Middle East and Africa Data Center Construction Market – Industry Outlook & Forecast 2026-2031

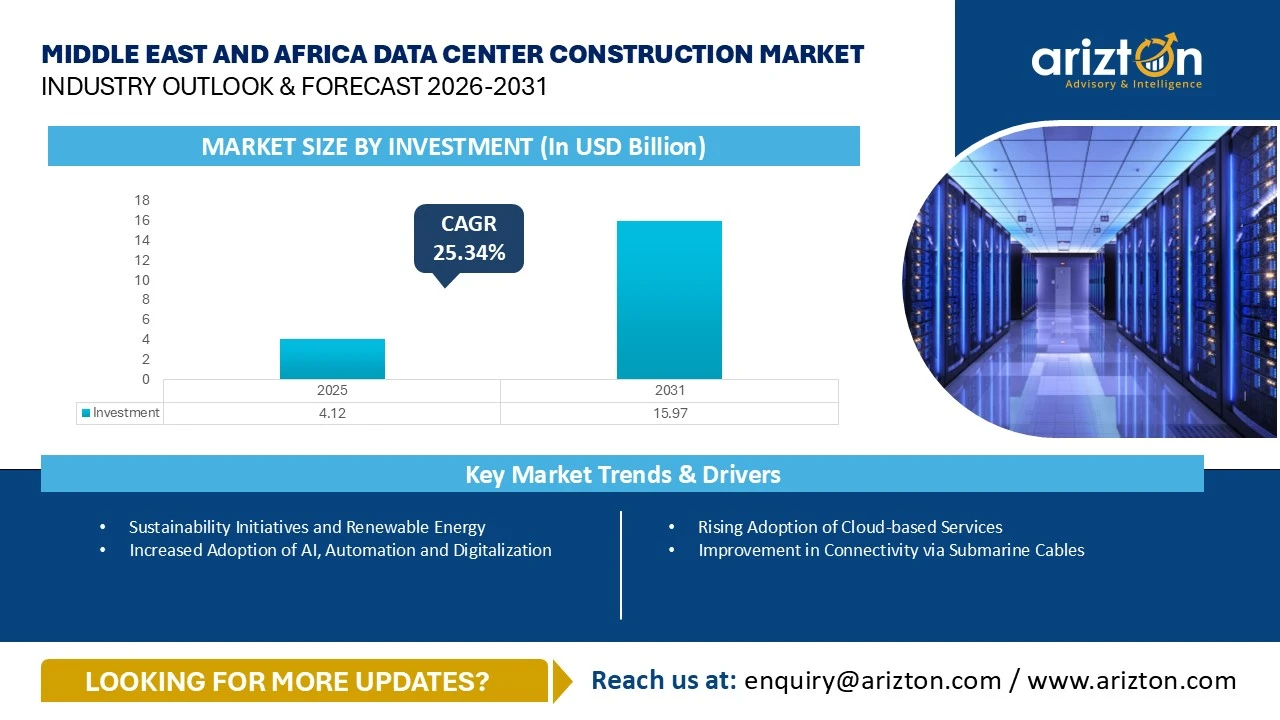

MIDDLE EAST AND AFRICA DATA CENTER CONSTRUCTION MARKET SIZE WAS VALUED AT USD 4.12 BILLION IN 2025 AND IS EXPECTED TO REACH USD 15.97 BILLION BY 2031, GROWING AT A CAGR OF 25.34% DURING 2025-2031.

328 pages

202 company

8 segments

2 region

14 countries

Purchase Options

Middle East and Africa Data Center Construction Market – Industry Outlook & Forecast 2026-2031

MIDDLE EAST AND AFRICA DATA CENTER CONSTRUCTION MARKET SIZE WAS VALUED AT USD 4.12 BILLION IN 2025 AND IS EXPECTED TO REACH USD 15.97 BILLION BY 2031, GROWING AT A CAGR OF 25.34% DURING 2025-2031.

