Spain Data Center Market - Investment Analysis & Growth Opportunities 2026-2031

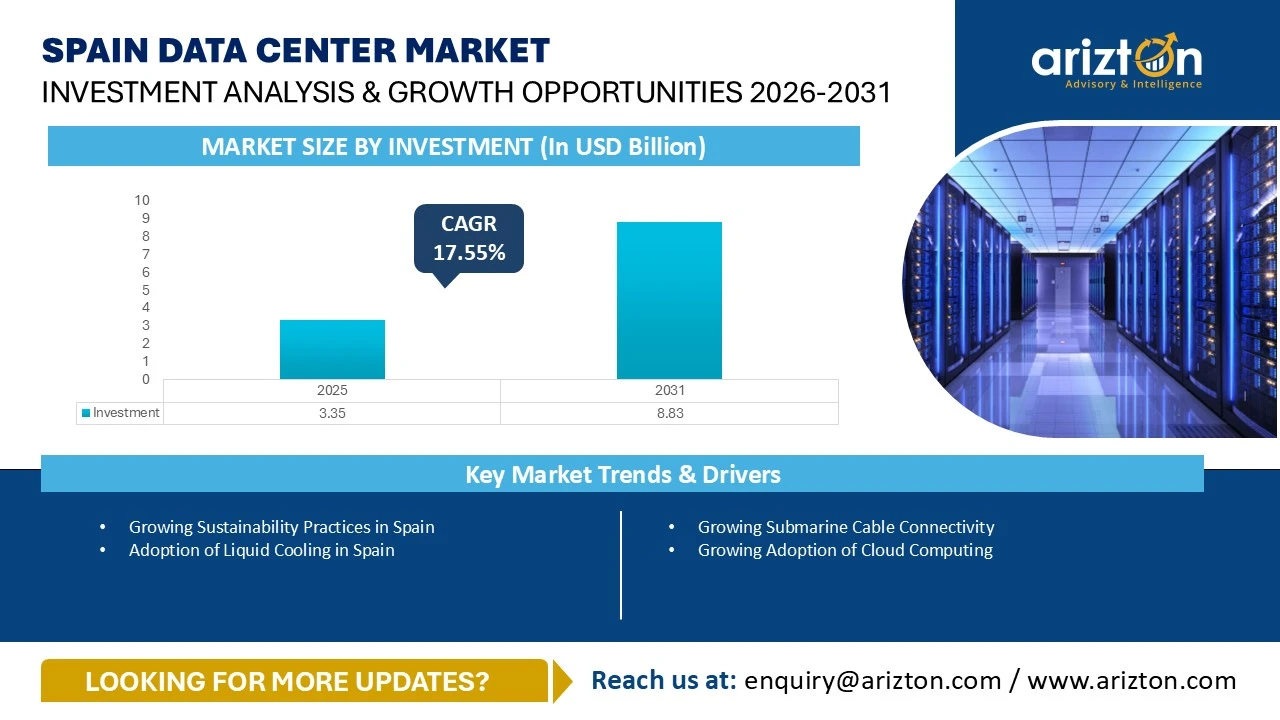

THE SPAIN DATA CENTER MARKET SIZE WAS VALUED AT USD 3.35 BILLION IN 2025 AND IS EXPECTED TO REACH USD 8.83 BILLION BY 2031, GROWING AT A CAGR OF 17.55% DURING THE FORECAST PERIOD.

127 pages

1 region

1 countries

70 company

7 segments

Purchase Options

Spain Data Center Market - Investment Analysis & Growth Opportunities 2026-2031

THE SPAIN DATA CENTER MARKET SIZE WAS VALUED AT USD 3.35 BILLION IN 2025 AND IS EXPECTED TO REACH USD 8.83 BILLION BY 2031, GROWING AT A CAGR OF 17.55% DURING THE FORECAST PERIOD.

