Global Yacht Market Research Report 2025-2030

THE GLOBAL YACHT MARKET WAS VALUED AT USD 11.6 BILLION IN 2024 AND IS PROJECTED TO REACH USD 17.06 BILLION BY 2030, GROWING AT A CAGR OF 6.65% DURING THE FORECAST PERIOD.

The Yacht Market Size, Share & Trends By Type, By Motorized Yacht, By Application, By Size, By Hull Type, & By Geography. The Industry Analysis Includes Market Size and Value (in USD Billions) for the Listed Segments, With Data Spanning 10 Years.

Published Date : September 2025

Last Updated : September 2025

format: PDF

edition : Second Edition

161 pages

7 tables

49 charts

45 company

6 segments

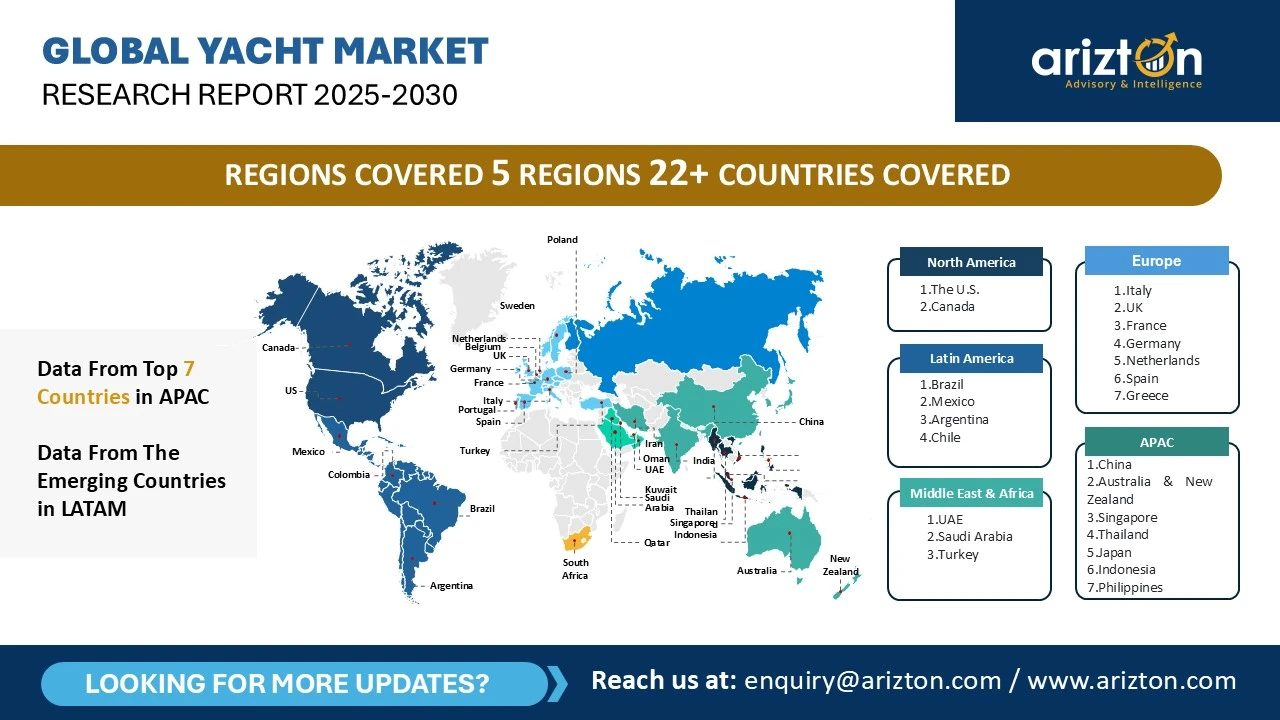

5 region

23 countries

Purchase Options

Global Yacht Market Research Report 2025-2030

THE GLOBAL YACHT MARKET WAS VALUED AT USD 11.6 BILLION IN 2024 AND IS PROJECTED TO REACH USD 17.06 BILLION BY 2030, GROWING AT A CAGR OF 6.65% DURING THE FORECAST PERIOD.

