Germany Data Center Market - Investment Analysis & Growth Opportunities 2026-2031

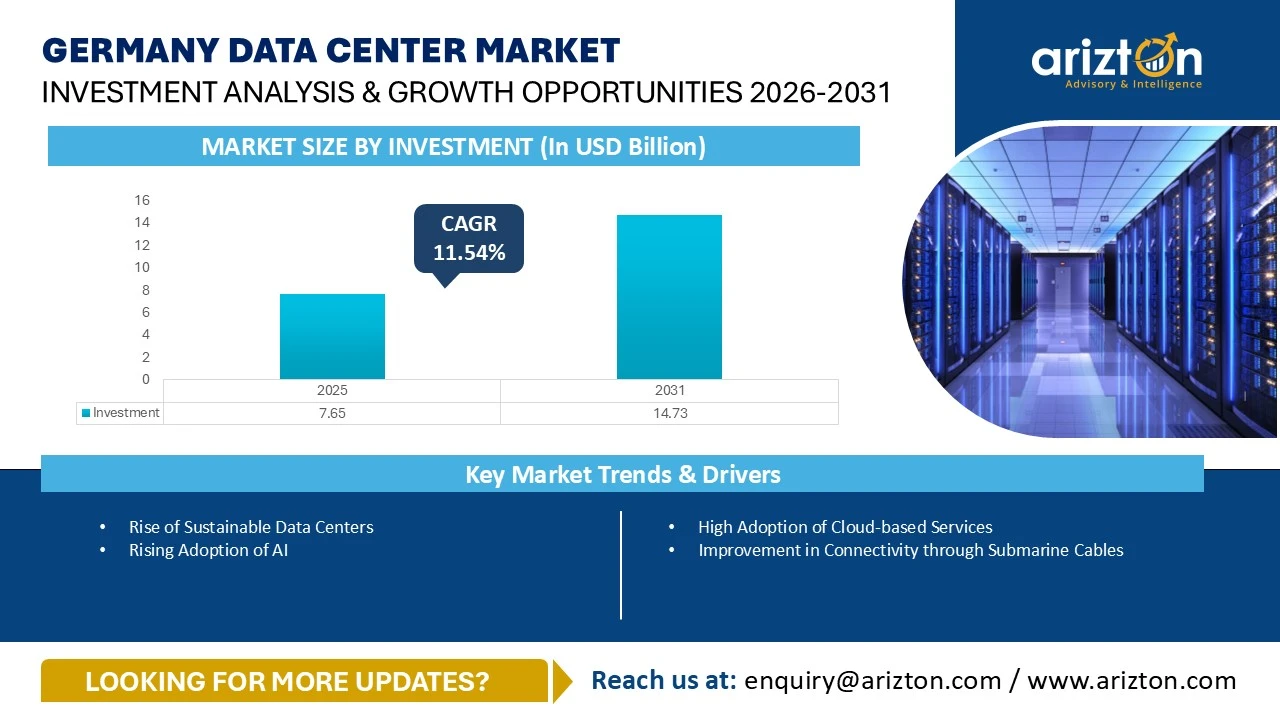

THE GERMANY DATA CENTER MARKET SIZE WAS VALUED AT USD 7.65 BILLION IN 2025 AND IS EXPECTED TO REACH USD 14.73 BILLION BY 2031, GROWING AT A CAGR OF 11.54% DURING THE FORECAST PERIOD.

Germany Data Center Market Growth Insights – Market Area to Reach 2,148.4 Thousand Sq. Ft. and Power Capacity to Exceed 524 MW by 2031, Driven by AI Data Center Investments, Renewable Energy Integration, and Expanding Digital Infrastructure

Published Date : April 2026

Last Updated : July 2026

format: PDF

edition : Eighth Edition

150 pages

1 region

1 countries

102 company

7 segments

Purchase Options

Germany Data Center Market - Investment Analysis & Growth Opportunities 2026-2031

THE GERMANY DATA CENTER MARKET SIZE WAS VALUED AT USD 7.65 BILLION IN 2025 AND IS EXPECTED TO REACH USD 14.73 BILLION BY 2031, GROWING AT A CAGR OF 11.54% DURING THE FORECAST PERIOD.

