U.S. Data Center Market Landscape 2026-2031

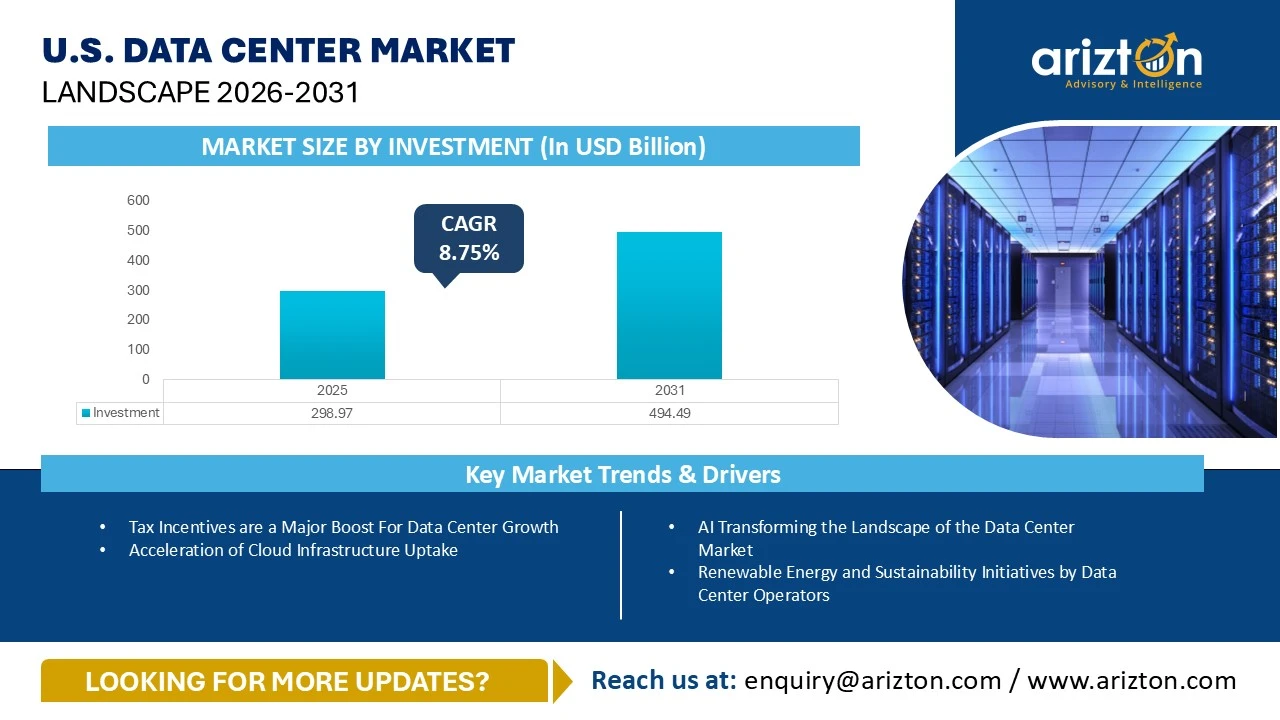

THE U.S. DATA CENTER MARKET SIZE WITNESSED INVESTMENTS OF USD 298.97 BILLION IN 2025 AND WILL WITNESS INVESTMENTS OF USD 494.49 BILLION BY 2031, GROWING AT A CAGR OF 8.75% DURING THE FORECAST PERIOD

U.S. Data Center Market Growth Insights – Market Area to Reach 52.57 Million Sq. Ft. and Power Capacity to Surpass 13,565 MW by 2031, Driven by Cloud Expansion, Edge Computing Growth, and Rising AI, Big Data & IoT Deployments Across the United States (2026–2031)