The Middle East and Africa Data Center Construction Market Research Report Includes Size, Share, and Growth in Terms of

- Infrastructure: Electrical Infrastructure, Mechanical Infrastructure, and General Construction

- Electrical Infrastructure: UPS Systems, Generators, Transfer Switches & Switchgears, PDUs, and Other Electrical Infrastructure

- Mechanical Infrastructure: Cooling Systems, Racks, and Other Mechanical Infrastructure

- Cooling System: CRAC & CRAH Units, Chiller Units, Cooling Towers, Condensers, Dry Coolers, and Other Cooling Units

- Cooling Techniques: Air-based Cooling and Liquid-based Cooling

- General Construction: Core & Shell Development, Installation & Commissioning Services, Engineering & Building Design, Fire Detection & Suppression, Physical Security, and DCIM/BMS Solutions

- Tier Standards: Tier I & Tier II, Tier III, and Tier IV

- Geography: Middle East (UAE, Saudi Arabia, Israel, Qatar, Kuwait, Oman, Bahrain, Turkey, and Other Middle Eastern Countries) and Africa (South Africa, Kenya, Nigeria, Egypt, and Other African Countries)

Industry Analysis Report, Regional Outlook, Growth Potential, Price Trends, Competitive Market Share & Forecast 2026–2031.

This report includes market data points, ranging from trend

analyses to market estimates & forecasts that you can customize

MIDDLE EAST AND AFRICA DATA CENTER CONSTRUCTION MARKET REPORT SCOPE

| REPORT ATTRIBUTE | DETAILS |

|---|---|

| MARKET SIZE BY INVESTMENT (2031) | USD 15.97 Billion |

| MARKET SIZE BY INVESTMENT (2025) | USD 4.12 Billion |

| CAGR BY INVESTMENT (2025-2031) | 25.34% |

| MARKET SIZE - AREA (2031) | 4,975.5 thousand Sq. Ft. |

| POWER CAPACITY (2031) | 1,269 MW |

| HISTORIC YEAR | 2022-2024 |

| BASE YEAR | 2025 |

| FORECAST YEAR | 2026-2031 |

| MARKET SEGMENTS | Infrastructure, Electrical Infrastructure, Mechanical Infrastructure, Cooling Systems, Cooling Technique, General Construction, Tier Standards, and Geography |

| GEOGRAPHICAL ANALYSIS | Middle East (UAE, Saudi Arabia, Israel, Qatar, Kuwait, Oman, Bahrain, Turkey, and Other Middle Eastern Countries) and Africa (South Africa, Kenya, Nigeria, Egypt, and Other African Countries) |

MIDDLE EAST AND AFRICA DATA CENTER CONSTRUCTION MARKET SIZE

The Middle East and Africa data center construction market size was valued at USD 4.12 billion in 2025 and is expected to reach USD 15.97 billion by 2031, growing at a CAGR of 25.34% during the forecast period. The MEA data centre construction market is experiencing substantial growth in investment, area development, and power capacity, driven by rising cloud adoption, AI deployments, digital transformation initiatives, and government-backed digital economy programs. Countries across the Middle East and Africa are increasingly attracting investments from hyperscale cloud operators, colocation providers, telecom companies, and institutional investors.

The Middle East continues to account for the largest share of investments within the MEA region, led by Saudi Arabia and the UAE. These countries benefit from strong government support, large-scale digital transformation programs, smart city developments, and increasing hyperscale cloud investments.

MEA DATA CENTER CONSTRUCTION MARKET KEY TRENDS

Sustainability Initiatives and Renewable Energy

- Data centers in the MEA region are energy-intensive facilities, and sustainability has become an important focus as the region expands its digital infrastructure. Operators are increasingly exploring renewable energy sources such as solar, wind, and hydro power to reduce emissions and operational costs. Several Middle Eastern and African countries have strong renewable energy potential, creating opportunities to build greener, more energy-efficient data centres across the continent.

- In September 2025, Kenya launched a new clean energy policy aimed at achieving universal access to green power by 2030 and reaching net-zero carbon emissions by 2050.

