Australia Agriculture Equipment Market Research Report 2026-2031

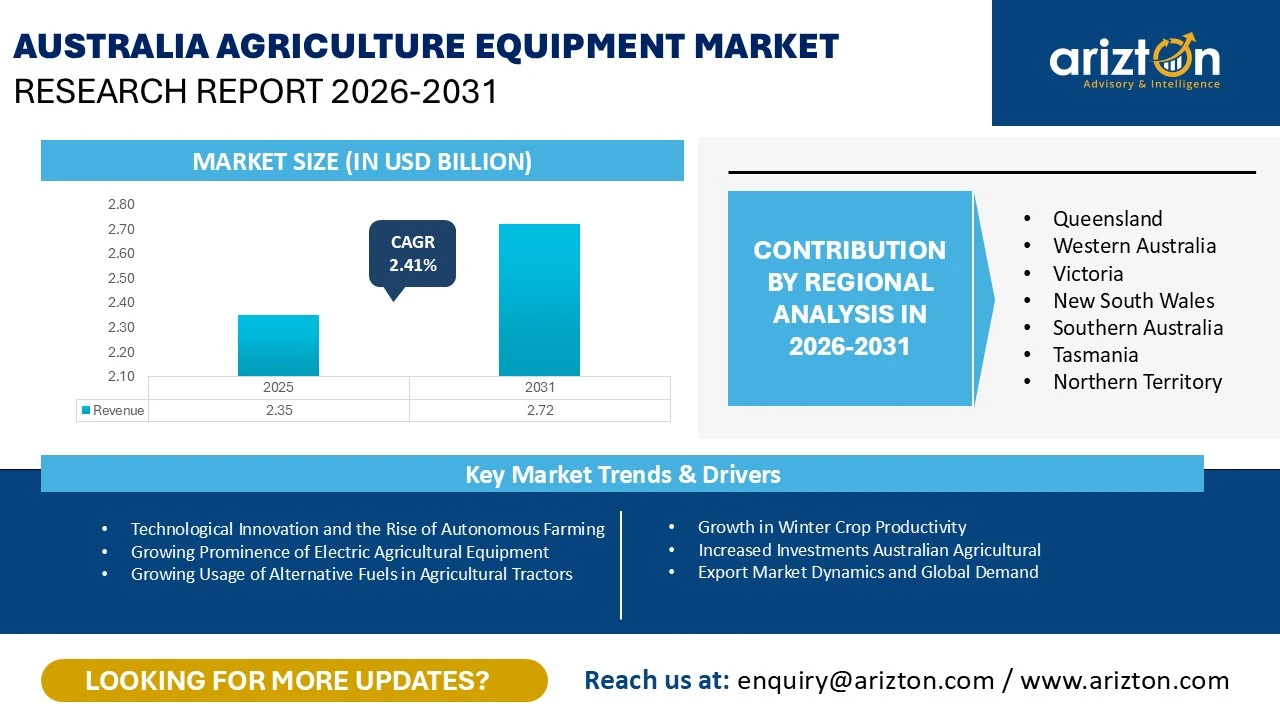

THE AUSTRALIA AGRICULTURE EQUIPMENT MARKET WAS VALUED AT USD 2.35 BILLION IN 2025 AND IS EXPECTED TO REACH USD 2.72 BILLION BY 2031, GROWING AT A CAGR OF 2.41%

143 pages

8 region

1 countries

24 company

5 segments

Purchase Options

Australia Agriculture Equipment Market Research Report 2026-2031

THE AUSTRALIA AGRICULTURE EQUIPMENT MARKET WAS VALUED AT USD 2.35 BILLION IN 2025 AND IS EXPECTED TO REACH USD 2.72 BILLION BY 2031, GROWING AT A CAGR OF 2.41%

The Australia Agriculture Equipment Market Research Report Includes Segments By

- Equipment Type: Land Preparation, Agriculture Tractor, Seedling & Planting, Plant Protection, Harvesting, And Other Equipment

- Land Preparation: Tiller, Plough and Harrow

- Seedling & Planting: Planters and Seed Drillers

- Other Equipment: Mowers and Balers

- Geography: Queensland, Western Australia, Victoria, New South Wales, Southern Australia, Tasmania, and Northern Territory

Industry Analysis Report, Regional Outlook, Growth Potential, Price Trends, Competitive Market Share & Forecast 2026–2031.

