Global Wall Panel Market Research Report 2026-2031

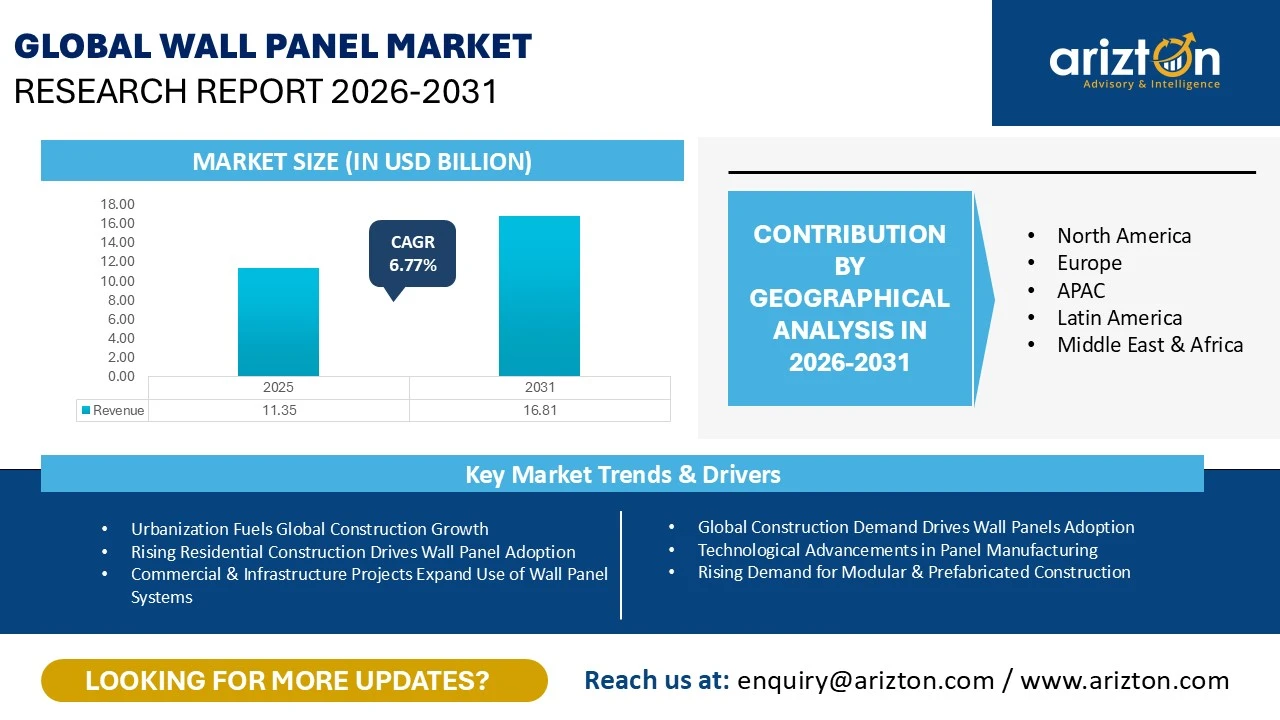

THE GLOBAL WALL PANEL MARKET WAS VALUED AT USD 11.35 BILLION IN 2025 AND IS EXPECTED TO REACH USD 16.81 BILLION BY 2031, GROWING AT A CAGR OF 6.77% DURING THE FORECAST PERIOD.

251 pages

5 region

28 countries

30 company

9 segments

Purchase Options

Global Wall Panel Market Research Report 2026-2031

THE GLOBAL WALL PANEL MARKET WAS VALUED AT USD 11.35 BILLION IN 2025 AND IS EXPECTED TO REACH USD 16.81 BILLION BY 2031, GROWING AT A CAGR OF 6.77% DURING THE FORECAST PERIOD.

The Wall Panel Market Size, Share, & Trends Analysis Report By

- Product Type: Interior Wall Panels and Exterior Wall Panels

- Material Type: Plastic, Wood, Metal, Gypsum, and Others

- Plastic: PVC wall panels, Polystyrene panels, WPC Panels, Acrylic Wall Panels, and Others

- Wood: MDF / HDF Panels, Plywood Panels, Solid Wood Panels, and Others

- Metal: Aluminum Panels, Steel Panels, and Others

- Panel Type: Insulated Wall Panels, Non-insulated Wall Panels, Structural Wall Panels, Non-structural Wall Panels, and Others

- End-Users: Residential, Commercial, and Industrial

- Commercial: Corporate Buildings, Retail Spaces, Hotels & Restaurants, Healthcare, Educational Institutions, and Others

- Geography: North America, Europe, APAC, Latin America, and Middle East & Africa

Industry Analysis Report, Regional Outlook, Growth Potential, Price Trends, Competitive Market Share & Forecast 2026–2031.

