U.S. Sustainable Data Center Market – Industry Outlook & Forecast 2026-2031

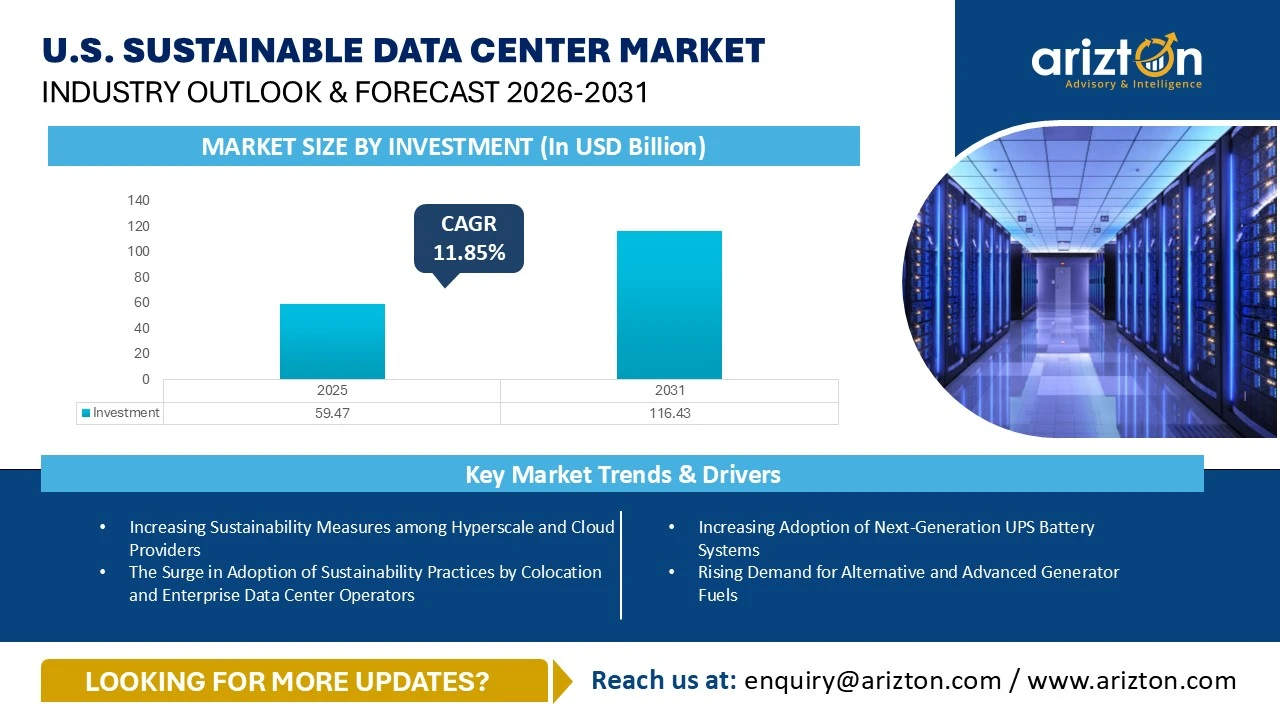

THE U.S. SUSTAINABLE DATA CENTER MARKET SIZE WAS VALUED AT USD 59.47 BILLION IN 2025 AND IS EXPECTED TO REACH USD 116.43 BILLION BY 2031, GROWING AT A CAGR OF 11.85%.

U.S. Sustainable Data Center Market Growth Insights – Power Capacity to Reach 12,144 MW by 2029, Driven by Rising Demand for Energy-Efficient Infrastructure, Sustainable Cooling Technologies, Clean Energy Integration, and Increasing Environmental Regulations 2031

Published Date : June 2026

Last Updated : July 2026

format: PDF

edition : Third Edition

222 pages

95 company

2 segments

1 region

5 countries

Purchase Options

U.S. Sustainable Data Center Market – Industry Outlook & Forecast 2026-2031

THE U.S. SUSTAINABLE DATA CENTER MARKET SIZE WAS VALUED AT USD 59.47 BILLION IN 2025 AND IS EXPECTED TO REACH USD 116.43 BILLION BY 2031, GROWING AT A CAGR OF 11.85%.

