U.S. Hyperscale Data Center Market – Industry Outlook & Forecast 2026-2031

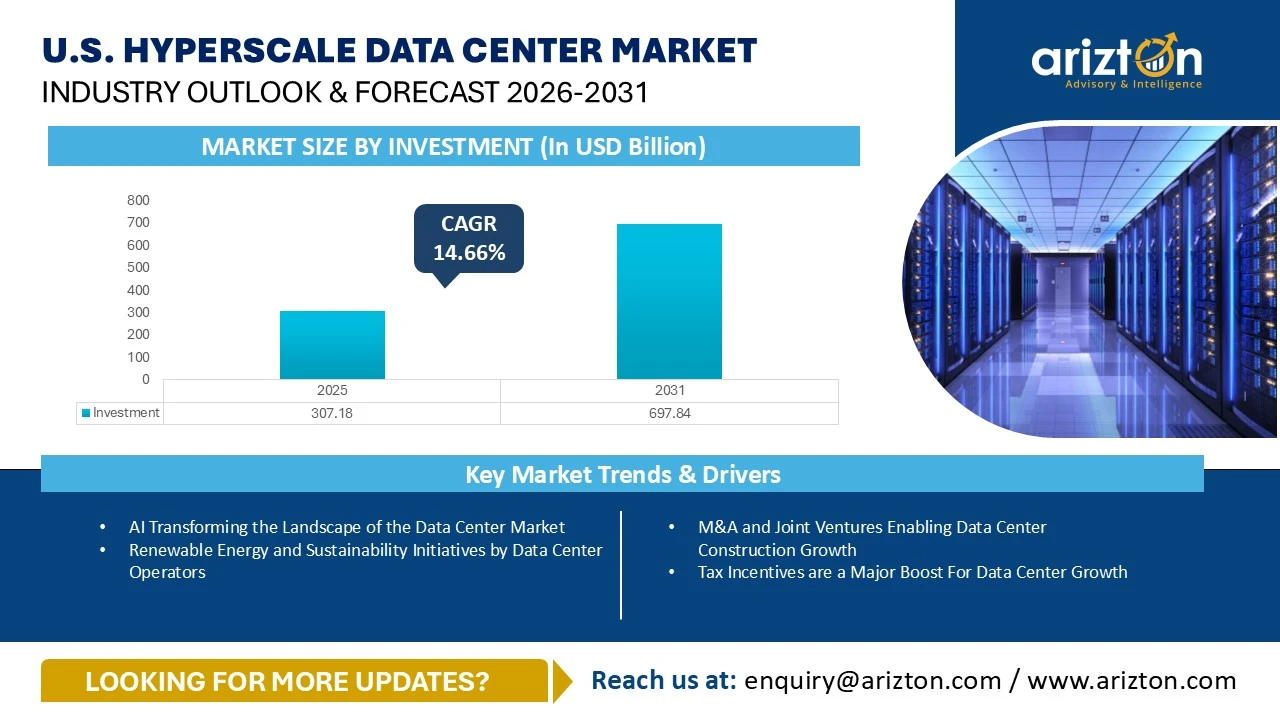

U.S. HYPERSCALE DATA CENTER MARKET SIZE WITNESSED INVESTMENTS OF USD 307.18 BILLION IN 2025 AND WILL WITNESS INVESTMENTS OF USD 697.84 BILLION BY 2031, GROWING AT A CAGR OF 14.66% DURING 2025-2031.

278 pages

5 region

1 countries

201 company

9 segments

Purchase Options

U.S. Hyperscale Data Center Market – Industry Outlook & Forecast 2026-2031

U.S. HYPERSCALE DATA CENTER MARKET SIZE WITNESSED INVESTMENTS OF USD 307.18 BILLION IN 2025 AND WILL WITNESS INVESTMENTS OF USD 697.84 BILLION BY 2031, GROWING AT A CAGR OF 14.66% DURING 2025-2031.