The Yacht Market Size, Share & Trend Analysis Report By

- Type: Motorized Yacht and Sailing Yacht

- Motorized Yacht: Super Yacht, Sport Yacht, Flybridge Yacht, and Others

- Application: Private and Commercial

- Size: 20 to 50 meters, Up to 20 meters, and Above 50 meters

- Hull Type: Monohull, Displacement Hull, Planing Hull, Multihull, and Specialized Hull

- Geography: North America, Europe, APAC, Middle East & Africa, and Latin America

Industry Analysis Report, Regional Outlook, Growth Potential, Price Trends, Competitive Market Share & Forecast 2025–2030.

This report includes market data points, ranging from trend

analyses to market estimates & forecasts that you can customize

YACHT MARKET REPORT SCOPE

| REPORT ATTRIBUTE | DETAILS |

|---|---|

| Market Size (2030) | USD 17.06 Billion |

| Market Size (2024) | USD 11.6 Billion |

| CAGR (2024-2030) | 6.65% |

| HISTORIC YEAR | 2021-2023 |

| BASE YEAR | 2024 |

| FORECAST YEAR | 2025-2030 |

| LARGEST REGION (2024) | Europe |

| SEGMENTS BY | Type, Motorized Yacht, Application, Size, Hull Type, and Geography |

| GEOGRAPHIC ANALYSIS | North America, Europe, APAC, Latin America, and the Middle East & Africa |

| KEY PLAYERS | Azimut-Benetti Group, BENETEAU, Ferretti Group, Princess Yachts, Sanlorenzo, and Sunseeker |

YACHT MARKET SIZE & SHARE

The global yacht market was valued at USD 11.6 billion in 2024 and is projected to reach USD 17.06 billion by 2030, growing at a CAGR of 6.65% during the forecast period. The market is experiencing significant growth driven by multiple factors, including the integration of smart technology and connectivity, the made-to-measure trend, rising demand for sustainable yachting, and the explorer yacht revolution. Additional drivers include the growing demand for luxury tourism, increasing interest in water sports and leisure activities, government initiatives and infrastructure development, and the emerging floating home concept.

There is significant demand for fully integrated AI-powered systems in motor yachts for managing everything from power consumption and navigation to entertainment and lighting with seamless tablet commands or voice. There are significant growth opportunities in the explorer yachts, which are built with robust hulls, extensive storage, and long-range capabilities.

YACHT MARKET NEWS

- In 2024, Azimut-Benetti and Rolls-Royce will work more closely on yacht propulsion systems. They have signed a four-year partnership and framework agreement on cooperation.

- In January 2025, Ferretti S.p.A. launches the first unit of the brand-new Ferretti Yachts 940. The company’s new model is the perfect blend of spaciousness and design.

- In February 2025, Sunseeker, the world's leading brand for luxury motor yachts, unveiled an extensive line-up at the Miami International Boat Show 2025. It has presented eight exceptional models - the Superhawk 55, Predator 55, Manhattan 55, Manhattan 68, Predator 75, 76 Yacht, Ocean 182, and 95 Yacht.

KEY TAKEAWAYS

- Market Growth: The global yacht market size was valued at USD 11.6 billion in 2024 and is projected to reach USD 17.06 billion by 2030, growing at a CAGR of 6.65% during the forecast period.

- By Type: The motorized yacht segment holds the largest market share of over 89%.

- By Motorized Yacht: The super yacht segment dominates and holds the largest market share.

- By Application: The commercial segment shows the highest growth of 6.74% during the forecast period.

- By Size: The 20 to 50 meters segment accounted for the largest global yacht market share.

- By Hull Type: The monohull segment accounted for the largest market share in 2024.

- By Geography: The European region dominates and holds the largest market share of 44%.

- Growth Factor: The global yacht market is set to grow due to growing demand for luxury tourism and rising interest in water sports and leisure activities.

YACHT MARKET TRENDS

Integration of Smart Technology and Connectivity

Integration of smart technology & connectivity is a significant trend in the yacht market. It is driven by several factors, including AI-driven navigation, intelligent operations & predictive maintenance, integrated bridge systems, centralized digital control systems, satellite connectivity & high-speed internet, and increased demand for smart entertainment. Smart technology in yachts incorporates advanced sensors, communication systems, electronics, and software. It enables real-time data collection, remote control & monitoring, seamless integration, and automated systems. Real-time updates from instruments and AI-integrated forecasts help to manage the plan for safer trips by avoiding rough waters. Yachts remain steady due to automated systems. The sensors use data analysis and critical components to predict maintenance. They help to ensure the safety at sea.