This report includes market data points, ranging from trend

analyses to market estimates & forecasts that you can customize

WALL PANEL MARKET REPORT SCOPE

| REPORT ATTRIBUTE | DETAILS |

|---|---|

| MARKET SIZE (2031) | USD 16.81 Billion |

| MARKET SIZE (2025) | USD 11.35 Billion |

| CAGR (2025-2031) | 6.77% |

| HISTORIC YEAR | 2022-2024 |

| BASE YEAR | 2025 |

| FORECAST YEAR | 2026-2031 |

| SEGMENTS BY | Product Type, Material Type, Panel Type, End-Users, and Geography |

| GEOGRAPHIC ANALYSIS | North America, Europe, APAC, Latin America, and Middle East & Africa |

| KEY PLAYERS | Kingspan Group, Saint-Gobain, Armstrong World Industries, USG Corporation, Knauf Group, CRH plc, Nichiha Corporation, and LIXIL Group Corporation |

WALL PANEL MARKET SIZE & SHARE

The global wall panel market size was valued at USD 11.35 billion in 2025 and is projected to reach USD 16.81 billion by 2031. This expansion represents a steady wall panels market growth at a CAGR of 6.77% over the forecast period.

As a critical segment of the broader building materials and construction ecosystem, the wall panels industry focuses on the design, manufacturing, and integration of engineered wall panel systems, modular panels, and advanced surface solutions. These innovations are utilized across residential, commercial, industrial, and institutional infrastructure.

In this technical domain, structural integrity, fire resistance, thermal performance, moisture protection, and long-term durability are paramount. Comprehensive wall panels industry analysis indicates that even minor deficiencies in panel strength, insulation quality, or fire ratings can significantly compromise building safety, operational costs, regulatory compliance, and asset lifespans.

Unlike traditional on-site construction, modern wall panel systems must comply with stringent local building codes, fire safety norms, energy efficiency standards, and sustainability certifications (such as LEED, BREEAM, and green building frameworks) while ensuring scalability and compatibility with prefabricated construction methods.

WALL PANEL MARKET TRENDS & DRIVERS

Urbanization and Infrastructure Expansion

According to current wall panels market trends, global urbanization is a primary catalyst for industry expansion. Over 55% of the global population lived in urban areas in 2024, a figure climbing steadily toward 58% by 2026. Rapid urban migration is particularly pronounced in the Asia-Pacific, Africa, and Latin America.

This population shift creates an immediate need for new housing units, apartments, and condominiums that require modern wall panels for interiors, partitioning, insulation, and aesthetic finishes. Furthermore, urban expansion fuels demand for commercial spaces, where panels provide modular partitioning, acoustic treatment, and fire resistance.

Sustainable and Prefabricated Construction

The wall panels market forecast is heavily influenced by a global shift toward sustainable, rapid-assembly construction. Green building standards and the necessity for accelerated project timelines favor the adoption of recyclable, modular, and multifunctional panels.

- North America: Modular, eco-friendly panels have become a standard specification for commercial projects and large-scale residential developments.

- Asia-Pacific: High-rise developments in Shanghai and affordable housing initiatives in Bangalore increasingly deploy modular, moisture-resistant panels to optimize construction speed.

- Global Impact: From dense urban renovations in New York City to mixed-use developments in Ho Chi Minh City, global construction demand directly drives the integration of high-performance wall panels to meet evolving energy codes and safety regulations.

WALL PANEL MARKET SEGMENTATION INSIGHTS

Product Type: Interior vs. Exterior Solutions

The global market is bifurcated into interior and exterior applications, with interior wall panels commanding the dominant market share at approximately 63%.

The massive footprint of the interior segment is propelled by widespread deployment across commercial offices, hospitality, healthcare, education, retail, and residential renovation projects. In these environments, design flexibility, acoustic performance, fire safety, and aesthetics are non-negotiable requirements.

Modern interior panel systems, including acoustic, decorative, PVC, wood, metal, and modular partition variations, have evolved from simple building materials into highly functional architecture solutions. Today, they serve a strategic role in sound management, space optimization, wellness-focused design, and brand-driven commercial aesthetics.