The U.S. Hyperscale Data Center Market Size, Share, & Trends Analysis By

- Infrastructure: IT Infrastructure, Electrical Infrastructure, Mechanical Infrastructure, and General Construction

- IT Infrastructure: Server Infrastructure, Storage Infrastructure, and Network Infrastructure

- Electrical Infrastructure: UPS Systems, Generators, Transfer Switches & Switchgear, PDUs, and Other Electrical Infrastructure

- Mechanical Infrastructure: Cooling Systems, Racks, and Other Mechanical Infrastructure

- Cooling System: CRAC & CRAH Units, Chiller Units, Cooling Towers, Condensers & Dry Coolers, Economizers & Evaporative Coolers, and Other Cooling Units

- Cooling Technique: Air-based and Liquid-based

- General Construction: Core & Shell Development, Installation & Commissioning Services, Engineering & Building Design, Fire Detection & Suppression, Physical Security, and DCIM/BMS Solutions

- Tier Standards: Tier I & Tier II, Tier III, and Tier IV

- Region: Southeastern U.S., Midwestern U.S., Southwestern U.S., Western U.S., and Northeastern U.S.

Industry Analysis Report, Regional Outlook, Growth Potential, Price Trends, Competitive Market Share & Forecast 2026–2031.

This report includes market data points, ranging from trend

analyses to market estimates & forecasts that you can customize

U.S. HYPERSCALE DATA CENTER MARKET REPORT SCOPE

| REPORT ATTRIBUTE | DETAILS |

|---|---|

| MARKET SIZE – INVESTMENT (2031) | USD 697.84 Billion |

| MARKET SIZE – INVESTMENT (2025) | USD 307.18 Billion |

| CAGR - INVESTMENT (2025-2031) | 14.66% |

| MARKET SIZE: AREA (2031) | 48.89 million sq. Feet |

| MARKET SIZE: POWER CAPACITY (2031) | 12,684 MW (2031) |

| HISTORIC YEAR | 2022-2024 |

| BASE YEAR | 2025 |

| FORECAST YEAR | 2026-2031 |

| SEGMENTS BY | Infrastructure, IT Infrastructure, Electrical Infrastructure, Mechanical Infrastructure, Cooling Systems, Cooling Technique, General Construction, Tier Standards, and Region |

| REGIONAL ANALYSIS | Southeastern U.S., Midwestern U.S., Southwestern U.S., Western U.S., and Northeastern U.S. |

U.S. HYPERSCALE DATA CENTER MARKET SIZE & SHARE

The U.S. hyperscale data center market size witnessed investments of USD 307.18 billion in 2025 and will witness investments of USD 697.84 billion by 2031, growing at a CAGR of 14.66% during the forecast period. The U.S. hyperscale data center market is currently experiencing significant growth, driven largely by the increasing adoption of technologies, particularly Artificial Intelligence (AI).

Investment in the U.S. hyperscale data centers nearly doubled compared with 2024, fueled by strong construction activity from both colocation and hyperscale operators. It is estimated that the demand for data centers will continue to grow as AI becomes more prevalent.

Major colocation and hyperscale operators are leading this investment surge, announcing significant funding for the development of new data centers across the U.S. over the next three to four years. For instance, in November 2025, Google, as part of a broader $9 billion investment in Oklahoma, announced plans to develop two new data center campuses in Muskogee County. This expansion is expected to significantly enhance Google’s presence in the state while supporting its rapidly developing technology and energy sectors.

U.S. HYPERSCALE DATA CENTER MARKET KEY TRENDS

AI Transforming the Landscape of the Data Center Market

- With the rising development of AI-optimized data center facilities in the U.S., the adoption of GPUs in data centers is significantly increasing in the market. AI-based data centers utilize GPUs as they can perform massively parallel computations, train and run AI models dramatically faster, use power more efficiently for each AI task, support real-time AI inference, and enable high-density, scalable facilities.

- In October 2025, Lambda, The Superintelligence Cloud, is setting up a next-generation AI factory in Kansas City, Missouri, converting a vacant facility (built in 2009) into a cutting-edge AI data center. The site will be powered by over 10,000 NVIDIA Blackwell Ultra GPUs, with plans to expand its capacity in later phases.