The U.S. Sustainable Data Center Market Research Report Includes Size, Share, and Growth in Terms of

- Infrastructure: Electrical Infrastructure, Mechanical Infrastructure, and General Construction

- Geography: United States (Southeastern U.S., Midwestern U.S., Southwestern U.S., Western U.S., and Northeastern U.S.)

Industry Analysis Report, Regional Outlook, Growth Potential, Price Trends, Competitive Market Share & Forecast 2026–2031.

This report includes market data points, ranging from trend

analyses to market estimates & forecasts that you can customize

U.S. SUSTAINABLE DATA CENTER MARKET REPORT SCOPE

| REPORT ATTRIBUTE | DETAILS |

|---|---|

| MARKET SIZE (2031) | USD 116.43 Billion |

| MARKET SIZE (2025) | USD 59.47 Billion |

| CAGR BY INVESTMENT (2025-2031) | 11.85% |

| POWER CAPACITY (2031) | 12,144 MW |

| HISTORIC YEAR | 2022-2024 |

| BASE YEAR | 2025 |

| FPRECAST YEAR | 2026-2031 |

| SEGMENTS BY | Infrastructure and Geography |

| GEOGRAPHICAL ANALYSIS | United States (Southeastern U.S., Midwestern U.S., Southwestern U.S., Western U.S., and Northeastern U.S.) |

U.S. SUSTAINABLE DATA CENTER MARKET SIZE

The U.S. sustainable data center market size by investment was valued at USD 59.47 billion in 2025 and is expected to reach USD 116.43 billion by 2031, growing at a CAGR of 11.85% during the forecast period. In 2025, the U.S. Sustainable data center market increased by approximately 76.57% compared to 2024 in terms of data center investments, owing to the increasing demand for sustainable data center infrastructure and the surge in environmental regulations. The sustainable practices support data center firms to minimize long-term data center operational costs and to enhance energy efficiency. The sustainable cooling technologies, energy-efficient electrical and mechanical infrastructure, clean energy integration, and smart infrastructure management in data centers help the companies to minimize electricity and water usage in the facilities. The growing usage of renewable energy is reshaping the U.S. sustainable data center market as operators are seeking to reduce their environmental impact. Data center companies are increasingly sourcing electricity from renewable resources such as solar, wind, and hydropower to lower carbon emissions and decrease dependence on fossil fuel-based energy. Sustainable data center operations support data center operators in minimizing the risks related to climate disruptions and environmental regulations. In 2025, the Southeast U.S. resulted in generating the highest sustainable data center investments in the US sustainable data center market, representing a sustainable data center investment share of around 30.87%, followed by the Midwestern U.S., the Southwest U.S., the Western U.S., and the Northeast U.S.

U.S. SUSTAINABLE DATA CENTER MARKET SEGMENTAL ANALYSIS

- The data center operators in the U.S. are increasingly replacing traditional VRLA batteries with more sustainable alternatives such as lithium-ion, liquid metal, sodium-ion, and nickel-zinc batteries, while vendors including ABB, Vertiv, and Schneider Electric continue to offer flexible and sustainable batteries and UPS systems to support data center operators in improving facility performance and reducing operating costs.

- Data center operators are increasingly transitioning from conventional diesel fuel to hydrotreated vegetable oil (HVO) as a cleaner alternative for backup generators, and the data centers across the US are expected to significantly reduce diesel generator usage by 2031 as various data center operators, like Vantage Data Centers and STACK Infrastructure, among others are increasingly adopting renewable hydrotreated vegetable oil-powered generators to support their sustainability and carbon reduction goals.

- The demand for PDUs is witnessing strong growth due to the rapid development of new data centers and the increasing number of hyperscale facilities. The growing adoption of intelligent PDUs among the US data centers will enable data center operators to monitor power in real-time and improve energy efficiency while reducing electricity consumption and lowering carbon emissions.

- The data center industry in the US is expected to witness higher adoption of hybrid cooling systems that combine air- and liquid-based technologies to improve cooling efficiency, while many operators are also increasingly utilizing natural air-cooling technologies to reduce their reliance on water-intensive cooling solutions.

- The expansion of AI workloads is driving the need for more advanced cooling infrastructure in data centers, as AI servers consume more power and generate greater heat than conventional systems. To address these challenges, operators are increasingly deploying innovative cooling technologies that enhance thermal efficiency and reduce energy usage. For instance, in January 2026, the French technology company Viridien announced plans to develop a data center campus in Washington County that is expected to incorporate immersion cooling technology.