The Spain Data Center Market Report Includes Size in Terms of

- IT Infrastructure: Servers, Storage Systems, and Network Infrastructure

- Electrical Infrastructure: UPS Systems, Generators, Transfer Switches & Switchgears, PDUs, and Other Electrical Infrastructure

- Mechanical Infrastructure: Cooling Systems, Rack Cabinets, and Other Mechanical Infrastructure

- Cooling Systems: CRAC & CRAH Units, Chiller Units, Cooling Towers, Condensers & Dry Coolers, and Other Cooling Units

- General Construction: Core & Shell Development, Installation & Commissioning Services, Engineering & Building Design, Fire Detection & Suppression Systems, Physical Security, and Data Center Infrastructure Management (DCIM)

- Tier Standard: Tier I & Tier II, Tier III, and Tier IV

- Geography: Madrid and Other Cities

Get Insights on 67 Existing Data Centers and 49 Upcoming Facilities across Spain

This report includes market data points, ranging from trend

analyses to market estimates & forecasts that you can customize

SPAIN DATA CENTER MARKET REPORT SCOPE

| REPORT ATTRIBUTE | DETAILS |

|---|---|

| MARKET SIZE (INVESTMENT) | USD 8.83 Billion (2031) |

| MARKET SIZE (AREA) | 1,610 Thousand Sq. feet (2031) |

| MARKET SIZE (POWER CAPACITY) | 421 MW (2031) |

| CAGR - INVESTMENT (2025-2031) | 17.55% |

| COLOCATION MARKET SIZE (REVENUE) | USD 2.96 Billion (2031) |

| HISTORIC YEAR | 2022-2024 |

| BASE YEAR | 2025 |

| FORECAST YEAR | 2026-2031 |

SPAIN DATA CENTER MARKET SIZE & OUTLOOK

The Spain data center market size was valued at USD 3.35 billion in 2025 and is expected to reach USD 8.83 billion by 2031, growing at a CAGR of 17.55% during the forecast period. Spain holds a significant market share of the data center market in Western Europe. It is driven by factor such as the growing adoption of digital platforms, adoption of cloud, adoptionof advanced technologies such as AI, IoT, and big data, the digital economy, expanding 5G network connectivity, increasing internet users and data traffic, government initiatives, and the rising growth in mobile and social media users: these factors are expected to significantly enhance data traffic and the demand for data centers.

Spain data center market is witnessing investment from both global as well as local data center operators. For Instance, in September 2025, Vantage Data Centers announced its plan to develop a data center campus in Villanueva de Gállego, near Zaragoza, in Aragón, Spain, with a total investment of around $3.71 billion. Additionally, the data center campus will be developed in five phases over around 10 years and it will span around 40 hectares of industrial land.

As of February 2026, the country hosts around 30 operational submarine cables such as 2Africa, Africa Coast to Europe (ACE), Alpal-2, Balalink, Canalink, DOS CONTINENTES l & ll, Est-Tet, Grace Hopper, MAREA, Penbal-5, Subcan Link 1, Tenerife-Gran Canaria, TRANSCAN-2, and West Africa Cable System (WACS). Additionally, the country continues to witness investments in around five more new submarine cables, which are expected to become operational by 2028.

In Spain we observe that data center operator are signed renewable energy Power Purchase Agreement (PPA) for its data center facility. For instance, in April 2025, nLighten announced the signing of a long-term Power Purchase Agreement (PPA) with Shell Spain to provide renewable energy for its MAD1 data center in Madrid.

SPAIN DATA CENTER MARKET - KEY HIGHLIGHTS

- In 2025, we observe that data center organizations in Spain are building high megawatt campuses to continuously increase the demand for digitalization across all sectors in Spain. Form8tion Data Centers, Nostrum Group, QTS (Blackstone), Solaria Edged Energy & Merlin Properties, Echelon Data Centres, SAMCA Group, Sierra DC, among others, are building data center campuses with capacities of more than 100 MW. These development initiatives clearly indicate that the market share of large colocation facilities is expected to grow significantly during the forecast period.

- The country is witnessing the development of an AI- ready data center across the nation. For instance, in December 2025, EdgeMode announced the securing of power for its AI-focused data center platform in Spain. Additionally, the project is being developed in a joint venture with Blackberry Alternative Investment Fund (BAIF), in partnership with Blackberry Alternative Investment Fund; it will consist of five campuses, with a combined power capacity of around 1.5 GW.

- The country is undergoing significant advancements in submarine and inland connectivity, with substantial investments. For instance, in July 2025, Google announced its plan to develop the new Sol subsea cable between Spain and the US. Additionally, the cable connects the US, Bermuda, the Azores, and Spain.

- In 2025, the Spain data center market is increasingly prioritizing sustainability, we observe that many data center operators are investing in energy-efficient infrastructure and renewable energy sources. Data centers are adopting green practices such as using solar and wind energy, implementing advanced cooling technologies and optimizing power usage effectiveness (PUE).