Published Date : June 2026

Last Updated : June 2026

format: PDF

edition : Fourth Edition

288 pages

region

countries

213 company

10 segments

Purchase Options

U.S. Data Center Market Landscape 2026-2031

THE U.S. DATA CENTER MARKET SIZE WITNESSED INVESTMENTS OF USD 298.97 BILLION IN 2025 AND WILL WITNESS INVESTMENTS OF USD 494.49 BILLION BY 2031, GROWING AT A CAGR OF 8.75% DURING THE FORECAST PERIOD

The U.S. Data Center Market Size, Share, & Trends Analysis By

- Facility Type: Hyperscale Data Centers, Colocation Data Centers, and Enterprise Data Centers

- Infrastructure: IT Infrastructure, Electrical Infrastructure, Mechanical Infrastructure, and General Construction

- IT Infrastructure: Server Infrastructure, Storage Infrastructure, and Network Infrastructure

- Electrical Infrastructure: UPS Systems, Generators, Transfer Switches & Switchgear, PDUs, and Other Electrical Infrastructure

- Mechanical Infrastructure: Cooling Systems, Racks, and Other Mechanical Infrastructure

- Cooling Systems: CRAC & CRAH Units, Chiller Units, Cooling Towers, Condensers, Dry Coolers, and Other Cooling Units

- Cooling Techniques: Air-based and Liquid-based

- General Construction: Core & Shell Development, Installation & Commissioning Services, Engineering & Building Design, Physical Security, Fire Detection & Suppression, and DCIM

- Tier Standard: Tier I & II, Tier III, and Tier IV

- Geography: South-Eastern U.S., South-Western U.S., Western U.S., Mid-Western U.S., and North-Eastern U.S.

Industry Analysis Report, Regional Outlook, Growth Potential, Price Trends, Competitive Market Share & Forecast 2026–2031.

This report includes market data points, ranging from trend

analyses to market estimates & forecasts that you can customize

U.S. DATA CENTER MARKET REPORT SCOPE

| REPORT ATTRIBUTE | DETAILS |

|---|---|

| MARKET SIZE – INVESTMENT (2031) | USD 494.49 Billion |

| MARKET SIZE – INVESTMENT (2025) | USD 298.97 Billion |

| CAGR - INVESTMENT (2025-2031) | 8.75% |

| MARKET SIZE - AREA (2031) | 52.57 million Square feet |

| POWER CAPACITY (2031) | 13,565 MW |

| HISTORIC YEAR | 2022- 2024 |

| BASE YEAR | 2025 |

| FORECAST YEAR | 2026-2031 |

| SEGMENTS BY | Facility Type, Infrastructure, IT Infrastructure, Electrical Infrastructure, Mechanical Infrastructure, Cooling Systems, Cooling Techniques, General Construction, Tier Standard, Geography |

| GEOGRAPHIC ANALYSIS | South-Eastern U.S., South-Western U.S., Western U.S., Mid-Western U.S., and North-Eastern U.S. |

U.S. DATA CENTER MARKET SIZE & INSIGHTS

The U.S. data center market size witnessed investments of USD 298.97 billion in 2025 and will witness investments of USD 494.49 billion by 2031, growing at a CAGR of 8.75% during the forecast period. The U.S. data center market continues to experience rapid global growth, driven by increasing cloud adoption, the expansion of edge computing, and the growing deployment of technologies such as AI, big data, and IoT.

The U.S. data center market is estimated to witness a cumulative investment of around $839 billion, excluding IT infrastructure, from 2026 to 2031; the southeastern U.S. region will contribute around $260 billion, representing around 30% of the overall share.

Investment in the U.S. data centers nearly doubled as compared with 2024, fueled by strong construction activity from both colocation and hyperscale operators. It is estimated that the demand for data centers will continue to grow as Artificial Intelligence (AI) becomes more prevalent

The cost of data center construction in the U.S. can range from $9 million to $14 million per MW, depending on the location. These elevated costs are influenced by factors such as limited land availability, high labour rates, inflation, and access to power.

