Middle East Data Center Market Landscape 2026-2031

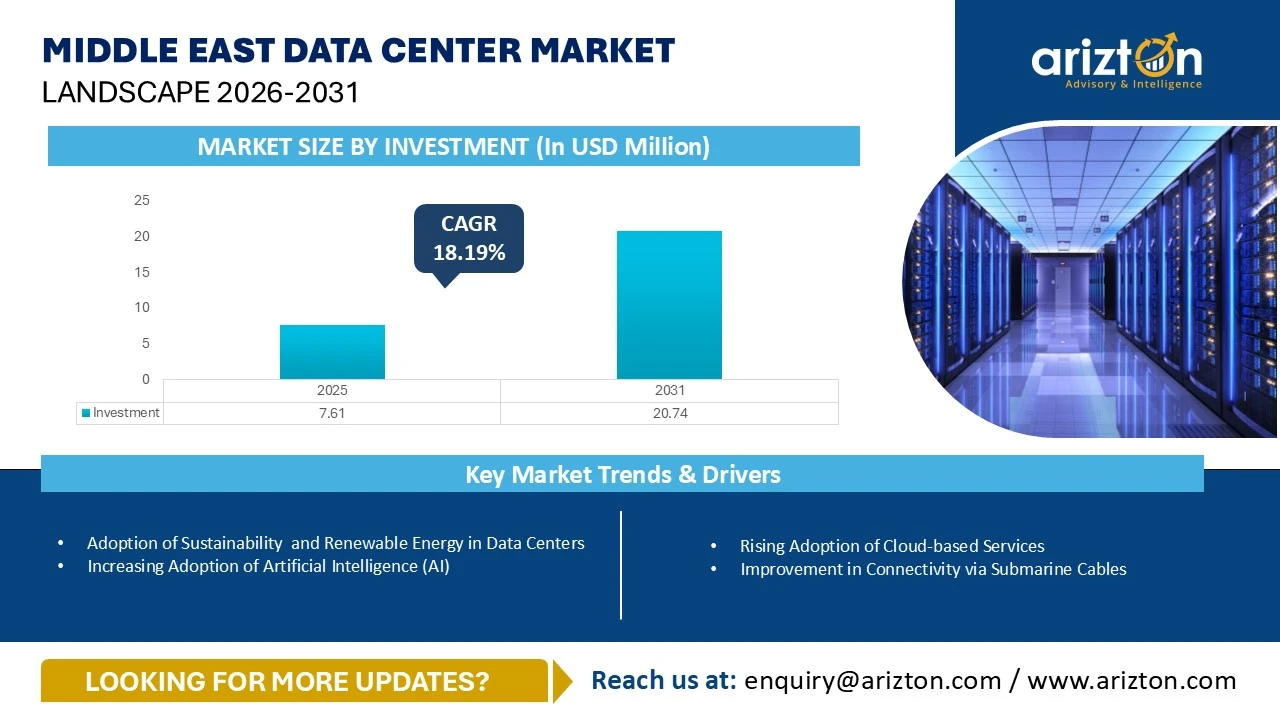

THE MIDDLE EAST DATA CENTER MARKET SIZE WITNESSED INVESTMENTS OF USD 7.61 BILLION IN 2025 AND WILL WITNESS INVESTMENTS OF USD 20.74 BILLION BY 2031, GROWING AT A CAGR OF 18.19% DURING THE FORECAST PERIOD

244 pages

region

countries

136 company

9 segments

Purchase Options

Middle East Data Center Market Landscape 2026-2031

THE MIDDLE EAST DATA CENTER MARKET SIZE WITNESSED INVESTMENTS OF USD 7.61 BILLION IN 2025 AND WILL WITNESS INVESTMENTS OF USD 20.74 BILLION BY 2031, GROWING AT A CAGR OF 18.19% DURING THE FORECAST PERIOD

The Middle East Data Center Market Size, Share, & Trends Analysis By

- Infrastructure: IT Infrastructure, Electrical Infrastructure, Mechanical Infrastructure, and General Construction

- IT Infrastructure: Server Infrastructure, Storage Infrastructure, and Network Infrastructure