- Data center companies in Oman are increasingly aligning their sustainability strategies with Oman Vision 2040 and the commitment of the country to achieve net-zero emissions by 2050. Operators such as Ooredoo Oman and DATAMOUNT continue to integrate energy efficiency measures, renewable energy adoption, and low-carbon infrastructure planning into their long-term roadmaps.

- In April 2025, the Egyptian government secured financing of approximately $3.5 billion to develop multiple wind and solar projects across the country to generate a wind energy of approximately 6.4 GW, and solar energy and around 5.6 GW in 2026 to increase the share of renewable sources in the nation's electricity mix.

- In February 2025, the South African government announced the decision to procure 4 GW and 10 GW of photovoltaic (PV) and wind energy, respectively, to meet the target of 9 GW of solar and 18 GW of wind capacity by 2030.

Increased Adoption of AI, Automation, and Digitalization

- The MEA region continues to accelerate its shift toward AI, automation, and digitization, supported by advances in cloud computing, data centers, and supercomputing capabilities for climate research. The region continues to leverage AI to enhance productivity across sectors, while prioritizing renewable energy and sustainable digital solutions.

- In August 2025, the Egyptian Ministry of Planning, Economic Development, and International Cooperation announced plans to invest approximately $255.6 million in the ICT sector of the country by the end of FY 2026 to accelerate digital transformation across Egypt, while positioning the country as one of the leading regional tech hubs in Africa.

- In January 2026, the UAE agreed to join the US-led Pax Silica initiative to build secure global semiconductor and technology supply chains spanning compute, connectivity, energy, and advanced manufacturing. The partnership is expected to strengthen the long-term AI and data center ecosystem resilience through international collaborations on critical infrastructure.

- In October 2025, Mega DC and Nebius launched their data center for processing AI in the Modi’in data center facility. It is the largest AI computing facility in Israel, 25% of which is likely to be allocated to the Israel Innovation Authority for the operation of the national supercomputer. The center, which provides AI processing using 8 MW of power, contains 4,000 NVIDIA graphics processors costing about $300 million.

- In February 2025, Resilience17 launched Go Time AI, the first AI accelerator in the country, providing startups with funding, compute resources, and mentorship to grow the AI innovation ecosystem in Nigeria.

- The South African government continues to invest in AI. For instance, in July 2025, South Africa’s Minister of Science, Technology, and Innovation announced the country’s investment of approximately $28.4 million in AI, blockchain, and other emerging technologies to strengthen foundational digital capabilities in the public sector. In addition, the fund supports the Foundational Digital Capabilities Research (FDCR) platform and the Centre for Artificial Intelligence Research (CAIR) across nine universities located in Cape Town, Pretoria, Stellenbosch, and Sol Plaatje University.

Rising Adoption of Cloud-based Services

- In March 2026, Atlancis Technologies and Everse Technology launched Servernah Cloud, Kenya’s first sovereign AI cloud platform, hosted at the iXAfrica Data Centres facility in Nairobi. The platform enables enterprises and government organizations to run AI workloads locally, supporting digital sovereignty and the expansion of AI infrastructure in Kenya.

- In January 2026, Tencent Cloud announced plans to expand its data center presence in the Middle East by increasing the number of availability zones for its cloud services. The company is actively exploring the development of new data centers in the region to better support local customers. Tencent Cloud currently operates a cloud region with two availability zones in Saudi Arabia and may also consider establishing an availability zone in Qatar.

- The Nigeria Cloud Computing Policy (NCCP), established by the National Information Technology Development Agency (NITDA), mandates government institutions to prioritize cloud-based solutions over traditional IT infrastructure. This policy aims to boost cloud adoption among Federal Public Institutions (FPIs) and Small and Medium Enterprises (SMEs), enhancing service delivery and stimulating economic growth.

- In October 2025, Vast Data partnered with Shonfeld Data Services (SDS) to build one of Israel’s most advanced sovereign AI cloud infrastructures for both local and international enterprises by using thousands of Nvidia Blackwell GPUs and dozens of petabytes of data storage.

- In September 2025, Oracle partnered with e& enterprise to launch a sovereign UAE OneCloud platform, powered by Oracle Alloy. The platform will deliver 200+ OCI services with full data residency to support government, regulated sectors, and enterprise AI adoption.