- In November 2025, Templus announced the initiation of the construction of a new data center facility in Ceuta, Spain. The facility will cover an area of around 26,910 square feet; it will initially offer a power capacity of 1.2 MW, with plans to expand up to 2.4 MW in a later phase. It is expected to become operational by mid-2026 and will be powered entirely by renewable energy.

WHY SHOULD YOU BUY THIS RESEARCH?

- Market size available in the investment, area, power capacity, and Spain colocation market revenue.

- An assessment of the data center investment in Spain by colocation, hyperscale, and enterprise operators.

- Data center investments in the area (square feet) and power capacity (MW) across cities in the country.

- A detailed study of the existing Spain data center market landscape, an in-depth industry analysis, and insightful predictions about the Spain data center market size during the forecast period.

- Snapshot of existing and upcoming third-party data center facilities in Spain

- Facilities Covered (Existing): 67

- Facilities Identified (Upcoming):49

- Coverage: 20+ Locations

- Existing vs. Upcoming (Data Center Area)

- Existing vs. Upcoming (IT Load Capacity)

- Data center colocation market in Spain

- Colocation Market Revenue & Forecast (2022-2031)

- Retail & Wholesale Colocation Revenue (2022-2031)

- Retail & Wholesale Colocation Pricing

- Spain data center landscape market investments are classified into IT, power, cooling, and general construction services with sizing and forecast.

- A comprehensive analysis of the latest trends, growth rate, potential opportunities, growth restraints, and prospects for the industry.

- Business overview and product offerings of prominent IT infrastructure providers, construction contractors, support infrastructure providers, and investors operating in the industry.

- A transparent research methodology and the analysis of the demand and supply aspect of the market.

SPAIN DATA CENTER MARKET VENDOR LANDSCAPE

- Some of the major colocation data center in Spain including AtlasEdge, CyrusOne, Equinix, Digital Realty, Data4, Global Switch, Iron Mountain, Merlin Properties, Nabiax, NTT DATA, and Templus.

- The cloud market in Spain is expected to continue experiencing significant growth in the forecast period. The major global cloud providers, such as Amazon Web Services (AWS), Microsoft, Google, IBM Cloud and Oracle Cloud, has dedicated cloud region in the country and company are continuing to expand their presence across the country. For instance, in March 2026, Amazon Web Services (AWS) announced its plans to expand its AI data center infrastructure in the region of Aragón, Spain. This expansion aims to support the growing demand for cloud computing and Artificial Intelligence (AI) services through the AWS cloud platform.

- The Spain data center market has the presence of several major IT infrastructure vendors including, Arista Networks, Atos, Cisco, Dell Technologies, Fujitsu, Hewlett Packard Enterprise, NVIDIA among others.

- In July 2025, Real Madrid, a professional football (soccer) club, and Cisco planned to build an AI-ready data center at the club’s Real Madrid City training campus. Additionally, Cisco will deploy 100 Gbps network infrastructure to connect the Santiago Bernabéu stadium to Real Madrid City; furthermore, the company will install Cisco Wi-Fi7 across the campus to improve speed, latency, and connectivity.

- The Spain data center market has the presence of global as well as local data center construction contractor & sub-contractors, including ACS Group, Arup, ARSMAGNA GROUP, CapIngelec, Ramboll, Ferrovial, IDOM, ISG, Hill International, Mercury, PQC, Quark Unlimited Engineering among others.

- In Spain support infrastructure companies, such as Vertiv, STULZ, and Schneider Electric, offers advanced liquid cooling solutions to data centers across Spain to support efficient heat management.

EXISTING VS. UPCOMING DATA CENTERS

- Existing Facilities in the region (Area and Power Capacity)

- Madrid

- Other Cities

- List of Upcoming Facilities in the region (Area and Power Capacity)

- Madrid

- Other Cities

REPORT COVERAGE:

This report analyses the Spain data center market share. It elaboratively analyses the existing and upcoming facilities and investments in IT, electrical, mechanical infrastructure, cooling systems, general construction, and tier standards. It discusses market sizing and investment estimation for different segments. The segmentation includes:

- IT Infrastructure

- Server Infrastructure

- Storage Infrastructure

- Network Infrastructure

- Electrical Infrastructure

- UPS Systems

- Generators

- Switches & Switchgears

- PDUs

- Other Electrical Infrastructure

- Mechanical Infrastructure

- Cooling Systems

- Rack Cabinets

- Other Mechanical Infrastructure

- Cooling Systems

- CRAC and CRAH

- Chillers

- Cooling Towers, Condensers and Dry Coolers

- Other Cooling Units

- General Construction

- Core & Shell Development

- Installation & commissioning Services

- Building & Engineering Design

- Fire Detection & Suppression Systems

- Physical Security

- Data Center Infrastructure Management (DCIM)

- Tier Standard

- Tier I & Tier II

- Tier III

- Tier IV

- Geography

- Madrid

- Other Cities

VENDOR LANDSCAPE

- IT INFRASTRUCTURE PROVIDERS: Arista Networks, Atos, Broadcom, Cisco, Dell Technologies, Fujitsu, Hewlett Packard Enterprise, IBM, Lenovo, and NVIDIA.