Increasing Popularity of the Made-to-Measure Trend

The Made to Measure trend is a prominent one in the global yacht market. The key customization trends in yachts include interior personalization, advanced features, wellness spaces, sustainability, and entertainment. This trend is driven by several factors, which include increased demand for modular designs, significant growth in expedition yachts, increased demand for personalized service, increased focus on floating wellness, increased social & family needs, innovative semi-custom layouts, and technological integration. Yacht owners are looking for attractive designs that can reflect their style and help to meet their preferences. People are engaging in several activities such as day entertaining, simple relaxation, or watersports.

YACHT MARKET DRIVERS

Growing Demand for Luxury Tourism

Growth in luxury tourism demand is a significant driver in the global yachts market. The demand is driven by several factors, including increased focus on privacy & safety, high emphasis on customized & exclusive travel experiences, growth in luxury tourism, increased lifestyle investments and status symbols, demand for event-based destination tourism, and the quest for experiential & adventure travels. The desire for exclusivity, privacy, and unique journeys has led many affluent tourists to consider yacht charters and yacht-based vacations as a preferred mode of travel. Regions such as the Amalfi Coast, St. Barts, the Bahamas, the French Riviera, and the Greek Isles are the yacht tourism hubs. The Monaco Yacht Show is one of the attractive events among luxury travelers who like to combine yachting with exclusive tourism events.

Rising Interest in Water Sports and Leisure Activities

Rising interest in water sports and leisure activities is a significant driver in the global yachts market. It is driven by several factors, including the increased demand for active leisure, growing popularity of yacht charters, growth in marine tourism, the demand for toy garages, integrating submarines & aircraft, and custom hubs for specific passions. The demand for adventure yachts is rising significantly they are designed for long-range expeditions with water sports. The demand for watersports and leisure activities is rising significantly. They include day boating & cruising, diving, snorkeling, beach clubs, electric power water toys, etc. The popularity of wake surfing & wakeboarding activities is further fueling the growth among younger demographics.

INDUSTRY RESTRAINTS

High Purchasing Costs

High cost is a major challenge in the global yachts market. Several factors, including economic sensitivity, higher initial costs, and significant ongoing ownership expenses, can hinder the growth of the market. There are various ongoing expenses associated with ownership. High operating costs and fluctuating fuel prices pose significant challenges to the global yachts market. The high cost of maintaining and operating yachts includes port fees & taxes, maintenance & repairs, among others. Yachting requires regular repair and maintenance, which is highly complex but necessary to ensure functionality and safety. This cost can be higher, especially for older yachts.

YACHT MARKET SEGMENTATION INSIGHTS

INSIGHTS BY TYPE

The global yacht market by type is segmented into motorized yachts and sailing yachts. The motorized yacht segment holds the largest market share of over 89%. The market is driven by several factors, including the growing desire for luxury amenities and space, the prestige associated with ownership, rising demand for business and entertainment platforms, preference for convenience and comfort, and the integration of smart technology. The appeal of this category lies in its accessibility, ease of operation, and ability to cover longer distances in shorter time frames, making motorized yachts a preferred choice for enthusiasts worldwide.

In the U.S., recreational boating has a long tradition, and this enthusiasm extends to motorized yachts. States with extensive coastlines, such as Florida, California, and the New England region, host a particularly strong market.

Globally, several regions stand out for their sustained demand for motorized yachts. The Mediterranean, encompassing countries such as Italy, France, Spain, and Greece, is especially renowned for its scenic coastlines, vibrant culture, and numerous idyllic islands. Here, demand is fueled by both local buyers and international tourists seeking the luxury and adventure of maritime exploration.

INSIGHTS BY MOTORIZED YACHT

The global yacht market by motorized yacht is categorized into super yacht, sport yacht, flybridge yacht, and others. Superyachts dominate the motorized yacht segment of the global yacht market. Market growth is being driven by factors such as rising demand for experiential travel, the pursuit of ultimate exclusivity, and the desire for bespoke customization.