- In March 2025, Microsoft partnered with Core42 and the Abu Dhabi government to develop a sovereign cloud and AI infrastructure to support over 11 million daily digital interactions and enable fully AI-driven government services. The initiative aligns with Abu Dhabi’s $3.54 billion digital strategy to automate 100% of government processes and deploy more than 200 AI solutions.

- In January 2025, the Abu Dhabi government issued an RFQ for the ADGOV Cloud to consolidate digital infrastructure across more than 40 entities into a centralized hybrid multi-cloud environment integrating Microsoft Azure, Oracle Cloud Infrastructure, and AWS. The project will create a unified government data center and accelerate large-scale cloud migration while increasing the demand for skilled IT capabilities.

MEA DATA CENTER CONSTRUCTION MARKET SEGMENTAL ANALYSIS

- The Middle East & Africa data center construction market continues to witness strong growth in infrastructure investments, driven by increasing hyperscale developments, colocation expansion, and rapid digital transformation across major markets such as the UAE, Saudi Arabia, South Africa, Kenya, Nigeria, and Egypt.

- Electrical infrastructure continues to account for a significant share of investments in the Middle East & Africa data center construction market owing to the increasing deployment of high-density IT loads and rising demand for reliable and resilient power infrastructure. UPS systems, generators, switchgear, and power distribution solutions are expected to witness strong demand as operators focus on ensuring uninterrupted operations and addressing grid reliability requirements across several regional markets.

- Mechanical infrastructure investments are also witnessing strong growth with the increasing adoption of advanced cooling technologies and energy-efficient systems across hyperscale and colocation facilities. Cooling systems continue to dominate the segment as operators increasingly prioritize sustainability initiatives, lower energy consumption, and improved power usage effectiveness (PUE), particularly in warm-climate countries across the Middle East and Africa.

- General construction investments are expected to grow significantly across the Middle East & Africa data center market due to rising greenfield developments, hyperscale expansion projects, and increasing demand for purpose-built facilities. Growing investments in core & shell infrastructure, modular construction, and sustainable building designs continue to support market expansion across the region.

- The increasing adoption of cloud computing, artificial intelligence, big data analytics, IoT, fintech services, and digital government initiatives across the Middle East & Africa is accelerating demand for scalable and high-performance data center facilities. This is encouraging operators to invest in advanced electrical and mechanical infrastructure capable of supporting higher rack densities and improving operational efficiency.

- Major operators and investors, including global hyperscale cloud providers and regional colocation companies, are actively expanding their presence across the Middle East & Africa. Rising investments in submarine cable connectivity, renewable energy integration, smart city initiatives, and digital infrastructure development continue to support long-term growth across electrical, mechanical, and general construction segments throughout the region.

MEA DATA CENTER CONSTRUCTION MARKET GEOGRAPHICAL ANALYSIS

- Saudi Arabia is the largest investment market within MEA, growing at a CAGR of around 27% by 2031. The country is witnessing significant data center developments driven by Vision 2030 initiatives, cloud region launches, AI infrastructure deployments, and large-scale digital projects, including NEOM.

- The UAE remains one of the most mature data center markets in the region, with Dubai and Abu Dhabi continuing to attract investments from global cloud providers, colocation operators, and enterprise customers due to their strategic location, advanced connectivity infrastructure, and business-friendly environment.

- Dubai and Abu Dhabi are recognized as the leading smart city ecosystems, both regionally and globally. Their continued development is expected to drive the demand for edge and modular data centers to enable real-time data processing, while simultaneously supporting the need for a limited number of large core facilities.

- Turkey is emerging as a major regional digital infrastructure hub, with the country's strategic location between Europe, Asia, and the Middle East continuing to support data center expansion and connectivity investments.

- Across Africa, South Africa continues to dominate the market in terms of investment, area development, and power capacity, supported by strong colocation demand, extensive fiber connectivity, and increasing cloud adoption. The country remains the primary data center hub for the African continent.