This report includes market data points, ranging from trend

analyses to market estimates & forecasts that you can customize

AUSTRALIA AGRICULTURE EQUIPMENT MARKET REPORT SCOPE

| REPORT ATTRIBUTE | DETAILS |

|---|---|

| MARKET SIZE (2031) | USD 2.72 Billion |

| MARKET SIZE (2025) | USD 2.35 Billion |

| CAGR (2025-2031) | 2.41% |

| HISTORIC YEAR | 2022-2024 |

| BASE YEAR | 2025 |

| FORECAST YEAR | 2026-2031 |

| SEGMENTS BY | Land Preparation, Agriculture Tractor, Seedling & Planting, Plant Protection, Harvesting, And Other Equipment |

| GEOGRAPHICAL ANALYSIS | Queensland, Western Australia, Victoria, New South Wales, Southern Australia, Tasmania, and Northern Territory |

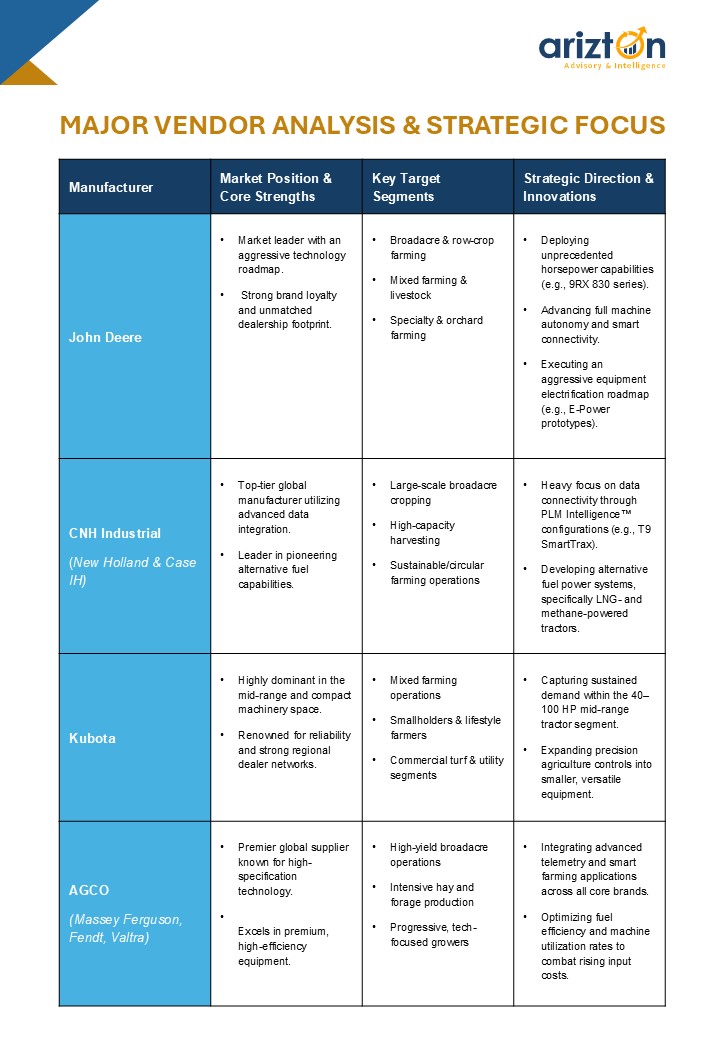

| KEY PLAYERS | John Deere, AGCO, CNH Industrial, Kubota, and Mahindra & Mahindra |

AUSTRALIA AGRICULTURAL EQUIPMENT MARKET ANALYSIS

The Australia agricultural equipment market was valued at USD 2.35 billion in 2025 and is projected to reach USD 2.72 billion by 2031, expanding at a compound annual growth rate (CAGR) of 2.41% over the forecast period.