Renewable Energy and Sustainability Initiatives by Data Center Operators

- Hyperscale and cloud service providers across the U.S. are significantly increasing their focus on sustainability as the rising demand for AI workloads, cloud computing, and digital infrastructure is continuously driving the need for higher electricity and advanced cooling technologies across large-scale data center facilities.

- In the U.S., hyperscale data center operators are increasingly investing in clean and renewable energy. Several companies are securing long-term Power Purchase Agreements (PPAs), building on-site solar and wind projects, as well as integrating battery storage systems to reduce carbon emissions and improve energy efficiency. In February 2026, Amazon Web Services planned to build a large-scale data center campus, comprising approximately 18 two-story data center buildings, with an investment of over $5 billion in Texas; the data center facility is likely to be powered by nuclear energy.

- As the demand for AI, cloud computing, and HPC continues to accelerate, hyperscale and cloud providers are expected to further strengthen sustainability measures to improve operational efficiency, reduce carbon emissions, and build more environmentally sustainable data centers.

Advance Cooling Solutions for AI/ML Workloads

- AI workloads are changing cooling standards in the U.S. hyperscale data centers, as traditional air cooling is insufficient to manage the heat output from GPU-dense clusters. To maintain efficiency and sustainability, operators are increasingly adopting various advanced cooling methods, such as direct liquid cooling (using cold plates), immersion cooling (submerging hardware in fluid), and hybrid systems, which combine air and liquid cooling. Additionally, AI-optimized cooling controls are being implemented.

- In August 2025, Meta expanded on its liquid-cooled rack design, Catalina, originally built to support NVIDIA GB200 Blackwell chips at densities of up to 140 kW. The company outlined how these high-density liquid-cooled GPUs can be integrated into older air-cooled data centers with much lower rack capacity. Meta showcased its NVL36x2 Catalina pod configuration—adapted from NVIDIA’s NVL72 system—demonstrating that Catalina pods can operate effectively even in 20 kW air-cooled environments.

- Driven by the increasing demands from AI workloads, Microsoft continues to integrate direct-to-chip liquid cooling and research microfluidic technologies to enhance energy efficiency in data centers. These innovations aim to optimize server layouts, reduce water consumption, and increase rack power density while enabling higher compute power per square foot. This shift supports Microsoft's goal of becoming water-positive by 2030 amidst rising water usage across its global operations.

Adoption of Advanced & Innovative Power Technologies

- Innovative power systems are becoming increasingly essential in the U.S. due to the rising deployment of high-density AI and cloud workloads. These workloads generate significantly more heat and require higher energy efficiency. As rack densities exceed 20 kW to 30 kW, traditional power components will no longer suffice, creating the demand for advanced technologies. This includes modern Uninterruptible Power Supply (UPS) systems, batteries, biofuels and fuel cells, HVO fuels for generators, and energy reuse systems. These solutions are necessary to maintain performance while managing operational costs and achieving sustainability targets.

- Google has integrated over 100 million lithium-ion (Li-ion) cells into its global data centers, marking a major milestone since it began adopting Li-ion backup systems in 2015. The company uses a 48V DC rack-level power architecture with built-in Battery Backup Units (BBUs) to ensure seamless, uninterrupted operations across its facilities.

- Nickel-zinc (NiZn) batteries are emerging as a promising alternative for data center backup systems due to their high-power density, fast discharge capability, and improved safety profile as compared with traditional chemistries. They offer longer cycle life, lower environmental impact, and reduced cooling requirements, making them well-suited for mission-critical environments. As operators push for more sustainable and efficient power solutions, NiZn technology is gaining traction as a reliable and cost-effective UPS option.

- Data centers across the U.S. consume rapidly growing amounts of electricity, particularly with the expansion of AI and High-Performance Computing (HPC). This has pushed operators and utilities to explore new power technologies that improve efficiency, resilience, sustainability, and cost-effectiveness.

