Global Data Center Market Landscape 2026-2031

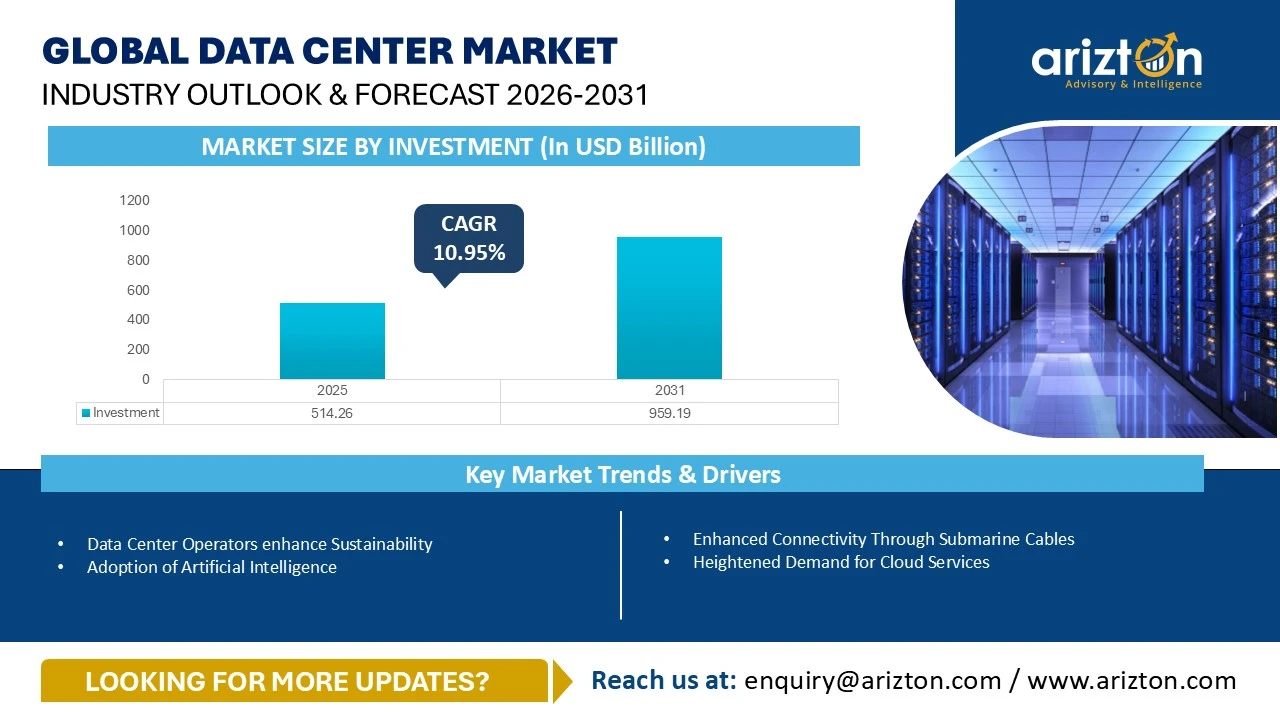

THE DATA CENTER MARKET SIZE WITNESSED INVESTMENTS OF USD 514.26 BILLION IN 2025 AND WILL WITNESS INVESTMENTS OF USD 959.19 BILLION BY 2031, GROWING AT A CAGR OF 10.95% DURING THE FORECAST PERIOD

960 pages

384 company

10 segments

9 region

54 countries

Purchase Options

Global Data Center Market Landscape 2026-2031

THE DATA CENTER MARKET SIZE WITNESSED INVESTMENTS OF USD 514.26 BILLION IN 2025 AND WILL WITNESS INVESTMENTS OF USD 959.19 BILLION BY 2031, GROWING AT A CAGR OF 10.95% DURING THE FORECAST PERIOD

The Global Data Center Market Size, Share, & Trends Analysis By

- Facility Type: Hyperscale Data Centers, Colocation Data Centers, and Enterprise Data Centers

- Infrastructure: IT Infrastructure, Electrical Infrastructure, Mechanical Infrastructure, and General Construction

- IT Infrastructure: Server Infrastructure, Storage Infrastructure, and Network Infrastructure

- Electrical Infrastructure: UPS Systems, Generators, Transfer Switches & Switchgear, PDUs, and Other Electrical Infrastructure

- Mechanical Infrastructure: Cooling Systems, Racks, and Other Mechanical Infrastructure