Material Type: Plastic, Wood, and Metal Dynamics

The choice of raw materials is heavily dictated by performance demands, environmental exposure, and lifecycle costs:

- The Plastic Segment (Highest Growth): Emerging as the fastest-growing category, this segment is expanding at a CAGR of 8.41%. Widespread adoption of PVC, WPC, polystyrene, acrylic, and PET panels spans residential, commercial, and institutional sectors where moisture resistance and rapid installation are vital.

- The PVC Dominance: Within plastics, PVC wall panels capture the largest market share. They offer an ideal equilibrium of affordability, durability, and hygiene, making them a staple in high-humidity or sterile environments such as bathrooms, kitchens, and hospitals. Compared to alternative composites, PVC delivers superior resistance to water, mold, and surface impact at a lower lifecycle cost.

- The Wood Segment (MDF/HDF Focus): Medium-Density Fiberboard (MDF) and High-Density Fiberboard (HDF) panels dominate this category. Chosen for their excellent surface finish quality and dimensional stability, they are cheaper and easier to machine into complex designs than solid wood or plywood. These materials act as critical enablers for premium, sustainable interior systems in corporate offices, retail spaces, and large-scale housing projects.

- The Metal Segment (Aluminum Cladding): Aluminum leads the metal space due to its high strength-to-weight ratio, structural resilience, and modern aesthetic. Highly favored for high-rise facades, airports, malls, and public infrastructure, aluminum panels are completely non-combustible, corrosion-resistant, and immune to pest or fungal damage, rendering them ideal for demanding coastal or high-risk urban environments.

Panel Type: Insulated Wall Systems

Insulated wall panels held the largest overall share of the market in 2025. This leading position is a direct result of their critical role in advancing energy efficiency, thermal performance, and green building metrics.

Industrial, logistics, cold storage, and data center developments heavily rely on these systems for precision temperature control. Driven by rising energy costs and global net-zero building regulations, prefabricated insulated panels offer an airtight, fire-resistant solution that drastically slashes on-site construction timelines compared to non-insulated alternatives.

End-User Profiles: Commercial and Corporate Drivers

The commercial sector stands out as a high-value, specification-driven segment where purchasing decisions are tightly bound to strict regulatory compliance, fire safety, acoustics, and lifecycle efficiency. Commercial construction demands advanced panel systems to support fast-track project delivery and maintain design consistency across large footprints.

Within the commercial arena, corporate buildings represent the primary demand driver. This sub-segment’s dominance is sustained by:

- Continuous global investments in Class-A office construction and corporate real estate.

- The rise of hybrid workspaces and smart offices requires frequent layout reconfigurations via modular partition walls.

- An industry-wide focus on ESG-driven (Environmental, Social, and Governance) retrofits and wellness-centric interior designs that prioritize employee comfort through acoustic paneling and aesthetic enhancement.

WALL PANEL MARKET GEOGRAPHICAL ANALYSIS

Europe: The Dominant Market Leader

Europe commands the largest geographic footprint in the global wall panel industry, accounting for over 35% of the total market share. The region's market dominance is underpinned by an aggressive regulatory push toward decarbonization, widespread building retrofits, and an established culture of sustainable building practices.

- Germany: Serving as the primary engine for continental Europe, Germany's market is propelled by rigid national energy codes and a mature prefabricated construction ecosystem. This has created a massive demand for high-performance, fire-rated, and insulated panels across commercial and industrial developments.

- United Kingdom: The UK stands as another major regional powerhouse, with growth primarily sustained by large-scale commercial retrofits, public sector infrastructure upgrades, and a steady demand for decorative and acoustic panel systems within healthcare and educational facilities.

Asia-Pacific (APAC): The Fastest-Growing Region

The Asia-Pacific region is emerging as the primary growth engine for the wall panel industry, driven by rapid macroeconomic shifts and a massive demographic transition.

Key nations leading this adoption include China, India, Japan, South Korea, Australia, and Singapore. Across these countries, the market is fueled by massive infrastructure investments, high-density residential housing projects, commercial real estate developments, and the rise of smart city initiatives.

To combat mounting labor shortages and meet tight project deadlines, developers across APAC are actively replacing traditional brick-and-mortar masonry with high-performance, prefabricated, and insulated wall panels that deliver quick installation times and superior energy efficiency.