- Electrical Infrastructure: UPS Systems, Generators, Transfer Switches & Switchgear, PDUs, and Other Electrical Infrastructure

- Mechanical Infrastructure: Cooling Systems, Racks, and Other Mechanical Infrastructure

- Cooling Systems: CRAC & CRAH Units, Chiller Units, Cooling Towers, Condensers, Dry Coolers, and Other Cooling Units

- Cooling Techniques: Air-based and Liquid-based

- General Construction: Core & Shell Development, Installation & Commissioning Services, Engineering & Building Design, Physical Security, Fire Detection & Suppression, and DCIM

- Tier Standard: Tier I & II, Tier III, and Tier IV

- Geography: Middle East (UAE, Saudi Arabia, Israel, Qatar, Oman, Kuwait, Bahrain, and Other Middle Eastern Countries)

Industry Analysis Report, Regional Outlook, Growth Potential, Price Trends, Competitive Market Share & Forecast 2026–2031.

This report includes market data points, ranging from trend

analyses to market estimates & forecasts that you can customize

MIDDLE EAST DATA CENTER MARKET REPORT SCOPE

| REPORT ATTRIBUTE | DETAILS |

|---|---|

| MARKET SIZE – INVESTMENT (2031) | USD 20.74 Billion |

| MARKET SIZE – INVESTMENT (2025) | USD 7.61 Billion |

| CAGR - INVESTMENT (2025-2031) | 18.19% |

| MARKET SIZE - AREA (2031) | 3,638 Thousand Square feet |

| POWER CAPACITY (2031) | 921 MW |

| HISTORIC YEAR | 2022-2024 |

| BASE YEAR | 2025 |

| FORECAST YEAR | 2026-2031 |

| SEGMENTS BY | Infrastructure, IT Infrastructure, Electrical Infrastructure, Mechanical Infrastructure, Cooling Systems, Cooling Techniques, General Construction, Tier Standard, Geography |

| GEOGRAPHIC ANALYSIS | Middle East (UAE, Saudi Arabia, Israel, Qatar, Oman, Kuwait, Bahrain, and Other Middle Eastern Countries) |

MIDDLE EAST DATA CENTER MARKET SIZE & INSIGHTS

The Middle East data center market size witnessed investments of USD 7.61 billion in 2025 and will witness investments of USD 20.74 billion by 2031, growing at a CAGR of 18.19% during the forecast period. The market is experiencing rapid global growth, fueled by rising cloud adoption, the expansion of edge computing, and the increasing use of technologies such as AI, big data, and the Internet of Things (IoT).

The UAE continues to rank among the most advanced data center markets in the Middle East, supported by accelerating digitalization, proactive government initiatives, high internet and social media penetration, extensive inland and submarine connectivity, as well as a well-defined regulatory framework. These factors collectively position the country as a preferred destination for regional and global investors.

The UAE government continues to introduce financial incentives and national programs to expand broadband infrastructure and accelerate 5G deployment. These initiatives prioritize rural and underserved regions, enabling wider access to ultra-high-speed connectivity and supporting digital inclusion.

MIDDLE EAST DATA CENTER MARKET KEY TRENDS

Adoption of Sustainability & Renewable Energy in Data Centers

- The adoption of sustainability and renewable energy in data center operators is increasing steadily in the Middle East region as data center firms are increasingly focusing on developing environmentally friendly data centers to reduce their carbon emissions. Data center firms are adopting a wide range of sustainability practices, such as leveraging renewable sources to power data center operations, installing liquid cooling technologies, replacing diesel generators with HVO-powered generators, and other practices to promote sustainability across data centers.

- The adoption of sustainability and renewable energy in data centers will help companies reduce their operational costs. Therefore, the trend of adopting sustainability and renewable energy in data centers will further increase over the next three to five years.

Increasing Adoption of Artificial Intelligence

- We observe that in the Middle East countries, the government is stepping up initiatives to accelerate digital transformation, signing strategic partnerships and launching public programs to bring cloud, AI, and secure local infrastructure online.

- The Saudi Data & AI Authority (SDAIA) is a national body that oversees the country’s data governance and AI strategy, while accelerating digital transformation by developing unified data platforms and promoting AI adoption across various sectors to position Saudi Arabia as one of the regional leaders in Artificial Intelligence (AI) in the Middle East region.

