Southeast Asia Data Center Market Landscape 2026-2031

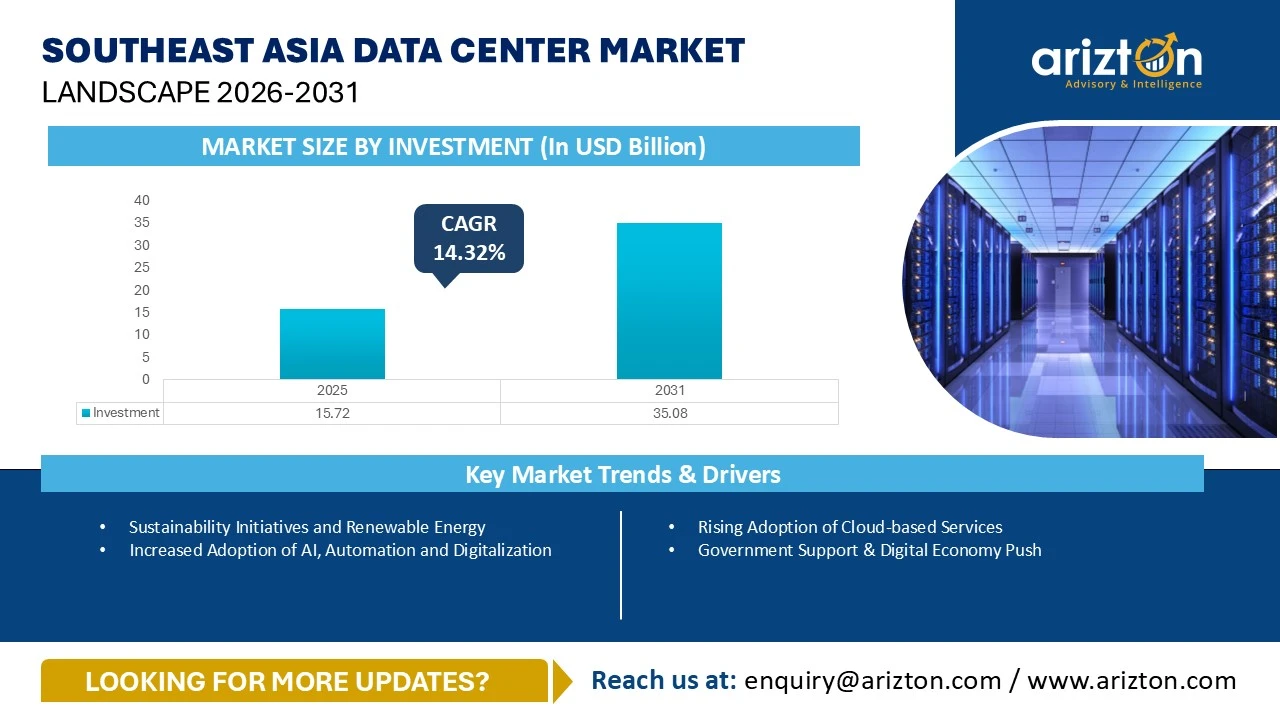

THE SOUTHEAST ASIA DATA CENTER MARKET SIZE WITNESSED INVESTMENTS OF USD 15.72 BILLION IN 2025 AND WILL WITNESS INVESTMENTS OF USD 35.08 BILLION BY 2031, GROWING AT A CAGR OF 14.32% DURING THE FORECAST PERIOD.

Southeast Asia Data Center Market Growth Insights – Market Area to Reach 5.83 Million Sq. Ft. and Power Capacity to Surpass 1,435 MW by 2031, Driven by Cloud Expansion, Edge Computing Growth, and Rising AI, Big Data & IoT Deployments Across the Region (2026–2031)

Published Date : June 2026

Last Updated : June 2026

format: PDF

edition : Fifth Edition

296 pages

region

countries

244 company

10 segments

Purchase Options

Southeast Asia Data Center Market Landscape 2026-2031

THE SOUTHEAST ASIA DATA CENTER MARKET SIZE WITNESSED INVESTMENTS OF USD 15.72 BILLION IN 2025 AND WILL WITNESS INVESTMENTS OF USD 35.08 BILLION BY 2031, GROWING AT A CAGR OF 14.32% DURING THE FORECAST PERIOD.