- Cooling Systems: CRAC & CRAH Units, Chiller Units, Cooling Towers, Condensers, Dry Coolers, and Other Cooling Units

- Cooling Techniques: Air-based and Liquid-based

- General Construction: Core & Shell Development, Installation & Commissioning Services, Engineering & Building Design, Physical Security, Fire Detection & Suppression, and DCIM

- Tier Standard: Tier I & II, Tier III, and Tier IV

- Geography: North America, Latin America, Western Europe, Nordic, Central & Eastern Europe, Middle East, Africa, APAC, and Southeast Asia

Industry Analysis Report, Regional Outlook, Growth Potential, Price Trends, Competitive Market Share & Forecast 2026–2031.

This report includes market data points, ranging from trend

analyses to market estimates & forecasts that you can customize

GLOBAL DATA CENTER MARKET REPORT SCOPE

| REPORT ATTRIBUTE | DETAILS |

|---|---|

| MARKET SIZE – INVESTMENT (2031) | USD 959.19 Billion |

| MARKET SIZE – INVESTMENT (2025) | USD 514.26 Billion |

| CAGR - INVESTMENT (2025-2031) | 10.95% |

| MARKET SIZE - AREA (2031) | 109.61 Million Square feet |

| POWER CAPACITY (2031) | 28,307 MW |

| HISTORIC YEAR | 2022-2024 |

| BASE YEAR | 2025 |

| FORECAST YEAR | 2026-2031 |

| SEGMENTS BY | Facility Type, Infrastructure, IT Infrastructure, Electrical Infrastructure, Mechanical Infrastructure, Cooling Systems, Cooling Techniques, General Construction, Tier Standard, and Geography |

| LARGEST REGION (BY INVESTMENT) | North America |

| GEOGRAPHIC ANALYSIS | North America, Latin America, Western Europe, Nordic, Central & Eastern Europe, Middle East, Africa, APAC, and Southeast Asia |

DATA CENTER MARKET SIZE & SHARE

The global data center market size was valued at USD 514.26 billion in 2025 and is expected to reach USD 959.19 billion by 2031, growing at a CAGR of 10.95% during the forecast period.

The data center market experienced investments of over $514.26 billion in 2025, which grew by around 35.22% in comparison to 2024. This is primarily driven by an increase in deployment of AI workloads across data centers worldwide, triggered by billions of dollars in yearly investments from hyperscale operators such as Amazon Web Services (AWS), Apple, Google, Meta (Facebook), and Microsoft.

Large-scale AI infrastructure initiatives are increasingly driving global data center expansion. Large-scale AI infrastructure initiatives are increasingly driving global data center expansion. A notable example is the Stargate Project, unveiled in January 2025 at the White House by OpenAI, SoftBank Group, Oracle, and MGX. The initiative aims to develop next-generation AI-ready data center infrastructure across the US, with plans to invest up to $500 billion over four years. An initial $100 billion has been committed for immediate deployment toward data centers and supporting infrastructure.

The data center market in Latin America is projected to attract a cumulative investment of $31.00 billion, excluding IT infrastructure, between 2026 and 2031. This growth is primarily driven by Brazil, Chile, Mexico, and other countries emerging as promising investment destinations.

Geopolitical conflicts and regional instability may lead to delays in data center construction due to supply chain disruptions, material shortages, and labor constraints. At the same time, the need for resilient and localized digital infrastructure is expected to drive higher investments in data centers across relatively stable markets in the region.

The UK and Germany are among the biggest data center markets in Europe, accounting for around 19.59% and 13.74% of the European data center market’s investments, respectively, in 2025; these countries continue to witness data center investments from local as well as global data center operators. By 2031, the UK and Germany are expected to contribute around 21.59% and 14.72% of the European data center market's investment share.

In 2025, the APAC data center market by investments increased by around 31.99%, compared to 2024. The rapid adoption of AI in China is becoming one of the key factors driving data center investments, as AI applications require massive, advanced data center facilities to process and store AI workloads. As of June 2025, approximately 515 million Chinese individuals have adopted AI for their daily operations; this count is expected to further increase in the upcoming years. China aims to increase the share of AI adoption to approximately 70% of the Chinese population by 2027, and to over 90% by 2030.