U.S. HYPERSCALE DATA CENTER MARKET SEGMENTATION INSIGHTS

- In the U.S. market, we observe an increasing number of partnerships among data center operators, cooling technology vendors, chip manufacturers, and energy innovators. These collaborations are becoming essential for developing sustainable AI infrastructure. They facilitate the adoption of liquid cooling, hybrid thermal systems, and energy-efficient designs that support high-density computing while managing energy consumption and minimizing environmental impact. This is crucial for meeting the competitive demands and regulatory standards of modern data centers in the U.S.

- In November 2025, Vertiv introduced its new CoolCenter immersion-cooling system, a fully engineered immersion-cooling tank designed to support workloads ranging from 25 kW to 240 kW per pod. Leveraging Vertiv’s long-standing liquid-cooling expertise, the solution is built to manage high heat densities safely and efficiently, offering a scalable and reliable option for expanding AI infrastructure to data center operators. The technology is currently deployed in the EMEA region, with potential adoption in the US expected soon.

- In March 2025, Crypto and IREN, an AI data center company, announced plans to develop a 75 MW AI data center in Texas. As per the agreement, the companies are planning to deploy a new 75 MW liquid-cooling data center for AI/HPC at its Childress site in Texas. It will be designed to support 200 kW per rack via direct-to-chip cooling for NVIDIA’s Blackwell GPUs.

U.S. HYPERSCALE DATA CENTER MARKET GEOGRAPHICAL ANALYSIS

- The southeastern U.S. includes states such as Alabama, West Virginia, Virginia, North Carolina, Mississippi, Tennessee, Arkansas, South Carolina, Florida, Georgia, Kentucky, and Louisiana.

- Meta is expanding its data center presence in the southeastern U.S. region, with major projects in South Carolina and Louisiana. Its South Carolina facility, located in the Sage Mill Industrial Park, is set for completion in 2027. In Monroe, Louisiana, Meta is building a nine-building campus, spread across an area of four million square feet (its largest to date); construction has been underway since December 2024 and will continue through 2030.

- The top markets in the Midwestern U.S. region include Ohio, Iowa, Illinois, and Missouri; these markets are preferred by major data center providers owing to the availability of renewable energy sources, strong connectivity, and tax incentives. In addition, the region has several Foreign Trade Zones (FTZs), Special Economic Zones (SEZs), as well as industrial parks that offer several incentives and tax reliefs.

- In November 2025, the data center development initiatives were officially banned in Lordstown, Ohio, following a vote by the Lordstown Village Council to approve an ordinance prohibiting all such proposals. The decision was prompted by a planned project from Bristolville 25 Developer LLC on a 133-acre site near Tod Avenue. This regulatory change can reduce investment in the mid-western region, potentially prompting operators to explore alternative locations for future development initiatives.

- The top markets in the southwestern U.S. region include Texas and Arizona, which are preferred by hyperscale & colocation operators owing to strong connectivity, renewable energy options, and tax incentives.

- In November 2025, Google revealed plans to develop two new data center campuses in Muskogee County, becoming part of a broader $9 billion investment in Oklahoma. The expansion will significantly augment Google’s presence in the state while supporting its rapidly developing technology and energy sectors.

- Top markets in the western U.S. region are Nevada, California, Utah, Oregon, and Idaho; these are preferred by major data center operators owing to good connectivity and proximity to IT hubs. In addition, the region has several FTZs, SEZs, and industrial parks, offering several incentives and tax reliefs. The cost of procuring land is higher in California than in other states in the western U.S. market.

- In March 2025, Goodman Group began construction on its LAX01 data center facility in Los Angeles, California, located on a 5.6-acre site in Vernon; the site previously housed the Farmer John meat-packing plant. Scheduled for completion by mid-2026, the three-story center will offer 32 MW of IT capacity. The company announced plans to raise $2.5 billion, with a part of the funds being intended to support its ongoing data center expansion.

- The northeastern U.S. region is a developing data center market. It includes states such as Maine, Massachusetts, Rhode Island, Connecticut, New Hampshire, Vermont, New York, Pennsylvania, New Jersey, Delaware, and Maryland.