The Southeast Asia Data Center Market Size, Share, & Trends Analysis By

- Facility Type: Hyperscale Data Centers, Colocation Data Centers, and Enterprise Data Centers

- Infrastructure: IT Infrastructure, Electrical Infrastructure, Mechanical Infrastructure, and General Construction

- IT Infrastructure: Server Infrastructure, Storage Infrastructure, and Network Infrastructure

- Electrical Infrastructure: UPS Systems, Generators, Transfer Switches & Switchgear, PDUs, and Other Electrical Infrastructure

- Mechanical Infrastructure: Cooling Systems, Racks, and Other Mechanical Infrastructure

- Cooling Systems: CRAC & CRAH Units, Chiller Units, Cooling Towers, Condensers, Dry Coolers, and Other Cooling Units

- Cooling Techniques: Air-based and Liquid-based

- General Construction: Core & Shell Development, Installation & Commissioning Services, Engineering & Building Design, Physical Security, Fire Detection & Suppression, and DCIM

- Tier Standard: Tier I & II, Tier III, and Tier IV

- Geography: Southeast Asia (Singapore, Indonesia, Malaysia, Thailand, Philippines, Vietnam, and Rest of Southeast Asia Countries)

Industry Analysis Report, Regional Outlook, Growth Potential, Price Trends, Competitive Market Share & Forecast 2025–2030.

This report includes market data points, ranging from trend

analyses to market estimates & forecasts that you can customize

SOUTHEAST ASIA DATA CENTER MARKET REPORT SCOPE

| REPORT ATTRIBUTE | DETAILS |

|---|---|

| MARKET SIZE – INVESTMENT (2031) | USD 35.08 Billion |

| MARKET SIZE – INVESTMENT (2025) | USD 15.72 Billion |

| CAGR - INVESTMENT (2025-2031) | 14.32% |

| MARKET SIZE - AREA (2031) | 5.83 Million Square feet |

| POWER CAPACITY (2031) | 1,435 MW |

| HISTORIC YEAR | 2022-2024 |

| BASE YEAR | 2025 |

| FORECAST YEAR | 2026-2031 |

| SEGMENTS BY | Facility Type, Infrastructure, IT Infrastructure, Electrical Infrastructure, Mechanical Infrastructure, Cooling Systems, Cooling Techniques, General Construction, Tier Standard, Geography |

| GEOGRAPHIC ANALYSIS | Singapore, Indonesia, Malaysia, Thailand, Philippines, Vietnam, and Rest of Southeast Asia Countries |

SOUTHEAST ASIA DATA CENTER MARKET SIZE & INSIGHTS

The Southeast Asia data center market size witnessed investments of USD 15.72 billion in 2025 and will witness investments of USD 35.08 billion by 2031, growing at a CAGR of 14.32% during the forecast period. The Southeast Asian data center market continues to experience rapid global growth, driven by increasing cloud adoption, the expansion of edge computing, and the growing deployment of technologies such as AI, big data, and the IoT.

The average cost of data center construction in Southeast Asia can range from $7 million to $11 million per MW, depending on the location. These elevated costs are influenced by factors such as limited land availability, high labour rates, inflation, and access to power.

Data center investments in Singapore have slowed down in recent years due to the moratorium on data center construction. However, after the lifting of the moratorium in 2022, the market has started receiving investments. Singapore has launched pilot projects to restart data center development, focusing on sustainability, energy efficiency, and controlled capacity growth after a temporary moratorium on new data centers.

Malaysia continues to emerge as a prime destination for data center investments due to its location between major Southeast Asian markets and robust digital infrastructure. Furthermore, the comparative affordability of land and energy costs, especially when contrasted with neighbouring countries such as Singapore, continues to attract global technology companies to establish and grow their operations in Malaysia.