Data Center Market By Area - 109.61 Million Sq. Ft. (2031)

Data Center Market By Power Capacity - 28,307 MW (2031)

DATA CENTER MARKET KEY TRENDS

Data Center Operators Enhance Sustainability

- The adoption of renewable energy is on the rise across the globe, and it will continue to grow. Data centers are responsible for most of the global electricity consumption, and they have a significant impact on the environment. To reduce their environmental impact, data center operators are powering their facilities with renewable and green energy.

- Latin America is strengthening its position as a sustainable data center hub through renewable energy expansion and policy support. Countries such as Argentina, Chile, Colombia, and Mexico have established ambitious clean energy targets, creating favorable conditions for hyperscale deployments. For example, Argentina's proposed OpenAI–Sur Energy Stargate project links AI infrastructure deployment with dedicated renewable energy supply, while Colombia released over 5GW of grid connection capacity in 2025 to accelerate new solar and wind projects that can support future data center demand.

- In the US, operators are increasingly securing long-term renewable energy supplies to support growing capacity requirements. Examples include TotalEnergies' 15-year agreement to provide Google with 1.5 TWh of solar energy from Ohio, Meta's 385 MW solar PPA in Louisiana that increased its 2025 solar procurement beyond 3 GW, and Digital Realty securing 1.5 GW of renewable energy capacity while achieving 75% renewable electricity usage across its global operations.

- Several hyperscale and colocation operators in Denmark are actively integrating district heating solutions into their facilities. Companies such as Microsoft, Meta, Apple, atNorth, and Penta Infra continue to incorporate heat recovery into new and existing developments. These partnerships are often formed with local utilities. The approach aligns commercial operations with community energy needs.

Adoption of Artificial Intelligence

- Europe is undergoing rapid digital transformation driven by widespread enterprise adoption of AI, cloud, and data-driven technologies, significantly increasing demand for data center infrastructure. Countries such as Germany, the UK, and Italy show near-universal digital connectivity, with Germany reporting 93% of organizations prioritizing AI and digital technologies, the UK reaching 97.8% internet penetration with over 55 million social media users, and Italy achieving 90% internet penetration.

- In the US, operators are redesigning facilities to support GPU-intensive workloads, liquid cooling, and higher rack power densities. Examples include Meta's redesign of multiple US data center projects to accommodate AI infrastructure, NTT DATA's 2025 expansion adding over 370 MW of capacity and enabling more than 200 MW of AI workloads, and Lambda's AI Factory in Missouri, which will deploy more than 10,000 NVIDIA Blackwell Ultra GPUs for next-generation AI computing.

- South Africa is positioning itself as a regional AI hub, with Cassava Technologies planning an NVIDIA-powered AI factory and AI supercomputer deployment. The government has also allocated $28.4 million toward AI, blockchain, and digital capability research.

- The Nordics are emerging as a leading destination for sustainable AI infrastructure, combining renewable energy availability with large-scale AI-focused data center investments. For Instance, Verne and Nscale's 15 MW liquid-cooled NVIDIA GB300 AI deployment in Iceland is powered entirely by renewable energy.

DATA CENTER MARKET SEGMENTATION INSIGHTS

- In Europe, Sweden led the data center market in terms of hyperscale data center investments, accounting for around 38.38% of the market’s hyperscale data center investments, followed by the UK (23.41%), Spain (17.19%), the Netherlands (7.47%), and others. In addition, the UK is expected to lead the European data center market in 2031, in terms of hyperscale data center investments, contributing to generating around 21.31% of the market's hyperscale data center investments during the same period, followed by Germany (19.00%), Norway (14.23%), France (9.94%), and others.

- The need for generators in data centers is still high, despite generators being the major contributors to carbon emissions. Africa Data Centres’ Lagos facility maintains 48 hours of diesel backup at full load, supported through agreements with trusted fuel vendors to ensure uninterrupted availability.

- Hydrotreated Vegetable Oil (HVO) is projected to become the preferred low-carbon backup fuel in the next decade; however, it will primarily serve as a backup power solution rather than a primary power source. Companies like Vantage Data Centers, Compass Data Centers, and Digital Realty, along with other colocation providers, are working on developing larger supply chains for HVO.

- Additionally, several innovative UPS batteries, such as Nickel-Zinc (NiZn) and Sodium-Ion batteries, are gaining traction in the market due to their high-power density, safety, sustainability, and other factors. VRLA remains the largest installed battery base in enterprise and colocation data centers due to decades of deployment and lower capital costs. Many hyperscale operators now prefer lithium-ion batteries for new facilities because they reduce space requirements and replacement costs.