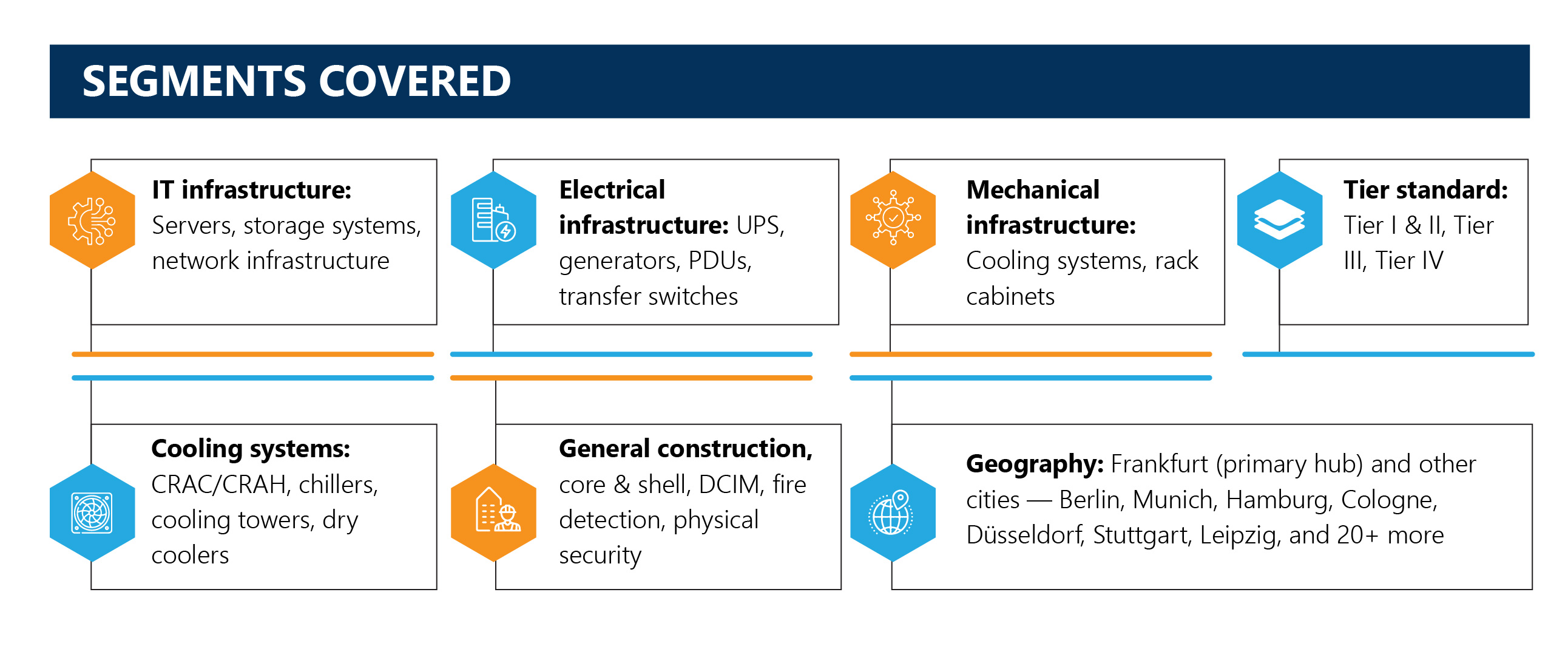

The Germany Data Center Market Report Includes Size in Terms of

- IT Infrastructure: Servers, Storage Systems, and Network Infrastructure

- Electrical Infrastructure: UPS Systems, Generators, Transfer Switches & Switchgears, PDUs, and Other Electrical Infrastructure

- Mechanical Infrastructure: Cooling Systems, Rack Cabinets, and Other Mechanical Infrastructure

- Cooling Systems: CRAC & CRAH Units, Chiller Units, Cooling Towers, Condensers & Dry Coolers, and Other Cooling Units

- General Construction: Core & Shell Development, Installation & Commissioning Services, Engineering & Building Design, Fire Detection & Suppression Systems, Physical Security, and Data Center Infrastructure Management (DCIM)

- Tier Standard: Tier I & Tier II, Tier III, and Tier IV

- Geography: Frankfurt and Other Cities

Get Insights on 194 Existing Data Centers and 43 Upcoming Facilities across Germany