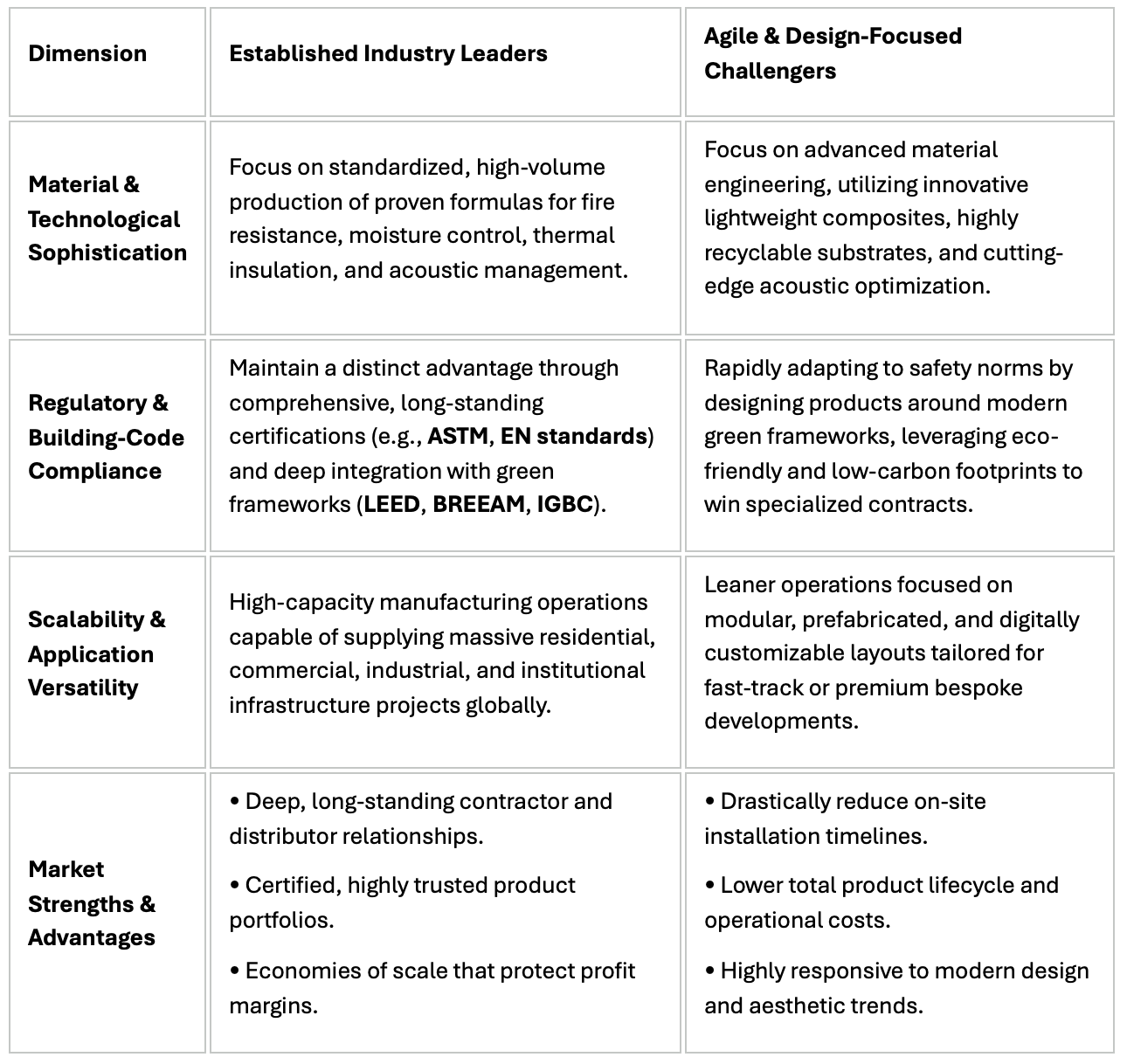

COMPETITIVE LANDSCAPE

Wall Panel Market Competitive Landscape

The global wall panel market is undergoing a profound structural transformation. This evolution is driven by the convergence of sustainable building practices, advanced material engineering, modular systems, and digital design technologies. Today, traditional manufacturers and innovation-driven startups alike are reshaping the industry by integrating lightweight composites, fire-resistant cores, acoustic optimization, and rapid-installation systems into their product portfolios.

The table below breaks down the core dimensions shaping market competition and outlines how established leaders compare against agile industry challengers.

Market Dynamics & Competitive Profiles

SNAPSHOT

The global wall panel market size is expected to grow at a CAGR of approximately 6.77% from 2025 to 2031.