Currently, the Australia farming machinery market is undergoing a profound structural shift. Accelerated technological innovation is driving widespread industry adoption of high-tech solutions, including GPS-guided automation, telemetry, and advanced precision farming systems.

KEY MARKET DYNAMICS & GROWTH CATALYST

- Surging Winter Crop Productivity: Stronger forecast yields for winter crops are set to directly stimulate sales across the Australia farm equipment market. Larger, high-yield harvests will intensify machinery utilization rates per hectare, driving local growers to resume deferred equipment replacement cycles to handle the increased operational workload.

- Supportive Government Initiatives: Capital access remains a vital driver for the Australian agricultural equipment industry. Key federal initiatives such as the $302.1 million Climate-Smart Agriculture Program, the On-Farm Connectivity Program, and RIC concessional loans effectively lower financial barriers, offering targeted incentives for farmers to adopt next-generation machinery.

- The Shift to Alternative Fuels: Driven by volatile diesel prices and stringent national decarbonization targets, the agricultural equipment landscape in Australia is seeing a major spike in interest toward sustainable powertrains, specifically liquid natural gas (LNG), compressed natural gas (CNG), and hydrogen-powered tractors.

- Resilient Mid-Range Demand: Highlighting the market's underlying stability, the 40–100 HP tractor segment demonstrated strong performance in late 2025. This sustained demand for mid-range tractors underscores active purchasing from mixed farming operations, even during periods when large-scale corporate capital investments remain temporarily subdued.

STRATEGIC MARKET DRIVERS

1. Surging Winter Crop Productivity

A primary catalyst for agricultural equipment sales in Australia in 2026 is the robust rebound in winter crop yields:

- Western Australia: Anticipating its second-highest winter crop production on record for the 2025–26 season.

- South Australia & Victoria: Recovering sharply from previous drought conditions, crop production is forecast to surge by 63% and 17%, respectively.

- Operational Impact: Higher yields of wheat, canola, barley, and lentils require increased machinery utilization rates per hectare, accelerating equipment wear and driving the resumption of deferred fleet replacement cycles.

2. Targeted Government Incentives and Capital Access

Public funding is lowering the barrier to entry for high-tech farm machinery Australia acquisitions:

- The $302.1 million Climate-Smart Agriculture Program (funded via the Natural Heritage Trust) directly incentivizes the adoption of low-emission machinery and precision agriculture systems.

- Programs like the On-Farm Connectivity Program and RIC concessional loans improve liquidity, allowing farmers to finance advanced machinery despite broader inflationary pressures.

- A $3.5 million commitment to Feeding Australia: A National Food Security Strategy aims to structurally scale up food system productivity and supply chain resilience.

3. Favorable Export Market Dynamics

Strong global demand for Australian commodities is boosting grower confidence. Wheat export values are forecast to climb 7% to $9.7 billion in 2025–26, while canola exports are expected to rise 5% to $4.2 billion. Meeting these tight seasonal windows requires local growers to rely on high-capacity seeding, harvesting, and grain-handling machinery.

EMERGING MARKET TRENDS

Technological Advancements and the Expansion of Autonomous Farming

The Australian agricultural equipment market is undergoing a significant transformation, fueled by rapid technological advancements and the growing adoption of precision agriculture solutions. Technologies such as GPS guidance, telematics, data analytics, and autonomous farming systems are increasingly being integrated into modern farm machinery to enhance productivity, efficiency, and operational decision-making.

Leading agricultural equipment manufacturers, including John Deere, AGCO Corporation, CNH Industrial, and Kubota Corporation, have incorporated advanced GPS and telematics capabilities into their latest tractor and machinery offerings in Australia. In 2025, John Deere launched its next-generation round balers in the Australian market, featuring enhanced performance, intelligent connectivity, and improved bale quality, reflecting the industry's shift toward smarter and more automated farming solutions.