- The data center liquid cooling market primarily features two methods, which include Direct-to-Chip (DTC) cooling and Liquid Immersion Cooling. As per the early trends and data, DTC is the larger and more widely adopted method at present. In contrast, immersion cooling is experiencing rapid growth, albeit from a smaller starting point, primarily due to the demands of AI and high-performance computing (HPC) workloads.

- The 42U rack unit is the most used in data centers. Rack units of 45U, 47U, and 48U are mainly installed in large data center environments. A single data center can comprise racks of different sizes. The Riyadh data center facility in Saudi Arabia, operated by NourNet, has been installed with approximately 450 rack cabinets.

DATA CENTER MARKET - GLOBAL GEOGRAPHICAL ANALYSIS

- The Canadian government supports AI technology. In January 2025, the Canadian government announced a $52 million fund for quantum technology projects, which is estimated to support around 107 projects across the country.

- The UAE continues to rank among the most advanced data center markets in the Middle East, supported by accelerating digitalization, proactive government initiatives, high internet and social media penetration, extensive inland and submarine connectivity, as well as a well-defined regulatory framework.

- In August 2025, Colombia launched its own data center association – the Colombian Association of Data Centers and Data Technology (ACOLDC). This non-profit organization aims to strengthen the digital infrastructure of the country by promoting the development of data centers as strategic pillars of the digital economy. The ACOLDC connects leading data centers in the Colombian market with high-quality providers to position the country as a technological hub in the region and to enhance the economic growth of the sector.

- In 2025, the APAC data center colocation market by area was valued at 17.36 million sq ft and is expected to reach 23.80 million sq ft by 2031, growing at a CAGR of 5.39%. Singapore is one of the most expensive markets in the world for developing data center facilities. In addition, land availability for data center development is very limited. Operators continue to purchase industrial plots to convert into data centers; however, such activities remain relatively low in the market.

- As of November 2025, South Africa hosts around 11 operational submarine cables. In July 2025, NVIDIA announced the signing of a partnership deal with Cassava Technologies to build AI-ready data centers across African countries such as Egypt, Nigeria, Kenya, and Morocco, for a total investment of around $700 million.

- Egypt is expected to witness the entry of foreign data center companies as the demand for data center services is increasing gradually in the country. The foreign data center companies are collaborating with the local Egyptian companies to develop data centers in the country.

GLOBAL DATA CENTER VENDORS - LANDSCAPE

- The global data center market has the presence of key investors such as AirTrunk, Aligned Data Centers, Amazon Web Services (AWS), Apple, CDC Data Centres, CloudHQ, Compass Datacenters, CyrusOne, DataBank, Digital Realty, EdgeConneX, Equinix, Global Switch, Google, Iron Mountain, Meta, Microsoft, NTT DATA, QTS Realty Trust, STACK Infrastructure, ST Telemedia Global Data Centres (STT GDC), Switch, Vantage Data Centers and others.

- In February 2026, Google announced a $500 million investment to develop a new international digital exchange hub (“Digital Port”) in the Dominican Republic, marking its first such facility in Latin America outside the US. The project also includes new submarine cable connections to the US, significantly enhancing regional connectivity and positioning the country as a strategic digital gateway across the Americas.

- In November 2025, Microsoft partnered with Powertrust to support the deployment of 270MW of solar power across Brazil and Mexico, receiving Renewable Energy Certificates from the projects. The initiative aligns with the broader investment of Microsoft in Brazil’s cloud and AI infrastructure and its long-term clean energy procurement strategy.

- New entrants in the MEA region include Agility Logistics Parks, Anan, Cloudoon, DataVolt, Desert Dragon Data Centers, Ezditek, Humain, Kasi Cloud, Mega DC, MultiDC, NED, NEOIX, Pure Data Centres, Qareeb Data Centres, Techtonic, Volt and others.

- In February 2025, DataVolt announced its plans for the development of a new AI-ready data center facility in Riyadh, Saudi Arabia; the company has planned to develop a Neom data center, with an IT power capacity of around 1.5 GW, in Neom, Saudi Arabia.

- In March 2025, Open Access Data Centres announced its plan to invest around $240 million for the development of a new data center facility in Lagos. The data center will support 24 MW on completion and will be built in two stages. The first phase, with 12 MW, is likely to become operational by 2026.

SNAPSHOT

The global data center construction market size by investment will reach USD 959.19 billion by 2031, growing at a CAGR of 10.95% from 2025 to 2031.