Thailand emerges as a key player in the Southeast Asia data center market, showcasing substantial growth potential. The upcoming data center projects in Thailand aim to address both local and wider ASEAN regional needs for data storage and cloud services. Once developed, these projects are anticipated to enhance the capabilities of the country in cloud computing and AI, while also creating new employment opportunities.

The Philippines is becoming an attractive alternative to more expensive regional markets, with a strategic location in Southeast Asia, expanding subsea connectivity, and government incentives further encouraging both local and foreign investors to enter the market. Its youthful workforce, expanding energy infrastructure, and strategic position within the APAC network corridor further strengthen its appeal.

SOUTHEAST ASIA DATA CENTER MARKET KEY TRENDS

Sustainability Initiatives and Renewable Energy

- The Southeast Asian data center market is witnessing a growing emphasis on sustainable infrastructure and clean energy adoption, driven by supportive government initiatives and corporate decarbonization goals. Several countries in the region are promoting renewable energy integration, carbon reduction strategies, and energy-efficient digital ecosystems, creating favourable conditions for the expansion of green hyperscale and colocation data centers.

- Data center operators invest in many data centers with power purchase agreements (PPAs) to make efficient use of and reduce their carbon footprint in their facilities. For instance, in October 2025, NeutraDC signed an electrical purchase agreement with Indonesian electrical utility, PT PLN Batam to supply 90MVA of medium-voltage electricity to its Batam data center between 2025 and 2028.

- The implementation of water sustainability practices is becoming increasingly popular among data center operators looking to enhance their environmental sustainability profiles. In August 2025, DayOne announced its plan to integrate alternative water sources into its data center operations in Johor, Malaysia. As part of the project, DayOne intends to implement Malaysia’s first river water treatment system, specifically designed for data center operations at its facility in Kempas Tech Park, Johor

- The combination of renewable energy expansion, supportive government policies, and sustainability-focused investments strengthens the position of Southeast Asia as an attractive destination for green data center development. These initiatives are expected to accelerate the adoption of low-carbon power, energy-efficient technologies, and environmentally responsible digital infrastructure across the region.

Increased Adoption of AI, Automation and Digitalization

- Southeast Asia continues to experience accelerated adoption of AI and ML across industries, including finance, healthcare, and logistics, fuelling rising demand for high-performance data centers. As AI computing requirements are projected to increase nearly tenfold by 2030, the data center capacity of the region is expected to almost triple to support this wave of digital transformation.

- The Thai government has come up with initiatives for automation and digitalization. The Thailand 4.0 framework promotes Smart City and Industry 4.0 projects. DEPA (Digital Economy Promotion Agency) collaborates with private and public partners to accelerate IoT deployment. It has also established the Digital Economy Promotion Agency (DEPA) under the Ministry of Digital Economy and Society (MDES). DEPA collaborates with the private sector and numerous partner organizations, including agencies under the Ministry of Industry, to drive IoT innovation.

- Vietnam is entering a new phase of digital maturity, and AI is at the forefront of this transformation. Major Investments by Global tech leaders, including NVIDIA, are significantly expanding their AI footprint in Vietnam. In December 2024, NVIDIA announced the signing of an MOU with Vietnam's Ministry of Planning and Investment to set up two advanced AI centers in the country.

- Singapore has been an early mover in AI governance, launching one of the first national AI strategies in the world in 2019 and updating it in 2023 through NAIS 2.0. The revised strategy outlines plan to more than triple the nation’s AI workforce within three to five years, accelerate AI creation and adoption among enterprises, strengthen national research priorities, and position Singapore as a global leader in responsible AI development

SOUTHEAST ASIA DATA CENTER MARKET SEGMENTATION INSIGHTS

- Server infrastructure in Southeast Asia's data center market is a rapidly evolving segment, driven by digital transformation, increasing internet penetration, and the need for cloud services in the region.

- The electrical infrastructure is witnessing several innovations in UPS systems, generators, transfer switches & switchgears and other electrical equipment. Most data centers adopt N+1 diesel generators, providing backup fuel for up to 24 hours or more. For instance, the SG1 data center facility by Equinix in Ayer Rajah Industrial Park is equipped with block-redundant UPS systems with 2N redundancy

- Additionally, several innovative UPS batteries such as Nickel-Zinc (NiZn) and Sodium-Ion batteries are gaining traction in the market due to their high-power density, safety, sustainability, and other factors.