- The demand for data centers in the New York-New Jersey market remains high. The expansion of the New York-New Jersey data center market can be attributed to the ongoing demand for data center space, thereby serving as a connectivity hub in the heart of New York City’s financial center.

U.S. HYPERSCALE DATA CENTER MARKET VENDOR LANDSCAPE

- U.S. hyperscale data center market has the presence of global as well as local IT providers such as Arista Networks, Atos, Broadcom, Cisco, DataDirect Networks, Dell Technologies, Extreme Networks, Fujitsu, Hewlett-Packard Enterprise (HPE), Hitachi Vantara, IBM, Intel, Infortrend Technology, Inspur, Lenovo, MiTAC Holdings, Micron Technology, NetApp, NVIDIA, Pure Storage, among Others.

- U.S. hyperscale data center market has the presence of key support infrastructure providers such as ABB, Caterpillar, Cummins, Delta Electronics, Eaton, Legrand, Rolls-Royce, Schneider Electric, STULZ, and Vertiv. These companies lead the market, driving advancements in power systems and cooling systems to ensure efficiency and reliability.

- The market is observing an increasing number of partnerships among data center operators, cooling technology vendors, chip manufacturers, and energy innovators. These collaborations are becoming essential for developing sustainable AI infrastructure. They facilitate the adoption of liquid cooling, hybrid thermal systems, and energy-efficient designs that support high-density computing while managing energy consumption and minimizing environmental impact. This is crucial for meeting the competitive demands and regulatory standards of modern data centers in the U.S.

- In November 2025, Carrier introduced a new lineup of Cooling Distribution Units (CDUs), designed for liquid cooling in data centers; these CDUs offer capacities ranging from 1.3 MW to 5 MW. This launch builds on the company’s earlier QuantumLeap suite, which includes chillers, air handlers, a liquid-cooling CDU, building management systems, and maintenance services for comprehensive data center thermal management.

- In November 2025, Switch and Schneider Electric signed an expanded $1.9 billion agreement, marking it as the largest data center cooling contract in North America. Under the supply capacity deal, Schneider Electric will provide prefabricated power modules and its Uniflair chiller systems for Switch’s facilities, with the chillers set to be used in the US for the first time.

- The market has a presence of key data center contractors such as AECOM, Ames Construction, Arup, Barge Design Solutions, Burns & McDonnell, Corgan, DPR Construction, Fortis Construction, Haydon, Holder Construction, Jacobs, KDC, Kiewit Corporation, Lewis Michael Consultants, Morgan Construction, Morgan Corp, Page, Rogers-O’Brien Construction, Rosendin Electric, Syska Hennessy Group, and Turner Construction. which provide construction, installation, engineering and commissioning services for the construction of data center facilities across the region.

- The market has key data center operators, including Apple, Amazon Web Services (AWS), CyrusOne, DataBank, Digital Realty, Equinix, Google, Meta, Microsoft, NTT DATA, and Vantage Data Centers.

- The market will witness new data center investor to investment in U.S. region, such as Ardent Data Centers, Ada Infrastructure, Beale Infrastructure, Big Sky Digital Infrastructure LLC, CleanArc Data Centers, CloudBurst Data Centers, Colovore, Crane Data Centers, Edged Energy, Fleet Data Centers, NE Edge, Penzance, Prometheus Hyperscale, Sailfish Investors, among others.

SNAPSHOT

The U.S. hyperscale data center market size is expected to grow at a CAGR of approximately 14.66% from 2025 to 2031.

The following factors are likely to contribute to the growth of the U.S. hyperscale data center market during the forecast period:

- M&A and Joint Ventures Enabling Data Center Construction Growth

- Tax Incentives are a Major Boost for Data Center Growth

- Enhanced Connectivity Through Submarine Cables Driving Growth in Data Center Market

- Acceleration of Cloud Infrastructure Uptake

Base Year: 2025

Forecast Year: 2026-2031

The report considers the present scenario of the U.S. hyperscale data center market and its market dynamics for 2026−2031. It covers a detailed overview of several market growth enablers, restraints, and trends. The study covers both the demand and supply sides of the market. It also profiles and analyzes leading companies and several other prominent companies operating in the market.