- DATA CENTER CONSTRUCTION CONTRACTORS & SUB-CONTRACTORS: ACS Group, AEON Engineering, Arup, ARSMAGNA GROUP, CapIngelec, Ramboll, Ferrovial, IDOM, ISG, Hill International, Mercury, PQC, and Quark Unlimited Engineering.

- SUPPORT INFRASTRUCTURE PROVIDERS: ABB, Caterpillar, Cummins, Delta Electronics, Eaton, GESAB, Legrand, Pillar Power Systems, Rittal, Rolls-Royce, Schneider Electric, STULZ, and Vertiv.

- DATA CENTER INVESTORS: Adam - Data Center, Aire, AtlasEdg, Box2bit, CyrusOne, Data4, Digital Realty, EdgeConneX, Equinix, Global Switch, Iron Mountain, Merlin Properties, Microsoft, Nabiax, NTT DATA and Templus

- NEW ENTRANTS: AQ Compute, AVAIO Digital, Best Wonder Business (BWB), DAMAC Digital, Echelon Data Centres, EdgeMode, Form8tion Data Centers, Global Technical Realty (GTR), Ingenostrum, Meta, NETHITS IT SOLUTIONS, Nostrum Group, NXN Datacenters, Panattoni, Prime Data Centers, Pure Data Centres, QTS Data Centers, Sierra DC

SNAPSHOT

The Spain data center market size is projected to reach USD 8.83 billion by 2031, growing at a CAGR of 17.55% from 2025 to 2031.

The following factors are likely to contribute to the growth of the Spain data center market

- Growing Submarine Cable Connectivity

- Growing Adoption of Cloud Computing

Base Year: 2025

Forecast Year: 2026-2031

The report considers the present scenario of the Spain data center market and its market dynamics for 2026-2031. It covers a detailed overview of several market growth enablers, restraints, and trends. The study includes the demand and supply aspects of the market.

This report also analyses the Spain data center market share. It elaborately analyses the existing and upcoming facilities and investments in IT, electrical, mechanical infrastructure, general construction, and tier standards. It discusses market sizing and investment estimation for different segments.

The segmentation includes:

- IT Infrastructure

- Servers

- Storage Systems

- Network Infrastructure

- Electrical Infrastructure

- UPS Systems

- Generators

- Transfer Switches & Switchgears

- PDUs

- Other Electrical Infrastructure

- Mechanical Infrastructure

- Cooling Systems

- Rack Cabinets

- Other Mechanical Infrastructure

- Cooling Systems

- CRAC & CRAH Units

- Chiller Units

- Cooling Towers, Condensers & Dry Coolers

- Other Cooling Units

- General Construction

- Core & Shell Development

- Installation & Commissioning Services

- Engineering & Building Design

- Fire Detection & Suppression Systems

- Physical Security

- Data Center Infrastructure Management (DCIM)

- Tier Standard

- Tier I & Tier II

- Tier III

- Tier IV

- Geography

- Madrid

- Other Cities

VENDOR LANDSCAPE

IT Infrastructure Providers

- Arista Networks

- Atos

- Broadcom

- Cisco

- Dell Technologies

- Fujitsu

- Hewlett Packard Enterprise

- IBM

- Lenovo

- NVIDIA

Data Center Construction Contractors & Sub-Contractors

- ACS Group

- AEON Engineering

- Arup

- ARSMAGNA Group

- CapIngelec

- Ramboll

- Ferrovial

- IDOM

- ISG

- Hill International

- Mercury

- PQC

- Quark Unlimited Engineering

Support Infrastructure Providers

- ABB

- Caterpillar

- Cummins

- Delta Electronics

- Eaton

- GESAB

- Legrand

- Piller Power Systems

- Rittal

- Rolls-Royce

- Schneider Electric

- STULZ

- Vertiv

Data Center Investors

- Adam - Data Center

- Aire

- AtlasEdge

- Box2Bit

- CyrusOne

- Data4

- Digital Realty

- EdgeConneX

- Equinix

- Global Switch

- Iron Mountain

- Merlin Properties

- Microsoft

- Nabiax

- NTT DATA

- Templus

New Entrants

- AQ Compute

- AVAIO Digital

- Best Wonder Business (BWB)