Rising Adoption of Electric Agricultural Equipment

The transition toward electrified agricultural machinery is gaining momentum across Australia, supported by technological innovation, sustainability initiatives, and the need to reduce operating costs. Growing concerns over carbon emissions, coupled with rising fuel expenses and supportive government policies, are encouraging farmers to explore electric-powered alternatives to conventional diesel equipment.

Advancements in battery technology are improving the practicality of electric tractors and farm machinery for a wider range of agricultural applications. In May 2025, John Deere introduced its E-Power tractor prototype in Australia, equipped with high-performance KREISEL battery technology and patented immersion-cooling systems. Delivering a continuous output of 130 horsepower and instant torque, the prototype demonstrates the increasing viability of electric solutions for demanding agricultural operations.

Increasing Focus on Alternative Fuel-Powered Tractors

The Australian agricultural sector is also witnessing growing interest in alternative fuel technologies as farmers seek to reduce emissions and improve long-term sustainability. While diesel-powered tractors continue to dominate due to their reliability and high-torque performance, advancements in engine efficiency and fuel technologies are creating opportunities for lower-carbon alternatives.

Government support for renewable and low-carbon fuels expanded in 2025 through federal and state-level funding programs aimed at developing alternative fuel infrastructure and production capacity. Although immediate incentives for farmers remain limited, these initiatives are expected to strengthen the long-term adoption of sustainable fuel solutions. In 2024, New Holland unveiled a prototype LNG-powered T7 series tractor, designed to operate using methane-derived fuels, including biogas generated from livestock waste. The innovation highlights the potential for circular farming systems that combine agricultural productivity with environmental sustainability.

INDUSTRY RESTRAINTS & CHALLENGES

Climate Volatility and Rainfall Deficiencies

Severe rainfall deficits since early 2024 across Tasmania, Victoria, South Australia, and parts of WA and NSW continue to cap market expansion. Notably, irrigation storage depletion within the Murray-Darling Basin has caused a sharp contraction in water-intensive rice production, chilling machinery demand in affected regions.

Margin Squeeze and Fertilizer Spikes

Rising inflation and global supply chain vulnerabilities have weakened farmer profitability.

Example: Heightened geopolitical risks caused local urea prices to peak at approximately $603.6 per ton in September 2025 a 21% surge from the start of the year limiting the available cash flow required for new capital equipment purchases.

Tariff Impact

While import tariffs have marginally pushed up input costs and steered some farmers toward the used equipment and rental markets, the overall impact on the Australia agricultural machinery market remains limited due to the country’s structurally low applied tariff regime and heavy reliance on machinery imports.

MARKET SEGMENTATION INSIGHTS

The Australian agricultural equipment market is led by the tractor segment, which is expected to account for the largest share of the market in 2025. Ongoing demand for mechanization, precision farming, and high-performance machinery is anticipated to support segment growth, with tractors projected to expand at a CAGR of 2.85% during the forecast period. Harvesting equipment, particularly combine harvesters, also represents a significant portion of the market and continues to witness strong adoption among large-scale farming operations.

Within the land preparation equipment category, tillers and plows hold substantial market shares due to their essential role in soil preparation and crop productivity enhancement. The segment is forecast to grow steadily, registering a CAGR of 1.42% through 2031, supported by increasing investments in modern farming practices and efficient land management solutions.

The seeding and planting equipment segment is expected to experience notable growth over the forecast period. Seed drills are projected to lead this category, accounting for approximately 6% of the market share in 2025. Growing emphasis on precision planting, optimized seed placement, and improved crop yields is driving the adoption of advanced seeding technologies across Australian farms.

Among harvesting equipment, combine harvesters maintain a prominent position owing to their operational efficiency and ability to support large-scale agricultural activities. Their advantages include faster harvesting speeds, reduced labor requirements, enhanced productivity, and lower crop losses through precise harvesting mechanisms. As a result, the combine harvester segment is anticipated to witness significant growth throughout the forecast period.