- Liquid cooling is becoming a significant trend that major colocation operators are implementing in their data center facilities. It is emerging as a key differentiator for colocation providers as AI and compute-intensive workloads continue to grow. The upcoming Jalan Boon Lay facility in Singapore by ST Engineering is likely to incorporate multiple cooling options, including the Airbitat DC Cooling System of the company, along with liquid and immersion cooling technologies.

SOUTHEAST ASIA DATA CENTER MARKET GEOGRAPHICAL ANALYSIS

- The total area in the Southeast Asia region that is dedicated to data centers reflects a diverse distribution across key countries. For instance, Malaysia contributes approximately 2,525 thousand sq ft, representing the largest share due to its growing infrastructure and favorable policies. Indonesia follows suit, with 545 thousand sq ft of area, as well as rapid industrial growth and increasing cloud adoption. Meanwhile, emerging markets, including Vietnam and the Philippines, although smaller at 170,000 sq ft and 185,000 sq ft, respectively, are demonstrating significant YoY expansion, indicating rising importance in the regional data center landscape

- Malaysia holds a significant share of the market in the data center growth in Southeast Asia. The digital transformation policies of the country, coupled with the widespread adoption of AI, support major investments in data center infrastructure. In September 2025, ZDATA Technologies, a Chinese data center operator, sought a $500 million loan to finance its upcoming data center project in Johor, Malaysia. The company aims to expand its footprint in the rapidly growing Malaysian market, particularly in Johor Bahru’s Gelang Patah region, located near the Singapore border.

- In Indonesia, Batam is gaining momentum due to its reliable power grids and constant power supply. The island has many power plants, such as coal-fired, natural gas, and renewable energy plants, making it the best choice to set up facilities over other cities in Indonesia. DayOne is constructing a new data center campus in Batam, which will have a combined IT load capacity of around 72MW.

- As of December 2025, Singapore hosts 45 operational data center facilities, spanning a total of 5,101.4 thousand sq ft of white floor space, and 6 upcoming facilities, covering around 652.5 thousand sq ft. Singapore is one of the most expensive markets in the world for developing data center facilities. In addition, land availability for data center development is very limited. Operators continue to purchase industrial plots to convert into data centers; however, such activities remain relatively low in the market.

- Thailand offers foreign ownership flexibility, access to pre-approved energy & fibre infrastructure, and various incentives through its EEC, which makes it the perfect location to invest in Southeast Asia. Bangkok is the preferred location in Thailand, with major investments from colocation service providers such as ST Telemedia Global Data Centres, AIS Business (CSL), OneAsia Network, True IDC, Internet Thailand, Telehouse, and SUPERNAP Thailand.

- The Vietnamese government aims to achieve net-zero carbon emissions by 2050. It is planning to increase the share of renewable energy in its national energy mix to 39.2% by 2030. The Vietnamese government is committed to promoting key sectors; this includes the development of clean energy solutions. It is currently establishing a Direct PPA, specifically for the data center industry, as well as refining digital regulations and laws to support the advancements in AI and digital technologies.

- The Philippines is becoming an attractive alternative to more expensive regional markets, with a strategic location in Southeast Asia, expanding subsea connectivity, and government incentives further encouraging both local and foreign investors to enter the market. Its youthful workforce, expanding energy infrastructure, and strategic position within the APAC network corridor further strengthen its appeal.

VENDOR LANDSCAPE

- The Southeast Asia data center market has the presence of key investors such as Bridge Data Centres, Digital Realty, Equinix, AirTrunk, NTT DATA, Princeton Digital Group, DayOne, ST Telemedia Global Data Centres, Vantage Data Centers, and others.

- New Entrants include A-FLOW, Aslan Energy Capital, Beeinfotech PH, BRIGHT RAY, BW Digital, CloudHQ, CtrlS Datacenters, DAMAC Digital, NEXTDC, ZDATA Technologies, STACK Infrastructure and several others.