- The Middle East region is boosting the development of AI with various initiatives, such as focusing on the development of AI-ready data centers, encouraging various companies to invest in developing AI, and promoting the adoption of AI across various industries, including healthcare, finance, and technology, to enhance digital transformation

Rise in Automation & Digitalization

- The Middle East region is witnessing a rapid surge in digitalization and automation, driven by advancements in cloud computing, Artificial Intelligence (AI), Internet of Things (IoT), and digital government services.

- The companies across various sectors are expected to adopt digital technologies for their daily operations to boost their productivity and stay competitive in the market; this is expected to significantly drive the demand for data center development in the Middle East during the forecast period.

- The governments of Middle East region countries are taking initiatives to accelerate digital transformation, signing strategic partnerships and launching public programs to bring cloud, AI, and secure local infrastructure online.

- The Saudi Vision 2030 aims to drive Saudi Arabia's digital transformation by expanding nationwide digital infrastructure, promoting e-government and smart city initiatives, supporting public and private sectors to focus on the development of emerging technologies, including Artificial Intelligence (AI), big data, and cloud computing, as well as encouraging innovation and private-sector participation to develop a highly efficient and interconnected digital economy

IMPACT OF WAR ON DATA CENTERS

- Israel launched its June 2025 strike on Iran with the stated aim of wiping out Iran’s nuclear and ballistic missile programs, after the UN nuclear watchdog said Iran violated its non-proliferation obligations; Iran then retaliated with missiles and drones, and the conflict quickly turned the Middle East's digital infrastructure into a risk zone. Iran responded by launching large-scale missile and drone attacks across Middle Eastern countries—including the UAE, Saudi Arabia, Bahrain, Qatar, and Kuwait—primarily because these states host US military bases and strategic infrastructure, effectively making them indirect participants in the conflict.

- The first major wave of attacks on data center infrastructure in the Middle East was reported around early March 2026, marking a significant escalation in regional risk exposure. During this period, cloud infrastructure providers began reporting physical disruptions to their facilities. The incidents highlighted that data centers, despite being civilian infrastructure, can be indirectly or directly affected during geopolitical conflicts. This marked a shift in perceived risk for digital infrastructure in the region.

- In early March 2026, facilities operated by Amazon Web Services in the UAE and Bahrain were impacted, with multiple sites facing operational disruption. With further reports of damage at the Pure Data Centres Group campus in Abu Dhabi, and a separate attack on an Oracle facility in Dubai. Reports indicated that two UAE-based facilities were directly struck, while a Bahrain facility experienced a nearby impact. These incidents caused interruptions in normal operations and required emergency response measures. It remains one of the few publicly confirmed physical impacts on hyperscale data centers in the Middle East.

- From an investment perspective, such incidents introduce short-term uncertainty and risk perception among global investors. There are indications that some operators have paused or reassessed planned investments in the region following the events. Concerns around geopolitical stability and infrastructure vulnerability can slow decision-making for new projects. This may temporarily impact the pace of data center expansion in affected markets.

- Rising energy prices and ongoing supply chain disruptions triggered by the Iran conflict have significantly increased the financial risk of investing in digital infrastructure across the Middle East. The war has disrupted oil and energy markets—impacting nearly 20% of global supply routes—leading to higher operating costs, inflationary pressure, and uncertainty around project execution timelines.

- This uncertainty has already begun to affect investor behavior, with companies such as Pure Data Centres pausing new investments in the Middle East due to geopolitical instability, material shortages, and concerns over infrastructure vulnerability. The conflict has exposed data centers as potential targets, while escalating costs and logistical challenges are making large-scale deployments more complex, thereby increasing hesitation among investors to commit capital until conditions stabilize.

- In the long term, these events are likely to increase the cost of capital and insurance for data center projects in the Middle East region. Investors may demand higher returns to compensate for elevated risk levels associated with regional instability. Additionally, stricter due diligence and risk assessments will become standard before funding large-scale projects. This could reshape how future investments are structured in the region.