The following factors are likely to contribute to the growth of the global data center construction market during the forecast period:

- Enhanced Connectivity Through Submarine Cables

- Heightened Demand for Cloud Services

Base Year: 2025

Forecast Year: 2026-2031

The study considers the present scenario of the global data center construction market and its market dynamics for 2026−2031. It covers a detailed overview of several market growth enablers, restraints, and trends. The report offers both the demand and supply aspects of the market. It profiles and examines leading companies and other prominent ones operating in the market.

The report includes the investment in the following areas:

Segmentation by Facility Type

- Hyperscale Data Centers

- Colocation Data Centers

- Enterprise Data Centers

Segmentation by Infrastructure

- IT Infrastructure

- Electrical Infrastructure

- Mechanical Infrastructure

- General Construction

Segmentation by IT Infrastructure

- Server Infrastructure

- Storage Infrastructure

- Network Infrastructure

Segmentation by Electrical Infrastructure

- UPS Systems

- Generators

- Transfer Switches & Switchgear

- PDUs

- Other Electrical Infrastructure

Segmentation by Mechanical Infrastructure

- Cooling Systems

- Racks

- Other Mechanical Infrastructure

Segmentation by Cooling Systems

- CRAC & CRAH Units

- Chiller Units

- Cooling Towers, Condensers, and Dry Coolers

- Other Cooling Units

Segmentation by Cooling Techniques

- Air-based

- Liquid-based

Segmentation by General Construction

- Core & Shell Development

- Installation & Commissioning Services

- Engineering & Building Design

- Physical Security

- Fire Detection & Suppression

- DCIM

Segmentation by Tier Standard

- Tier I & II

- Tier III

- Tier IV

Segmentation by Geography

- North America

- U.S.

- Canada

- Latin America

- Brazil

- Chile

- Mexico

- Colombia

- Argentina

- Rest of Latin America

- Western Europe

- U.K.

- Germany

- France

- Netherlands

- Ireland

- Switzerland

- Italy

- Spain

- Belgium

- Portugal

- Greece

- Other Western European Countries

- Nordics

- Denmark

- Sweden

- Norway

- Finland

- Iceland

- Central & Eastern Europe

- Russia

- Poland

- Austria

- Czechia

- Other Central & Eastern European Countries

- Middle East

- UAE

- Saudi Arabia

- Israel

- Qatar

- Kuwait

- Oman

- Bahrain

- Turkey

- Jordan

- Other Middle East Countries

- Africa

- South Africa

- Kenya

- Nigeria

- Egypt

- Other African Countries

- APAC

- China

- Hong Kong

- Australia

- New Zealand

- Japan

- India

- South Korea

- Taiwan

- Rest of APAC

- Southeast Asia

- Singapore

- Indonesia

- Malaysia

- Thailand

- Philippines

- Vietnam

- Other Southeast Asia Countries

Prominent Data Center IT Infrastructure Providers

- Arista Networks

- Atos

- Broadcom

- Cisco Systems

- Dell Technologies

- Extreme Networks

- Fujitsu

- Hewlett Packard Enterprise

- Hitachi

- Huawei Technologies

- IBM

- Inspur

- Intel

- Lenovo

- Micron Technology

- NetApp

- NVIDIA

- Oracle

- Everpure (Pure Storage)

- QNAP Systems

- Quanta Cloud Technology (QCT)

- Quantum

- Seagate

- Supermicro

- Western Digital

Prominent Data Center Support Infrastructure Providers

- 3M

- ABB

- Airedale

- Alfa Laval

- Caterpillar

- Carrier

- Cummins

- Cyber Power Systems

- Daikin Applied

- Delta Electronics

- Eaton

- HITEC Power Protection

- Honeywell

- Johnson Controls

- Legrand

- Mitsubishi Electric

- Rehlko

- Rittal

- Rolls-Royce

- Siemens

- Schneider Electric

- Stulz

- Vertiv

Other Prominent Data Center Support Infrastructure Providers

- Aggreko

- Aksa Power Generation

- Baudouin

- EMPATEL SAPEM

- Canovate

- Condair

- EAE Group

- ENGIE

- Envicool

- Generac Power Systems

- Green Revolution Cooling (GRC)