The plant protection equipment segment is evolving toward precision-based and environmentally sustainable solutions. Farmers are increasingly adopting low-volume, camera-guided self-propelled sprayers and advanced application systems that enable targeted chemical deployment. These technologies help reduce chemical consumption, minimize spray drift, and ensure compliance with increasingly stringent environmental and sustainability regulations.

In the other equipment category, mowers are expected to hold the largest market share in 2025, driven by their widespread use in pasture management and forage production. Meanwhile, the baler segment, valued at approximately USD 54 million in 2025, is projected to record strong growth during the forecast period, supported by rising demand for efficient hay and forage handling solutions across the livestock and agricultural sectors.

REGIONAL ANALYSIS

New South Wales (NSW): The most diverse market (broadacre, cotton, livestock), where activity is driven by precision upgrades and machinery replacement cycles rather than fleet expansion.

- Victoria: Characterized by high machinery utilization per hectare, yielding consistent demand for compact to mid-range tractors, mowers, and balers.

- Queensland: Large-scale corporate operations, sugarcane, and grain farms drive demand for ultra-high-horsepower (HP) tractors and specialized harvesting machinery.

- Western Australia (WA): A low-volume but high-value market dominated by massive broadacre export farms, yielding premium transaction values for ultra-high-HP tractors and large-scale seeders.

- Tasmania: Focused on high-value niche crops (hemp, canola, vegetables). Market direction is guided by the Tasmanian Institute of Agriculture’s (TIA) 2026–2031 strategic plan for sustainable food production.

VENDOR LANDSCAPE & KEY DEVELOPMENTS

The market is highly consolidated and competitive, led by premier global OEMs leveraging robust local dealership networks and targeted technological rollouts:

Major Vendor Analysis & Strategic Focus

Why Purchase This Report?

This research stands out as a definitive guide to navigating the Australian ag-tech and machinery space. It delivers actionable data on:

- Volume & Value Forecasts: Granular unit and revenue projections spanning 2022–2031.

- Segment Breakdown: Deep-dive analysis across equipment types, market shares, and import/export trade dynamics.

- Policy & Tech Mapping: Clear overviews of upcoming government funding schemes and OEM technology roadmaps (electric, autonomous, and alternative fuel).

- Competitive Intelligence: Comprehensive profiles of key manufacturers, domestic distributors, and shifting market share dynamics.

SNAPSHOT

The Australia agriculture equipment market size is expected to grow at a CAGR of approximately 2.41% from 2025 to 2031.

The following factors are likely to contribute to the growth of the Australia agriculture equipment market during the forecast period:

- Growth in Winter Crop Productivity

- Increased Investments Australian Agricultural

- Export Market Dynamics and Global Demand

Base Year: 2025

Forecast Year: 2026-2031

The report considers the present scenario of the Australia agriculture equipment market and its market dynamics for 2026−2031. It covers a detailed overview of several market growth enablers, restraints, and trends. The study covers both the demand and supply sides of the market. It also profiles and analyzes leading companies and several other prominent companies operating in the market.

Key Company Profile

- John Deere

- Business Overview

- Product Offerings

- Key Developments

- Key Strategies

- Key Strengths

- Key Opportunities

- AGCO

- CNH Industrial

- Kubota

- Mahindra & Mahindra

Other Prominent Company Profiles

- Silvan Australia

- Business Overview

- Product Offerings

- Same Deutz-Fahr

- Class

- Kioti

- ISEKI

- Lovol Tractors

- YTO Group

- Zoomlion

- K-Line Ag

- KUHN Group

- JCB

- HARDI Australia

- AFGRI Equipment Australia

- RDO Equipment Australia

- Emmetts

- Terrequipe Pty Ltd

- Yanmar

- Inlon Pty Ltd

- On-Trac Ag

Segmentation by Equipment Type

- Land Preparation

- Tillers

- Plough

- Harrow

- Agriculture Tractor

- Seedling & Planting

- Planters

- Seed Drillers

- Plant Protection

- Harvesting

- Other Equipment

- Mowers

- Balers

- States/Regions Covered

- Queensland

- Western Australia

- Victoria

- New South Wales

- Southern Australia

- Tasmania

- Northern Territory

AUSTRALIA AGRICULTURE EQUIPMENT MARKET FAQs

How big is the Australia agriculture equipment market?