Renowned for their opulence and exclusivity, superyachts cater to ultra-high-net-worth individuals seeking the pinnacle of luxury and sophistication in maritime experiences. These vessels feature extravagant amenities, including multiple decks, swimming pools, helipads, and lavish interiors, effectively making them floating palaces on the water.

The superyacht segment is experiencing robust global expansion, supported by sustained growth in global wealth and an increasing appetite for unparalleled travel experiences. Despite economic fluctuations, demand for larger vessels has remained resilient. Notable examples include the Ocean Alexander Explorer series, valued for its transoceanic capabilities, and the Nordhavn 96, designed for long-range cruising in style.

INSIGHTS BY APPLICATION

Based on the application, the commercial segment shows the highest growth of 6.74% during the forecast period. The commercial yacht market is driven by several factors, including the rising demand for corporate hospitality and events, the need to offset high operational costs, growing preference for access over ownership among luxury tourists, and the increasing popularity of the “try-before-you-buy” concept.

Corporate events play a pivotal role in fueling demand, as businesses increasingly view yachts as unique and memorable venues for conferences, seminars, team-building activities, and client engagement initiatives. Beyond corporate use, commercial yachts are also sought after for special occasions such as weddings, anniversaries, and milestone celebrations, with the allure of hosting events against stunning coastal landscapes and pristine waters further heightening their appeal.

The market is also being shaped by modern travelers’ preference for immersive and experiential journeys. Commercial yachts enable exploration of diverse destinations while offering the comfort and luxury of a private vessel. Moreover, the ability to customize yachts to specific event requirements has become a key growth driver, with charter companies providing tailored options that allow clients to craft bespoke experiences aligned with their objectives and preferences.

INSIGHTS BY SIZE

By size, the 20 to 50 meters segment accounted for the largest global yacht market share. The segment is also the fastest-growing segment. Several factors are driving the market for yachts in the 20 to 50-meter range, including rising demand for customization, the growing “try-before-use” trend, an increasing number of UHNWIs, the allure of luxury tourism, and the emerging concept of floating homes. Luxury tourism, in particular, has amplified demand, as travelers seeking unique and exclusive experiences increasingly opt for yacht charters to indulge in opulent cruising and exploration.

This segment is highly competitive, with new entrants continuously entering the market. However, established industry leaders continue to hold a significant share, supported by strong brand reputations and loyal customer bases. Their ability to consistently deliver exceptional yachts with cutting-edge features and superior craftsmanship further strengthens their industry prominence.

Looking ahead, evolving trends such as sustainability, connectivity, and advanced customization are expected to shape the future of the 20 to 50-meter yacht segment. The integration of features once exclusive to larger vessels, such as compact gyms, hybrid propulsion systems, and beach clubs, is further fueling growth in this size category, promising increasingly luxurious and personalized experiences for consumers.

INSIGHTS BY HULL TYPE

The monohull segment accounted for the largest global yacht market share in 2024. The monohull yacht market is driven by several factors, including strong familiarity and heritage among yacht buyers, a rising preference for racing events and regattas, and lower costs compared to multihulls. Defined by their single, central hull extending below the waterline, monohull yachts are distinguished from multihull vessels and are celebrated for their graceful, time-honored design, typically featuring a single keel.

Monohull yachts enjoy global recognition, supported by a passionate and diverse sailing community. Regions with strong maritime traditions, such as the Mediterranean, the Caribbean, and the Pacific, represent vibrant markets, offering ideal conditions for both leisurely cruising and competitive regattas.

Recent trends highlight the integration of modern technology, advanced materials, and innovative design features to improve both performance and comfort. Sustainability has also emerged as a key focus, with manufacturers increasingly incorporating eco-friendly materials and propulsion systems into their designs.

YACHT MARKET GEOGRAPHICAL ANALYSIS

The European region dominates and holds the largest global yacht market share of 44%. Germany, the UK, France, Italy, and Spain are among the leading revenue contributors to the European yacht market. The region has witnessed significant adoption of smart technology and rising demand for AI-driven yacht connectivity, further shaping market growth.