- The U.S. sustainable data center market is attracting significant investments in energy-efficient infrastructure and intelligent facility management technologies, with data center operators increasingly deploying AI-driven software, automation platforms, and advanced building management systems to optimize power utilization and cooling performance in data centers. For example, STACK Infrastructure has equipped its SVY01A data center in Silicon Valley, California, with a building management system (BMS) control system.

- Data center operators are increasingly incorporating sustainable construction practices by using eco-friendly building materials, energy-efficient designs, and modular development practices to minimize environmental impact. Many companies are also pursuing certifications such as LEED to highlight their commitment to sustainability. For instance, PowerHouse Data Centers uses recycled green concrete instead of conventional steel in its data centers across the US to help data center operators reduce construction-related carbon emissions.

U.S. SUSTAINABLE DATA CENTER MARKET KEY TRENDS

Increasing Adoption of Next-Generation UPS Battery Systems

- The growing development of AI-optimized data centers across the U.S. is driving the demand for reliable and energy-efficient backup power infrastructure, and operators are increasingly adopting advanced UPS battery technologies that provide an uninterrupted power supply during power disturbances while offering longer lifespans and a lower environmental impact.

- The US data center industry is increasingly adopting advanced UPS battery technologies, like lithium-ion batteries, as they offer higher energy efficiency, longer lifespan, and lower maintenance requirements. Additionally, emerging alternatives such as liquid metal batteries, sodium-ion batteries, and nickel-zinc batteries are gaining traction to support large-scale energy storage and reduce environmental impact compared to conventional battery systems.

- The increasing deployment of advanced UPS battery technologies is reshaping backup power systems across the U.S. data center market, as data center operators are prioritizing greater energy efficiency and sustainability. The advanced battery technologies enable data center operators to enhance energy storage capabilities, reduce maintenance needs, and minimize the environmental impact.

Rising Demand for Alternative and Advanced Generator Fuels

- The rapid growth of Artificial Intelligence and high-performance computing (HPC) workloads is significantly increasing electricity demand across US data centers, driving the need for reliable backup generators. The rising concerns over the environmental impact of traditional diesel generators are prompting data center operators to adopt advanced fuel technologies to enhance sustainability and reduce carbon emissions.

- As data center operators are seeking sustainable alternatives to diesel generators, technologies such as fuel cells, HVO (hydrotreated vegetable oil), natural gas generators, advanced nuclear energy solutions, and biofuels are gaining traction due to their ability to provide reliable backup power with lower emissions. These alternatives can reduce environmental impact in data centers while addressing the increasing demands for sustainable power infrastructure in AI and hyperscale data center facilities.

- The rising adoption of advanced fuels and low-carbon backup power technologies is playing a crucial role in enhancing sustainability across U.S. data centers. Solutions like fuel cells, hydrotreated vegetable oil, natural gas generators, nuclear-powered energy systems, and other backup power technologies are enabling data center companies to build more sustainable data centers.

Surge in Adoption of Modern Cooling Solutions

- The rapid adoption of Artificial Intelligence, machine learning, cloud computing, and high-performance computing (HPC) workloads is increasing the heat generated in data centers across the U.S., requiring data center operators to deploy advanced cooling technologies, such as direct-to-chip liquid cooling and immersion cooling technologies that enhance energy efficiency, reduce water usage, and operational costs to support sustainable data center operations.

- To enhance energy efficiency and sustainability in data centers, companies are increasingly adopting advanced cooling technologies such as free cooling, immersion cooling, and direct-to-chip liquid cooling, and are also focusing on developing underwater and floating data centers, which help the companies to reduce power consumption, improve heat dissipation efficiently, and minimize environmental impact.

- The adoption of advanced liquid cooling technologies, such as immersion cooling, direct-to-chip liquid cooling, and free cooling, among others, is anticipated to increase among data centers in the U.S. as the demand for processing complex artificial intelligence and high-performance computing (HPC) workloads is rising significantly.

New Innovations in Data Center Construction Methods

- The rapid expansion of cloud computing, AI, and hyperscale data center infrastructure in the U.S. is driving the adoption of innovative and sustainable construction methods among data center operators that reduce environmental impact and carbon emissions, optimize resource efficiency, and support long-term sustainable data center operations.