- KSTAR

- KyotoCooling

- Munters

- Narada

- Panduit

- Submer

- Systermair Group

- Piller Power Systems

- Socomec

- Toshiba

- Trane

Prominent Data Center Contractors

- AECOM

- Arup

- AtkinsRéalis

- Black & Veatch

- DPR Construction

- Fluor Corporation

- Future-tech

- Gensler

- H&MV Engineering

- HDR

- Hill International

- ISG

- Jacobs

- Laing O'Rourke

- Linesight

- M+W Group (Exyte)

- Mace

- McLaren Construction Group

- Mercury

- PQC

- RED Engineering Design

- Rider Levett Bucknall (RLB)

- Royal HaskoningDHV

- Salute Mission Critical

- Skanska

- STO Building Group

- Sudlows

- Syska Hennessy Group

- Tetra Tech

- The Weitz Company

- Turner Construction

- Turner & Townsend

- Corgan

- Fortis Construction

- Holder Construction

Other Prominent Data Center Contractors

- Aurecon

- Basler & Hofmann

- CapIngelec

- Collen Construction

- COWI

- Dornan

- DSCO Group

- Edarat Group

- EMCOR Group

- EYP MCF

- Gilbane Building Company

- HITT Contracting

- Hoffman Construction

- Hyundai Engineering & Construction

- John Paul Construction

- Kirby Group

- Larsen & Toubro

- Mortenson

- NTT Facilities

- Obayashi Corporation

- Quark

- Raghav Contracting

- Ramboll

- Rogers-O’Brien Construction

- Sterling and Wilson

- Sunway Construction Group

- Urbacon

- Winthrop Technologies

Key Data Center Investors

- AirTrunk

- Aligned Data Centers

- Amazon Web Services (AWS)

- Apple

- CDC Data Centres

- CloudHQ

- Compass Datacenters

- CyrusOne

- DataBank

- Digital Realty

- EdgeConneX

- Equinix

- GDS Holdings

- Global Switch

- Gulf Data Hub

- Iron Mountain

- Meta

- Microsoft

- NTT DATA

- QTS Realty Trust

- STACK Infrastructure

- ST Telemedia Global Data Centres (STT GDC)

- Switch

- Vantage Data Centers

Other Data Center Investors

- AdaniConneX

- Africa Data Centres

- American Tower

- Applied Digital

- AQ Compute

- AtlasEdge

- Atman

- atNorth

- Bulk Infrastructure

- CapitaLand

- center3

- China Mobile International

- China Telecom Corporation

- China Unicom

- Chindata Group

- Chunghwa Telecom

- Cirion Technologies

- Cologix

- Colt Data Centre Services

- Corescientific

- Crusoe

- Csqaure

- DAMAC Digital

- Data4

- DCI Indonesia

- Digital Edge DC

- Edgecore Digital Infrastructure

- Echelon Data Centres

- Elea Data Centers

- Empyrion Digital

- ePLDT

- eStruxture Data Centers

- Etix Everywhere

- Flexential

- Global Technical Realty

- Goodman

- GTD

- iXAfrica Data Centres

- Kao Data

- Keppel Data Centres

- Khazna Data Centers

- KIO Data Centers

- LCL Data Centers

- LG CNS

- LG Uplus

- maincubes SECURE DATACENTERS

- MedOne

- MEEZA

- NEXTDC

- NextStream

- NorthC

- Novva Data Centers

- Nxtra by Airtel

- OneAsia Network

- Open Access Data Centres

- Orange Business

- Penta Infra

- PowerHouse Data Centers

- Prime Data Centers

- Princeton Digital Group

- Pure Data Centres Group

- QScale

- Quantum Switch

- Racks Central

- Rostelecom

- Sabey Data Centers

- Scala Data Centers

- Serverfarm

- Sify Technologies

- Singtel (Nxera)

- Skybox Datacenters

- SUNeVision Holdings

- Tecto Data Centers

- Telehouse

- Urbacon Data Centre Solutions

- VIRTUS Data Centres

- WhiteFiber

- Yondr

New Entrants

- 3E Network Technology Company

- 1911 Data Centers

- 247 Data Centers

- Adriatic DC

- AmpTank & Greensky Energy

- Ada Infrastructure

- Agility Logistics Parks

- Anan

- Anglesey Land Holdings

- Apatura

- Apto

- Aqylon Nexus

- Arcem

- AREA Group of Companies

- Ardent Data Centers

- Art Data Centres

- Asia Pacific Land (APL)