High disposable incomes across European countries support greater spending on premium lifestyles and leisure activities, fueling demand for yachts. Europe’s deep-rooted yachting tradition, combined with its appeal as a major tourist destination, makes it a hub for charter yachts. Both small and large yachts are in strong demand, as tourists seek to explore the continent’s diverse coastlines, historic ports, and scenic islands. In 2024, Barcelona welcomed around 12 million visitors, while UK ports recorded approximately 1.6 million passenger embarkations, underscoring the region’s robust potential for yacht tourism.

The APAC yacht market is expanding rapidly, fueled by a growing population of HNWIs and a notable increase in yacht ownership. Japan stands out for its advanced yacht construction capabilities, emphasizing precision and innovation, while Australia’s vast coastlines and azure waters provide an ideal backdrop for both leisurely sailing and adventurous experiences. The region is also witnessing rising demand for smaller yachts, often favored for private leisure and exploration.

Hybrid-electric luxury catamarans are gaining significant traction in the APAC market, creating opportunities for brands that tailor their offerings to local preferences. Inland waterways such as the Yangtze River in China and the Mekong River in Cambodia and Vietnam are increasingly popular for cultural and exotic cruising experiences.

Motorized yachts are also experiencing strong growth in the region, driven by consumer preference for speed and convenience in short getaways, day cruises, and island-hopping. China, Hong Kong, Singapore, and Thailand are seeing rising yacht purchases alongside infrastructure development, with Thailand further strengthened by favorable tax incentives. Meanwhile, Australia and New Zealand maintain mature yachting cultures comparable to Europe, reinforcing APAC’s position as a key growth region in the global yacht market.

YACHT MARKET COMPETITIVE LANDSCAPE

The global yacht market report consists of exclusive data on 45 vendors. The market has a highly competitive and fragmented landscape with a mix of small players, niche players, and established global players. Larger players are heavily investing in developing new products to attract wider consumers and stay competitive in the market. Prominent companies have attained global recognition and are known for their exceptional craftsmanship and design. Companies focus on offering personalized and customized products to boost the consumer experience. The companies present in this market offer competitive pricing and promotions to attract new buyers. Mergers and acquisitions have been a defining feature of the yacht industry, reshaping its competitive landscape and fostering market expansion. Companies are focused on building greener, quieter, and more efficient yachts, which drive the investment in alternative fuels, sustainable materials, and hybrid propulsion. Companies are more focused on maintaining brand prestige and heritage. Many companies are focused on specialization in product offerings such as vessel purpose, by size, and by hull type.

SNAPSHOT

The global yacht market size is expected to grow at a CAGR of approximately 6.65% from 2024 to 2030.

Base Year: 2024

Forecast Year: 2025-2030

The report considers the present scenario of the global yacht market and its market dynamics for 2025−2030. It covers a detailed overview of several market growth enablers, restraints, and trends. The study covers both the demand and supply sides of the market. It also profiles and analyzes leading companies and several other prominent companies operating in the market.