The following factors are likely to contribute to the growth of the global wall panel market during the forecast period:

- Technological Advancements in Panel Manufacturing

- Global Construction Demand Drives Wall Panels Adoption

- Rising Demand for Modular & Prefabricated Construction

- Regulatory Support for Fire, Acoustic, and Thermal Performance

Base Year: 2025

Forecast Year: 2026-2031

The report examines the current state of the global wall panel market and its market dynamics through 2026−2031. It covers a detailed overview of several market growth enablers, restraints, and trends. The study covers both the demand and supply sides of the market. It also profiles and analyses leading companies and several other prominent companies operating in the market.

Key Company Profiles

- Kingspan Group

- Business Overview

- Product Offerings

- Key Developments

- Key Strategies

- Key Strengths

- Key Opportunities

- Saint-Gobain

- Armstrong World Industries

- USG Corporation

- Knauf Group

- CRH plc

- Nichiha Corporation

- LIXIL Group Corporation

Other Prominent Company Profiles

- USG Boral Limited

- Business Overview

- Product Offerings

- Jotun A/S

- Etex Group

- Greenlam Industries

- Euroacoustic

- Hunter Douglas

- Ideatec

- Caimi

- Plexwood

- Arper

- Casalis

- Offecct

- Vicoustic

- Celenit

- Fabcon Precast

- Builders Firstsource

- PacificPanel

- RedBuilt

- Arktura

- The Raymond Group

- UsiHome

- KoreaPuff

Segmentation by Product Type

- Interior Wall Panels

- Exterior Wall Panels

Segmentation by Material Type

- Plastic

- Wood

- Metal

- Gypsum

- Others

Segmentation by Plastic

- PVC wall panels

- Polystyrene panels

- WPC Panels

- Acrylic Wall Panels

- Others

Segmentation by Wood

- MDF / HDF Panels

- Plywood Panels

- Solid Wood Panels

- Others

Segmentation by Metal

- Aluminum Panels

- Steel Panels

- Others

Segmentation by Panel Type

- Insulated Wall Panels

- Non-insulated Wall Panels

- Structural Wall Panels

- Non-structural Wall Panels

- Others

Segmentation by End-Users

- Residential

- Commercial

- Industrial

Segmentation by Commercial

- Corporate Buildings

- Retail Spaces

- Hotels & Restaurants

- Healthcare

- Educational Institutions

- Others

Segmentation by Geography

- Europe

- Germany

- UK

- France

- Italy

- Spain

- Netherlands

- Sweden

- Switzerland

- Denmark

- Russia

- Rest of Europe

- North America

- U.S.

- Canada

- APAC

- China

- India

- Japan

- South Korea

- Australia

- Thailand

- Singapore

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Argentina

- Colombia

- Chile

- Rest of Latin America

- Middle East & Africa

- Saudi Arabia

- UAE

- South Africa

- Egypt

- Rest of MEA

WALL PANEL MARKET FAQs

What are the key trends in the global wall panel market?

How big is the global wall panel market?

What is the growth rate of the global wall panel market?

Which region dominates the global wall panel market?

Who are the major players in the global wall panel market?

For more details, please reach us at [email protected]

1. Scope & Coverage

- Market Definition

- Inclusions

- Exclusions

- Market Estimation Caveats

- Market Size & Forecast Periods

- Historic Period: 2022-2024

- Base Year: 2025

- Forecast Period: 2026-2031

- Market Size (2022-2031)