- Nigeria, Kenya, and Egypt are among the fastest-growing African markets, supported by increasing enterprise digitalization, fintech growth, submarine cable connectivity, and rising cloud adoption. These countries are attracting investments from regional and international operators seeking to expand their footprint across Africa.

- Several emerging markets, including Qatar, Kuwait, Oman, Bahrain, Morocco, Ghana, Rwanda, Ethiopia, and Angola, are witnessing increasing investments in edge facilities, colocation developments, and telecom-based data center projects to support growing digital infrastructure requirements.

- In terms of area development, Saudi Arabia, the UAE, and South Africa account for a significant share of new white floor space additions across the MEA region. Large-scale hyperscale campuses and AI-ready facilities are increasingly driving the expansion of raised floor area across major metropolitan markets.

- In terms of power capacity, Saudi Arabia, the UAE, and South Africa continue to lead the region owing to large hyperscale deployments and colocation expansions. Significant capacity additions are also expected across Nigeria, Egypt, Kenya, Israel, and Turkey as operators scale infrastructure to meet growing cloud and AI workloads.

- The MEA region is increasingly benefiting from investments in renewable energy integration, particularly solar and wind projects across Saudi Arabia, the UAE, Egypt, South Africa, and Morocco. Governments across the region are implementing digital economy strategies, AI initiatives, smart city programs, and connectivity infrastructure projects that are expected to support long-term growth in the data center construction market.

MEA DATA CENTER CONSTRUCTION MARKET VENDOR LANDSCAPE

- Key support infrastructure vendors operating in the Middle East & Africa data center construction market include ABB, Aggreko, Airedale, Alfa Laval, Baudouin, Carrier, Caterpillar, Cummins, Delta Electronics, Eaton, Enrogen, Envicool, Evapco, GE Vernova, Hitachi Energy, Honeywell, Johnson Controls, Legrand, Mitsubishi Electric, nVent, Rittal, Rolls-Royce, Schneider Electric, Siemens, STULZ, Vertiv, and Toshiba Corporation. These vendors provide power, cooling, UPS systems, backup generators, switchgear, and rack infrastructure solutions required for large-scale data center operations across MEA.

- The market also has a strong presence of regional and global construction contractors, engineering firms, and consultants such as AECOM, ALDAR, ALEC Data Center Solutions, Arup, AtkinsRéalis, Dar Group, DC PRO Engineering, Future-tech, Gruppo ICM, and Hill International. These firms are actively involved in design, engineering, commissioning, and turnkey construction of hyperscale and colocation facilities across the region.

- Increasing investments in hyperscale and colocation infrastructure across the UAE, Saudi Arabia, Qatar, Oman, Israel, South Africa, Kenya, Nigeria, and Egypt are creating strong revenue opportunities for civil contractors, MEP service providers, and specialist subcontractors in the Middle East & Africa data center construction market. The continued development of digital infrastructure and smart city initiatives is further supporting demand for advanced construction capabilities.

- The market is witnessing investments from new and expanding regional data center operators such as Gulf Data Hub, Khazna Data Centers, GPX Global Systems, DataVolt, Mega Data Centers (MEGA DC), Moro Hub, N+One Datacenter, PAIX, Pure Data Centres, Rack Centre, Sahayeb Data Centers, Serverfarm, Telecom Egypt, and iXAfrica Data Centres. These companies are expanding capacity through hyperscale, AI-ready, and carrier-neutral facilities to address increasing enterprise and cloud demand across MEA.

- Major cloud and hyperscale operators such as Amazon Web Services, Google, Microsoft, Oracle, and Alibaba Group are increasing investments across the Middle East & Africa through cloud regions, AI infrastructure deployments, and colocation partnerships. Their expansion strategies, along with growing enterprise digitalization and rising data localization requirements, continue to drive large-scale data center construction activity throughout the region.

SNAPSHOT

The Middle East & Africa data center construction market size by investment will reach USD 15.97 billion by 2031, growing at a CAGR of 25.34% from 2025 to 2031.