MIDDLE EAST DATA CENTER MARKET SEGMENTATION INSIGHTS

- Traditional data centers typically accommodate racks with densities ranging from 5kW to 8 kW, which is inadequate for efficiently supporting AI workloads. Thus, data center operators are investing significantly to install high-density racks in their data center facilities. For instance, in 2025, Khazna Data Centers was involved in the development of the AUH7 data center, which has been designed to support rack densities of over 50 kW–65 kW per rack.

- To manage the high heat densities associated with advanced computing workloads, several data center operators in the Middle East region are expected to invest in the adoption of advanced liquid cooling technologies, including Direct-to-Chip Liquid Cooling (DLC) and immersion cooling technologies, in the coming years.

- In May 2025, DataVolt, a Saudi Arabian data center firm, signed a supplier contract with Vertiv and Chemours to procure advanced power, cooling, and liquid cooling equipment for data center development

- In April 2025, NED started the construction of the first phase of its debut Alpha Campus in Israel, which will support multiple cooling options, including Direct Liquid Cooling (DLC) starting at 100 kW per rack, in-row cooling, and rear-door heat exchangers for entire data halls.

GEOGRAPHICAL ANALYSIS

- In the Middle East data center market, in 2025, the UAE dominates the market in terms of power capacity, with a market share of around 37.66% in 2025, followed by Saudi Arabia with a market share of around 27.60%, Israel with a market share of around 8.77%, and this is followed by Turkey, Kuwait, Oman, Qatar, and Bahrain.

- Abu Dhabi and Dubai are the primary locations for the development of data centers in the UAE; these cities are among the country’s leading smart cities.

- Dammam, Riyadh, and Jeddah are the primary locations for the development of data centers in Saudi Arabia. Cities including Al Qassim, Al Ahsa, Madinah, Makkah, Neom, and Al Khobar are gaining momentum for data center development in recent years.

- Petah Tikva, Herzliya, and the Jerusalem corridor are the emerging secondary hubs for data center development in Israel, which attract both enterprise and government projects as well as complement the Tel Aviv metro area.

- In Israel, northern cities such as Haifa and regions in the Negev continue to gain attraction for data center investments owing to available land, the potential for renewable energy use, and opportunities for larger-scale facilities

- Doha, the capital city of Qatar, it hosts the highest number of data centers in Qatar. Due to its strong connectivity, business ecosystem, and proximity to government institutions, make its preferred location for data center development in Qatar.

- In Oman, Muscat hosts the highest number of data centers, this is followed by Salalah. This concentration can primarily be attributed to the status of Muscat as the capital and main commercial hub, offering strong connectivity, government presence, enterprise demand, and reliable power infrastructure. Salalah follows due to its strategic location as a major subsea cable landing point, making it attractive for interconnection and edge-focused data center developments.

- In Bahrain, Manama is one of the primary locations for data center investment. Other cities, such as Hamala, are expected to attract investments in data center in the upcoming year due to their low land costs and high space availability for facility development.

- In Turkey, Istanbul hosts the highest number of data centers, and the city has strong digital infrastructure and connectivity, accounting for a large concentration of businesses and a skilled IT workforce, making it the natural hub for cloud providers, colocation services, and enterprise-scale data operations in the country.

- In the Middle East, some developing markets, such as Iraq, Jordan, and Lebanon, offer relatively lower land and operational costs as compared with the more mature Middle Eastern markets.

VENDOR LANDSCAPE

- The Middle East data center market has the presence of IT infrastructure providers such as Arista Networks, Atos, Cisco, Dell Technologies, Lenovo, NVIDIA, among others.

- In December 2025, NVIDIA announced plans to build the largest server farm in Israel at the Mevo Carmel industrial zone, investing about $1.5 billion in infrastructure, including its own computing equipment. The facility is estimated to house advanced supercomputers and Blackwell GPUs for the AI development and testing of next-generation chips. Construction is slated to begin in 2027, with initial occupancy planned for 2031.

- In the Middle East region, the cloud market is expected to steadily experience significant growth in the forecast period. The major global cloud providers, such as Alibaba Cloud, Amazon Web Services (AWS), Huawei Cloud, Microsoft, Google, Oracle Cloud, and Tencent Cloud, have a dedicated cloud region across the region; these providers will continue to expand their presence across the region. For instance, in November 2025, Google partnered with Turkcell to develop a cloud region and a data center in Turkey for an investment of over $2 billion. Under the collaboration, Turkcell will serve as the infrastructure provider while also acting as a reseller of Google’s cloud services.