The U.S. is witnessing the development of large-scale, strategic data center projects, supported by both private and public-sector stakeholders. For instance, in January 2024, the Stargate Project was announced, involving OpenAI, Oracle, SoftBank, and MGX, with reported planned investments exceeding $100 billion.

With the rising sustainability efforts across the U.S., access to renewable power for data centers is improving. In July 2025, Google signed a multi-billion-dollar hydroelectric framework agreement with Brookfield Renewable to secure up to 3 GW of firm hydro power. The initial $3 billion contracts in Pennsylvania will power its US data center expansion.

Demand for data centers remains extremely strong, particularly in primary locations such as Northern Virginia, Silicon Valley, Chicago, Dallas-Fort Worth, and Phoenix. This demand is largely driven by AI and cloud workloads. However, the supply of data centers is limited due to power constraints, land scarcity, and lengthy utility lead times. As a result, vacancy rates are near historic lows, rents are increasing, and pre-leasing activity is high. Construction is at record levels, with significant hyperscale projects transforming the industry landscape.

There is a growing trend toward regional diversification in secondary markets such as Austin, Seattle, Charlotte, Denver, and Minneapolis. However, the risks related to grid capacity, community opposition, and infrastructure bottlenecks are becoming increasingly important factors in planning and investment decisions.

U.S. DATA CENTER MARKET KEY TRENDS

AI Transforming the Landscape of the Data Center Market

- The AI industry is set to significantly increase the size of hyperscale data centers. Even though the current AI investments haven’t fully compensated for the growth in hyperscale data centers, the capacity of these data centers, especially for AI workloads, is expected to almost triple in the next five to six years. With the rising adoption of AI across several industries, new data centers are being designed to support high-density AI-based workloads.

- With the rise in the development of AI-optimized data center facilities, the adoption of GPUs in data centers is significantly increasing in the market. AI-based data centers utilize GPUs as they can perform massively parallel computations, train and run AI models dramatically faster, use power more efficiently for each AI task, support real-time AI inference, and enable high-density, scalable facilities.

- In October 2025, Lambda, The Superintelligence Cloud, is setting up a next-generation AI Factory in Kansas City, Missouri, converting a vacant facility (built in 2009) into a cutting-edge AI data center. The site will be powered by over 10,000 NVIDIA Blackwell Ultra GPUs, with plans to expand its capacity in later phases

- In 2025, Oracle plans to invest approximately $40 billion in NVIDIA's cutting-edge chips to power OpenAI's new data center in the U.S. As part of the deal, Oracle will acquire around 400,000 of NVIDIA’s top-tier GB200 chips and provide the computing capacity to OpenAI through its cloud infrastructure.

- Data centers are poised to be instrumental in the advancement and efficacy of Artificial Intelligence (AI). However, this increasing reliance presents significant challenges for data center providers. The demand for high computational performance, driven by GPUs along with specialized chips including ASICs and FPGAs, leads to a substantial requirement for energy. As the density of equipment in server racks continues to rise, the pressing issues related to power consumption and cooling will increase.

Renewable Energy and Sustainability Initiatives by Data Center Operators

- With the rapid growth in AI and cloud workloads, energy demand is increasing significantly. As a result, sustainability has become essential for managing carbon emissions, operating costs, and ensuring long-term grid stability. Data centers must prioritize sustainability, especially as local governments and residents are increasingly opposing projects that consume excessive energy, strain water resources, and contribute to higher emissions or noise levels.

- For a more sustainable approach, data center operators in the U.S. are increasingly investing in clean and renewable energy. Several companies are securing long-term power purchase agreements, building on-site solar and wind projects, as well as integrating battery storage systems to reduce carbon emissions and improve energy efficiency.

- In November 2025, TotalEnergies signed a 15-year power purchase agreement to supply Google with 1.5 TW-hours of renewable energy from its Montpelier solar farm in Ohio. The deal will support the clean energy needs of Google’s data centers in the state.