- The data center operators in the U.S. are increasingly adopting sustainable construction materials, including green concrete, wood, and timber, instead of cement. Additionally, the companies are also investing in modular construction, energy-efficient building designs, smart construction technologies, advanced cooling systems, recycled materials, and AI-optimized data center management techniques to reduce carbon emissions, minimize material waste, and improve overall resource efficiency.

- Innovative construction practices are increasingly reshaping the construction of data centers in the U.S. by enhancing sustainability, lowering environmental impact, and improving operational efficiency. The solutions, such as green concrete, modular construction, and energy-efficient building designs, are supporting data center operators to achieve their broader sustainability targets.

Advancements in Power Utilities and Smart Grid Integration

- Advancements in utility infrastructure and the adoption of smart grid technologies are enhancing data center sustainability by enabling data center operators to manage power supply more efficiently and to improve the integration of renewable energy sources for data center operations while reducing energy waste and carbon emissions.

- Microgrids and smart grids are increasingly being adopted to enhance data center sustainability and power reliability in the U.S. data center industry by enabling data center companies with localized power generation, energy storage, real-time electricity management, and renewable energy integration through continuous and resilient power supply.

- The growing adoption of microgrids and smart grids is expected to significantly enhance sustainability in data centers by enabling companies with efficient and flexible energy management, supporting the companies to reduce reliance on traditional grids, and ensuring a stable electricity supply.

Emerging Technologies Driving Demand for Liquid Cooling Systems

- The rapid expansion of emerging technologies such as artificial intelligence, machine learning, high-performance computing, cloud computing, and advanced analytics is substantially increasing the heat generated in modern data centers, thereby accelerating the need for advanced and energy-efficient liquid cooling solutions.

- As the demand for processing artificial intelligence and high-performance computing workloads is rising among the U.S. data centers, data center operators are increasingly deploying high-density racks capable of delivering rack power densities of more than 100 kW per rack to support intensive computing requirements. For example, in January 2025, Prime Data Centers planned to develop a new data center campus in California, the US, that will be equipped with racks, offering rack densities ranging between 40 kW and 120 kW per rack.

- As technology companies, AI service providers, and data center operators continue to advance artificial intelligence, high-density computing, and other next-generation digital technologies, the demand for high-density racks, AI-optimized data centers, and GPU-ready infrastructure is projected to rise further over the forecast period, leading to a rise in demand for advanced and energy-efficient cooling technologies in the U.S. data center industry.

Increasing Sustainability Measures among Hyperscale and Cloud Providers

- Hyperscale and cloud service providers across the U.S. are increasing their focus on sustainability as growing demand for processing artificial intelligence and high-performance Computing workloads, cloud computing, and digital infrastructure is increasing the need for higher electricity and energy-efficient cooling technologies across large-scale data center facilities.

- In May 2025, Meta entered into two Environmental Attribute Purchase Agreements (EAPAs) with Sunraycer Renewables to secure renewable solar energy from Sunraycer Renewables' Midpoint Solar and Gaia Solar projects in Navarro County, Texas, to power Meta's data center operations across the U.S.

- As the demand for artificial intelligence, cloud computing, and high-performance computing continues to grow, hyperscale and cloud providers are expected to accelerate their sustainability efforts to enhance operational efficiency, reduce carbon emissions, and develop environmentally sustainable data center infrastructure across the country.

The Surge in Adoption of Sustainability Practices by Colocation and Enterprise Data Center Operators

- Colocation and enterprise data center operators across the U.S. are increasingly investing in adopting sustainability initiatives, including the use of renewable energy, deployment of energy-efficient cooling systems, water conservation measures, and adoption of sustainable support infrastructure such as HVO-powered generators and lithium-ion batteries, to reduce environmental impact, improve operational efficiency, and support the long-term sustainable digital infrastructure growth.

- In January 2026, CyrusOne entered into a partnership with Eolian, the renewable energy firm, to procure renewable energy for powering CyrusOne's DFW7 data center campus in Fort Worth, Texas, supporting the company's sustainability goals.

- As demand for AI, cloud computing, and digital services continues to grow across the U.S., colocation and enterprise data center operators are expected to further strengthen their sustainability practices to reduce carbon emissions across their data centers.

Government Policies and Incentives Supporting Green Data Center Infrastructure Development

- Government policies, environmental regulations, clean energy initiatives, tax incentives, and sustainability programs across the U.S. are supporting data center operators to enhance energy efficiency, lower carbon emissions, adopt sustainable practices to operate data centers, and invest in the development of environmentally friendly digital infrastructure across the country.