The report includes the investment in the following areas:

Segmentation by Infrastructure

- IT Infrastructure

- Electrical Infrastructure

- Mechanical Infrastructure

- General Construction

Segmentation by IT Infrastructure

- Server Infrastructure

- Storage Infrastructure

- Network Infrastructure

Segmentation by Electrical Infrastructure

- UPS Systems

- Generators

- Transfer Switches & Switchgear

- PDUs

- Other Electrical Infrastructure

Segmentation by Mechanical Infrastructure

- Cooling Systems

- Racks

- Other Mechanical Infrastructure

Segmentation by Cooling System

- CRAC & CRAH Units

- Chiller Units

- Cooling Towers, Condensers & Dry Coolers

- Economizers & Evaporative Coolers

- Other Cooling Units

Segmentation by Cooling Technique

- Air-based

- Liquid-based

Segmentation by General Construction

- Core & Shell Development

- Installation & Commissioning Services

- Engineering & Building Design

- Fire Detection & Suppression

- Physical Security

- DCIM/BMS Solutions

Segmentation by Tier Standards

- Tier I & Tier II

- Tier III

- Tier IV

Geography

- Southeastern U.S.

- Western U.S.

- Midwestern U.S.

- Southwestern U.S.

- Northeastern U.S.

IT Infrastructure Providers

- Arista Networks

- Atos

- Broadcom

- Cisco

- DataDirect Networks

- Dell Technologies

- Extreme Networks

- Fujitsu

- Hewlett-Packard Enterprise (HPE)

- Hitachi Vantara

- IBM

- Intel

- Infortrend Technology

- Inspur

- Lenovo

- MiTAC Holdings

- Micron Technology

- NetApp

- Nimbus Data

- NVIDIA

- Oracle

- Pure Storage

- Seagate Technology

- QNAP Systems

- Quanta Cloud Technology (QCT

- Supermicro

- Synology

- Western Digital

- Wiwynn

Key Data Center Support Infrastructure Providers

- ABB

- Caterpillar

- Cummins

- Delta Electronics

- Eaton

- Legrand

- Rolls-Royce

- Schneider Electric

- STULZ

- Vertiv

Other Data Center Support Infrastructure Providers

- Airedale

- Alfa Laval

- Asetek

- Bloom Energy

- Carrier

- Condair

- Cormant

- Cyber Power Systems

- nVent Data Center Solutions (Enlogic)

- FNT Software

- Generac Power Systems

- Green Revolution Cooling (GRC)

- HITEC Power Protection

- Johnson Controls

- Rehlko (KOHLER)

- KyotoCooling

- Mitsubishi Electric

- NetZoom

- Nlyte Software

- Rittal

- Siemens

- Trane

- ZincFive

- HIMOINSA (Yanmar)