- Meta expanded its data center renewable energy investments by signing a 385 MW solar power purchase agreement in Louisiana. The company will purchase the renewable energy certificates from two utility-scale solar projects, bringing its total solar procurement in 2025 to over 3 GW

- Several data center operators have committed to becoming carbon neutral. For example, Equinix and CyrusOne have announced plans to achieve carbon neutrality by 2030, indicating that all their data center facilities will be powered by carbon-free, renewable energy. These commitments reflect the industry's response to increasing energy consumption, the investor demand for strong Environmental, Social, and Governance (ESG) performance, as well as the regulatory pressure to decarbonize before 2030.

- AI data centers are changing sustainability standards in several ways, including raising acceptable power density limits, expanding metrics beyond Power Usage Effectiveness (PUE), driving the adoption of liquid cooling, tightening expectations for water use, requiring sourcing of carbon-free energy, promoting waste heat reuse, demanding grid-friendly operations, and emphasizing the full lifecycle impact.

U.S. DATA CENTER MARKET SEGMENTATION INSIGHTS

- Server infrastructure in the U.S. data center market is a rapidly evolving segment, driven by digital transformation, increasing internet penetration, and the need for cloud services in the region.

- The electrical infrastructure is witnessing several innovations in UPS systems, generators, transfer switches & switchgears and other electrical equipment. Most data centers adopt N+1 diesel generators, providing backup fuel for up to 24 hours or more. For instance, the NVA05 campus of STACK Infrastructure, located in Northern Virginia, is equipped with an N+1 block-redundant UPS system, accounting for a minimum of 24 hours of fuel storage for operations.

- Additionally, several innovative UPS batteries such as Nickel-Zinc (NiZn) and Sodium-Ion batteries are gaining traction in the market due to their high-power density, safety, sustainability, and other factors.

- AI workloads are changing cooling standards in U.S. data centers, as traditional air cooling is insufficient to manage the heat output from GPU-dense clusters. The market is observing an increasing number of partnerships among data center operators, cooling technology vendors, chip manufacturers, and energy innovators, for instance, in November 2025, Switch and Schneider Electric signed an expanded $1.9 billion agreement, marking as the largest data center cooling contract in North America. Under the supply capacity deal, Schneider Electric will provide prefabricated power modules and its Uniflair chiller systems for Switch’s facilities, with the chillers set to be used in the U.S. for the first time.

U.S. DATA CENTER MARKET REGIONAL ANALYSIS

- The U.S. data center market is currently experiencing significant growth, driven largely by the increasing adoption of technologies, particularly Artificial Intelligence (AI).

- The South-eastern U.S., including states such as Virginia, Georgia, and North Carolina, continues to lead in data center investments, contributing over $26 billion in 2025. This is followed by the Mid-Western U.S., with investments exceeding $23 billion in the same year, while the North-Eastern U.S. region accounted for approximately $3 billion

- Northern Virginia is recognized as the data center capital of the world, often referred to as an alley of data centers. It continues to be the largest data center market, boasting over 4 gigawatts (GW) of core and shell colocation capacity along with more than 3 GW of hyperscale self-built capacity. This market is increasingly becoming a prime location for large contiguous capacities and hyperscale campuses, with growing competition and intensifying pricing pressures.

- Atlanta, Georgia, has emerged as a preferred location in recent times, attracting investments from all four major hyperscalers: Meta, Microsoft, Google, and AWS. This trend is driven by the industry’s demand for ample land, fiber optic infrastructure, power, and water.

- The state of Texas as well as cities including Dallas, Austin, and San Antonio, have gained prominence as key locations for data center development in the US. The availability of land, lower utility costs, and a favorable business climate have made these locations an attractive choice for companies looking to establish or expand their data center operations. Austin is considered one of the fastest-growing data center markets in terms of secondary markets. It has emerged as a strategic digital infrastructure hub within the Texas Triangle, which includes Dallas-Fort Worth, Houston, Austin, and San Antonio.