- The Middle East data center market has the presence of support infrastructure providers such as ABB, Airedale, Alfa Laval, Canovate, Caterpillar, Cummins, Eaton, Generac Power Systems, Johnson Controls, Legrand, Rolls-Royce, STULZ, Vertiv, among others. These companies lead the market, driving advancements in power systems and cooling systems to ensure efficiency and reliability

- The Middle East data center market has a presence of global and local contractors and subcontractors such as AECOM, Al Latifia Trading & Contracting, ALDAR, Anel Group, Arup, Ashtrom Group, Black & White Engineering, HHM Group, Mace, Qatar Site & Power, Skorka Architects, Sudlows, Turner & Townsend, among others. which provides construction, installation, engineering, and commissioning services for the construction of data center facilities across the region.

- The Middle East data center market has global and local data center operators, including Amazon Web Services (AWS), Batelco, Bynet Data Communications, Compass Datacenters, DAMAC Digital, Du, Equinix, Google, Gulf Data Hub, Khazna Data Centers, among others, who are the major investors in the Middle East data region. Many of these companies are competing with new entrants in supporting multi-megawatt requirements across key data center destinations in the region.

- The Middle East data center market will witness new data center investors to invest in the region, such as Agility Logistics Parks, Anan, DataVolt, Desert Dragon Data Centers, Ezditek, HUMAIN, Keystone, NED, and Techtonic.

SNAPSHOT

The Middle East data center construction market size by investment will reach USD 20.74 billion by 2031, growing at a CAGR of 18.19% from 2025 to 2031.

The following factors are likely to contribute to the growth of the Middle East data center construction market during the forecast period:

- Rising Adoption of Cloud-based Services

- Improvement in Connectivity via Submarine Cables

Base Year: 2025

Forecast Year: 2026-2031

The study considers the present scenario of the Middle East data center construction market and its market dynamics for 2026−2031. It covers a detailed overview of several market growth enablers, restraints, and trends. The report offers both the demand and supply aspects of the market. It profiles and examines leading companies and other prominent ones operating in the market.

Segmentation by Infrastructure

- IT Infrastructure

- Electrical Infrastructure

- Mechanical Infrastructure

- General Construction

Segmentation by IT Infrastructure

- Server Infrastructure

- Storage Infrastructure

- Network Infrastructure

Segmentation by Electrical Infrastructure

- UPS Systems

- Generators

- Transfer Switches & Switchgear

- PDUs

- Other Electrical Infrastructure

Segmentation by Mechanical Infrastructure

- Cooling Systems

- Racks

- Other Mechanical Infrastructure

Segmentation by Cooling Systems

- CRAC & CRAH Units

- Chiller Units

- Cooling Towers, Condensers, and Dry Coolers

- Other Cooling Units

Segmentation by Cooling Techniques

- Air-based

- Liquid-based

Segmentation by General Construction

- Core & Shell Development

- Installation & Commissioning Services

- Engineering & Building Design

- Physical Security

- Fire Detection & Suppression

- DCIM

Segmentation by Tier Standard

- Tier I & II

- Tier III

- Tier IV

Segmentation by Geography

- Middle East

- UAE

- Saudi Arabia

- Israel

- Qatar

- Oman

- Kuwait

- Bahrain

- Other Middle Eastern Countries

IT Infrastructure Providers

- Arista Networks

- Atos

- Broadcom

- Cisco

- Dell Technologies

- Fujitsu

- Hewlett Packard Enterprise (HPE)