Key Vendors

- Azimut-Benetti Group

- Business Overview

- Product Offerings

- Key Developments

- Key Strategies

- Key Opportunities

- Key Strengths

- BENETEAU

- Ferretti Group

- Princess Yachts

- Sanlorenzo

- Sunseeker

Other Prominent Vendors

- Baglietto

- Business Overview

- Product Offerings

- Bavaria Yachts

- Damen Yachting

- Feadship

- Gulf Craft

- HanseYachts AG

- Heesen Yachts

- Horizon Yachts

- Lurssen Yachts

- Ocean Alexander

- Oceanco

- The Italian Sea Group

- Viking Yacht Company

- ABEKING & RASMUSSEN

- AES Yacht

- Alpha Yachts

- Antonini Navi

- Arcadia Yachts

- Ark Yacht

- Astondoa

- AvA Yachts

- Baltic Yachts

- Bayliss Boatworks

- Bering Yachts

- Bertram Yachts

- BILGIN YACHTS

- Cantiere delle Marche

- Catalina Yachts

- Fountaine Pajot

- Grand Banks Yachts

- Hargrave Custom Yachts

- Kingship Marine Limited

- Mondomarine

- Nobiskrug

- Pacific Asian Enterprises

- Permare

- Sunreef Yachts

- Uniesse Marine Group

- Westport Yachts

SEGMENTATION & FORECASTS

- By Type

- Motorized Yacht

- Sailing Yacht

- By Motorized Yacht

- Super Yacht

- Sport Yacht

- Flybridge Yacht

- Others

- By Application

- Private

- Commercial

- By Size

- 20 to 50 meters

- Up to 20 meters

- Above 50 meters

- By Hull Type

- Monohull

- Displacement Hull

- Planing Hull

- Multihull

- Specialized Hull

- By Geography

- Europe

- Italy

- UK

- France

- Germany

- Netherlands

- Spain

- Greece

- North America

- US

- Canada

- APAC

- China

- Australia & New Zealand

- Singapore

- Thailand

- Japan

- Indonesia

- Philippines

- Middle East & Africa

- UAE

- Saudi Arabia

- Turkey

- Latin America

- Brazil

- Mexico

- Argentina

- Chile

YACHT MARKET FAQs

Which type segment has the largest share in the global yacht market?

How big is the global yacht market?

What are the key drivers of the global yacht market?

Which motorized yacht segment provides more business opportunities in the global yacht market?

What is the growth rate of the global yacht market?

Which region dominates the global yacht market?

Who are the major players in the global yacht market?

EXHIBIT 1 Global Yacht Market 2021-2030 ($ million)

EXHIBIT 2 Global Yacht Market by Type 2021-2030 ($ million)

EXHIBIT 3 Market by Motorized Yacht 2021-2030 ($ million)

EXHIBIT 4 Market by Sailing Yacht 2021-2030 ($ million)

EXHIBIT 5 Global Yacht Market by Motorized Yacht 2021-2030 ($ million)

EXHIBIT 6 Market by Super Yacht 2021-2030 ($ million)

EXHIBIT 7 Market by Sport Yacht 2021-2030 ($ million)

EXHIBIT 8 Market by Flybridge Yacht 2021-2030 ($ million)

EXHIBIT 9 Market by Others 2021-2030 ($ million)

EXHIBIT 10 Global Yacht Market by Application 2021-2030 ($ million)

EXHIBIT 11 Market by Private 2021-2030 ($ million)

EXHIBIT 12 Market by Commercial 2021-2030 ($ million)

EXHIBIT 13 Global Yacht Market by Size 2021-2030 ($ million)

EXHIBIT 14 Market by 20 to 50 meters 2021-2030 ($ million)

EXHIBIT 15 Market by Up to 20 meters 2021-2030 ($ million)

EXHIBIT 16 Market by Above 50 meters 2021-2030 ($ million)

EXHIBIT 17 Global Yacht Market by Hull Type 2021-2030 ($ million)

EXHIBIT 18 Market by Monohull 2021-2030 ($ million)

EXHIBIT 19 Market by Displacement Hull 2021-2030 ($ million)

EXHIBIT 20 Market by Planing Hull 2021-2030 ($ million)

EXHIBIT 19 Market by Multihull 2021-2030 ($ million)

EXHIBIT 20 Market by Specialized Hull 2021-2030 ($ million)

EXHIBIT 21 Global Yacht Market by Geography 2021-2030 ($ million)

EXHIBIT 22 Europe YACHT Market 2021-2030 ($ million)

EXHIBIT 23 Italy YACHT Market 2021-2030 ($ million)

EXHIBIT 24 UK YACHT Market 2021-2030 ($ million)

EXHIBIT 25 France YACHT Market 2021-2030 ($ million)

EXHIBIT 26 Germany YACHT Market 2021-2030 ($ million)

EXHIBIT 27 Netherlands YACHT Market 2021-2030 ($ million)

EXHIBIT 28 Spain YACHT Market 2021-2030 ($ million)

EXHIBIT 29 Greece YACHT Market 2021-2030 ($ million)

EXHIBIT 30 North America YACHT Market 2021-2030 ($ million)

EXHIBIT 31 US YACHT Market 2021-2030 ($ million)

EXHIBIT 32 Canada YACHT Market 2021-2030 ($ million)

EXHIBIT 33 APAC YACHT Market 2021-2030 ($ million)

EXHIBIT 34 China YACHT Market 2021-2030 ($ million)

EXHIBIT 35 Australia & New Zealand YACHT Market 2021-2030 ($ million)