- The U.S. Securities and Exchange Commission (SEC) Climate Disclosure Rules require publicly listed companies, including data center operators such as Equinix, Digital Realty, Iron Mountain, and CyrusOne, to report climate-related risks, energy usage, greenhouse gas emissions, sustainability initiatives, and ESG governance practices the companies are adopting to enhance transparency regarding environmental risks associated with data center operations.

- As federal and state governments across the U.S. continue to strengthen sustainability regulations and expand clean energy incentive programs, data center operators are expected to invest in adopting renewable energy, energy-efficient cooling solutions, and low-carbon infrastructure equipment to support sustainable data center operations during the forecast period.

Increasing Electricity and Data Center Construction Prices Pushing Data Center Operators Toward Sustainability

- The rising electricity prices, data center construction costs, and demand for AI-optimized data center infrastructure across the U.S. are increasing financial pressure on data center operators across the country, requiring the firms to adopt sustainable and cost-effective strategies to optimize power usage and improve operational efficiency in data centers.

- To minimize long-term electricity expenses, data center firms are prioritizing the development of on-site substations and battery storage systems, which help the companies to reduce reliance on utilities to source electricity for data center operations. For example, in March 2026, Core Scientific announced plans to develop a new data center campus in Hunt County, Texas, that will include the development of an on-site substation to support the facility's operations.

- Data center operators are increasingly sourcing direct funds from investment firms to accelerate the development of large-scale, renewable energy-powered data center infrastructure in the U.S. For instance, in October 2025, Oracle planned to secure approximately $38 billion in debt financing to support data center developments in Texas and Wisconsin.

U.S. SUSTAINABLE DATA CENTER MARKET GEOGRAPHICAL ANALYSIS

- In the Southeastern US, states such as Virginia, North Carolina, South Carolina, Georgia, and Florida have emerged as key hubs for data center development, attracting significant investment from hyperscale, colocation, and enterprise operators. The region accounted for around 30.87% of the U.S. sustainable data center market's data center investments in 2025.

- In Virginia, the adoption of sustainable practices among data centers is gaining momentum as operators are increasingly investing in renewable energy sources, advanced liquid cooling technologies, and smart grid solutions to reduce dependence on conventional power infrastructure. Additionally, the Virginia Clean Economy Act is supporting this transition by encouraging data center operators to lower greenhouse gas emissions and enhance environmental sustainability.

- Georgia is continuing to strengthen its position as one of the sustainable data center markets, supported by utility providers such as Georgia Power, which introduce renewable energy procurement initiatives such as the Clean and Renewable Energy Subscription (CARES) program, allowing hyperscale operators to access electricity from dedicated clean energy projects and increase the use of renewable energy for their data center operations.

- In the Midwestern U.S., states such as Ohio, Illinois, and Indiana have established themselves as major data center markets, while emerging locations including Michigan, Missouri, Minnesota, Kansas, and Nebraska are expected to attract increasing data center investments during the upcoming years.

- In Minnesota, the development of sustainable data center infrastructure is gaining momentum, supported by the state's goal to achieve 100% carbon-free electricity by 2040. To meet growing demand for AI-ready data center infrastructure while advancing sustainability, data center operators are increasingly collaborating with utilities such as Xcel Energy to secure large-scale renewable energy for their data center operations.

- The Southwestern US comprises Texas, Arizona, New Mexico, and Oklahoma, and the region is emerging as a prominent data center hub. Texas and Arizona account for the majority of investments in the region, and it continues to attract substantial data center development due to the rapid surge in digital transformation, expanding cloud and AI demand, and the availability of robust power infrastructure.

- In Arizona, companies can benefit from various incentives that support sustainable digital infrastructure development, including sales tax exemptions on solar and wind energy equipment, favorable property tax treatment for on-site renewable energy installations, and incentives for incorporating energy-efficient building technologies. The state also provides tax credits to encourage investments in clean electricity generation.

- The Western US includes Hawaii, Alaska, Oregon, Wyoming, California, Utah, Colorado, Montana, Nevada, Idaho, and Washington, among others. It is one of the most sustainability-focused regions in the country. In the Western US, Oregon, California, Utah, Washington, and Nevada have emerged as some of the leading data center markets, attracting significant data center investments.