What are the key trends in the Australia agriculture equipment market?

Who are the major players in the Australia agriculture equipment market?

What is the growth rate of the Australia agriculture equipment market?

Which region dominates the Australia agriculture equipment market?

For more details, please reach us at [email protected]

1. Scope & Coverage

- Market Definition

- Inclusions

- Exclusions

- Market Estimation Caveats

- Market Size & Forecast Periods

- Historic Period: 2022-2024

- Base Year: 2025

- Forecast Period: 2026-2031

- Market Size (2025-2031)

- Revenue

- Market Segments

- Market Segmentation by Equipment Type

3. Introduction

- Supply Chain Analysis

- Impact Of Tariff

4. Market Dynamics

Market Opportunities & Trends

- Technological Innovation and The Rise of Autonomous Farming

- Growing Prominence of Electric Agricultural Equipment

- Growing Usage of Alternative Fuels in Agricultural Tractors

Market Growth Enablers

- Growth In Winter Crop Productivity

- Increased Investments Australian Agricultural

- Export Market Dynamics and Global Demand

Market Restraints

- Declining Farmer Profitability and Commodity Price Weakness

- Rainfall Deficiency and Prolonged Drought Conditions

- Operational And Workforce Challenges Constraining Demand for Smart Agricultural Equipment

5. Market Landscape

- Market Size & Forecast

- Five Forces Analysis

6. Equipment Type (Market Size & Forecast: 2022-2031)

- Land Preparation Equipment

- Agriculture Tractor

- Seedling & Planting Equipment

- Plant Protection Equipment

- Harvesting Equipment

- Other Equipment

7. Geography

- Australia

- Queensland

- Western Australia

- Victoria

- New South Wales

- Southern Australia

- Tasmania

- Northern Territory

8. Competitive Landscape

- Competitive Overview

- Key Company Profiles: Deere & Company, AGCO Corporation, CNH Industrial N.V., KUBOTA Corporation, and Mahindra & Mahindra

- Other Prominent Company Profiles: Silvan, Same Deutz-Fahr, Class, Kioti, Iseki, Weichai Lovol Intelligent Agricultural Technology Co., Ltd, Yto Group, Zoomlion, K-Line Ag, Kuhn Group, JCB, and Hardi

- Distributor Profiles: Afgri Equipment, RDO Equipment, Terrequipe Pty Ltd, Emmett Motors, Inlon Pty Ltd, and On-Trac Ag

9. Report Summary

- Key Takeaways

- Strategic Recommendations

Select a license type that suits your business needs

Single User Licence

- Report accessible by one user only

- Free 10% or 3 days of customization

- Free post-sale service assistance

- Continuous support through email

5 User Licence

- Report accessible by 5 users within the organization

- Free 15% or 4.5 days of customization

- Continuous support through email and telephone

- Free analyst hour

- Free Upgrade: If an updated report published within 180 days of purchase, you will get the revised report free of charge

Corporate Licence

- Free Datasheet worth $1500

- Report accessible by the entire organization

- Free 20% or 6 days of customization

- Free post-sale service assistance

- Continuous support through email and telephone

- Direct access to lead analysts

- Free analyst hour

- Free Upgrade: If an updated report published within 180 days of purchase, you will get the revised report free of charge

Datasheet Licence

- Report accessible by 1 user only

- Free 15% or 32 hours of customization

- Free post-sale service assistance

- Direct access to lead analysts

Frequently Asked Questions

How big is the Australia agriculture equipment market?

What are the key trends in the Australia agriculture equipment market?

Who are the major players in the Australia agriculture equipment market?

What is the growth rate of the Australia agriculture equipment market?

Which region dominates the Australia agriculture equipment market?

Other RELATED Reports