- DAMAC Digital

- Echelon Data Centres

- EdgeMode

- Form8tion Data Centers

- Global Technical Realty (GTR)

- Ingenostrum

- Meta

- NETHITS IT SOLUTIONS

- Nostrum Group

- NXN Datacenters

- Panattoni

- Prime Data Centers

- Pure Data Centres

- QTS Data Centers

- Sierra DC

SPAIN DATA CENTER MARKET FAQs

How big is the Spain data center market?

How much MW of power capacity will be added across Spain during 2026-2031?

What factors are driving the Spain data center market?

Which all geographies are included in Spain data center market report?

For more details, please reach us at [email protected]

1. CHAPTER 1: EXISTING & UPCOMING THIRD-PARTY DATA CENTERS IN SPAIN

• Data Center Snapshot

• Data Center Snapshot By Cities

• Existing & Upcoming Data Center Supply

• List of Upcoming Data Center Projects in Spain

2. CHAPTER 2: INVESTMENT OPPORTUNITIES IN SPAIN

• Microeconomic & Macroeconomic Factors for Spain Market

• Impact of AI in Data Center Industry in Spain

• Investment Opportunities in Spain

• Digital data in Spain

• Market Investment by Area

• Market Investment by Power Capacity

3. CHAPTER 3: DATA CENTER COLOCATION MARKET IN FRANCE

• Colocation Services Market in Spain

• Retail vs Wholesale Data Center Colocation

• Industry Demand share

• Colocation Pricing (Quarter Rack, Half Rack & Full Rack) & Add-ons

4. CHAPTER 4: MARKET DYNAMICS

• Market Enablers

• Market Trends

• Market Restraints

5. CHAPTER 5: MARKET SEGMENTATION

• IT Infrastructure: Market Size & Forecast

• Electrical Infrastructure: Market Size & Forecast

• Mechanical Infrastructure: Market Size & Forecast

• General Construction: Market Size & Forecast

• Break-up of Construction Cost

6. CHAPTER 6: TIER STANDARDS INVESTMENT

• Tier I & II

• Tier III

• Tier IV

7. CHAPTER 7: GEOGRAPHY SEGMENTATION

• Madrid

• Other Cities

8. CHAPTER 8: KEY MARKET PARTICIPANTS

• IT Infrastructure Providers

• Construction Contractors & Sub-Contractors

• Support Infrastructure Providers

• Data Center Investors

• New Entrants

9. CHAPTER 9: APPENDIX

• Market Derivation

• Site Selection Criteria

• Quantitative Summary

Select a license type that suits your business needs

Single User Licence

- Report accessible by one user only

- Free 10% or 3 days of customization

- Free post-sale service assistance

- Continuous support through email

5 User Licence

- Report accessible by 5 users within the organization

- Free 15% or 4.5 days of customization

- Continuous support through email and telephone

- Free analyst hour

- Free Upgrade: If an updated report published within 180 days of purchase, you will get the revised report free of charge

Corporate Licence

- Free Datasheet worth $1500

- Report accessible by the entire organization

- Free 20% or 6 days of customization

- Free post-sale service assistance

- Continuous support through email and telephone

- Direct access to lead analysts

- Free analyst hour

- Free Upgrade: If an updated report published within 180 days of purchase, you will get the revised report free of charge

Datasheet Licence

- Report accessible by 1 user only

- Free 15% or 32 hours of customization

- Free post-sale service assistance

- Direct access to lead analysts

Frequently Asked Questions

How big is the Spain data center market?

How much MW of power capacity will be added across Spain during 2026-2031?

What factors are driving the Spain data center market?

Which all geographies are included in Spain data center market report?

Other RELATED Reports

Germany Data Center Market - Investment Analysis & Growth Opportunities 2026-2031

Published : April 2026

UK Data Center Market - Investment Analysis & Growth Opportunities 2026-2031

Published : April 2026

Ireland Data Center Market – Investment Analysis & Growth Opportunities 2026-2031

Published : April 2026

Finland Data Center Market - Investment Analysis & Growth Opportunities 2026-2031

Published : April 2026