- In the months of May-June of 2025, six new projects were approved by Thailand BOI with a cumulative investment of $3.6 billion (521.2 billion baht). Five among them are the new entrants to the Thailand market, which include Galaxy Data Centers, Galaxy Peak Data Centers, ZDATA Technologies (Stratus Technologies), Vistas Technologies, and Digital Edge DC. The one existing investor is Bridge Data Centers. In November 2025, the Thailand BOI approved four additional data center projects with a total investment of $3.1 billion from Telehouse, ZDATA Technologies, NextGen Data Center and Cloud Services Co., Ltd., a subsidiary of Dubai-based DAMAC Digital and Zenith Data Center and Cloud Services.

- The Southeast Asia region continues to witness investment from hyperscalers like Microsoft, Google, AWS, and others. For instance, in Indonesia, Microsoft launched its first data center in May 2025 and is expected to contribute around $2.5 billion to the economy and create 60,000 jobs by 2028. In addition, it will also support digital training for one million people, with 840,000 already participating in AI capability-building.

SNAPSHOT

The Southeast Asia data center construction market size by investment will reach USD 35.08 billion by 2031, growing at a CAGR of 14.32% from 2025 to 2031.

The following factors are likely to contribute to the growth of the Southeast Asia data center construction market during the forecast period:

- Rising Adoption of Cloud-based Services

- Government Support & Digital Economy Push

- Improvement in Connectivity via Submarine Cables

Base Year: 2025

Forecast Year: 2026-2031

The study considers the present scenario of the Southeast Asia data center construction market and its market dynamics for 2026−2031. It covers a detailed overview of several market growth enablers, restraints, and trends. The report offers both the demand and supply aspects of the market. It profiles and examines leading companies and other prominent ones operating in the market.