This report includes market data points, ranging from trend

analyses to market estimates & forecasts that you can customize

GERMANY DATA CENTER MARKET REPORT SCOPE

| REPORT ATTRIBUTE | DETAILS |

|---|---|

| MARKET SIZE (INVESTMENT) | USD 14.73 Billion (2031) |

| MARKET SIZE (AREA) | 2,148.4 Thousand Sq. feet (2031) |

| MARKET SIZE (POWER CAPACITY) | 524 MW (2031) |

| CAGR - INVESTMENT (2025-2031) | 11.54% |

| COLOCATION MARKET SIZE (REVENUE) | USD 6.25 Billion (2031) |

| HISTORIC YEAR | 2022-2024 |

| BASE YEAR | 2025 |

| FORECAST YEAR | 2026-2031 |

GERMANY DATA CENTER MARKET SIZE & SHARE ANALYSIS

The Germany data center market is undergoing a profound structural transformation, solidifying its position as the premier powerhouse of European digital infrastructure. Valued at USD 7.65 billion in 2025, the market is on a steep upward trajectory, projected to reach USD 14.73 billion by 2031. This rapid expansion represents a robust Compound Annual Growth Rate (CAGR) of 11.54% over the forecast period.

This sustained Germany data center growth is fueled by a confluence of macroeconomic and technological drivers. At the forefront is a thriving digital economy characterized by wholesale enterprise IT modernization and aggressive cloud migration. Furthermore, stringent European and domestic regulations regarding digital sovereignty are compelling organizations to store and process data within national borders, boosting localized investments. High internet and social media penetration, combined with an industrialized economy rapidly adopting automated technologies, further amplifies the need for scalable infrastructure.

Crucial to this development is Germany's world-class connectivity network. A dense grid of terrestrial fiber-optic networks and strategic submarine cable landing stations provides the low-latency backbone required by international and domestic investors alike. As corporate Germany shifts away from legacy on-premises server rooms, the reliance on advanced third-party facilities has elevated the strategic importance of the Germany data center industry to unprecedented heights.

Facility pipeline

194 Existing Facilities | 43 Upcoming Facilities | 30+ Cities | $10–$12/W Construction Cost

As of 2025, developing a data center in Germany costs between $10-$12 per W. These costs are expected to increase annually due to persistent supply chain disruptions, rising inflation, and higher interest rates.

Various cities across Germany, including Berlin, Munich, Hamburg, Stuttgart, Düsseldorf, Cologne, and Leipzig, have been enhancing their power infrastructure to accommodate data center growth by enhancing grid connectivity and renewable energy solutions.

WANT THE FULL LIST OF 43 UPCOMING DATA CENTERS? CUSTOMIZATION AVAILABLE!

Key Market Dynamics & Infrastructure Pipeline

Facility Pipeline and Escalating Development Costs

The physical footprint of the Germany data center market highlights both its current scale and its aggressive roadmap for future expansion.

- Existing Infrastructure: There are 194 active facilities currently operational across the country, establishing a massive baseline of computing power and storage capacity.

- Upcoming Pipeline: To meet skyrocketing demand, an additional 43 planned facilities are in various stages of design and construction, spanning more than 30 cities.

Despite this robust development pipeline, operators are facing significant headwinds on the macroeconomic front. In 2025, data center capital expenditure (CapEx) construction costs stood at an estimated $10 to $12 per Watt. Moving deeper into the forecast period, these development costs are anticipated to climb steadily. This capital inflation is driven by persistent global supply chain disruptions for critical components, rising material costs, labor shortages, and elevated interest rates that complicate project financing. Consequently, developers are forced to optimize their supply chains and adopt highly efficient modular construction techniques to protect their margins.

The Rise of AI-Ready Infrastructure

A massive technological paradigm shift toward Germany cloud data centers and high-density, AI-driven infrastructure is actively reshaping the market. The sudden explosion of generative artificial intelligence, large language models (LLMs), and complex machine learning (ML) workloads has rendered traditional data center architectures obsolete for high-performance computing.

Dense AI and ML workloads require vastly more power per rack than standard cloud applications. To prevent thermal throttling and maximize operational efficiency, the industry is witnessing a rapid overhaul of Germany data center infrastructure. Legacy air-cooling frameworks are being supplemented or replaced by advanced power delivery systems and next-generation cooling technologies, most notably liquid immersion cooling and direct-to-chip cooling systems.