The following factors are likely to contribute to the growth of the Middle East & Africa data center construction market during the forecast period:

- Rising Adoption of Cloud-based Services

- Improvement in Connectivity via Submarine Cables

Base Year: 2025

Forecast Year: 2026-2031

The study examines the current state of the Middle East & Africa data center construction market and its dynamics for 2026−2031. It covers a detailed overview of several market growth enablers, restraints, and trends. The report offers both the demand and supply aspects of the market. It profiles and examines leading companies and other prominent ones operating in the market.

The report includes the investment in the following areas:

- Infrastructure

- Electrical Infrastructure

- Mechanical Infrastructure

- General Construction

- Electrical Infrastructure

- UPS Systems

- Generators

- Transfer Switches & Switchgears

- PDUs

- Other Electrical Infrastructure

- Mechanical Infrastructure

- Cooling Systems

- Racks

- Other Mechanical Infrastructure

- Cooling System

- CRAC & CRAH Units

- Chillers Units

- Cooling Towers, Condensers, and Dry Coolers

- Other Cooling Units

- Cooling Techniques

- Air-based Cooling Technique

- Liquid-based Cooling Technique

- General Construction

- Core & Shell Development

- Installation & Commissioning Services

- Engineering & Building Design

- Fire Detection & Suppression

- Physical Security

- DCIM/BMS Solutions

- Tier Standards

- Tier I & Tier II

- Tier III

- Tier IV

- Geography

- Middle East

- UAE

- Saudi Arabia

- Israel

- Qatar

- Kuwait

- Oman

- Bahrain

- Turkey

- Other Middle Eastern Countries

- Africa

- South Africa

- Kenya

- Nigeria

- Egypt

- Other African Countries

Key Data Center Support Infrastructure Providers

- ABB

- Alfa Laval

- Baudouin

- Carrier

- Caterpillar

- Cummins

- Delta Electronics

- Eaton

- Envicool

- Evapco

- Honeywell

- Johnson Controls

- KSTAR

- Legrand

- nVent

- Piller Power Systems

- Rehlko (Kohler)

- Rittal

- Rolls-Royce

- Schneider Electric

- Siemens

- STULZ

- Trane

- Vertiv

Key Data Center Construction Contractors

- ABL Technical Services

- Absal Paul Contracting

- AECOM

- Arup

- Ashi & Bushnag

- Ashtrom Group

- ASU

- AtkinsRéalis

- ALDAR

- ALEC Data Center Solutions

- Auerbach HaLevy Architects

- Azura Consultancy

- B2 Architects

- Black & White Engineering

- BlueSun DC

- Capitoline

- Copy Cat Group

- Crovik Technologies

- Core Emirates

- Dar Group

- Datalec Precision Installations (DPI)

- DC PRO Engineering

- Deerns

- DMC Global Partners

- Eastra Solutions

- Edarat Group

- EDS Engineering

- Egypro

- Future-tech

- GREA

- Gruppo ICM

- H&MV Engineering

- HATCO

- HHM Group

- HubTech

- Hill International

- Ingenium

- ICS Nett

- Interkel Group

- ISF Group

- ISG

- JAMED

- James L Williams

- John Paul Construction

- Kent

- Laing O’Rourke

- Kinetic Controls

- Laith Electro Mechanical

- Linesight

- LYT Architecture

- M+W Group (Exyte)