- Aslan Energy Capital

- Atlantic Data Centers

- Aroundtown SA

- AVAIO Digital Partners

- Ava Telecom

- Azora

- Beacon AI Centers

- Beale Infrastructure

- Big Sky Digital Infrastructure

- Bilt Technology

- BW Digital

- Changhae Development

- Chinachem Group

- CleanArc Data Centers

- Cloudoon

- Compute Nordic

- Crane Data Centers

- CURRENC Group

- DARKNX

- Data Castle

- Data Center Partners

- Data District

- DATA for MED

- DataGrid New Zealand

- DataR GmbH

- DataVolt

- DC Connects

- Deep Green

- Desert Dragon Data Centers

- Digital Land & Development

- Digital Reef

- Doma Infrastructure Group

- Drax Group

- ECO-LocaXion

- EDC One

- Edora

- EID LLP

- Elite UK REIT

- Energia Group

- EngineNode

- Everstone Group

- Evolution Data Centres

- evroc

- FCDC Corp

- Fermaca Networks

- FF Ventures

- Fleet Data Centers

- FLOW Digital Infrastructure

- Form8tion Data Centers

- Fossefall

- FutureData

- GARBE Data Centers

- Gatineau Data Hub (GDH)

- GIGA-42

- Global Telecommunications

- GreenScale Data Centres

- GreenSquareDC

- Greystoke

- Haoyang Data

- Henox IT and Datacenters

- House of Data

- HUMAIN

- ICADE

- IGIS Asset Management

- Infracrowd Capital

- Inuverse

- IPTP Networks

- Kakao Corp

- Kasi Cloud

- Kennedy Wilson

- Keystone

- Keysource and Namsos DataSenter

- KOSCOM

- Lambda

- Layer 9 Data Centers

- Lehr Consultants International

- Liberum Navitas

- LightHouse Data Centers

- Latos Data Centres

- MARKHAM

- Megaspeed AI

- Metrobloks

- Mistral AI

- MyTelehaus

- NED

- NE Edge

- NEOIX

- NES DATA

- NETHITS IT SOLUTIONS

- Northtree Investment Management

- NXN Datacenters

- OKESTRO

- Otech

- Panattoni

- Penzance

- Polarise

- Polarnode

- Portland Trust

- Prometheus Hyperscale

- Related Digital

- Rowan Digital Infrastructure

- Scale42

- SC Zeus Data Centers

- SEAX Global

- SEGRO plc

- Sesterce

- SGC Energy

- Siagon Asset Management

- Sierra DC

- sineQN

- Skygard

- Supernode by Quinbrook Infrastructure Partners

- Surfix Data Center

- Techtonic

- Terranova

- Thylander

- TPG Angelo Gordon

- Tract

- Trifalga

- Tritax Group

- Valencia Digital Port Connect

- Valore Group

- VDR

- VITALI SPA Società Benefit

- VSDATA

- Wilton International

- WS Computing AS

- X5 Group

- XTX Markets

- ZDATA Group

- Zr Power Holdings

DATA CENTER MARKET FAQs

What is the growth rate of the global data center market?

How big is the global data center market?

What is the estimated market size in terms of area in the global data center market by 2031?

What are the key trends in the global data center market?

How much MW of power capacity is expected to reach the global data center market by 2031?

For more details, please reach us at [email protected]

For more details, please reach us at [email protected]

Select a license type that suits your business needs

Single User Licence

- Report accessible by one user only

- Free 10% or 3 days of customization

- Free post-sale service assistance

- Continuous support through email

5 User Licence

- Report accessible by 5 users within the organization

- Free 15% or 4.5 days of customization

- Continuous support through email and telephone

- Free analyst hour

- Free Upgrade: If an updated report published within 180 days of purchase, you will get the revised report free of charge

Corporate Licence

- Free Datasheet worth $1500

- Report accessible by the entire organization

- Free 20% or 6 days of customization

- Free post-sale service assistance

- Continuous support through email and telephone

- Direct access to lead analysts

- Free analyst hour

- Free Upgrade: If an updated report published within 180 days of purchase, you will get the revised report free of charge

Datasheet Licence

- Report accessible by 1 user only

- Free 15% or 32 hours of customization

- Free post-sale service assistance

- Direct access to lead analysts

Frequently Asked Questions

What is the growth rate of the global data center market?

How big is the global data center market?

What is the estimated market size in terms of area in the global data center market by 2031?

What are the key trends in the global data center market?

How much MW of power capacity is expected to reach the global data center market by 2031?