Recent landmark investments highlight this trend toward high-density architecture:

- Polarise (March 2026): Announced a major 30 Megawatt (MW) AI-ready data center campus in Amberg. Designed with long-term scalability in mind, the site can expand up to 120 MW and will utilize 100% renewable wind and solar power in direct partnership with energy provider WV Energie AG.

- Data Center Partners (January 2025): Unveiled a 17 MW high-density facility in Munich. Built specifically to handle dense computing loads, it features a massive 30MVA utility feed and targets a highly optimized Power Usage Effectiveness (PUE) metric of 1.2.

KEY TAKEAWAYS

- Market grows from $7.65B (2025) to $14.73B (2031) at 11.54% CAGR — driven by AI, cloud, and hyperscale demand.

- Frankfurt remains the primary hub but faces land scarcity; Berlin, Munich, Hamburg, Cologne & Düsseldorf are high-growth alternatives.

- 194 existing facilities + 43 upcoming tracked across 30+ German cities; construction cost at $10–$12/W and rising.

- Wholesale colocation leads at $1,498M revenue (2025); retail growing faster at 22.98% CAGR through 2031.

- AI-ready, high-density facilities integrating renewable energy and waste-heat reuse are reshaping investment priorities.

- New entrants, including Bluestar, Data4, VIRTUS, and STACK Infrastructure, are accelerating capacity expansion.

GERMANY DATA CENTER MARKET - KEY HIGHLIGHTS

- New entrants, such as Bluestar Data Center, DATA CASTLE, Data4, Goodman, Green Mountain & KMW, maincubes SECURE DATACENTERS, SDC Capital Partners, Mainova WebHouse, STACK Infrastructure, and VIRTUS Data Centres, continue to invest significantly to develop data centers across the country.

- Frankfurt is facing land scarcity for new data center development due to rapid industrial expansion and limited space availability. At the same time, cities such as Berlin, Munich, Hamburg, Cologne, and Düsseldorf continue to emerge as key locations, attracting vast data center investments to support the growing digital economy of the nation.

- Modern facilities are engineered with ultra-low PUE and waste-heat reuse systems, ensuring that dense AI workloads are delivered sustainably and at scale. For instance, in January 2025, Data Center Partners announced a 17 MW data center in Munich with a 30MVA utility feed and a PUE target of 1.2. The facility is tailored for AI and ML loads while incorporating waste heat reuse to support local sustainability goals.

Emerging Locations of Data Centers in Germany

While Frankfurt remains the primary data center hub, it faces land scarcity and power constraints due to rapid expansion. As a result, secondary cities such as:

- Berlin

- Munich

- Hamburg

- Cologne

- Düsseldorf

are emerging as high-growth investment destinations, supported by improved infrastructure and policy backing.

Regional Breakdown: Frankfurt vs. Emerging Secondary Cities

Geographically, Germany’s digital infrastructure is undergoing a necessary and rapid decentralization. While the traditional core continues to attract capital, severe resource constraints, namely acute real estate shortages, strict municipal zoning laws, and overextended power grid capacity, are forcing a broader geographic distribution of investment.

Despite these operational hurdles, Frankfurt remains the nation's primary hub, anchoring the market as Europe's largest data ecosystem and core connectivity zone due to the presence of the DE-CIX internet exchange. However, to bypass Frankfurt’s severe bottlenecks and position themselves closer to regional enterprise clusters, operators are increasingly funneling new investments into high-growth secondary cities, including Berlin, Munich, Hamburg, Cologne, Düsseldorf, Stuttgart, and Leipzig. These emerging regional markets are capturing substantial market share by upgrading local grid infrastructure, deploying low-latency edge computing nodes, and integrating facilities directly with regional renewable energy grids to meet modern sustainability targets.

A primary catalyst for this regional expansion is the intense industry focus on sustainability and sovereign operations. Modern facilities in both primary and secondary markets are engineered with ultra-low PUE targets and integrated waste-heat reuse systems to comply with strict environmental mandates.

Sustainability Benchmark: In March 2026, Stadtwerke Lübeck launched its first self-operated, digitally sovereign data center. This project serves as a blueprint for secondary market development, featuring fully redundant backup systems, onsite solar power integration, and direct municipal waste-heat utilization to warm local public infrastructure.

Want a city-level or segment-specific data cut? We customize any section — ask about "Frankfurt vs. Secondary City" breakdowns.