U.S. DATA CENTER MARKET VENDOR LANDSCAPE

- The U.S. data center market has the presence of key investors such as CyrusOne, DataBank, Digital Realty, Equinix, NTT DATA, EdgeConneX, Aligned Data Centers, H5 Data Centers, HostDime, Hut 8, Iron Mountain, QTS Realty Trust, Sabey Data Centers, Skybox Datacenters, STACK Infrastructure, Stream Data Centers, Switch, T5 Data Centers, TierPoint, Vantage Data Centers and others.

- In June 2025, EdgeCore Digital Infrastructure, a data center provider based in Denver, announced plans to invest $17 billion in the construction of a 1.1 GW data center facility in Virginia. The campus, spread across an area of 3.9 million square feet, will be developed on 697 acres within the Shannon Hill Regional Business Park in Louisa County. Upon completion, it will become EdgeCore’s third data center campus in Virginia

- In May 2025, NTT DATA announced a major expansion, delivering over 370 MW of new capacity, launching 10 new data centers, and enabling more than 200 MW of AI workloads. Once online, the company will position it as the world’s third-largest data center provider. As AI transforms infrastructure requirements, the company continues to lead in innovation by deploying advanced liquid cooling systems and designing facilities specifically for high-density AI workloads. NTT DATA is rapidly scaling its operations to meet the growing demand for AI-optimized, sustainable infrastructure across North America, Europe, and Asia

- New Entrants include Ada Infrastructure, CloudHQ, Beale Infrastructure, CloudBurst Data Centers, CleanArc Data Centers, Edged Energy, Fleet Data Centers, NE Edge, Penzance, Prometheus Hyperscale, Quantum Loophole, Rowan Digital Infrastructure, Related Digital, Tract and several others.

- In October 2025, Related Digital began construction on a $1.2 billion data center campus within the 900-acre Cheyenne Business Parkway in Wyoming. The 115-acre development is planned to support up to 302 MW of IT capacity at full buildout, with the first phase comprising a 184,000-square-foot building on 36 acres; it is scheduled for completion in late 2026.

- Major hyperscale operators are leading this investment surge, announcing significant funding for the development of new data centers across the U.S. over the next three to four years. For instance, in November 2025, Google, as part of a broader $9 billion investment in Oklahoma, announced plans to develop two new data center campuses in Muskogee County. AWS is set to develop two data centers in Madison County, Mississippi, with a total investment of $10 billion. The project, expected to generate around 1,000 construction jobs, is scheduled for completion by 2027.

- In September 2025, Microsoft announced plans for a second large-scale AI data center in Wisconsin, increasing its total investment in the state to more than $7 billion. The newly planned $4 billion facility will be developed alongside the company’s existing $3.3 billion data center in Mount Pleasant in south-eastern Wisconsin.

SNAPSHOT

The U.S. data center construction market size by investment will reach USD 494.49 billion by 2031, growing at a CAGR of 8.75% from 2025 to 2031.

The following factors are likely to contribute to the growth of the U.S. data center construction market during the forecast period:

- Tax Incentives are a Major Boost for Data Center Growth

- M&A and Joint Ventures Enabling Data Center Growth

- Enhanced Connectivity Through Submarine Cables Driving Growth in Data Center Market

- Acceleration of Cloud Infrastructure Uptake

Base Year: 2025

Forecast Year: 2026-2031

The study considers the present scenario of the U.S. data center construction market and its market dynamics for 2026−2031. It covers a detailed overview of several market growth enablers, restraints, and trends. The report offers both the demand and supply aspects of the market. It profiles and examines leading companies and other prominent ones operating in the market.