EXHIBIT 36 Singapore YACHT Market 2021-2030 ($ million)

EXHIBIT 37 Thailand YACHT Market 2021-2030 ($ million)

EXHIBIT 38 Japan YACHT Market 2021-2030 ($ million)

EXHIBIT 39 Indonesia YACHT Market 2021-2030 ($ million)

EXHIBIT 40 Philippines YACHT Market 2021-2030 ($ million)

EXHIBIT 41 Middle East & Africa YACHT Market 2021-2030 ($ million)

EXHIBIT 42 UAE YACHT Market 2021-2030 ($ million)

EXHIBIT 43 Saudi Arabia YACHT Market 2021-2030 ($ million)

EXHIBIT 44 Turkey YACHT market 2021-2030 ($ million)

EXHIBIT 45 Latin America YACHT Market 2021-2030 ($ million)

EXHIBIT 46 Brazil YACHT Market 2021-2030 ($ million)

EXHIBIT 47 Mexico YACHT Market 2021-2030 ($ million)

EXHIBIT 48 Argentina YACHT Market 2021-2030 ($ million)

EXHIBIT 49 Chile YACHT Market 2021-2030 ($ million)

LIST OF TABLES

TABLE 1Global Yacht Market 2021-2030 ($ million)

TABLE 2Global Yacht Market by Type 2021-2030 ($ million)

TABLE 3Global Yacht Market by Motorized Yacht 2021-2030 ($ million)

TABLE 4Global Yacht Market by Application Segment 2021-2030 ($ million)

TABLE 5Global Yacht Market by Size Segment 2021-2030 ($ million)

TABLE 6Global Yacht Market by Hull Type Segment 2021-2030 ($ million)

TABLE 7Global Yacht Market by Geography 2021-2030 ($ million)

CHAPTER – 1: Global Yacht Market Overview

- Executive Summary

- Key Findings

- Key Developments

CHAPTER – 2: Global Yacht Market Segmentation Data

- Type Market Insights (2021-2030)

- Motorized Yacht

- Sailing Yacht

- Motorized Yacht Market Insights (2021-2030)

- Super Yacht

- Sport Yacht

- Flybridge Yacht

- Others

- Application Market Insights (2021-2030)

- Private

- Commercial

- Size Market Insights (2021-2030)

- 20 to 50 meters

- Up to 20 meters

- Above 50 meters

- Hull Type Market Insights (2021-2030)

- Monohull

- Displacement Hull

- Planing Hull

- Multihull

- Specialized Hull

CHAPTER – 3: Global Yacht Market Prospects & Opportunities

- Global Yacht Market Drivers

- Global Yacht Market Trends

- Global Yacht Market Constraints

CHAPTER – 4: Global Yacht Market Overview

- Global Yacht Market -Competitive Landscape

- Global Yacht Market - Key Players

- Global Yacht Market - Key Company Profiles

CHAPTER – 5: Appendix

- Research Methodology

- Abbreviations

- Arizton

Select a license type that suits your business needs

Single User Licence

- Report accessible by one user only

- Free 10% or 3 days of customization

- Free post-sale service assistance

- Continuous support through email

5 User Licence

- Report accessible by 5 users within the organization

- Free 15% or 4.5 days of customization

- Continuous support through email and telephone

- Free analyst hour

- Free Upgrade: If an updated report published within 180 days of purchase, you will get the revised report free of charge

Corporate Licence

- Free Datasheet worth $1500

- Report accessible by the entire organization

- Free 20% or 6 days of customization

- Free post-sale service assistance

- Continuous support through email and telephone

- Direct access to lead analysts

- Free analyst hour

- Free Upgrade: If an updated report published within 180 days of purchase, you will get the revised report free of charge

Datasheet Licence

- Report accessible by 1 user only

- Free 15% or 32 hours of customization

- Free post-sale service assistance

- Direct access to lead analysts

Frequently Asked Questions

Which type segment has the largest share in the global yacht market?

How big is the global yacht market?

What are the key drivers of the global yacht market?

Which motorized yacht segment provides more business opportunities in the global yacht market?

What is the growth rate of the global yacht market?

Which region dominates the global yacht market?

Who are the major players in the global yacht market?