GERMANY DATA CENTER - INDUSTRY TRENDS & GROWTH DRIVERS

1. Surging AI & Supercomputing Adoption

High-density computing demand across Germany’s core economic sectors—specifically manufacturing (Industry 4.0), automotive, healthcare, and corporate finance is forcing data centers to modernize. To remain competitive, operators must provision infrastructure capable of hosting specialized hardware like GPUs and tensor processing units (TPUs). This trend ensures that future facilities will be measured by their power density per rack rather than pure physical square footage.

2. 5G Rollouts & Edge Data Centers

The nationwide expansion of standalone 5G networks is transforming data processing requirements. To support low-latency applications such as autonomous driving, smart city infrastructure, and real-time Internet of Things (IoT) analytics in manufacturing, operators are accelerating the deployment of localized edge data centers. These smaller, decentralized nodes process data closer to the end-user, reducing backhaul traffic to central hubs in Frankfurt.

3. Stringent Green Infrastructure Regulations

Germany’s strict regional and federal environmental guidelines, along with the European Energy Efficiency Directive (EED), are forcing a massive green transition. Operators must prioritize renewable energy procurement and invest heavily in energy-efficient mechanical, electrical, and plumbing (MEP) infrastructure. This includes upgrading to high-efficiency computer room air conditioning and air handler units (CRAC/CRAH), advanced chillers, and localized cooling towers designed to minimize water and power consumption.

GERMANY DATA CENTER MARKET COMPETITIVE LANDSCAPE

The Germany data center investment landscape is highly competitive and fragmented, consisting of specialized IT infrastructure providers, mechanical and electrical engineering firms, global real estate investors, and aggressive new entrants.

IT Infrastructure Providers

These companies supply the foundational technology stack, including AI-optimized hardware, high-performance servers, enterprise storage arrays, and high-speed networking components.

- Key Players: Atos, Broadcom, Cisco Systems, Dell Technologies, Fujitsu, Hewlett Packard Enterprise (HPE), Huawei Technologies, IBM, Lenovo, NetApp, NVIDIA.

Support Infrastructure Providers

Specialized in power delivery and thermal management, these vendors supply critical infrastructure such as uninterruptible power supply (UPS) systems, industrial generators, switchgears, power distribution units (PDUs), and advanced liquid or air-cooling systems.

- Key Players: ABB, Airedale, Caterpillar, Cummins, Delta Electronics, Eaton, Legrand, Mitsubishi Electric, Pillar Power Systems, Rehlko (formerly Kohler Power Systems), Riello Elettronica Group, Rittal, Rolls-Royce, Schneider Electric, Siemens, Socomec Group, STULZ, Vertiv.

Data Center Construction & Engineering

These specialized engineering, procurement, and construction (EPC) firms focus on core and shell development, modular prefabrication, architectural design, structural engineering, and final facility commissioning.

- Key Players: AECOM, Arup, Collen Construction, DPR Construction, Ethos Engineering, HOCHTIEF, ICT Facilities, EXYTE (M+W Group), SPIE, Winthrop Technologies, Zech Group.

Established Investors & Colocation Operators

These organizations dominate the existing Germany data center market share, managing massive multi-tenant wholesale campuses and retail facilities across primary and secondary markets.

- Key Players: Digital Realty, Equinix, CyrusOne, Colt Data Centre Services, NTT DATA, EdgeConneX, Global Switch, Iron Mountain, Vantage Data Centres, Yondr, maincubes, Mainova WebHouse.

Prominent New Entrants

Capitalizing on the unmet demand for hyperscale cloud and AI capacity, these aggressive new players are injecting billions in capital to accelerate new construction starts across Germany.

- Key Players: Argaman Group, Aroundtown, Bluestar Data Centre, Data Castle, Data Center Partners, Data4, dataR GmbH, Lidl (Schwarz Digits), NEOIX, PGIM Real Estate, SDC Capital Partners, STACK Infrastructure, VIRTUS Data Centres.

NEED CUSTOM VENDOR PROFILES? CUSTOMIZATION AVAILABLE!

WHY SHOULD YOU BUY THIS DATA CENTER RESEARCH REPORT?

- Market size available in the investment, area, power capacity, and Germany colocation market revenue.

- An assessment of the data center investment in Germany by colocation, hyperscale, and enterprise operators.

- Data center investments in the area (square feet) and power capacity (MW) across cities in the country.