- Huawei Technologies

- IBM

- Inspur Group

- Lenovo

- NetApp

- NVIDIA

- Oracle

- Supermicro

Data Center Support Infrastructure Providers

- ABB

- Airedale

- Alfa Laval

- Canovate

- Caterpillar

- Cummins

- Dakin Applied

- Delta Electronics

- EAE Group

- Eaton

- Enrogen

- Envicool

- Generac Power Systems

- HITEC Power Protection

- Johnson Controls

- Legrand

- Mitsubishi Electric

- Piller Power Systems

- Rittal

- Rolls-Royce

- Schneider Electric

- Siemens

- STULZ

- Vertiv

Data Center Construction Contractors and Sub Contractors

- AECOM

- Al Latifia Trading & Contracting

- ALDAR

- ALEC Data Center Solutions

- Anel Group

- Arup

- Ashi & Bushnag

- Ashtrom Group

- ASU

- AtkinsRéalis

- Auerbach HaLevy Architects

- Azura Consultancy

- Black & White Engineering

- Capitoline

- Core Emirates

- DAR Group

- Datalec Precision Installations (DPI)

- DC PRO Engineering

- Deerns

- DMC Global Partners

- Edarat Group

- EGEC

- Electra

- Enmar Engineering

- Group AMANA

- Harinsa Qatar

- HATCO

- HHM Group

- Hill International

- ICS Nett

- INT’LTEC

- ISG

- Juffali Airconditioning, Mechanical, and Electrical Company (JAMED)

- James L. Williams (JLW)

- John Paul Construction

- Laing O’Rourke

- Laith Electro Mechanical

- Linesight

- M+W Group (Exyte)

- Mace

- McLaren Construction Group

- MEC - Margolin Bros. Engineering & Consulting

- Middle East Modern Architecture (MEMA)

- Mercury

- MIS

- NDA Group

- Prota Engineering

- PTS

- Qatar Site & Power

- Raghav Contracting

- RED Engineering Design

- RW Armstrong

- SANA Control Systems

- Scientechnic

- Site & Power DK (Midis Group)

- Skorka Architects

- Sudlows

- Telal Engineering & Contracting

- Turner & Townsend

- UBIK

- Yeda Engineering

Data Center Investors

- Adgar Investments & Development

- Amazon Web Services (AWS)

- Batelco

- Bynet Data Communications

- Compass Datacenters

- DAMAC Digital

- Du

- EdgeConneX

- Equinix

- Gulf Data Hub

- Khazna Data Centers

- MedOne

- MEEZA

- Mega Data Centers (MEGA DC)

- Microsoft

- Mobily

- Moro Hub

- NGN

- Ooredoo

- Oracle

- Pure Data Centres

- Quantum Switch

- Sahayeb Data Centers

- center3

- Türk Telekom

- Turkcell

New Entrants

- Agility Logistics Parks

- Anan

- DataVolt

- Desert Dragon Data Centers

- Ezditek

- HUMAIN

- Keystone

- NED

- Techtonic

MIDDLE EAST DATA CENTER MARKET FAQs

What is the growth rate of the Middle East data center market?

How big is the Middle East data center market?

What is the estimated market size in terms of area in the Middle East data center market by 2031?

What are the key trends in the Middle East data center market?

How much MW of power capacity is expected to reach the Middle East data center market by 2031?

For more details, please reach us at [email protected]

For more details, please reach us at [email protected]

Select a license type that suits your business needs

Single User Licence

- Report accessible by one user only

- Free 10% or 3 days of customization

- Free post-sale service assistance

- Continuous support through email

5 User Licence

- Report accessible by 5 users within the organization

- Free 15% or 4.5 days of customization

- Continuous support through email and telephone

- Free analyst hour

- Free Upgrade: If an updated report published within 180 days of purchase, you will get the revised report free of charge

Corporate Licence

- Free Datasheet worth $1500

- Report accessible by the entire organization

- Free 20% or 6 days of customization

- Free post-sale service assistance

- Continuous support through email and telephone

- Direct access to lead analysts

- Free analyst hour

- Free Upgrade: If an updated report published within 180 days of purchase, you will get the revised report free of charge

Datasheet Licence

- Report accessible by 1 user only

- Free 15% or 32 hours of customization

- Free post-sale service assistance

- Direct access to lead analysts

Frequently Asked Questions

What is the growth rate of the Middle East data center market?

How big is the Middle East data center market?

What is the estimated market size in terms of area in the Middle East data center market by 2031?

What are the key trends in the Middle East data center market?

How much MW of power capacity is expected to reach the Middle East data center market by 2031?

Other RELATED Reports

Middle East Data Center Construction Market – Industry Outlook & Forecast 2026-2031

Published : June 2026