Segmentation by Facility Type

- Hyperscale Data Centers

- Colocation Data Centers

- Enterprise Data Centers

Segmentation by Infrastructure

- IT Infrastructure

- Electrical Infrastructure

- Mechanical Infrastructure

- General Construction

Segmentation by IT Infrastructure

- Server Infrastructure

- Storage Infrastructure

- Network Infrastructure

Segmentation by Electrical Infrastructure

- UPS Systems

- Generators

- Transfer Switches & Switchgear

- PDUs

- Other Electrical Infrastructure

Segmentation by Mechanical Infrastructure

- Cooling Systems

- Racks

- Other Mechanical Infrastructure

Segmentation by Cooling Systems

- CRAC & CRAH Units

- Chiller Units

- Cooling Towers, Condensers, and Dry Coolers

- Other Cooling Units

Segmentation by Cooling Techniques

- Air-based

- Liquid-based

Segmentation by General Construction

- Core & Shell Development

- Installation & Commissioning Services

- Engineering & Building Design

- Physical Security

- Fire Detection & Suppression

- DCIM

Segmentation by Tier Standard

- Tier I & II

- Tier III

- Tier IV

Segmentation by Geography

- The U.S.

- South-Eastern U.S.

- South-Western U.S.

- Western U.S.

- Mid-Western U.S.

- North-Eastern U.S.

Key Data Center It Infrastructure Providers

- Arista Networks

- Atos

- Broadcom

- Cisco Systems

- DataDirect Networks (DDN)

- Dell Technologies

- Extreme Networks

- Fujitsu

- Hewlett Packard Enterprise

- Hitachi Vantara

- IBM

- Infortrend Technology

- Inspur

- Intel

- Lenovo

- Micron Technology

- MiTAC Holdings

- NetApp

- Nimbus Data

- NVIDIA

- Oracle

- Pure Storage

- Quanta Cloud Technology

- QNAP Systems

- Quantum

- Seagate Technology

- Silk

- Super Micro Computer

- Synology

- Toshiba

- Western Digital

- Wiwynn

- Hon Hai Technology Group (Foxconn)

Key Data Center Support Infrastructure Providers

- ABB

- Caterpillar

- Cummins

- Delta Electronics

- Eaton

- Legrand

- Rolls-Royce

- Schneider Electric

- STULZ

- Vertiv

Other Data Center Support Infrastructure Providers

- Airedale

- Alfa Laval

- Asetek

- Bloom Energy

- Carrier

- Condair

- Cormant

- Cyber Power Systems

- Enlogic

- FNT Software

- Generac Power Systems

- Green Revolution Cooling (GRC)

- HITEC Power Protection

- Johnson Controls

- KOHLER (Rehlko)

- KyotoCooling

- Mitsubishi Electric

- Natron Energy

- NetZoom

- Nlyte Software

- Rittal

- Siemens

- Trane

- ZincFive,

- HIMOINSA (Yanmar)

Key Data Center Contractors & Subcontractors

- AECOM

- Ames Construction

- Arup

- Barge Design Solutions

- Burns & McDonnell

- Corgan

- DPR Construction

- Fortis Construction

- Haydon

- Holder Construction

- Jacobs

- KDC

- Kiewit Corporation

- Lewis Michael Consultants

- Morgan Construction

- Morgan Corp

- Page

- Rogers-O’Brien Construction

- Rosendin Electric

- Syska Hennessy Group

- Turner Construction

Other Data Center Contractors & Subcontractors

- AlfaTech

- Aplena

- Black & Veatch

- BlueScope Construction

- Brasfield & Gorrie

- CallisonRTKL

- Clark Construction Group

- Clayco

- Climatec

- Clune Construction

- EMCOR Group

- EYP MCF

- Fitzpatrick Architects

- Fluor Corporation

- Gensler

- Gilbane Building Company

- Gray

- HDR

- Hensel Phelps

- HITT Contracting

- Hoffman Construction

- JE Dunn Construction

- JHET Architects

- JTM Construction Group

- kW Engineering

- Linesight,

- M+W Group (Exyte)