Segmentation by Facility Type

- Hyperscale Data Centers

- Colocation Data Centers

- Enterprise Data Centers

Segmentation by Infrastructure

- IT Infrastructure

- Electrical Infrastructure

- Mechanical Infrastructure

- General Construction

Segmentation by IT Infrastructure

- Server Infrastructure

- Storage Infrastructure

- Network Infrastructure

Segmentation by Electrical Infrastructure

- UPS Systems

- Generators

- Transfer Switches & Switchgear

- PDUs

- Other Electrical Infrastructure

Segmentation by Mechanical Infrastructure

- Cooling Systems

- Racks

- Other Mechanical Infrastructure

Segmentation by Cooling Systems

- CRAC & CRAH Units

- Chiller Units

- Cooling Towers, Condensers, and Dry Coolers

- Other Cooling Units

Segmentation by Cooling Techniques

- Air-based

- Liquid-based

Segmentation by General Construction

- Core & Shell Development

- Installation & Commissioning Services

- Engineering & Building Design

- Physical Security

- Fire Detection & Suppression

- DCIM

Segmentation by Tier Standard

- Tier I & II

- Tier III

- Tier IV

Segmentation by Geography

- Singapore

- Indonesia

- Malaysia

- Thailand

- Philippines

- Vietnam

- Rest of Southeast Asia Countries

VENDOR LANDSCAPE

Key Data Center IT Infrastructure Providers

- Arista Networks

- Business Overview

- Service Offerings

- Atos

- Broadcom

- Cisco Systems

- Dell Technologies

- Fujitsu

- Hewlett-Packard Enterprise

- Huawei Technologies

- IBM

- Inspur

- Lenovo

- NetApp

- NVIDIA

Key Data Center Support Infrastructure Providers

- ABB

- Business Overview

- Service Offerings

- Aggreko

- Airedale

- Bosch

- Caterpillar

- Cummins

- Cyber Power Systems

- Delta Electronics

- Eaton

- EKG M & E

- Fuji Electric

- HITEC Power Protection

- Johnson Controls

- Legrand

- Mitsubishi Electric

- Narada

- Piller Power Systems

- Rittal

- Rehlko

- Rolls-Royce

- Schneider Electric

- Siemens

- Socomec Group

- Systemair

- STULZ

- TECO Electric & Machinery

- Trane

- Vertiv

- ZTE

Key Data Center Contractors & Subcontractors

- Advance Power Engineering

- Business Overview

- Service Offerings

- AECOM

- AEON SERVICES

- Aesler Grup

- AO Construction

- Apave

- Arcadis

- Archetype Group

- Architects 49

- ARKONIN

- Arup

- Asdi Swasatya

- Asima Architects

- AtkinsRealis

- Aurecon

- AVO Technology

- AWP Architects

- BECA

- B-Global Tech

- Binastra Corporation

- Chaan

- China Construction Industrial & Energy Engineering Group

- Critical Holdings Berhad

- Comfac

- CSF Group

- Cundall

- CTC-Global

- Cyclect Group

- Data Center Design Corporation (DCDC)

- DCD Technology

- DSCO Group

- Design Coordinates

- Exyte (M+W Group)

- Endec Group

- First Balfour

- Finishing Touch Design Studio

- Fortis Construction

- Gamuda

- Gammon Construction

- Gensler

- GCM Technologies

- GreenVeit

- Greatians Consulting

- HSS Engineers

- Infraset

- IJM Corporation

- ISG

- INHERIT TECHNOLOGY ENGINEERING

- Jaya Karya Integrasi

- JSLA Architects

- Jurutera JRK

- Kienta Engineering Construction

- KAJIMA CORPORATION

- LandArc Associates

- Leighton Asia

- Linesight

- LSK Engineering

- Mace

- Meg Consult

- Megawide Construction Corporation

- Meinhardt Group

- MES Group

- Mitrajaya Holdings

- Monocrete

- MN Holdings

- NTT Facilities

- Nakano Corporation

- OWH Consulting

- Parker, van den Bergh

- PKT Quantity Surveyors

- Plan Architect

- PM Group

- PMX Malaysia

- Powerware Systems

- PT Berca Buana Sakti

- PT Jaya Teknik

- PT Jaya Obayashi

- PT AtoZ Teknik

- PT Total Bangun Persada Tbk

- PT PP

- PT Indokoei International

- PT SMI

- PT Sumaraja Indah

- PT Acset Indonusa Tbk

- PPS Group

- PRONET

- QTCG

- Regional Development Consortium (RDC) Arkitek

- Ramboll

- Red Engineering

- Sato Kogyo

- S5 Engineering

- Shaw Architect

- SOL E&C Investment Construction Joint Stock Company

- Sunway Construction Group

- Syska Hennessy Group

- Syntec Construction

- Tarnas

- Taikisha

- Tetra

- Thornton Tomasetti

- Turner & Townsend

- Unique Central

- Universal Smart Data Center Technology (USDC Technology)

- Vale Architects

- VINCI Energies

- WT Asia

Key Data Center Investors

- AIMS Data Centre

- Business Overview

- Service Offerings

- AirTrunk

- AIS Business

- Alibaba Cloud

- Amazon Web Services (AWS)

- BDx Data Centers

- Bitera Data Centers

- Biznet Data Center

- Bridge Data Centres

- China Mobile

- Converge ICT Solutions

- CMC Telecom

- Datacomm Diangraha

- DayOne

- DCI Indonesia

- Digital Edge DC

- Digital Hyperspace Indonesia

- Digital Realty

- DITO Telecommunity

- EdgeConneX

- Elitery

- Empyrion Digital

- ePLTD

- Epsilon Telecommunications

- Equinix

- Etix Everywhere

- FPT Telecom

- Global Switch

- Hanoi Telecom

- IDC Indonesia

- IndoKeppel Data Centres

- Internet Thailand

- Iron Mountain

- K2 Strategic

- Keppel Data Centres

- Mapletree

- MettaDC

- Microsoft

- Nxera

- NTT DATA

- OneAsia Network

- Open DC

- Princeton Digital Group

- Pure Data Centres

- Racks Central

- SM+

- ST Engineering

- ST Telemedia Global Data Centres

- SUPERNAP Thailand

- Telehouse

- Telekom Malaysia (TM)

- Telin Singapore

- Telkom Indonesia (NeutraDC)