- A detailed study of the existing Germany data center market landscape, an in-depth industry analysis, and insightful predictions about the Germany data center market size during the forecast period.

- Snapshot of existing and upcoming third-party data center facilities in Germany

- Facilities Covered (Existing): 194

- Facilities Identified (Upcoming): 43

- Coverage: 30+ Cities

- Existing vs. Upcoming (Data Center Area)

- Existing vs. Upcoming (IT Load Capacity)

- Data center colocation market in Germany

- Colocation Market Revenue & Forecast (2022-2031)

- Retail & Wholesale Colocation Revenue (2022-2031)

- Retail & Wholesale Colocation Pricing

- Germany data center landscape market investments are classified into IT, power, cooling, and general construction services, with sizing and forecast.

- A comprehensive analysis of the latest trends, growth rate, potential opportunities, growth restraints, and prospects for the industry.

- Business overview and product offerings of prominent IT infrastructure providers, construction contractors, support infrastructure providers, and investors operating in the industry.

- A transparent research methodology and the analysis of the demand and supply aspects of the market.

SNAPSHOT

The Germany data center market size is projected to reach USD 14.73 billion by 2031, growing at a CAGR of 11.54% from 2025 to 2031.

The following factors are likely to contribute to the growth of the Germany data center market

- High Adoption of Cloud-based Services

- Improvement in Connectivity through Submarine Cables

Base Year: 2025

Forecast Year: 2026-2031

The report considers the present scenario of the Germany data center market and its market dynamics for 2026-2031. It covers a detailed overview of several market growth enablers, restraints, and trends. The study includes the demand and supply aspects of the market.

This report also analyses the Germany data center market share. It elaborately analyses the existing and upcoming facilities and investments in IT, electrical, mechanical infrastructure, general construction, and tier standards. It discusses market sizing and investment estimation for different segments.

The segmentation includes:

- IT Infrastructure

- Servers

- Storage Systems

- Network Infrastructure

- Electrical Infrastructure

- UPS Systems

- Generators

- Transfer Switches & Switchgears

- PDUs

- Other Electrical Infrastructure

- Mechanical Infrastructure

- Cooling Systems

- Rack Cabinets

- Other Mechanical Infrastructure

- Cooling Systems

- CRAC & CRAH Units

- Chiller Units

- Cooling Towers, Condensers & Dry Coolers

- Other Cooling Units

- General Construction

- Core & Shell Development

- Installation & Commissioning Services

- Engineering & Building Design

- Fire Detection & Suppression Systems

- Physical Security

- Data Center Infrastructure Management (DCIM)

- Tier Standard

- Tier I & Tier II

- Tier III

- Tier IV

- Geography

- Frankfurt

- Other Cities

VENDOR LANDSCAPE

IT Infrastructure Providers

- Atos

- Broadcom

- Cisco Systems

- Dell Technologies

- Fujitsu

- Hewlett Packard Enterprise

- Huawei Technologies

- IBM

- Lenovo

- NetApp

- NVIDIA

Data Center Construction Contractors & Sub-Contractors

- AECOM

- Arup

- Collen Construction

- DPR Construction

- Ethos Engineering

- HOCHTIEF

- ICT Facilities

- KLEINUNDARCHITEKTEN

- Lupp Group

- Max Bögl

- Mercury

- M+W Group (EXYTE)