- McCarthy Building Companies

- Morrison Hershfield

- Mortenson

- Pepper Construction

- Rosendin

- Ryan Companies

- Salute Mission Critical

- Sheehan Nagle Hartray Architects

- Skanska

- Southland Industries

- Sturgeon Electric Company

- Structure Tone

- Suffolk Construction

- STO Building Group

- Sundt Construction

- The Mulhern Group

- The Walsh Group

- The Weitz Company

- The Whiting-Turner Contracting Company

- TRINITY Group Construction

- Walbridge

- WSP

Key Data Center Investors

- Apple

- Applied Digital

- AWS

- CyrusOne

- DataBank

- Digital Realty

- Equinix

- Meta (Facebook)

- Microsoft

- NTT DATA

- Vantage Data Centers

Other Data Center Investors

- AAIM Data Centers

- Aligned Data Centers

- American Tower

- AUBix

- Centersquare

- CloudHQ

- Cologix

- Compass Datacenters

- COPT Data Center Solutions

- Centra

- Crusoe

- Core Scientific

- DartPoints

- DC BLOX

- DigiPower X

- EdgeConneX

- EdgeCore Digital Infrastructure

- Element Critical

- Flexential

- fifteenfortyseven Critical Systems Realty (1547)

- H5 Data Centers

- HostDime

- Hut 8

- Iron Mountain

- Netrality Data Centers

- Novva Data Centers

- PhoenixNAP

- PowerHouse Data Centers

- Prime Data Centers

- QTS Realty Trust

- Sabey Data Centers

- Skybox Datacenters

- Stream Data Centers,

- STACK Infrastructure

- Switch

- T5 Data Centers

- TierPoint

- WhiteFiber

- Yondr

- 365 Data Centers

- 5C Data Centers

New Entrants

- Ardent Data Centers

- Ada Infrastructure

- Beale Infrastructure

- Big Sky Digital Infrastructure

- CleanArc Data Centers

- Colovore

- CloudBurst Data Centers,

- Crane Data Centers

- Edged Energy

- Fleet Data Centers

- LightHouse Data Centers

- Lambda

- Metrobloks

- NE Edge

- Penzance

- Prometheus Hyperscale

- Quantum Loophole

- RadiusDC

- Related Digital

- Rowan Digital Infrastructure

- Sailfish Investors

- Tract

US DATA CENTER MARKET FAQs

How big is the U.S. data center market?

What is the growth rate of the U.S. data center market?

What are the key trends in the U.S. data center market?

What is the estimated market size in terms of area in the U.S. data center market by 2030?

What is the estimated market size in terms of area in the U.S. data center market by 2030?

For more details, please reach us at [email protected]

For more details, please reach us at [email protected]

Select a license type that suits your business needs

Single User Licence

- Report accessible by one user only

- Free 10% or 3 days of customization

- Free post-sale service assistance

- Continuous support through email

5 User Licence

- Report accessible by 5 users within the organization

- Free 15% or 4.5 days of customization

- Continuous support through email and telephone

- Free analyst hour

- Free Upgrade: If an updated report published within 180 days of purchase, you will get the revised report free of charge

Corporate Licence

- Free Datasheet worth $1500

- Report accessible by the entire organization

- Free 20% or 6 days of customization

- Free post-sale service assistance

- Continuous support through email and telephone

- Direct access to lead analysts

- Free analyst hour

- Free Upgrade: If an updated report published within 180 days of purchase, you will get the revised report free of charge

Datasheet Licence

- Report accessible by 1 user only

- Free 15% or 32 hours of customization

- Free post-sale service assistance

- Direct access to lead analysts

Frequently Asked Questions

How big is the U.S. data center market?

What is the growth rate of the U.S. data center market?

What are the key trends in the U.S. data center market?

What is the estimated market size in terms of area in the U.S. data center market by 2030?

What is the estimated market size in terms of area in the U.S. data center market by 2030?

Other RELATED Reports

U.S. Data Center Colocation Market - Industry Outlook & Forecast 2025-2030

Published : August 2025

U.S. Data Center Construction Market - Industry Outlook & Forecast 2025-2030

Published : May 2025