- Mace

- MEC - Margolin Bros. Engineering & Consulting

- McLaren Construction Group

- MEMA Architecture

- Mercury

- Master Power Technologies

- MWK Engineering

- Norkun Intakes

- Orascom Construction PLC

- Prota Engineering

- PTS

- Qatar Site & Power

- Raghav Contracting

- Raya Network Services

- REDCON Construction Co. S.A.E

- Remax Consult

- Reno Design and Finish

- RED Engineering Design

- Rider Levett Bucknall

- Royal HaskoningDHV

- RW Armstrong

- Shaker Consultancy Group

- Sterling and Wilson

- Site & Power DK

- Skorka Architects

- Sudlows

- Summit Technology Solutions

- Telal Engineering & Contracting

- Tetra Tech

- Tri-Star Construction

- Turner & Townsend

- United For Technology Solutions

- WBHO Construction

- Westwood Management

- X2X Group

- Yeda Engineering

Data Center Investors

- 21st Century Technologies

- Adgar Investments & Development

- Africa Data Centres

- Alibaba Group

- Amazon Web Services

- Batelco

- Bezeq International

- Bynet Data Communications

- center3

- Cloud Acropolis

- COMnet Solutions

- Compass Datacenters

- Core42

- DAMAC Digital

- Datacenter Vaults

- DataCasa

- DATAMOUNT

- Digital Parks Africa

- Digital Realty

- du

- e& Egypt

- ECC Solutions

- EdgeConneX

- Equinix

- Global Technical Realty (GTR)

- G42

- GPX Global Systems

- Gulf Data Hub

- iXAfrica Data Centres

- Khazna Data Centers

- Mannai Corporation

- MedOne

- MEEZA

- Mega Data Centers (MEGA DC)

- Microsoft

- Mobily

- Moro Hub

- MTN

- N+One Datacenter

- NGN

- Nxtra by Airtel

- Oman Data Park

- Ooredoo

- Open Access Data Centres

- Oracle

- Orange Business (Etix Everywhere)

- Pacific Controls

- PAIX Data Centres

- Paratus Namibia

- PenDC

- Pure Data Centres

- Quantum Switch

- Rack Centre

- Radore

- Raya Data Center

- SDS Data Center

- Sadece Hosting

- Safaricom

- Sahayeb Data Centers

- Serverfarm

- Serverz Data Center

- Sparkle

- Syntys

- Telecom Egypt

- Telehouse

- Telkom Kenya

- Tencent Cloud

- TONOMUS

- Türk Telekom

- Turkcell

- Vantage Data Centers

- Vodafone

- XDS DATACENTERS

New Entrants

- Agility Logistics Parks

- Anan

- Blue Owl Capital

- Cloudoon

- DataVolt

- Desert Dragon Data Centers

- ezditek

- HUMAIN

- Kasi Cloud

- Keystone

- MultiDC

- NED

- NEOIX

- Otech

- Techtonic

- Volt

MIDDLE EAST AND AFRICA DATA CENTER CONSTRUCTION MARKET FAQs

How big is the Middle East & Africa data center construction market?

What is the estimated market size in terms of area in the Middle East & Africa data center construction market by 2031?

What is the growth rate of the Middle East & Africa data center construction market?

What are the key trends in the Middle East & Africa data center construction market?

How much MW of power capacity is expected to reach the Middle East & Africa data center construction market by 2031?

For more details, please reach us at [email protected]

For more details, please reach us at [email protected]

Select a license type that suits your business needs

Single User Licence

- Report accessible by one user only

- Free 10% or 3 days of customization

- Free post-sale service assistance

- Continuous support through email

5 User Licence

- Report accessible by 5 users within the organization

- Free 15% or 4.5 days of customization

- Continuous support through email and telephone

- Free analyst hour

- Free Upgrade: If an updated report published within 180 days of purchase, you will get the revised report free of charge

Corporate Licence

- Free Datasheet worth $1500

- Report accessible by the entire organization

- Free 20% or 6 days of customization

- Free post-sale service assistance

- Continuous support through email and telephone

- Direct access to lead analysts

- Free analyst hour

- Free Upgrade: If an updated report published within 180 days of purchase, you will get the revised report free of charge

Datasheet Licence

- Report accessible by 1 user only

- Free 15% or 32 hours of customization

- Free post-sale service assistance

- Direct access to lead analysts

Frequently Asked Questions

How big is the Middle East & Africa data center construction market?

What is the estimated market size in terms of area in the Middle East & Africa data center construction market by 2031?

What is the growth rate of the Middle East & Africa data center construction market?

What are the key trends in the Middle East & Africa data center construction market?

How much MW of power capacity is expected to reach the Middle East & Africa data center construction market by 2031?

Other RELATED Reports

Middle East Data Center Construction Market – Industry Outlook & Forecast 2026-2031

Published : June 2026

Africa Data Center Construction Market – Industry Outlook & Forecast 2026-2031

Published : May 2026