- In California, data center developers must comply with the California Environmental Quality Act (CEQA), which requires the companies to undergo environmental assessments before large-scale projects can obtain regulatory approval. Additionally, the 100% Clean Energy Law (SB 100) established a target for the state's electricity supply to be entirely generated from carbon-free energy sources by 2045.

- The Northeastern U.S. comprises Connecticut, Delaware, Maine, Maryland, Massachusetts, New Hampshire, New Jersey, New York, Pennsylvania, Rhode Island, and Vermont. The region is witnessing growing demand for sustainable data center infrastructure, driven by ambitious climate policies. Therefore, data center operators across the region are increasingly focusing on improving sustainability, enhancing energy efficiency, and reducing both power and water consumption within their facilities.

U.S. SUSTAINABLE DATA CENTER MARKET VENDOR LANDSCAPE

- Leading hyperscalers and cloud service providers such as Amazon Web Services (AWS), Microsoft, Google, Meta, Apple, and Oracle are strengthening their renewable energy strategies through long-term power purchase agreements (PPAs) with clean energy suppliers, investing in dedicated renewable energy infrastructure, and developing on-site renewable energy substations to increase the use of carbon-free electricity for data center operations.

- Major hyperscale companies have established ambitious sustainability goals, with Apple, Google, and Meta targeting net-zero carbon emissions by 2030, while Amazon Web Services (AWS) is working toward net-zero emissions by 2040, and Oracle has set a goal to achieve net-zero greenhouse gas emissions by 2050. Microsoft is committed to achieving a carbon-negative target by 2030.

- Colocation service providers such as Equinix, Digital Realty, Vantage Data Centers, STACK Infrastructure, Applied Digital, CyrusOne, EdgeConneX, Flexential, H5 Data Centers, Iron Mountain, NTT DATA, Prime Data Centers, QTS Data Centers, and Sabey Data Centers are advancing sustainability initiatives to strengthen their position by deploying energy-efficient power and cooling systems, increasing the use of renewable energy, improving Power Usage Effectiveness and Water Usage Effectiveness metrics, adopting modular construction practices, and reducing electricity and water consumption to minimize the environmental impact and carbon footprint.

- Prime Data Centers is designing its new facilities to achieve a low Power Usage Effectiveness of approximately 1.33. Additionally, colocation providers such as NTT DATA, Iron Mountain, EdgeConneX, Cologix, and others are accelerating sustainability initiatives and pursuing net-zero carbon emission goals across their data center operations by 2030.

- Major renewable energy providers such as NextEra Energy, Enel Group, ENGIE, and TotalEnergies are playing a key role in supporting data center sustainability by supplying utility-scale renewable and low-carbon energy to data center operators through long-term power purchase agreements that help operators to achieve their decarbonization goals.

- Energy companies such as Algonquin Power & Utilities, AES Corporation, Apex Clean Energy, Avangrid, Brookfield Renewable, Constellation, Dominion Energy, EDF Power Solutions, and Enel Group are utilizing a diverse portfolio of energy resources, including solar, wind, hydropower, nuclear, geothermal, and natural gas to deliver a reliable, and scalable energy supply that supports the growing energy requirements of large-scale data center campuses across the U.S.

- Traditional oil and gas companies such as Chevron and Shell are increasingly expanding their presence in the renewable energy market through investments in clean power generation projects to support sustainable digital infrastructure across the U.S.

SNAPSHOT

The U.S. sustainable data center market size by investment will reach USD 116.43 billion by 2031, growing at a CAGR of 11.85% from 2025 to 2031.

The following factors are likely to contribute to the growth of the U.S. sustainable data center market during the forecast period:

- Increasing Sustainability Measures among Hyperscale and Cloud Providers

- The Surge in Adoption of Sustainability Practices by Colocation and Enterprise Data Center Operators

- Government Policies and Incentives Supporting Green Data Center Infrastructure Development

- Increasing Electricity & Data Center Construction Prices Pushing Data Center Operators Toward Sustainability

Base Year: 2025

Forecast Year: 2026-2031

The study considers the present scenario of the U.S. sustainable data center market and its market dynamics for 2026−2031. It covers a detailed overview of several market growth enablers, restraints, and trends. The report offers both the demand and supply aspects of the industry. It profiles and examines leading companies and other prominent ones operating in the industry.