- Revenue

- Market Segments

- Market Segmentation by Product Type

- Market Segmentation by Material Type

- Market Segmentation by Plastic

- Market Segmentation by Wood

- Market Segmentation by Metal

- Market Segmentation by Panel Type

- Market Segmentation by End-Users

- Market Segmentation by Commercial

2. Opportunity Pockets

3. Introduction

- Major Factors Driving Growth in The Wall Panel Market

- Recent Developments in the Wall Pannel Industry

- Role Of Wall Panels in The Global Construction Ecosystem

- Technology Integration & Smart Features the Global Wall Panel Market

- Dominant Segments in The Global Wall Panel Market

- Parameters Impacting Market Growth

4. Market Opportunities & Trends

- Urbanization Fuels Global Construction Growth

- Rising Residential Construction Drives Wall Panel Adoption

- Commercial & Infrastructure Projects Expand Use of Wall Panel Systems

- Sustainability & Green Building Codes Increase Preference for Wall Panels

5. Market Growth Enablers

- Global Construction Demand Drives Wall Panels Adoption

- Technological Advancements in Panel Manufacturing

- Rising Demand for Modular & Prefabricated Construction

- Regulatory Support for Fire, Acoustic, and Thermal Performance

6. Market Restraints

- High Initial Material and Installation Costs

- Limited Awareness in Price-Sensitive and Rural Markets

- Dependence on Construction Cycles

- Complex Compliance and Certification Requirements

7. Market Landscape

8. Five Forces Analysis

9. Product Type Covered: (Market Size & Forecast: 2022-2031)

- Interior Wall Panels

- Exterior Wall Panels

10. Material Type Covered: (Market Size & Forecast: 2022-2031)

- Plastic

- Wood

- Metal

- Gypsum

- Others

11. Plastic Covered: (Market Size & Forecast: 2022-2031)

- PVC wall panels

- Polystyrene panels

- WPC Panels

- Acrylic Wall Panels

- Others

12. Wood Covered: (Market Size & Forecast: 2022-2031)

- MDF / HDF Panels

- Plywood Panels

- Solid Wood Panels

- Others

13. Metal Covered: (Market Size & Forecast: 2022-2031)

- Aluminum Panels

- Steel Panels

- Others

14. Panel Type Covered: (Market Size & Forecast: 2022-2031)

- Insulated Wall Panels

- Non-insulated Wall Panels

- Structural Wall Panels

- Non-structural Wall Panels

- Others

15. End-users Covered: (Market Size & Forecast: 2022-2031)

- Residential

- Commercial

- Industrial

16. Commercial Covered: (Market Size & Forecast: 2022-2031)

- Corporate Buildings

- Retail Spaces

- Hotels & Restaurants

- Healthcare

- Educational Institutions

- Others

17. Geography (Market Size & Forecast: 2022-2031)

Regional Analysis within North America

- US

- CANADA

Regional Analysis within Europe

- Germany

- UK

- France

- Italy

- Spain

- Netherlands

- Sweden

- Switzerland

- Denmark

- Russia

- RoEurope

Regional Analysis within APAC

- China

- India

- Japan

- South Korea

- Australia

- Thailand

- Singapore

- RoAPAC

Regional Analysis within Latin America

- Brazil

- Mexico

- Argentina

- Colombia

- Chile

- RoLA

Regional Analysis within Middle East Africa

- Saudi Arabia

- UAE

- South Africa

- Egypt

- RoMEA

18. Competitive Landscape

19. Competitive Overview

- Key Developments

20. Key Company Profiles

- KINGSPAN GROUP

- SAINT-GOBAIN

- ARMSTRONG WORLD INDUSTRIES

- USG CORPORATION

- KNAUF GROUP

- CRH plc

- NICHIHA CORPORATION

- LIXIL GROUP CORPORATION

21. Other Prominent Company Profiles

- USG BORAL LIMITED

- JOTUN A/S

- ETEX GROUP

- GREENLAM INDUSTRIES

- EUROACOUSTIC

- HUNTER DOUGLAS

- IDEATEC

- CAIMI

- PLEXWOOD

- ARPER

- CASALIS

- OFFECCT

- VICOUSTIC

- CELENIT

- FABCON PRECAST

- BUILDERS FIRSTSOURCE

- PACIFICPANEL

- REDBUILT

- ARKTURA

- THE RAYMOND GROUP

- USIHOME

- KOREAPUFF

20. Report Summary

- Key Takeaways

- Strategic Recommendations

Select a license type that suits your business needs

Single User Licence

- Report accessible by one user only

- Free 10% or 3 days of customization

- Free post-sale service assistance

- Continuous support through email

5 User Licence

- Report accessible by 5 users within the organization

- Free 15% or 4.5 days of customization

- Continuous support through email and telephone

- Free analyst hour

- Free Upgrade: If an updated report published within 180 days of purchase, you will get the revised report free of charge

Corporate Licence

- Free Datasheet worth $1500

- Report accessible by the entire organization

- Free 20% or 6 days of customization

- Free post-sale service assistance

- Continuous support through email and telephone

- Direct access to lead analysts

- Free analyst hour

- Free Upgrade: If an updated report published within 180 days of purchase, you will get the revised report free of charge

Datasheet Licence

- Report accessible by 1 user only

- Free 15% or 32 hours of customization

- Free post-sale service assistance

- Direct access to lead analysts

Frequently Asked Questions

What are the key trends in the global wall panel market?

How big is the global wall panel market?

What is the growth rate of the global wall panel market?

Which region dominates the global wall panel market?

Who are the major players in the global wall panel market?

Other RELATED Reports