Key Data Center Contractors

- AECOM

- Ames Construction

- Arup

- Barge Design Solutions

- Burns & McDonnell

- Corgan

- DPR Construction

- Fortis Construction

- Haydon

- Holder Construction

- Jacobs

- KDC

- Kiewit Corporation

- Lewis Michael Consultants

- Morgan Construction

- Morgan Corp

- Page

- Rogers-O’Brien Construction

- Rosendin

- Syska Hennessy Group

- Turner Construction

Other Data Center Contractors

- AlfaTech

- Aplena

- Black & Veatch

- Brasfield & Gorrie

- BlueScope Construction

- CallisonRTKL

- Clark Construction Group

- Clayco

- Climatec

- Clune Construction

- EYP MCF

- EMCOR Group

- Fluor Corporation

- Fitzpatrick Architects

- Gensler

- Gilbane Building Company

- Gray

- HDR

- Hensel Phelps

- HITT Contracting

- Hoffman Construction

- JE Dunn Construction

- JHET Architects

- JTM Construction Group

- kW Engineering

- Linesight

- M+W Group

- McCarthy Building Companies

- Mortenson

- Morrison Hershfield

- Pepper Construction

- Ryan Companies

- Salute Mission Critical

- Sheehan Nagle Hartray Architects

- Southland Industries

- Skanska

- Sturgeon Electric Company

- STO Building Group

- Sundt Construction

- Suffolk Construction

- The Weitz Company

- The Mulhern Group

- The Whiting-Turner Contracting Company

- The Walsh Group

- TRINITY Group Construction

- WSP

- Walbridge

Key Data Center Investors

- Apple

- Amazon Web Services (AWS)

- CyrusOne

- DataBank

- Digital Realty

- Equinix

- Meta

- Microsoft

- NTT DATA,

- Vantage Data Centers

Other Data Center Investor

- Aligned Data Centers

- American Tower

- AUBix

- CloudHQ

- Cologix,

- Compass Datacenters

- COPT Defense Properties

- Core Scientific

- Corscale Data Centers

- Crusoe

- Csquare

- DartPoints

- DC BLOX

- DigiPower X

- EdgeConneX

- EdgeCore Digital Infrastructure

- Element Critical

- fifteenfortyseven Critical Systems Realty (1547)

- Flexential

- H5 Data Centers

- HostDime

- Hut 8

- Iron Mountain

- Netrality Data Centers

- Novva Data Centers

- PhoenixNAP

- PowerHouse Data Centers

- Prime Data Centers,

- QTS Realty Trust

- Sabey Data Centers

- Skybox Datacenters

- STACK Infrastructure

- Stream Data Centers

- Switch

- T5 Data Centers

- TierPoint

New Entrants

- Ardent Data Centers

- Ada Infrastructure

- Beale Infrastructure

- Big Sky Digital Infrastructure

- CleanArc Data Centers

- CloudBurst Data Centers,

- Colovore

- Crane Data Centers

- Edged Energy

- Fleet Data Centers

- LightHouse Data Centers

- Lambda

- Metrobloks

- NE Edge

- Penzance

- Prometheus Hyperscale

- Quantum Loophole

- RadiusDC

- Related Digital

- Rowan Digital Infrastructure

- Sailfish Investors

- Tract

- WhiteFiber

U.S. HYPERSCALE DATA CENTER MARKET FAQs

How big is the U.S. hyperscale data center market in terms of investments?

What is the estimated market size in terms of area in the U.S. hyperscale data center market by 2031?

How much MW of power capacity is expected to reach the U.S. hyperscale data center market by 2031?

What is the growth rate of the U.S. hyperscale data center market?

Which region holds the most significant U.S. hyperscale data center market share?

For more details, please reach us at [email protected]

For more details, please reach us at [email protected]

Select a license type that suits your business needs

Single User Licence

- Report accessible by one user only

- Free 10% or 3 days of customization

- Free post-sale service assistance

- Continuous support through email

5 User Licence

- Report accessible by 5 users within the organization

- Free 15% or 4.5 days of customization

- Continuous support through email and telephone

- Free analyst hour

- Free Upgrade: If an updated report published within 180 days of purchase, you will get the revised report free of charge

Corporate Licence

- Free Datasheet worth $1500

- Report accessible by the entire organization

- Free 20% or 6 days of customization

- Free post-sale service assistance

- Continuous support through email and telephone

- Direct access to lead analysts

- Free analyst hour

- Free Upgrade: If an updated report published within 180 days of purchase, you will get the revised report free of charge

Datasheet Licence

- Report accessible by 1 user only

- Free 15% or 32 hours of customization

- Free post-sale service assistance

- Direct access to lead analysts

Frequently Asked Questions

How big is the U.S. hyperscale data center market in terms of investments?

What is the estimated market size in terms of area in the U.S. hyperscale data center market by 2031?

How much MW of power capacity is expected to reach the U.S. hyperscale data center market by 2031?

What is the growth rate of the U.S. hyperscale data center market?

Which region holds the most significant U.S. hyperscale data center market share?