Data Center Investors

- Aligned Data Centers

- Amazon Web Services

- American Tower

- Apple

- Applied Digital

- Centersquare

- CloudHQ

- Cologix

- Compass Datacenters

- COPT Data Center Solutions

- Crusoe

- CyrusOne

- DartPoints

- DataBank

- DC BLOX

- DigiPower X

- Digital Realty

- EdgeConneX

- EdgeCore Digital Infrastructure

- Element Critical

- Equinix

- fifteenfortyseven Critical Systems Realty

- Flexential

- H5 Data Centers

- HostDime

- Hut 8

- Iron Mountain

- Meta

- Microsoft

- Nautilus Data Technologies

- Netrality Data Centers

- Novva Data Centers

- NTT DATA

- Oracle

- PowerHouse Data Centers

- Prime Data Centers

- QTS Data Centers

- Sabey Data Centers

- Serverfarm

- Skybox Datacenters

- Soluna

- STACK Infrastructure

- Stream Data Centers

- Switch

- T5 Data Centers

- TierPoint

- Vantage Data Centers

- WhiteFiber

- Yondr Group

Renewable Energy Providers

- Adapture Renewables

- Algonquin Power & Utilities

- The AES Corporation

- Apex Clean Energy

- Avangrid

- Brookfield Renewable

- Chevron

- Constellation

- D. E. Shaw Renewable Investments (DESRI)

- Dominion Energy

- ECL

- EDF Power Solutions

- EDP Renewables

- Enbridge

- Enel Group

- ENGIE

- Eolian

- Fervo Energy

- First Solar

- Invenergy

- Leeward Renewable Energy

- Lightsource bp

- NextEra Energy

- NV Energy

- Oklo

- Ørsted

- Overview Energy

- PacifiCorp

- Pattern Energy

- Qcells

- Shell

- Solar Alliance

- TerraPower

- Torch Clean Energy

- TotalEnergies

- Vitol

- Xcel Energy

- XGS Energy

- Sunraycer

- Current Hydro

- Origis Energy

- Treaty Oak Clean Energy

- EnergyRe

- Entergy

- Zelestra

Segmentation by Infrastructure

- Electrical Infrastructure

- Mechanical Infrastructure

- General Construction

Segmentation by Geography

- United States

- Southeastern U.S.

- Midwestern U.S.

- Southwestern U.S.

- Western U.S.

- Northeastern U.S.

U.S. SUSTAINABLE DATA CENTER MARKET FAQs

How big is the U.S. sustainable data center market?

What is the growth rate of the U.S. sustainable data center market?

How much MW of power capacity is expected to reach the U.S. sustainable data center market by 2031?

What are the key trends in the United States sustainable data center market?

How much MW of power capacity is expected to reach the U.S. sustainable data center market by 2031?

For more details, please reach us at [email protected]

For more details, please reach us at [email protected]

Select a license type that suits your business needs

Single User Licence

- Report accessible by one user only

- Free 10% or 3 days of customization

- Free post-sale service assistance

- Continuous support through email

5 User Licence

- Report accessible by 5 users within the organization

- Free 15% or 4.5 days of customization

- Continuous support through email and telephone

- Free analyst hour

- Free Upgrade: If an updated report published within 180 days of purchase, you will get the revised report free of charge

Corporate Licence

- Free Datasheet worth $1500

- Report accessible by the entire organization

- Free 20% or 6 days of customization

- Free post-sale service assistance

- Continuous support through email and telephone

- Direct access to lead analysts

- Free analyst hour

- Free Upgrade: If an updated report published within 180 days of purchase, you will get the revised report free of charge

Datasheet Licence

- Report accessible by 1 user only

- Free 15% or 32 hours of customization

- Free post-sale service assistance

- Direct access to lead analysts

Frequently Asked Questions

How big is the U.S. sustainable data center market?

What is the growth rate of the U.S. sustainable data center market?

How much MW of power capacity is expected to reach the U.S. sustainable data center market by 2031?

What are the key trends in the United States sustainable data center market?

How much MW of power capacity is expected to reach the U.S. sustainable data center market by 2031?

Other RELATED Reports

Europe Sustainable Data Center Market - Industry Outlook & Forecast 2024-2029

Published : October 2024

APAC Sustainable Data Center Market - Industry Outlook & Forecast 2024-2029

Published : October 2024