- Tencent Cloud

- True Internet Data Center (True IDC)

- Vantage Data Centers

- Viettel IDC

- VNPT

- VNTT

- WHA Group

- YTL Data Center Holdings

NEW ENTRANTS

- A-FLOW

- Business Overview

- Service Offerings

- Aslan Energy Capital (AEC)

- Beeinfotech PH

- BRIGHTRAY

- BW Digital

- CloudHQ

- CtrlS Datacenters

- CURRENC Group

- DAMAC Digital

- Digital Halo

- Diode Ventures

- Doma Infrastructure

- Epoch Digital

- Evolution Data Centres

- FutureData

- Gaw Capital

- Galaxy Data Centers

- Global Telecommunications

- Haoyang Data

- i-Berhad

- Infinaxis Data Centre Holdings

- Infracrowd Capital

- Minoro Energi

- NEXTDC

- SEAX Global

- SC Zeus Data Centers

- Siagon Asset Management

- STACK Infrastructure

- TikTok

- YCO Cloud

- ZDATA Technologies

SOUTHEAST ASIA DATA CENTER MARKET FAQs

How big is the Southeast Asia data center market?

What is the growth rate of the Southeast Asia data center market?

What is the estimated market size in terms of area in the Southeast Asia data center market by 2030?

What are the key trends in the Southeast Asia data center market?

How much MW of power capacity is expected to reach the Southeast Asia data center market by 2030?

What is the estimated market size in terms of area in the Southeast Asia data center market by 2030?

How big is the Southeast Asia data center market?

How much MW of power capacity is expected to reach the Southeast Asia data center market by 2030?

What are the key trends in the Southeast Asia data center market?

What is the growth rate of the Southeast Asia data center market?

How much MW of power capacity is expected to reach the Southeast Asia data center market by 2030?

What is the growth rate of the Southeast Asia data center market?

How big is the Southeast Asia data center market?

What is the estimated market size in terms of area in the Southeast Asia data center market by 2030?

What are the key trends in the Southeast Asia data center market?

For more details, please reach us at [email protected]

For more details, please reach us at [email protected]

Select a license type that suits your business needs

Single User Licence

- Report accessible by one user only

- Free 10% or 3 days of customization

- Free post-sale service assistance

- Continuous support through email

5 User Licence

- Report accessible by 5 users within the organization

- Free 15% or 4.5 days of customization

- Continuous support through email and telephone

- Free analyst hour

- Free Upgrade: If an updated report published within 180 days of purchase, you will get the revised report free of charge

Corporate Licence

- Free Datasheet worth $1500

- Report accessible by the entire organization

- Free 20% or 6 days of customization

- Free post-sale service assistance

- Continuous support through email and telephone

- Direct access to lead analysts

- Free analyst hour

- Free Upgrade: If an updated report published within 180 days of purchase, you will get the revised report free of charge

Datasheet Licence

- Report accessible by 1 user only

- Free 15% or 32 hours of customization

- Free post-sale service assistance

- Direct access to lead analysts

Frequently Asked Questions

How big is the Southeast Asia data center market?

What is the growth rate of the Southeast Asia data center market?

What is the estimated market size in terms of area in the Southeast Asia data center market by 2030?

What are the key trends in the Southeast Asia data center market?

How much MW of power capacity is expected to reach the Southeast Asia data center market by 2030?

What is the estimated market size in terms of area in the Southeast Asia data center market by 2030?

How big is the Southeast Asia data center market?

How much MW of power capacity is expected to reach the Southeast Asia data center market by 2030?

What are the key trends in the Southeast Asia data center market?

What is the growth rate of the Southeast Asia data center market?

How much MW of power capacity is expected to reach the Southeast Asia data center market by 2030?

What is the growth rate of the Southeast Asia data center market?

How big is the Southeast Asia data center market?

What is the estimated market size in terms of area in the Southeast Asia data center market by 2030?

What are the key trends in the Southeast Asia data center market?

Other RELATED Reports

Southeast Asia Data Center Construction Market – Industry Outlook & Forecast 2026-2031

Published : April 2026