- SPIE

- Winthrop Technologies

- Zech Group

Support Infrastructure Providers

- ABB

- Airedale

- Caterpillar

- Cummins

- Delta Electronics

- Eaton

- Legrand

- Mitsubishi Electric

- Piller Power Systems

- Rehlko

- Riello Elettronica Group

- Rittal

- Rolls-Royce

- Schneider Electric

- Siemens

- Socomec Group

- STULZ

- Vertiv

Data Center Investors

- 3U Telecom

- aixit GmbH

- AtlasEdge

- CloudHQ

- Carrier Colo

- China Mobile International

- Centron

- Cogent Communications

- Comarch

- Contabo

- Colt Data Centre Services

- CyrusOne

- Digital Realty

- DOKOM21

- Equinix

- EdgeConneX

- EVF Data Center

- FirstColo

- Goodman

- GRASS-MERKUR

- GTT

- Global Switch

- Iron Mountain

- ITENOS

- maincubes SECURE DATACENTERS

- Lumen Technologies

- Mainova WebHouse

- NewTelco

- NorthC

- nLighten

- Noris Network

- NTT DATA

- Penta Infra

- Portus Data Centers

- PFALZKOM

- PlusServer

- Speedbone

- STACKIT

- Telehouse

- TelemaxX

- Vantage Data Centres

- WIIT

- Yondr

New Entrants

- Argaman Group

- Aroundtown

- Bluestar Data Centre

- Data Castle

- Data Center Partners

- DataHall

- Data4

- dataR GmbH

- Lidl

- NEOIX

- PGIM Real Estate

- SDC Capital Partners

- STACK Infrastructure

- VIRTUS Data Centres

GERMANY DATA CENTER MARKET FAQs

How big is the Germany data center market?

How much mw of power capacity will be added across Germany during 2026-2031?

What factors are driving the Germany data center market?

Which all geographies are included in Germany center market report?

For more details, please reach us at [email protected]

1. CHAPTER 1: EXISTING & UPCOMING THIRD-PARTY DATA CENTERS IN GERMANY

• Data Center Snapshot

• Data Center Snapshot by Cities

• Existing and Upcoming Data Center Supply

• List of Upcoming Data Center Projects in Germany

2. CHAPTER 2: INVESTMENT OPPORTUNITIES IN GERMANY

• Microeconomic & Macroeconomic Factors for Germany Market

• Impact of AI on Data Center Industry in Germany

• Investment Opportunities in Germany

• Digital Data in Germany

• Government Rule and Regulation for Data Center

• Market Investment by Area

• Market Investment by Power Capacity

3. CHAPTER 3: DATA CENTER COLOCATION MARKET IN GERMANY

• Colocation Services Market in Germany

• Demand Across Several Industries in Germany

• Retail Vs. Wholesale Data Center Colocation

• Industry Demand Share

• Colocation Pricing (Quarter Rack, Half Rack, & Full Rack) and Addons

4. CHAPTER 4: MARKET DYNAMICS

• Market Enablers

• Market Trends

• Market Restraints

5. CHAPTER 5: MARKET SEGMENTATION

• IT Infrastructure: Market Size & Forecast

• Electrical Infrastructure: Market Size & Forecast

• Mechanical Infrastructure: Market Size & Forecast

• General Construction: Market Size & Forecast

• Break-up of Construction Cost

6. CHAPTER 6: TIER STANDARDS INVESTMENT

• Tier I & II

• Tier III

• Tier IV

7. CHAPTER 7: GEOGRAPHY SEGMENTATION

• Frankfurt

• Other Cities

8. CHAPTER 8: KEY MARKET PARTICIPANTS

• IT Infrastructure Providers

• Construction Contractors & Sub-Contractors

• Support Infrastructure Providers

• Data Center Investors

• New Entrants

9. CHAPTER 9: APPENDIX

• Market Derivation

• Site Selection Criteria

• Quantitative Summary

Select a license type that suits your business needs

Single User Licence

- Report accessible by one user only

- Free 10% or 3 days of customization

- Free post-sale service assistance

- Continuous support through email

5 User Licence

- Report accessible by 5 users within the organization

- Free 15% or 4.5 days of customization

- Continuous support through email and telephone

- Free analyst hour

- Free Upgrade: If an updated report published within 180 days of purchase, you will get the revised report free of charge

Corporate Licence

- Free Datasheet worth $1500

- Report accessible by the entire organization

- Free 20% or 6 days of customization

- Free post-sale service assistance

- Continuous support through email and telephone

- Direct access to lead analysts

- Free analyst hour

- Free Upgrade: If an updated report published within 180 days of purchase, you will get the revised report free of charge

Datasheet Licence

- Report accessible by 1 user only

- Free 15% or 32 hours of customization

- Free post-sale service assistance

- Direct access to lead analysts

Frequently Asked Questions

How big is the Germany data center market?

How much mw of power capacity will be added across Germany during 2026-2031?

What factors are driving the Germany data center market?

Which all geographies are included in Germany center market report?

Other RELATED Reports

UK Data Center Market - Investment Analysis & Growth Opportunities 2026-2031

Published : April 2026

France Data Center Market - Investment Analysis & Growth Opportunities 2026-2031

Published : April 2026

Ireland Data Center Market – Investment Analysis & Growth Opportunities 2026-2031

Published : April 2026

Finland Data Center Market - Investment Analysis & Growth Opportunities 2026-2031

Published : April 2026