape

- Tax Benefits and Sales Incentives supporting Data Center Investments

- Expansion of Submarine Cable Networks enhancing Digital Connectivity

- Rising Adoption of Cloud Infrastructure strengthening Data Center Demand

Prominent Colocation Operators

- Applied Digital

- CyrusOne

- DataBank

- Digital Realty

- Equinix

- NTT DATA

- QTS Realty Trust

- Vantage Data Centers

Other Prominent Colocation Operators

- AAIM Data Centers

- Aligned Data Centers

- American Tower

- AUBix

- Csquare

- CloudHQ

- Cologix

- Compass Datacenters

- COPT Data Center Solutions

- Core Scientific

- Centra

- Crusoe

- DC BLOX

- DigiPowerX (DigiHost)

- EdgeConneX

- Edged

- EdgeCore Digital Infrastructure

- Element Critical

- FifteenFortySeven Critical Systems Realty (1547)

- Flexential

- H5 Data Centers

- HostDime

- Hut 8

- Iron Mountain

- Netrality Data Centers

- Novva Data Centers

- PowerHouse Data Centers

- Prime Data Centers

- RadiusDC

- Sabey Data Centers

- Skybox Datacenters

- STACK Infrastructure

- Stream Data Centers

- Switch

- T5 Data Centers

- TierPoint

- WhiteFiber

- Yondr

- 365 Data Centers

- 5C Data Centers

New Entrants

- Ada Infrastructure

- Ardent Data Centers

- Beale infrastructure

- Big Sky Digital Infrastructure

- CleanArc Data Centers

- CloudBurst Data Centers

- Colovore

- Crane Data Centers

- Fleet Data Centers

- Lambda

- LightHouse Data Centers

- Metroblocks

- NE Edge

- Penzance

- Prometheus Hyperscale

- Related digital

- Rowan Digital Infrastructure

- Tract

Segmentation by Colocation Type

- Retail Colocation

- Wholesale Colocation

Segmentation by Infrastructure

- Electrical Infrastructure

- Mechanical Infrastructure

- General Construction

Segmentation by Electrical Infrastructure

- UPS Systems

- Generators

- Transfer Switches & Switchgear

- PDUs

- Other Electrical Infrastructure

Segmentation by Mechanical Infrastructure

- Cooling Systems

- Racks

- Other Mechanical Infrastructure

Segmentation by Cooling Systems

- CRAC & CRAH Units

- Chiller Units

- Cooling Towers, Condensers & Dry Coolers

- Economizers & Evaporative Coolers

- Other Cooling Units

Segmentation by Cooling Techniques

- Air-based Cooling

- Liquid-based Cooling

Segmentation by General Construction

- Core & Shell Development

- Installation & Commissioning Services

- Engineering & Building Design

- Fire Detection & Suppression

- Physical Security

- DCIM/BMS Solutions

Segmentation by Tier Standard

- Tier I & II

- Tier III

- Tier IV

Segmentation by Geography

- U.S.

- Southeastern U.S.

- Southwestern U.S.

- Western U.S.

- Midwestern U.S.

- Northeastern U.S.

U.S. DATA CENTER COLOCATION MARKET FAQs

How big is the U.S. data center colocation market?

What is the growth rate of the U.S. data center colocation market?

What are the key trends in the U.S. data center colocation market?

What is the estimated market size in terms of area in the U.S. data center colocation market by 2031?

How much MW of power capacity is expected to reach the U.S. data center colocation market by 2031?

How big is the U.S. data center colocation market?

What is the growth rate of the U.S. data center colocation market?

What are the key trends in the U.S. data center colocation market?

What is the estimated market size in terms of area in the U.S. data center colocation market by 2031?

How much MW of power capacity is expected to reach the U.S. data center colocation market by 2031?

For more details, please reach us at [email protected]

For more details, please reach us at [email protected]

Select a license type that suits your business needs

Single User Licence

- Report accessible by one user only

- Free 10% or 3 days of customization

- Free post-sale service assistance

- Continuous support through email

5 User Licence

- Report accessible by 5 users within the organization

- Free 15% or 4.5 days of customization

- Continuous support through email and telephone

- Free analyst hour

- Free Upgrade: If an updated report published within 180 days of purchase, you will get the revised report free of charge

Corporate Licence

- Free Datasheet worth $1500

- Report accessible by the entire organization

- Free 20% or 6 days of customization

- Free post-sale service assistance

- Continuous support through email and telephone

- Direct access to lead analysts

- Free analyst hour

- Free Upgrade: If an updated report published within 180 days of purchase, you will get the revised report free of charge

Datasheet Licence

- Report accessible by 1 user only

- Free 15% or 32 hours of customization

- Free post-sale service assistance

- Direct access to lead analysts

Frequently Asked Questions

How big is the U.S. data center colocation market?

What is the growth rate of the U.S. data center colocation market?

What are the key trends in the U.S. data center colocation market?

What is the estimated market size in terms of area in the U.S. data center colocation market by 2031?

How much MW of power capacity is expected to reach the U.S. data center colocation market by 2031?

How big is the U.S. data center colocation market?

What is the growth rate of the U.S. data center colocation market?

What are the key trends in the U.S. data center colocation market?

What is the estimated market size in terms of area in the U.S. data center colocation market by 2031?

How much MW of power capacity is expected to reach the U.S. data center colocation market by 2031?